Key themes and stocks discussed today:

- US markets were closed for a public holiday. This week, all eyes will be on the labour market, the August Non-farm payrolls, and the unemployment rate due to the drop on Friday morning. This data point will determine whether the Fed goes with a 25—or 50-bps cut in two weeks’ time. September could be a choppy month, with earnings forecasts too high for the quarter. Having some powder set aside for these seasonally weaker months is prudent.

- JP Morgan is leaning toward being more cautious and noted this week that “at the market level, we looked for the consolidation through summer, on slowing activity, lower yields, and the risk of concentration unwind. While SPX recovered of late…JPM believes that markets are not out of the woods yet. September has seasonally been a challenging month for equities. I continue to see a second leg to the corrective selloff that began early last month.

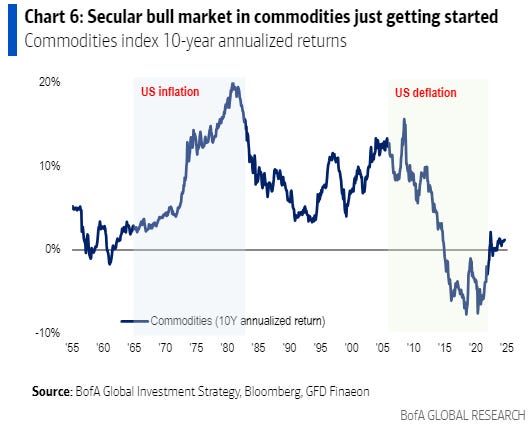

- Bank of America believes that the secular bull market in commodities is only just getting started.

- In Australia, GDP will come in tomorrow and is expected to show the slowest growth since 2021. Meanwhile, the economy is doing it tough. I see the first rate cut from the RBA being no later than Xmas.

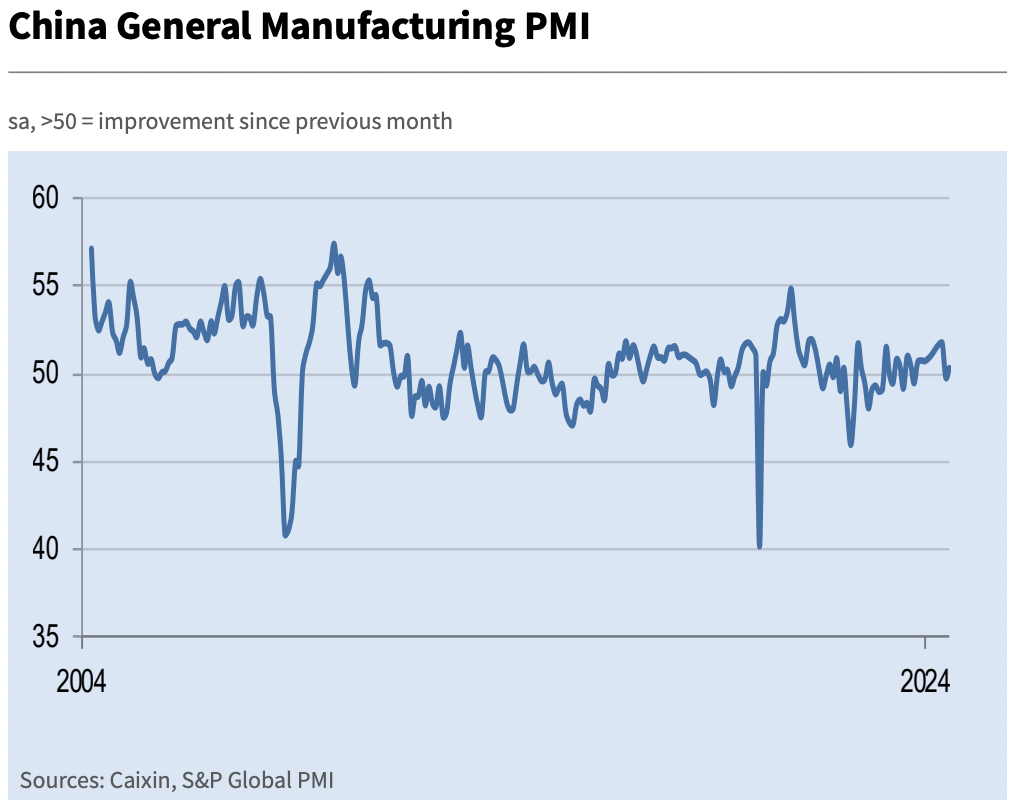

- Conflicting manufacturing data weighed on Greater China stocks, with the Hang Seng beginning September trading on the back foot, interrupting a nearly +4% rally in August.

- Japanese benchmarks crept higher, supported by advances from financials and transportation stocks.

- UK benchmarks dipped on Monday amid quiet trading due to the US holiday. This was despite a “Buy British” note from Goldman Sachs and some notable M&A news. European benchmarks were mixed as the manufacturing sector continued to struggle. Political news from Germany also ruffled a few feathers.

- Notable charts and stock mentions today include the S&P500, FTSE250, Antofagasta, REA Group, Barratt Developments, Kainos, Rio Tinto, 29Metals, REA Group, CBA, Viva Energy, Red 5, Bellevue Gold, China Vanke, Japanese banks, and Yaskawa Electric.

US markets were closed for Labor Day on Monday, but futures markets point to a slight gain when trading resumes tomorrow. This week, the big focal point for the markets will be the August non-farm payrolls print, which is due to drop on Friday morning. The key labour market data will be influential, given last month’s growth scare narrative and ahead of the September FOMC meeting, when the Fed is expected to deliver the first-rate cut.

Will it be 25 bps or 50 bps? The state of the labour market will play a key role here. A weaker or hotter-than-expected print will likely determine whether the Fed runs with 25 or 50 bps.

We could also see some volatility as we head into September as volumes pick up with the Northern Hemisphere summer over. September and October have historically been seasonally weak, so pruning portfolios and carrying some extra cash is prudent. October could also be choppy given the uncertainty around the US election and a closely run race.

Resistance at the SPX’s record highs is likely to prove a barrier as we enter the seasonally weaker months of September and October. A retest of the early August lows between 5100 and 5200 would not surprise. However, once the election is out of the way, the SPX could lead global stock markets higher into new record territory for a strong finish to the year.

However, I expect a strong finish in the stock markets running into year-end when the election is out of the way. [stu alias=”buying_british_made”]

Statistically, the US and international stock markets typically rally strongly after the election outcome. Buying the September or October lows has also worked well in most years, with one notable exception being the GFC in 2008 (the market bottomed in March 2009).

JP Morgan is also leaning into being more cautious and noted this week that “at the market level, we looked for the consolidation through summer, on slowing activity, lower yields and the risk of concentration unwind. While SPX recovered of late…We are not out of the woods yet. September has seasonally been a challenging month for equities. The Fed will start easing, but more in a reactive way and as a response to weakening growth – this might not be enough to drive a next leg higher.” This is a fair point, and any doubt around the predominant soft-landing narrative (such as less hiring and rising unemployment) would likely mark a return of volatility. The corrective selloff last month likely has “a second accompanying leg”.

JPM also cited valuation in the US is not cheap and that “profit margins are peaking, topline growth is weakening, while net interest expense is set to move back up.” I also see downside risks to earnings forecasts, which are too high. JPM highlighted this point on Monday, citing that 2024 SPX EPS forecasts, calling for 11% profit growth re-acceleration, “are at risk of further downgrades. At 21x, the US forward P/E is very stretched, especially vs real yields…among International markets, we stay bullish on Japan and UK, relative to Eurozone and EM.” Valuation is more compelling outside the US, and we will therefore likely see markets such as Australia, UK, and Japan hold up better during any selloff. China and Hong Kong are also screening cheap despite deeply negative sentiment.

Bank of America is upbeat on commodities and sees a secular bull market playing out between now and the end of the decade. In a note on Friday, BOA cited that “a structural rise of inflation suggests the commodity bull is just starting. Commodities such as oil and gold have long been considered reliable inflation hedges, and investors will demand them more if inflation makes a return.” While inflation is presently headed down, I fear other forces could see it make a return next year. The weakening US dollar could be one potential catalyst that boosts inflation and commodity demand another in the coming years.

BOA said, “Commodities could generate annualized returns of 11% as debt, deficits, demographics, reverse-globalization, AI and net zero policies are all inflationary. Those potential returns mean commodities represent a better asset class to allocate”. BOA also likes gold, which has been a particularly strong force driving the solid performance of the commodities sector this year.

Turning to Australia, the debate continues to heat up around the state of the economy and when the RBA will move with the first rate cut. There is now clear evidence that economic growth has completely stalled, while futures markets are pricing the cuts to go in by November. This is at odds with the narrative from the RBA, which is leaning towards next year.

There is no question that the economy is doing it tough, and we are seeing this play out with weaker earnings, especially in the retail and hospitality sectors. Wage growth is also slowing, although we have yet to see unemployment climb. However, I expect this to soon happen in the months ahead. Meanwhile, the high cash rate is biting into discretionary income and driving a retail recession. The key GDP data set is due on Wednesday, which will provide a window into how tough the economy is faring.

PM Anthony Albanese backed up comments from Treasurer Jim Chalmers over the weekend when he said that the “combination of global uncertainty and interest rate rises are smashing the economy, and it would be no surprise at all if the national accounts on Wednesday show growth is soft and subdued”.

NAB senior economist Brody Viney said the challenging profitability environment for consumer-facing industries was consistent with business surveys, which show confidence at its weakest among employers in the retail and wholesale trade sectors. “The wider picture from the business indicators release remained one of subdued activity”. The consumer slowdown was also very evident in the recent ASX 200 profit reporting season.

While RBA deputy governor Andrew Hauser last week reinforced that the RBA will not follow the Fed and ease monetary policy this year, slowing growth, rising unemployment, and falling inflation over coming months will galvanise the case for rate cuts by year-end.

Yesterday, the ASX200 recovered from shallow losses in morning trade to close +0.18% higher at 8,109, only five points below the all-time record high achieved in late July. Banks extended a YTD rally to do most of the heavy lifting, with support from some energy stocks offsetting losses for many miners as traders digested more economic data from China. SPI futures are pointing to a flat open.

While there was some local data, nothing moved the needle. The final reading for the Judo Bank Australia Manufacturing PMI was revised marginally lower to 48.5 for August (initial estimate: 48.7). Still, it remained in contraction, albeit modestly improved from the 47.5 reading in July. Incoming new orders and production remained in contraction, though export orders expanded at the fastest clip in a couple of years.

Building permit approvals jumped 10.4% monthly to a seasonally adjusted 14,797 units in July, rebounding from the 6.5% fall in June and easily topping expectations for a 2.5% increase. Finally, the ANZ Job Ads data showed a 2.1% monthly decline in August, extending a streak of declines since February. I expect upcoming data to show the widening cracks in the local job market.

The big banks extended their YTD rally, with CBA rising another +1.6% to a fresh record high of $141.77. ANZ +0.9%, Westpac +1.2% and NAB +1.3% followed close behind, with the XBK (bank sub-index) up +1.3% to be the day’s best performer. These gains came as last Friday’s US inflation data bolstered the case for rate cuts by the Federal Reserve beginning at this month’s meeting.

The energy sector followed closely, buoyed by decent performances from Woodside +1.4% and Santos +1.1%. Ampol +2.4% and Viva Energy +2.4% added support.

Coal miners were more subdued, with Whitehaven Coal edging up 0.5% and New Hope Corporation gaining a modest 0.7%. Uranium players were mostly lower, with Paladin Energy -1.9% and Boss Energy -3.9% below water at the close.

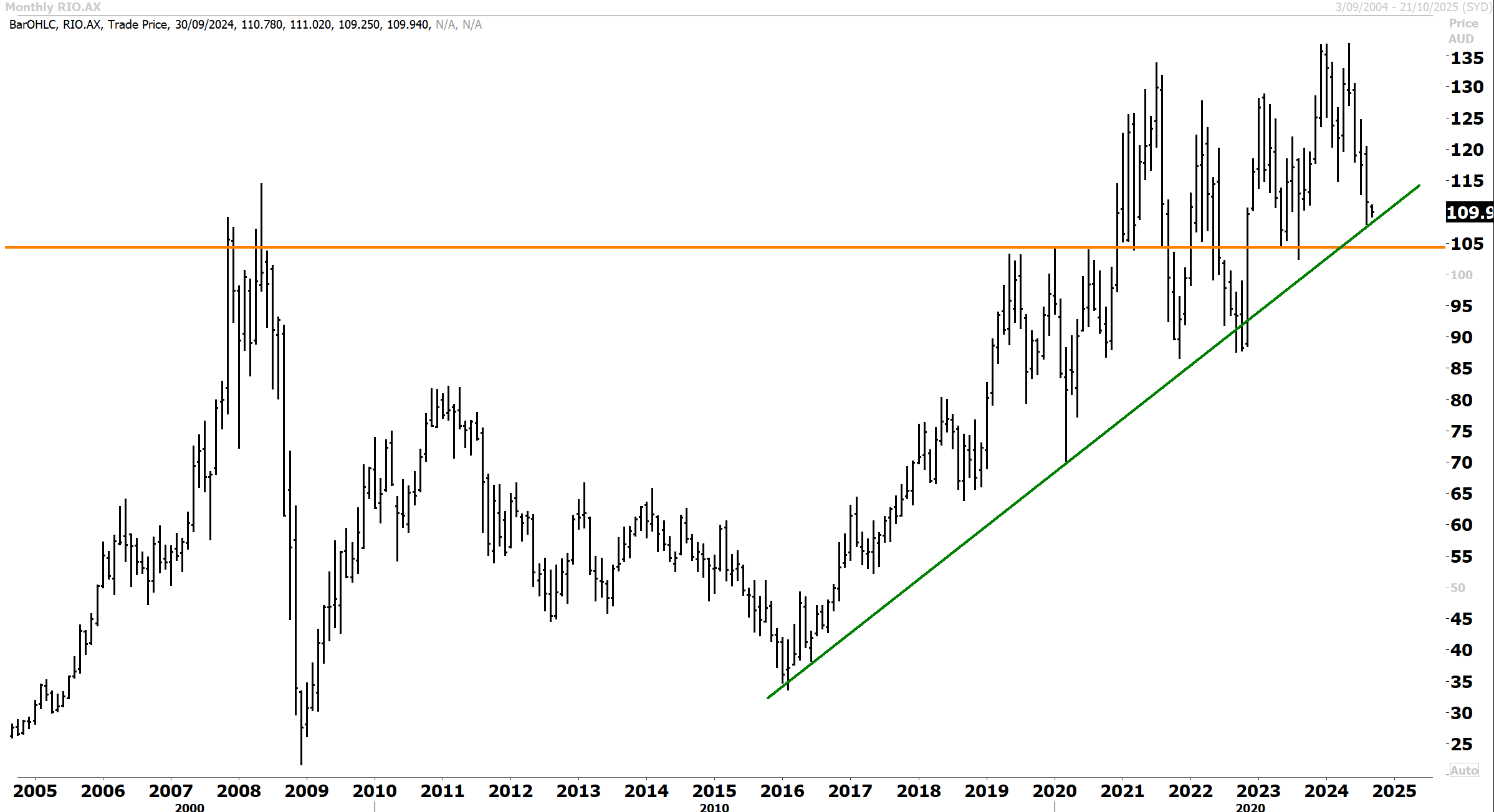

The materials sector struggled due to concerns over China’s economic health. Iron ore futures in Singapore dropped roughly 3% to around $US98 per tonne, dragging on BHP -1.1%, Rio Tinto -1.4%, and Fortescue -0.5%. Rio posted a solid set of full-year numbers during the August reporting season and has some growth projects set to contribute in the coming years.

In our last technical update on 17th August, we highlighted that “Our base case technical outlook for Rio remains unchanged. The stock remains within a consistent uptrend and has found support at $116 following the recent corrective pullback. The technical setup continues to skew to the bull side, with a resumption in upward momentum and an eventual retest of the resistance level at the record highs anticipated over the coming year.”

The correction in Rio has been steep, but the shares are now finding support. Rio has consistently respected the primary uptrend and historical support at $105/$109. Our technical outlook for Rio remains unchanged. When the incumbent consolidation phase is complete, upward momentum should resume, favouring a retest of the record highs over the coming year.

Gold miners had a rough day due to the soft lead from US$ gold prices. Evolution Mining fell -3.1%, Northern Star Resources dropped -1.1%, Red 5 tumbled -7.4%, St Barbara slid -5.9%, and Bellevue Gold plunged -9.1% (more on Bellevue below). Red 5 looks oversold here, given the benefits of the merger with Silver Lake. Lower copper prices hurt 29Metals -5.3% and Sandfire -0.5% to a lesser extent. 29Metals reported improved 1H24 numbers last week, and the stock is highly leveraged to the copper price.

In our last technical update back in July, we highlighted that “A sustained breakout in 29 Metals above 50 cents has not yet materialised, and the stock has corrected lower to consolidate below the primary uptrend. However, 29M remains well off the intra-year lows, with a retest of the primary downtrend anticipated sometime this year. Our base case technical outlook is that once a breakout is confirmed, there remains significant scope for upside recovery, with a $1/$1.20 handle being plausible in the coming years.

Our anticipated breakout above 50 cents has proven elusive as the copper sector has broadly corrected lower. 29M however looks to finding support at 35 cents while copper spot prices consolidate. We anticipate 29M to resume higher once copper prices also reassert to the topside. A topside breakout above resistance and the primary downtrend at 50 cents would confirm an inflection.

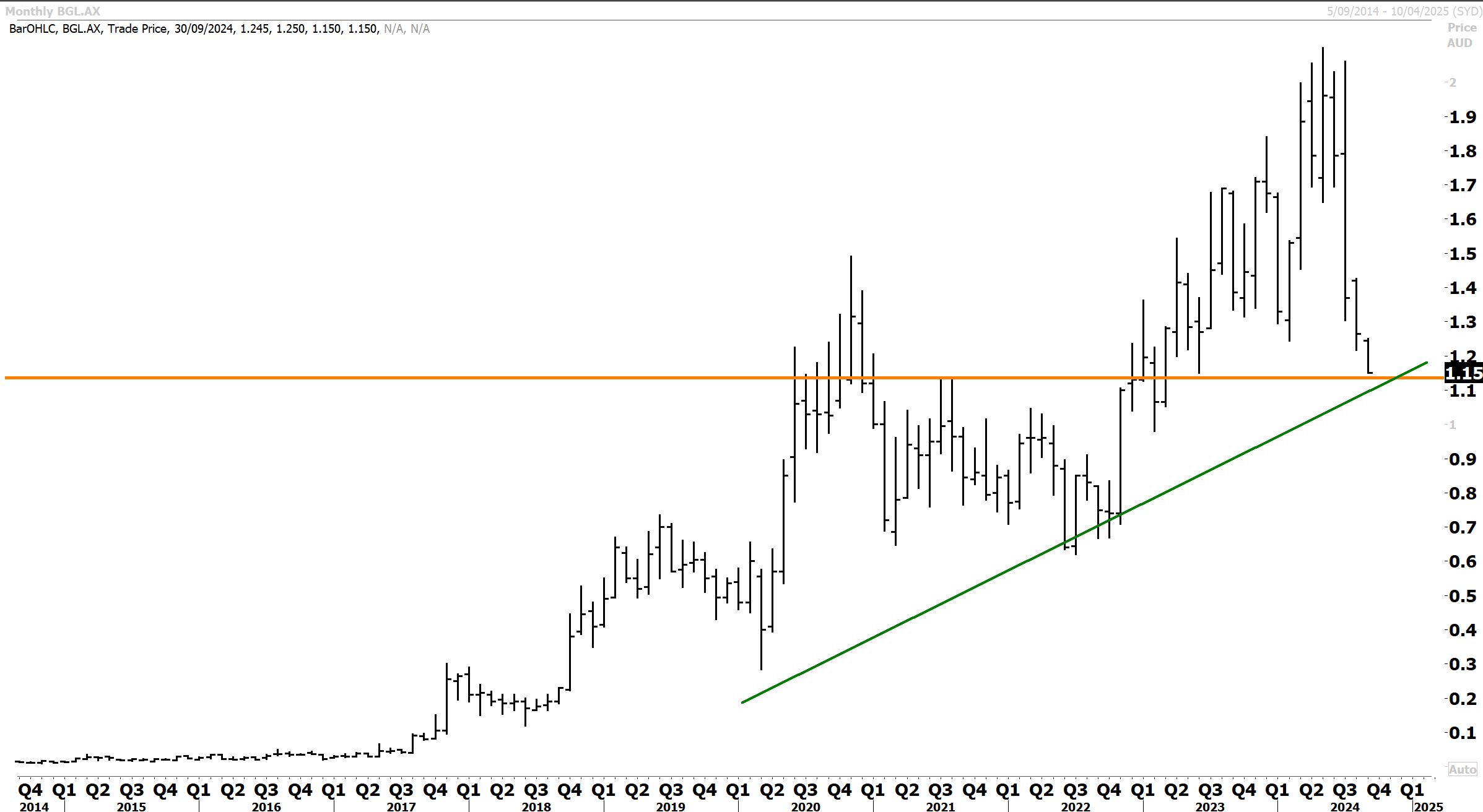

On other corporate news, while reporting season ended last Friday, there will be a smattering of reports over the coming weeks. Bellevue Gold slumped -9.1% despite FY24 results confirming a maiden net profit of $75 million, aligning with expectations. The Bellevue Gold Mine in WA started commercial production in May and poured 42,705 ounces for the June quarter. FY25 guidance is for 165-180k gold ounces production at an attractive AISC of A$1,750-1,850/oz.

Bellevue Gold has corrected sharply after making a record high above $2. The shares now look to be finding support at the primary uptrend at around $1.10.

REA Group slid -5.3% after confirming it is considering a cash and share bid for UK-listed Rightmove. Smartgroup rallied +5.4% after broker Morgans upgraded the stock to a buy rating. This optimism followed solid half-year results released last week. Imugene jumped 9.7% after announcing some results from an early-stage Phase 1b trial of its cancer treatment.

Turning to Asia, China’s CSI 300 fell 1.7%, while the Hong Kong benchmark slid 1.65%. An official report revealed that China’s manufacturing sector contracted for the fourth straight month, and soft reports from banks and property developers dampened sentiment, interrupting the Hang Seng’s almost 4% upward run in August.

The official manufacturing PMI purchasing managers’ index (PMI) dropped to 49.1 in August from 49.4 in July, missing the consensus forecast of 49.5. On the other hand, the private Caixin survey painted a more upbeat picture, with a headline reading of 50.4, improving from 49.8 in July. This indicated a slight expansion, driven by improved new orders. This latter survey is shown below:

In Hong Kong trading, property developers tumbled after New World Development issued a profit warning, and China Vanke reported its first interim loss in two decades. New World fell -13% to the bottom of the Hang Seng, while China Vanke fell -6.9%. China Overseas Land & Investment -4.7% and Longfor Group -3.9% were down on the read-across.

Industrial and Commercial Bank of China (ICBC) -2.% and China Construction Bank (CCB) -1.6% fell after reporting weaker first-half profits.

Consumer-facing companies like Nongfu Spring -5.5%, Budweiser APAC -4.6% and Li Auto -4.6% skidded lower. Big tech stocks were red, with Alibaba -2.4%, Kuaishou Technology -2%, JD.com -2% and NetEase -1.9% leading the group south.

A small group of advancers included Xinyi Solar +3%, China Resources Power +1.2%, and hotpot chain Haidilao International +0.3%.

In Japan, the Nikkei +0.14% and Topix +0.12% posted slight gains, supported by a softer yen, although some profit-taking capped overall gains. Transportation equipment and financial stocks posted decent advances. If US economic data continues supporting the soft-landing narrative, benchmarks will likely extend higher.

The yen traded around the mid-146 range late afternoon, while the 10-year JGB yield rose 1.5bps to 0.905%. Daiwa Securities +2.7%, Mebuki Financial +2% and Concordia Financial +1.9% led financials higher.

Other notable advances were convenience store operator Seven & I, semiconductor giant Advantest and Toyota +0.7%. Touch screen sensor expert Nissha Co added +2.3%, and industrial automation and robots firm Yaskawa Electric gained +1.7%.

Pharmaceutical stocks featured among the retreating group, led lower by Sumitomo Pharma -6.1% and Chugai Pharma -6.1%.

London’s benchmarks closed in negative territory on Monday, as trading activity was dampened by the closure of US markets for the Labor Day holiday. The FTSE 100 edged down by 0.15% to finish at 8,363 points, while the more domestically focused FTSE 250 shed – 0.5%.

UK manufacturing is showing resilience, with the final reading for the S&P Global Manufacturing PMI revised upward, reaching 52.5 in August compared to 52.1 in July. August’s reading was the highest in over two years. The sector has expanded in five of the last six months. The strength in manufacturing was mainly attributed to domestic demand, as export orders continued to decline—a trend that has persisted since early 2022. Rob Dobson of S&P Global highlighted that while the domestic market is buoyant, challenges such as weaker European demand, a slowdown in China, and global uncertainties hinder growth.

It was interesting to see a Goldman Sachs note titled “Buy British,” which highlighted UK equities’ undervaluation and strategic appeal, particularly within the context of global diversification. The note outlines several points that underscore the attractiveness of the UK market, which I have touched on previously.

This includes the valuation discount. UK stocks, especially those listed on the FTSE 100, are trading at a significant discount compared to their US counterparts. Despite a robust performance in 2024, London-listed stocks have experienced a decade of underperformance, reducing the UK’s weighting in the MSCI World Index from 5.3% in 2010 to just 2.2%. This reflects a materially different composition, with few large-cap tech stocks in the UK. The heavy weighting in sectors like financials, energy, mining, healthcare, and consumer staples makes the UK market defensive and potentially less volatile.

With its greater domestic exposure, Goldman believes the FTSE 250 stands to benefit from a stronger pound and improving UK economic conditions. This index, where around 50% of revenues are generated within the UK, is particularly appealing in the current macroeconomic environment, where inflation is stabilising and consumer confidence is rising. Additionally, policy initiatives from the new Labour Government, such as pension reviews and efforts to boost homebuilding, could further support UK equities.

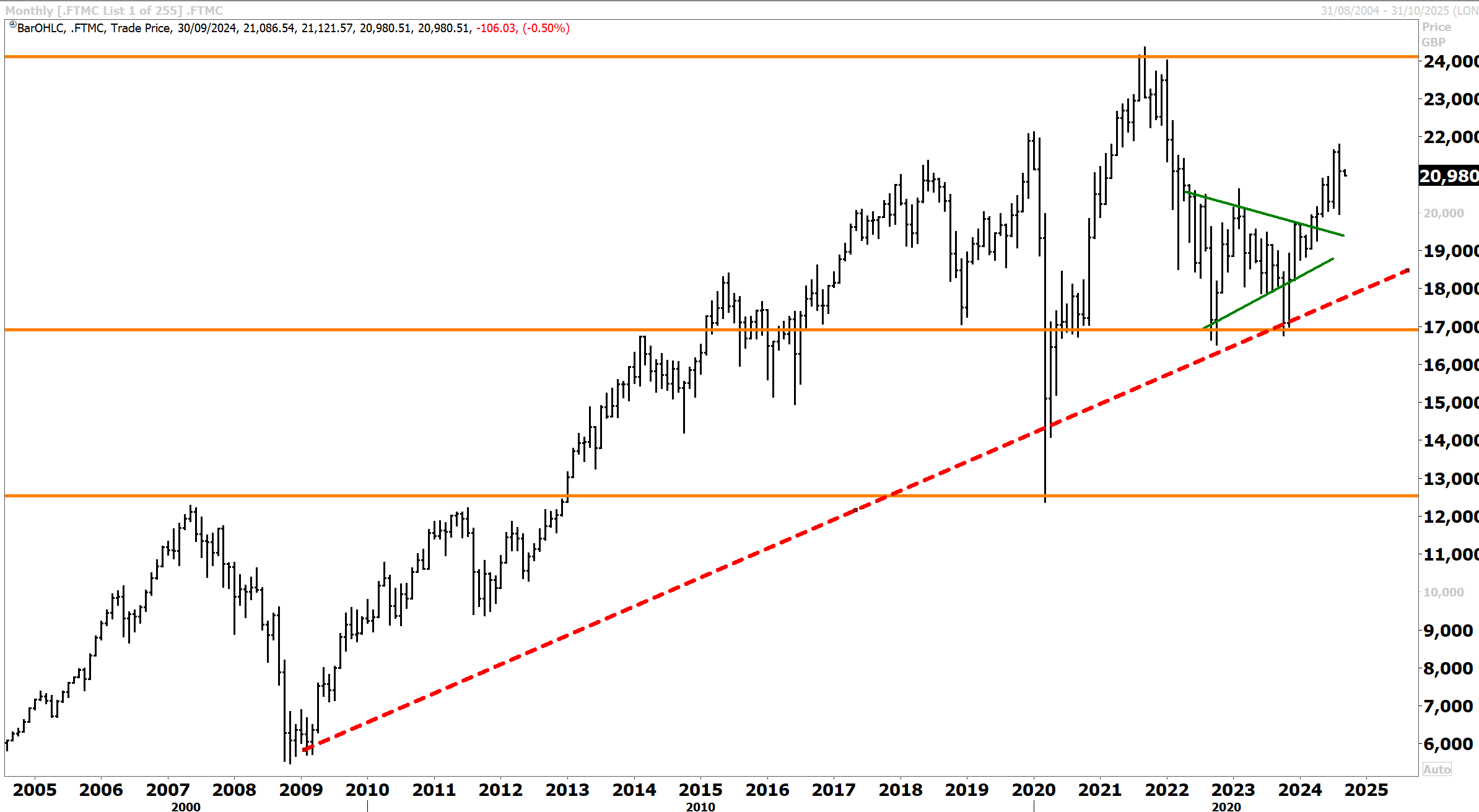

The FTSE250 index has remained within a primary uptrend since the lows at 6000 were established back during the GFC. The FTSE250 has corrected since the 2021 record high above 24000 and traced at a double bottom at 17000. The index has since broken above near-term resistance and is reasserting on the topside, with a retest of the record highs anticipated over the coming year.

UK equities have benefited somewhat in 2024 from being seen as a safe haven, offering both income and stability. The high dividend yield and the potential for capital appreciation make UK stocks an interesting proposition.

On that note, UK stocks have seen substantial inbound M&A over the past few years. This continued on Monday. Online property platform Rightmove surged +27.4% to the top of the FTSE 100 table on the news that Australia’s larger market-cap REA Group is mulling a cash-and-scrip offer, although no formal approach has been made. REA has a long track record of acquisitions and now has until the end of September to make a formal bid after publicly disclosing an interest. Rightmove dominates the UK online property portal market, and its market cap shot higher to around £5.6 billion. Online auto classifieds leader Auto Trader advanced +3.1% on the read-across.

Barratt Developments advanced +3.1% after UBS upgraded its rating to ‘buy’, indicating renewed investor confidence in the UK housing market. Bodycote gained +1% after receiving a ‘buy’ rating from Berenberg.

Kainos Group plummeted by -14% after issuing a profit warning, citing a challenging trading environment and delays in client projects. Rolls-Royce -6.5%, BAE Systems -2.5% and Carnival -2% were some other decliners.

Antofagasta’s -0.6% 1H profits took a hit as expected, with pretax profit dropping 7% to $712.6 million due to lower sales volumes and higher depreciation. Firm copper and gold prices helped lift revenue by 3.6% to $2.955 billion. Management remains optimistic about the future, reaffirming full-year production guidance and ramping up capital expenditure to $2.7 billion to expand key operations, signalling confidence in copper’s long-term trajectory.

In our last technical update back on August 8th, we highlighted that “Antofagasta has corrected sharply in line with copper spot prices back towards support at the 1900p level, which is encouragingly looking to hold. Following the pullback, consolidation above support is now well underway, and we anticipate upward momentum to soon return to Antofagasta. Our base technical case remains for the record highs to be challenged again in the year ahead.”

Antofagasta has consolidated above support at 1800p, which is the breakout level in line with the broader correction in spot copper prices. The technical setup still favours a resumption of upward momentum and a retest of the record highs above 2400p over the coming year.

On the continent, regional bourses were mixed amid subdued trading due to the US market holiday and general caution ahead of the looming US non-farm payrolls report later in the week. The Eurozone’s manufacturing sector continued to struggle, with the PMI for August remaining in contraction territory at 45.8, albeit a slight upward revision from the preliminary estimate of 45.6. This marked the 26th consecutive month where the PMI has been below the neutral 50-point mark.

In Germany, markets opened with a bearish tone following the weekend’s local elections in the eastern state of Thuringia, where the far-right Alternative for Germany (AfD) party won 32.8% of the vote. This was the first time a far-right party had won a state election in Germany since World War II, sparking concerns about the country’s political stability and its implications for economic policy. Nevertheless, stocks recovered, and the DAX closed +0.13% higher.

At the close, the pan-European Stoxx 50 was up +0.3%, while France’s CAC 40 added +0.2%. Italy’s FTSE MIB retreated -0.15%, while Spain’s IBEX 35 dipped -0.06%.

Carpe Diem!

Angus

Disclosure: Fat Prophets and its affiliates, officers, directors, and employees may hold an interest in the securities or other financial products relating to any company or issuer discussed in this report. Fat Prophet’s disclosure of interest related to Investment Recommendations can be provided upon request to members@fatprophets.com.au.

Chart Source: Thomson Reuters