A bumper start

Agribusiness, Elders (ASX.ELD) has seen its shares continue to climb and virtually deflecting the headwinds caused by COVID-19. The fact that people still need to eat despite being holed up in their homes due to the pandemic has been a boon for Elders along with its peers but improving weather conditions and a bumper season gave the sector a solid boost. Today, we take a look at the latest round of results and update our view.

Remove term: FAT-AUS-1020

Remove term: FAT-AUS-1020 What’s new?

The last time we checked in on the agribusiness giant was back in November (FAT-AUS-996) where we saw the company report an solid performance at the end of fiscal 2020 unscathed from the COVID-19 pandemic. The pandemic has been one of the most disruptive events in recent history with many businesses across sectors suffering, with agriculture seemingly one of the exceptions. This is evidenced by Elders sending the year with an impressive 29% surge in revenues and underlying earnings per share surging 35% year-on-year.

Since then, the company has issued another round of results which we review today to see how it has measured up since. Prior to that, we want to highlight some key expectations for the sector which was based on the March 2021 release of the Australian Bureau of Agricultural and Resource Economics and Sciences noting that they expect 2020-21 season to be the “second most profitable season ever for Australian farmers.” It seems that the drought that has affected the sector in recent history has subsided with better conditions and higher than average rainfall pushing expected cash incomes up 18% – and that’s for the average farmer.

With such a bullish outlook, we now take a look at Elders to see if it’s up to compete:

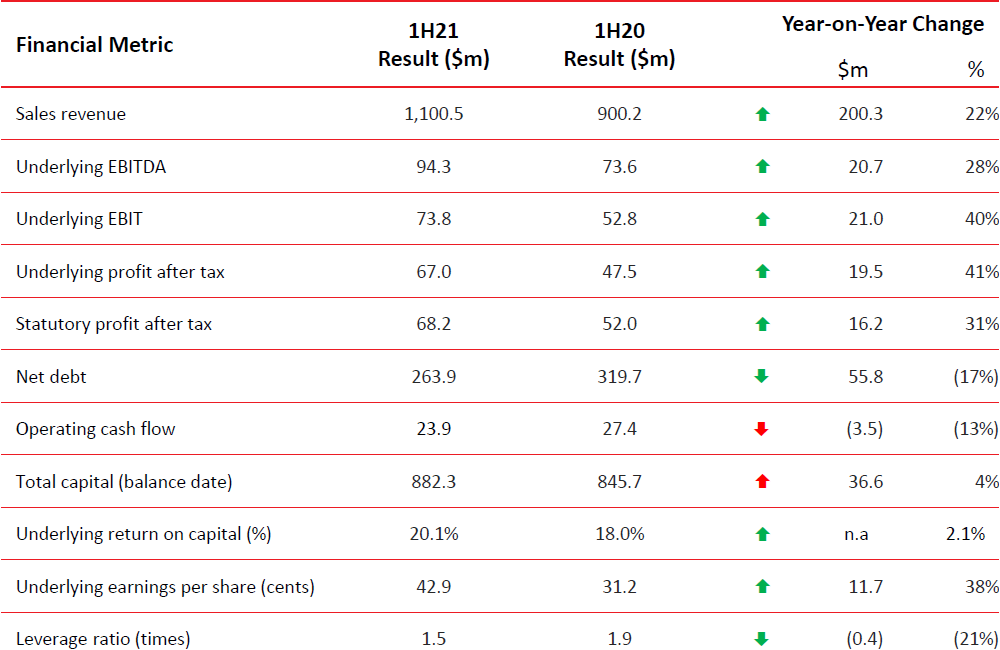

1H21 Results Overview

Starting from the top and revenues in 1H21 surged up 22% year-on-year to $1.1 billion, reflecting the improving conditions in Australia as well as management efforts to diversify the business model by geography, channel and product category – the diversification typically balances out the good with bad, however, this time all divisions benefited. We’re pleased to see that agriculture was one of the sectors showing to be largely resistant from the disruptive effects of COVID-19 with demand for agricultural products remaining strong (people still need to eat after all).