2022; payback

With 2022 just a few days from entering the history books, we look back at the year that carried many twists and turns with inflation and central banks playing key roles. The pandemic year of 2020 and recovery year of 2021 are now well in the history books, with the ‘payback year’ an appropriate label for 2022. Australia and the ASX200 were not immune from the key influencing metrics of inflation and the Reserve Bank (RBA) in 2022, along with the Federal Reserve influencing global sentiment. The following chart shows the year-to-date (YTD) performance of the ASX200:

Source: google

The ASX200 lost 5.8% YTD, dropping to 7,148 at the time of writing, but has however outperformed the S&P 500 YTD. The S&P 500 also weakening over 2022 by 19.7%, driven primarily by the recalibration of a very overvalued tech sector. The ASX200 was held up by the financials with the ASX200 financial index losing just 1.7% YTD, while the ASX200 materials gained 3.3% YTD, to turn in a very good performance for the year. The ASX200 Energy index was a notable performer, adding 35.85% YTD. Consumer discretionary felt the pain of the inflationary environment and RBA action, as did Consumer staples, reporting falls of 19.9% and 5.8% respectively. The tech sector, like its US peer, on valuation pressures fell a whopping 32% YTD. The gold sector was also on the backfoot, losing YTD 9.15% as a rising US dollar stifled the gold price and with this the sector.

The Real Estate index was a notable decliner on the interest rate headwinds. The following chart shows the YTD performance of the ASX200 Real Estate index:

Source: Marketindex

The rising fear of a recession, rising cost of living pressures and property valuation compression, on rising interest rates, all had a compounding impact on the sector to turn it into a major underperformer for the year.

Across 2022, we remained well weighted to the financial sector with buys across Australia and New Zealand Bank, National Australia Bank and Westpac on strong balance sheet strength and the positive impact of rising interest rates on their net interest margins. Regionals Bank of Queensland and Suncorp were also buys over the year for similar reasons as the three big banks, while being major players in the lucrative Queensland market.

Materials also remained in focus over 2022, with BHP, Rio Tinto and Fortescue Metals all recommended as buys across the year. The following chart shows BHP’s YTD share price:

Source: google

The iron ore price YTD has fallen 8.0%, to US$112 a tonne, on China’s Zero COVID policy disrupting growth in that country and dislocating the workforce. A late in the year loosening of this policy, and on a populous revolt, brought relief to the iron ore price and lifted it off the US$80 lows reached earlier in the year. Investor fears of the policy entrenching in 2023 eased on this softening. China has also been countering the damaging impact of its COVID policy on the economy in 2022 with selective stimulatory activities.

Exposures were maintained in South32 (base metals), Sandfire Resources (copper) and Mincor Resources (nickel), on specific positive thematics around the sea change occurring in the auto industry and global climate change. China remained a thorn, as the country adhered, across the majority of 2022, to a strict Zero COVID policy. Lockdowns across the country unsettled markets throughout 2022 on demand concerns. As with iron ore, a late waylaying of the policy fear entrenching in 2023 lifted base metal prices.

Our exposure to Real Estate was confined to BWP Trust, National Storage, Scentre Group, Stockland and Vicinity Centres. All are quality exposures in the real estate sector with long-term value metrics to sustain the rotation of interest rate tightening cycles and easing ones. Satellite staff continues to hinder demand for office space as workforces have yet to fully return to the workplace. These exposures were maintained as holds over 2022.

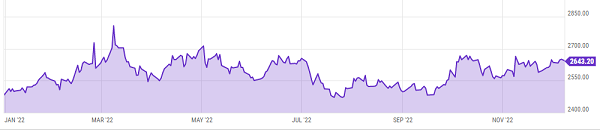

Our gold exposures were heavily tilted toward Australian dollar producers, where the benefit of a weakening Australian dollar impacted positively on their financials. The following image shows the Australian gold price (in ounces):

Source: YCharts

The Australian dollar gold price rose over 2022 adding 6.4% YTD to be trading at A$2,643.20 an ounce. Although our exposures saw some share prices fall, we maintained a buy bias across the year on revenues for the sector remaining robust and balance sheets very strong. There will be some margin compression, as costs have risen across the year, with the likes of Evolution Mining shedding 31.9% YTD on this compression fear and growth concerns, while Northern Star Resources added 13.2% YTD on the Aussie dollar gold prices and a sound growth profile.

We remained positive over 2022 on Telstra (TLS), with its strategy to go digital and restructure its tower assets. The following chart shows TLS’s YTD share price:

Source: google

TLS is the dominate player in the Australian telecommunications sector and uses this dominant position to good effect with product and service offerings. TLS saw its share price fall a modest 4.0% YTD. Our other key exposure in the telecom space in TPG telecom (TPG) was moved to a hold mid-year on a poor interim report. TPG has struggled in the trading environment to maintain traction, despite moving to digital platforms.

There were four new arrivals into the portfolio over 2022, with Beston Global Food (Beston) bought in May 2022, while the other three were bought in the second half of 2022. The following chart shows the YTD share price for Beston:

Source: google

Beston was brought into the portfolio as a specialist dairy product producer and premium food distributor. The company undertook a recapitalisation during the year and we view Beston as a turnaround opportunity. Integral Diagnostics is a major radiology provider whose share price has compressed on operational headwinds. We took advantage of the depressed share price to bring in a well-run and strategy focussed operation, facing the aging population thematic. Ansell came into the portfolio on its stable business in safety protection solutions. Putting the COVID period behind it, Ansell shows all the signs of a classic recovery as demand for its product offerings return to normal. A strong global presence is driving sales and will continue to do so in the years ahead. Worley Energy (Worley) offers services to the resources sector, including engineering, project delivery and consulting services. The $15.4 billion of forward contracted work is a major attraction in Worley, as is its ability to turn this work into future revenue.

Ten full or half sales were completed in 2022 and these can be viewed in our report titled ‘Where we took Profits and Losses’ published with our 2022 year in review.

2022 brought with it a change of stance by the RBA to a cash rate tightening cycle on the back of inflation running rampant after a year of excessively easy monetary and fiscal policies. Meanwhile, a very strong US dollar brought winds for Australia, playing havoc with commodity prices. All of this was couched in a war that commenced early in 2022 with Russia invading the Ukraine.

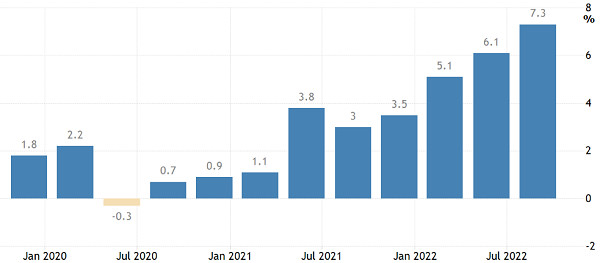

Inflation became the menace of 2022, as the excessive easing and stimulatory policies of 2020/21 came to roost in prices over the year. The following chart shows quarterly changes in annual CPI for Australia:

Source: TradingEconomics

As Members can see from the above chart, inflation accelerated over 2022 to hit an annual rate of 7.3% and hit the highest level since the early 1990’s. The inflation rate has moved well above the RBA’s target of maintaining inflation in a range of 2% to 3%. The prospects of inflation continuing to rise, with the December quarter read expected to be the peak at around 8.0%, remains a daunting task for the RBA to bring under control. The December 2022 quarter read may prove to be the peak in Australia’s inflation with forecasts for it, as commodity prices have especially softened late in 2022, to ease to around 4.0% by the end of 2023. The RBA however remained committed, in 2022, to bringing inflation down. Supply chain disruptions continued to play a role in impacting inflation in 2022, including China’s Zero COVID policy. These pressures were however easing as 2022 draws to a close, as logistics in a post COVID world started to normalise.

Australia was not alone on this front, with the inflationary “genie being let out of the bottle” across most developed nations in 2022, with predicable central bank reactions in raising cash rates.

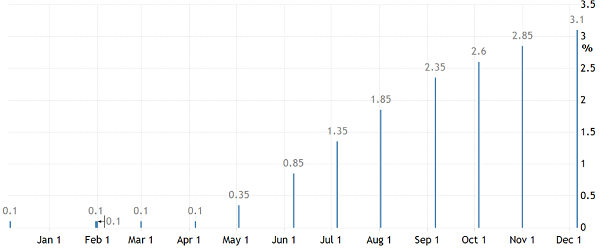

In the face of this pricing onslaught, the RBA reacted accordingly to regain control of inflation with the only real weapon in its arsenal and that is raising cash rates. The following chart shows the rise and rise of Australia’s cash rate over 2022:

Source: TradingEconomics

Starting 2022 at just above zero, the RBA lifted its official cash rate, and swiftly, to 3.1% following a decade of cash rates falling. After initiating a 25 basis point cash rate increase to commence the current rate tightening cycle, the RBA moved to the unprecedent step of raising cash rates by incremental 50 basis point increases for the next four monthly meetings. The goal of the RBA is to slow Australia’s economy, with markets concerned that the swift interest rate hikes may induce a recession in Australia. Many of the other major developed economies are in the exact same position, but at varying severity levels, as Australia.

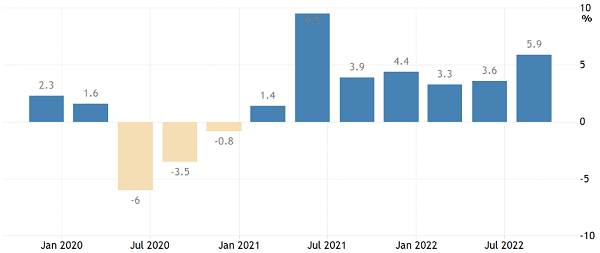

Despite the efforts of the RBA to slow Australia’s economy, the September 2022 quarter Gross Domestic Product (GPD) read shows an acceleration. The following chart shows quarterly changes in Australia’s GDP:

Source: TradingEconomics

As Members can see from the above chart, Australia’s GDP continued to expand at 5.9% for the September 2022 quarter, while expectations were set at a 6.2% expansion. As cash rate increases have a laggard effect on the economy, GDP numbers are yet to show any material effect. A slowing relative to consensus may be the first tentative signs of what is to come.

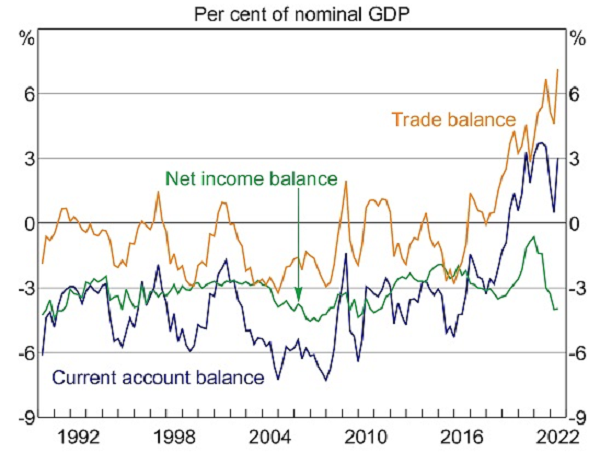

Driving Australia’s GDP success has been its external performance, with a very strong export performance. The following chart shows the export sectors (Trade Balance) contribution to Australia’s GDP performance together with net income:

Source: Australian Bureau of Statistics

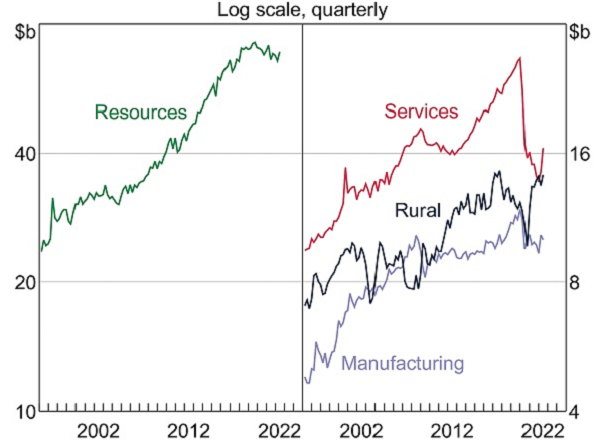

Resources performed strongly over 2022, with iron ore, coal, natural gas and the rural sector swelling Australia’s export coffers. Meanwhile the services and manufacturing sectors have reported a slowing in their contribution to Australia’s external position. The following chart shows the contribution, by volume, of key sectors of Australia’s economy (in Australian dollars):

Source: Australian Bureau of Statistics/RBA

The added performance of the resources and rural sectors staved off a recession in Australia in 2022. Both sectors, unfortunately for the RBA and its efforts to control inflation, performed independently of what is happening inside the Australian economy.

Australian manufacturing has shown the first signs of slowing in 2022, following the excessive growth years of 2020 and 2021. Constant bottlenecks in logistic chains, tight labour conditions including a lack of a workforce and wage pressures have all brought pressure on Australia’s manufacturing base in 2022. Added headwinds came from the RBA moving to a rate tightening cycle.

Australia’s manufacturing sector has coped with the vagaries of the 2022 trading environment. We will not know how well or otherwise until the December reporting season gets underway in February 2023. Companies listed on the Australian Stock Exchange (ASX) have throughout 2022 initiated major share buyback programmes. The following table shows a selection of share buyback programmes initiated in 2022:

Source: AFR

These buyback programmes certainly reflect the confidence ASX listed companies have in their outlooks and finances. The quantum and spread of ASX companies undertaking buyback programmes has certainly been a major positive over 2022. Buybacks will have a positive bearing on corporate earnings reports.

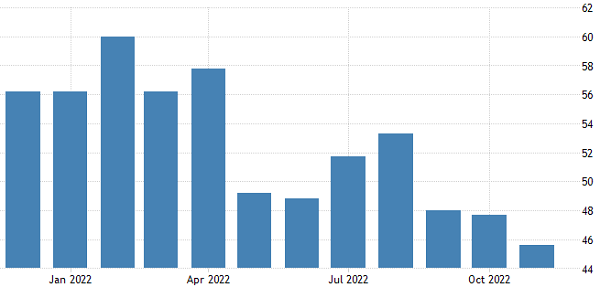

The Services sector has certainly recovered from the COVID support and physical spending withdrawals by governments during 2022. The Services sector has directly benefited from pent up demand in the population and the call on a considerable pool of COVID savings, estimated at A$140 billion, now winding through the economy and especially directed at the entertainment component. The following chart shows Australia’s Services Purchasing Managers index (PMI):

Source: TradingEconomics

As Members can see from the above chart the Services sector PMI is in contraction with reads over the past three months below the 50 growth/contraction threshold, with the November read the lowest at 45.6. The impact of this pool of savings is waning ln late 2022, as real wage growth remains negative, the cost of living is rising and debt servicing and especially mortgage debt is rising.

The ”R” word raised its head in 2022, from the quiet whispers heard in 2021. Market commentors are now loudly calling the European Union (EU) and the United Kingdom (UK) will enter a recession in 2023 and are likely in the early stages already. For the EU, the Ukraine and Russian war and the disruptions to energy supplies will herald a recession, along with the broader slowdown in global economic activity. The UK has experienced rising interest rates, as the Bank of England moved to control inflation in 2022 and a hard landing scenario has ensued.

The chorus of voices has added the United States (US) to the 2023 list to face a recession and it too may also be in the first stage of one already, although this is heavily debated, and it is certainly not a ‘typical’ recession given continued strength in the jobs market and consumer spending. Like the UK, the swift rise in the cash rate over 2022 has raised the spectre of a hard landing scenario in the US, with most market commentators now expecting this eventuality.

The “R” word remains a little more hushed in Australia in 2022, despite the RBA’s action to slow the economy by lifting rates. The latest GDP number is certainly no reflection of such an event occurring. Antidotally, data reads coming out late in 2022, point to a slowing Australian economy but a hard landing recession scenario has yet to gain market traction. The strong showing of Australia’s external performance under the umbrella will help stave off a recession in 2022.

An unforeseen war with Russia invading the Ukraine in early 2022, although not directly impacting Australia, the effect on coal, natural gas and grains pricing was significant. Russia and the Ukraine are major grain producers and the war brought sky-rocketing grain prices. Russia weaponised, by blocking Ukraine exports of grain, and western nations sanctioned Russian grain. Via a negotiated agreement grain started making its way out of Ukrainian ports later.

Natural gas and coal, with Russia a major supplier of each, saw prices spike on western sanctions. Both commodities are key Australian exports and underpinned along with iron ore Australia’s export performance over the majority of 2022. As the war drags on, changed supply and production patterns trended toward the normal and the early pricing volatility slowly dissipated over 2022.

The impact of COVID in 2022 was modest. Although it remains present in the community, its impact, because of successful inoculation programmes, has become a pandemic Australia is learning to live with.

The tribe has spoken

If the results from our Member Survey for 2022 are any indication, our stock recommendations, in combination with our big picture analysis, continue to be appreciated.

The daily email from Angus Geddes is a vital part of our communication with Members and a channel through which Fat Prophets provides clarity on our views on macro and micro-economic developments, and the implication for stock markets. The daily email was separately graded and received an ‘A’. This is a testament to the value placed on his daily note by many Members.

Our efforts on the Australian Equities research service have also been awarded an ‘A’ grade from Members for 2022. This is a pleasing result, given the many continued challenges the markets faced this year and was the same as 2021. As usual, there was plenty of dispersion with comments and constructive feedback. This gives us areas to improve upon in 2023.

Our weekly research webinars continue to be well received. These sessions give Members the chance to hear direct from the Fat Prophets team. The forum style with a Q&A session at the end has also been a great way for us to engage with Members and the feedback here continues to be positive. Our weekly podcasts in 2022, where founder and CEO Angus Geddes discusses the issues penned in his daily communiques have also been well received by Members. Members also remain receptive towards our weekly fatWRAP which summarises the ideas from across Fat Prophets suite of research products. We continue to put plenty of thought into our covers and design, so it is pleasing that feedback here remains positive.

Our Income Portfolio continues to have a following from those seeking a steady dividend, considering the abysmal offerings for cash in the bank, despite rate increases. We review the Income Portfolio quarterly and on the income side, it had a return to 26 September 2022 of 26.8% and it should be noted that this is an average income return. The average forward yield for the Income Portfolio stocks stood at 4.8% for 2022 and 5.7% for FY23 which are solid projected yields, given the forward yield for the ASX200 for 2022 was 4.4% and for 2023 4.2%. The average 12-month fixed bank offering was 3.6% at 26 September 2022. A re-rating in share price values saw the total return on the portfolio come in at 44.8% versus 51.4% at our last update.

We will be publishing our Bakers Dozen predictions for 2023 in two parts, with the first in the week beginning 2nd January 2023, and the second in the week commencing 9th January 2023. As usual, these predictions will cover a range of topics.

Signing off for 2022 and we would like to once again, thank all Members for their continued support and wish all a safe and happy Christmas and a prosperous New Year.

Best regards,

Fat Prophets

Disclosure: Interests associated with Fat Prophets hold shares in BHP, Rio Tinto, South32, Sandfire Resources, Mincor Resources, Evolution Mining, Northern Star, BWP Trust, National Storage, Scentre Group, Vacinity Centres, Stockland Group, Westpac, Australia and New Zealand Bank, National Australia Bank, Bank of Queensland, Telstra, Fortescue Metals and Beston Food Group.