RIOJuly 21, 2020 FAT-AUS-980

Rio Tinto

2Q20; iron ore to the fore

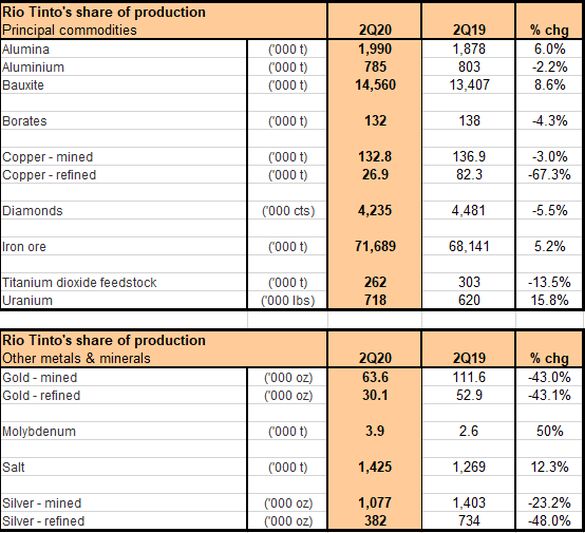

Rio Tinto has reported its operational results for the second quarter to 30 June, and despite what has been a challenging, COVID-19 driven global environment, we consider the overall result as reasonable Rio Tinto’s key operational segment in iron ore was the standout for the quarter, as was bauxite and mid-stream alumina. Copper and aluminium were again thorns for the quarter, on lower production numbers, with a majority of Rio Tinto’s minor product offerings also reporting softer outcomes. Pleasingly, guidance for 2020 remained unchanged across all of Rio Tinto’s product offerings. The following table is a synopsis, by commodity, of Rio Tinto’s operational results for the June quarter:

Source: Rio Tinto

The step-up in iron ore production, given Rio Tinto’s reliance on it, is the reason for our satisfaction with the result for the quarter. Bauxite was again a bright spot for Rio Tinto, on the back of another solid performance with alumina also adding a little more value to the aluminium segment. Unfortunately, the finished product for the segment, in aluminium, again disappointed. Copper again delivered a disappointing quarterly result, with Rio Tinto, it appears, yet to fully get on top of this segments ongoing operational issues. Overall, we view the operational result as reasonable and expect it will, thanks to iron ore, have a small positive impact on Rio Tinto’s first half result for 2020. Rio Tinto will report its first half financial result to 30 June 2020, on 29 July 2020.

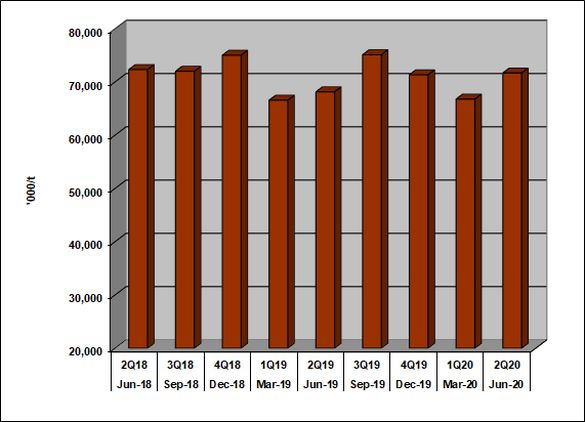

Rio Tinto’s key commodity offering is iron ore and it delivered a good result for the June quarter. The following chart shows quarterly iron ore production:

Source: Rio Tinto

The segment delivered a 5.2% rise in production year-on-year (yoy), to 71.7 million tonnes. The Hamersley mines (Rio Tinto must purchase 100% of the iron ore produced from these mines) was the driver, with the group of mines delivering a 6.2% yoy increase, to 53.2 million tonnes. Operational availability and efficiencies, on better third-party demand drove the result.

Iron Ore Company of Canada (Rio’s interest 58.7%, IOCC) reported a rise in production for the quarter of 9.1% yoy, to 2.8 million tonnes of concentrate and pellets. An improvement in utilization levels, on better third-party demand, drove the result.

Rio Tinto kept its 2020 guidance for iron ore unchanged with a forecast in the range of 324 million to 334 million tonnes (100% basis). IOCC guidance for 2020 was also unchanged with a forecast in the range of 10.5 million to 12.0 million tonnes.

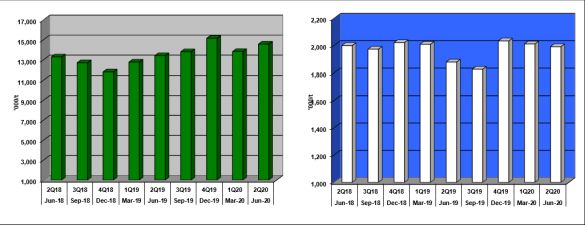

The aluminium segment delivered two bright spots for the June quarter, reporting better upstream and mid-stream performances. The following charts show quarterly production for both bauxite (left chart) and alumina (right chart):

Source: Rio Tinto

Up-stream bauxite production increased by 6.0% yoy, to 14.6 million tonnes. Rio Tinto’s Weipa operation drove the result, following the reporting of a 9.7% yoy increase, to 9.4 million tonnes. Driving the result were productivity improvements and infrastructure availability. Including Weipa, Rio Tinto reported increased production from three of its four sites for the quarter, with only its Porto Trombetas mine (Rio’s interest 12%) delivering a fall.

[pms-restrict subscription_plans=”9,10″]

Mid-stream alumina production for the June quarter also came in higher by 6.0% yoy, to 2.0 million tonnes. Rio Tinto reported higher alumina production across all four of its refineries for the quarter, with its three key sites all reporting better quarterly numbers. The standout was Sao Luis (Rio’s interest 10%), following the reporting of a 9.3% increase yoy, to 945,000 tonnes. Queensland Alumina (Rio’s interest 80%) and Yanwun delivered yoy increases of 6.6% and 8.3% respectively, to 889,000 tonnes and 820,000 tonnes.

On 2020 guidance, bauxite production is forecast to be in the range of 55 million to 58 million tonnes and alumina in the range of 7.8 million to 8.2 million tonnes, with both unchanged.

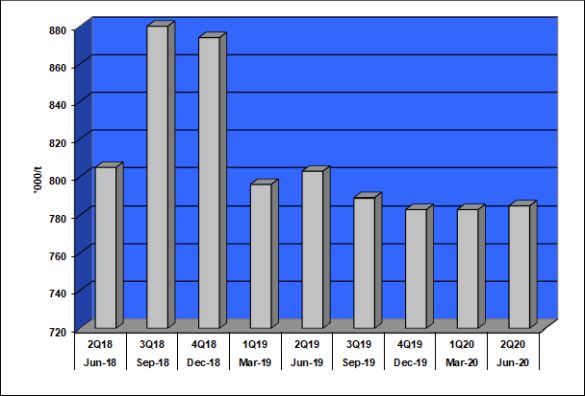

Disappointing was downstream aluminium, following the reporting of a fall in production for the quarter, with the segment again failing to deliver. The following chart shows quarterly aluminium production:

Source: Rio Tinto

The segment reported a fall of 2.2% yoy, to 785,000 tonnes of aluminium for the quarter. Rio Tinto’s six wholly owned Canadian smelters drove the result, with the reporting of a 7.5% fall yoy in production, to 370,000 tonnes. Infrastructure availability was the primary driver of the result. The Becancour smelter (Rio’s interest 25%) was a bright spot, as it successfully ramps up, with the reporting of a 550% yoy increase in production, to 26,000 tonnes. At the other extreme, Rio Tinto has announced the closure of its New Zealand smelter, on operating cost grounds, and will wind down operations over the next 14 months. The Tiwai Point smelter (Rio’s interest 79.4%) contributed 82,000 tonnes to the segments June quarter. The results from its remaining aluminium smelters, for the quarter, were generally flat to marginally higher.

Production guidance the aluminium for 2020 remained unchanged and is forecast to be in the range of 3.1 million to 3.3 million tonnes.

The challenges faced by Rio Tinto’s copper segment have returned, with both mined and refined copper production numbers falling for the quarter. The segment has proven, like aluminium, to be difficult to manage.

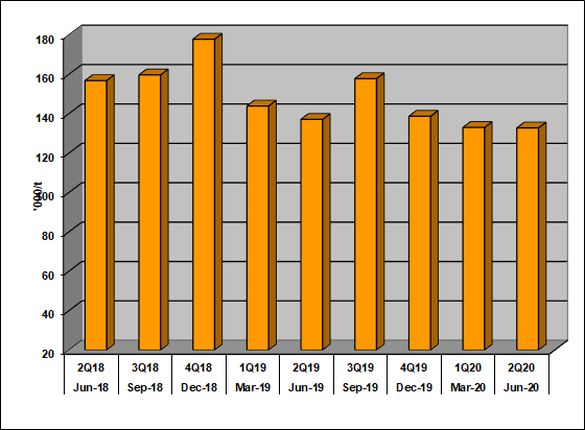

Refined copper production headed the copper segments’ charge in the June quarter. The following chart shows quarterly refined copper production:

Source: Rio Tinto

Production of refined copper fell by 67% yoy, to 26,900 tonnes. The Kennecott operation drove the result, reporting an 89% fall in production yoy, to 7,200 tonnes. An earthquake caused the suspension of operations during the quarter, with the mine now heading back to normal operational levels. Rio Tinto’s other remaining site in Escondida (Rio’s interest 30%), reported a flat operational result of 19,700 of refined copper for the quarter, compared to 19,000 tonnes from a year earlier.

Pleasingly, refined copper production guidance for 2020 remained unchanged and is forecast to be in the range of 165,000 tonnes to 205,000 tonnes.

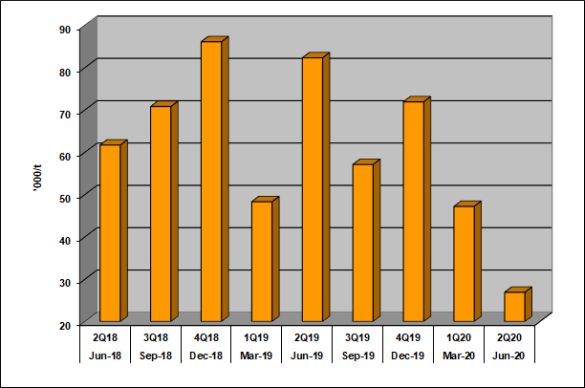

Mined copper also came in lower for the June quarter. The following chart shows quarterly mined copper production:

Source: Rio Tinto

The Bingham Canyon mine (part of the Kennecott operation0 was the primary driver after delivering an 11.25 fall yoy in production, to 36,500 tonnes. Mine sequencing and lower copper grades impacted the June quarter numbers. Escondida partially offset the Bingham Canyon mine performance, with the reporting of a 1.6% yoy increase in mined copper, to 84,000 tonnes. Oyu Tolgoi reported a modest fall in mined copper production for the June quarter, to 12,200 tonnes from 13,100 tonnes from a year earlier.

Mined copper production guidance for 2020 was unchanged and is forecast to be in the range of 475,000 tonnes to 520,000 tonnes.

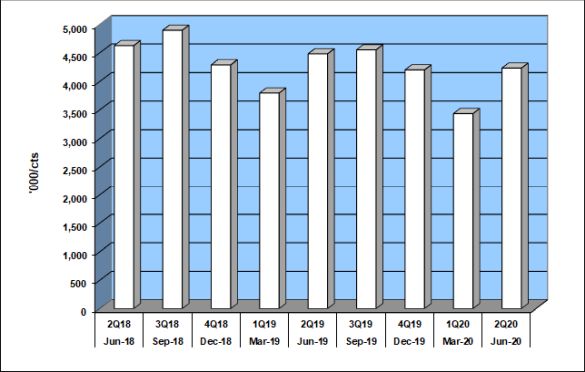

Diamonds turned in a lower result for the June quarter 2020, following the printing of a 5.5% fall yoy, to 4.2 million carats. The following chart shows quarterly diamond production:

Source: Rio Tinto

The Diavik mine (Rio’s interest 60%) reported a fall of 18.9% yoy, to 963,000 carats and was the primary driver behind the lower result. Lower diamond grades drove the Diavik result. The Argyle mine reported a flat performance of 3.27 million carats for the June quarter compared to 3.29 million carats from a year earlier. Argyle operated as expected, however activities to cease production, on end-of-mine-life, by end 2020 are ongoing.

Guidance for diamond production in 2020 is forecast to be in the range of 12 million to 14 million carats and remained unchanged.

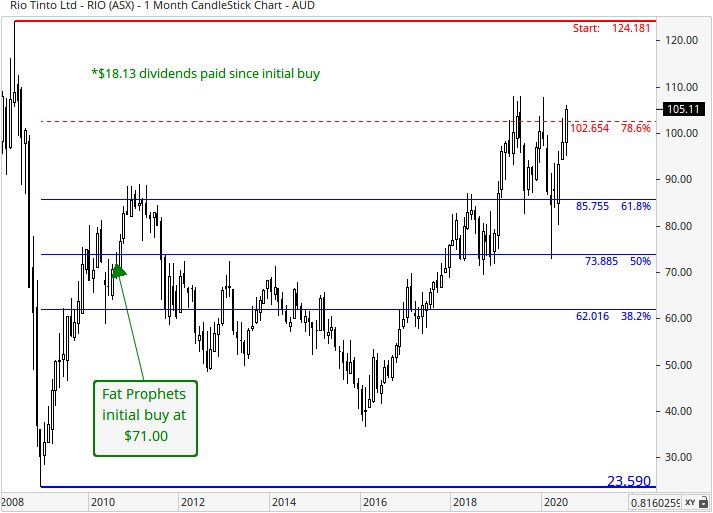

Turning to the charts and looking at the daily chart, our move back to a buy on Rio in early April has since coincided with a strong rebound in the share price. Resistance levels at $82.42 and $87.25 have been successfully probed, while that at $93.95 and more recently $103.27, have also fallen. A strong move above the red 50 day (red) and 200 day (green) averages adds to the positive picture, and a bullish moving average crossover (where the 50 day goes above the 200 day) is also forming. Our prediction a few months ago that ‘triple digit’ prices would return for Rio has proven on the money.

Looking at the monthly chart and Rio Tinto has made strong headway since 2016, taking out the 38.2%, 50%, and 61.8% Fibonacci retracements in the process. Support at $85.75 held up well during the Covid crisis, and a sustained move above the 78.6% Fibonacci retracement at $102.65 could well be in the offing.

Of Rio Tinto’s minor product offerings, gold, both mined and refined, reported significantly lower production numbers for the June quarter. Mined and refined gold production fell 43% each yoy, to 63,600 ounces and 30,100 ounces respectively. Rio Tinto reported lower numbers across all three of its gold producing sites in Bingham Canyon, Escondida and Oyu Tolgoi, on lower gold grades and the same factors that impact on primary metal production.

Exploration expenditure came in at US$136 million for the June quarter, representing a yoy fall of 16.6%. Central exploration consumed approximately 44% of the amount spent, copper and diamond exploration consumed 41%, energy and minerals 10%, with the remaining 5% spread across iron ore and aluminium. We believe Rio Tinto has enough Tier 1 assets that can generate future brownfield growth, without having to spend significant exploration dollars. Our view on this advantage has remained the same for some years and reflects the quality of Rio Tinto’s asset base.

We expect iron ore prices will be supportive over the remainder of 2020 and certainly beyond, when it comes to Rio’s financials.

We take comfort in Rio Tinto maintaining its 2020 guidance numbers and are of the view that its operations will have a modestly positive impact on the interim result, to be released on 29 July 2020.

Despite the recent rally in Rio Tinto’s share price, we believe the momentum is building in the broader economy, as government throw dollars at their economies. The ripple effects of infrastructure building will impact on commodity demand not just in 2020, but well into the years that follow. Consequently, our recommendation for Rio Tinto as a buy for Members with no exposure remains unchanged.

Disclosure: Interests associated with Fat Prophets holds shares in Rio Tinto.

[/pms-restrict]