Silver lining

Monday’s (24 November) gains have been a relief on Wall Street after volatility returned in November as investors questioned whether the AI boom might be morphing into a bubble. There have also been concerns around the US economy after a prolonged government shutdown denied markets of key data, which is only now resuming. The S&P 500 and Nasdaq were headed for monthly losses in November and the steepest declines since the April Liberation selloff.

The correction was badly needed in my view, with stock markets showing signs of overheating after what has been a stellar run since the April lows. Conditions had become quite overbought, and positioning was extreme. Many traders and hedge funds sitting on large year-to-date gains became worried before the December 31st cutoff and acutely dialled back risk and squared up positions. Many hedge funds are now running with much lower positioning and much higher cash balances. This is a positive outcome, and sets markets up for a strong finish in December in my view, especially after the strongest US earnings quarter in four years.

The S&P500 appears to be finding support at the bottom of the trend channel following a 5% corrective pullback. Time will tell, but the recent inflection higher is encouraging. We maintain a bullish outlook for the SPX benchmark in December and into the new year.

Against this backdrop, US and global benchmarks could finish strongly in December, and a Fed rate cut would be the icing on the cake. A number of major banks have lifted their 2026 forecasts. Deutsche Bank raised its price target and expects the S&P500 to hit 8,000 by December next year, citing resilient corporate earnings and AI-driven gains. UBS Securities’ trading desk now thinks the selloff in US stocks might have run its course, especially with Fed rate cuts back in play next month.

Chris Murphy, a strategist at Susquehanna, said that “I believe the combination of a reset of the equity market and the increased odds of a rate cut in December has propelled stocks higher and put the year-end melt-up back on the table.” He might well be right.

They join Morgan Stanley’s CIO Mike Wilson (who pivoted to being more bullish last week), who said on Bloomberg yesterday that “a bout of withering volatility in stocks over the last few weeks might be a blessing”. Mr Wilson said that he sees a silver lining in the tech-led selling in stocks, as it’s “building the case for Fed rate cuts into 2026. The Fed will eventually have to signal a clear path for interest rates to come down. The markets will dictate the Fed’s timing. Markets are like children, right? They have a little temper tantrum, and then the Fed will respond to that.”

In his Monday update, Mr Wilson noted that liquidity concerns have helped spark recent selling in stocks as investors protest weaker odds of rate cuts. Declines in momentum stocks and crypto could eventually create enough financial stress that the Fed will have to respond by either lowering interest rates or using its balance sheet tools, such as quantitative easing.

“Importantly, any volatility driven by liquidity concerns in the market should be a buying opportunity. We would view a Fed and liquidity-driven correction and reset on expectations as an opportunity to double down on our rolling recovery thesis, which remains very much out of consensus.” I concur with these views, and we added to equity positions in recent weeks throughout the November tremors.

Mr Wilson believes that markets could be in for a repeat of the dynamic that played out in 2018. Wilson pointed to the sell-off that ensued at the end of that year, after the Fed hiked interest rates and struck a more hawkish tone than investors had expected. The central bank began a fresh quantitative easing cycle the following year that drove a big rebound rally.

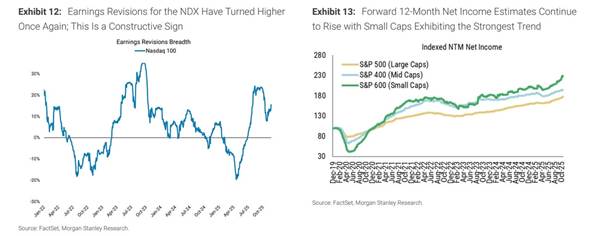

Morgan Stanley also believes the market is flashing other positive signals that could begin a fresh move higher going into next year. “The job market is softening, which supports the case for Fed rate cuts. Earnings revision breadth for the Nasdaq 100 is rising, and forward net income estimates for the S&P 500 are also climbing. We think there’s this sort of tug-of-war going back and forth, but ultimately it results in a more dovish policy path”.

Source: FactSet/Morgan Stanley Research

Morgan Stanley and Mr Wilson’s outlook on the US economy and the stock market has decisively shifted from bearish to bullish in recent years. Morgan Stanley recently lifted its 12-month S&P 500 price target to 7,800, implying another 16% upside. “The economy looks like it’s rebalancing toward the private sector. The US economy and corporate earnings are in the midst of a rolling recovery. Bottom line, we have high conviction in our bullish 12-month stance. Any weakness is an opportunity to add long-term investments to their portfolio going into the next year.”

At the risk of sounding like a stuck record player, I also believe the setup for markets into next year is bullish following the November setback. Institutional investors and hedge funds remain cautious and are hesitant about adding risk. Retail equity flows and persistent demand continue to act as a price setter of equities. Retail equity volumes are the highest since February 2021. Corporate buybacks are resuming following the earnings season blackout, which is adding incremental demand.

After the recent de-grossing and factor rotations by many fund managers, discretionary portfolios remain potentially underexposed to an upside move. We could well see institutional fund managers chasing the market higher in December and January if the Fed surprises with a rate cut.

The October/November volatility spike has likely already peaked and topped out at above 28 after being tested on two occasions. Sequentially, the VIX could subside quickly over the coming months and slip back into a range between 15 and 20 as confidence returns to the market.

Lastly, following the November shakeout, investors have become quite pessimistic and bearish – but this has been accompanied by an absence of negative catalysts following one of the strongest reporting seasons in four years.

The AAII Bull/Bear ratio now skews on the pessimistic side, which also sets the market up for a decent rally in December/January.

Moving on, UBS’s leading China property analyst John Lam, a longtime contrarian, has dialled back his earlier bullish calls that the country’s four-year real estate downturn is over. Mr Lam said in a Bloomberg interview that he expects home prices to fall for at least another two years before a recovery in China’s beleaguered residential property market can take hold. One reason cited was that potential buyers are increasingly opting to rent properties while prices are declining.

“People who bought homes in the past decade may all be loss making. This has fundamentally changed housing price expectations.” Mr Lam has turned more cautious on China’s housing market just months after he predicted that home prices could “turn stable in early 2026, led by a revival in top-tier cities”.

Mr Lam famously called the top of the Chinese property market and downgraded leading developer Evergrande at the beginning of 2021, before house prices began falling.

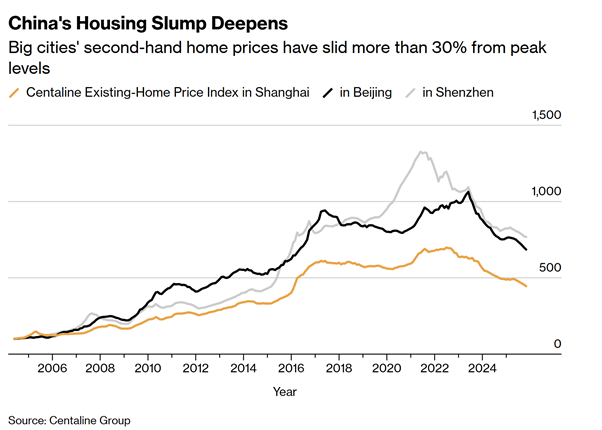

After making a bearish call, China’s leading developer defaulted on debt just eleven months later. Since 2021, big cities’ second-hand home prices have slid more than 30% from peak levels. Mr Lam took a bolder stance last year by turning bullish on the property sector.

However, despite the pivot, I still believe that China’s property market is close to a bottom. Bearishness on residential housing has become a one-way street of traffic. Global banks mostly have dim outlooks for China’s real estate, where a renewed sales slump is underway since the second quarter, reflected in the steepest price declines in at least a year. Second-hand home prices have also been dropping across China, and are down more than a third from the peak levels in major metropolitan areas.

The recovery in China’s property is likely delayed, and at some point, could lead to Government intervention. The key to unleashing consumer spending is property prices, which need to stabilise. Bellwether property developer and manager Longfor remains trapped within a range. This stock is one litmus test for the Chinese property market. A breakout in Longfor on the topside of the range would likely be a precursor for a stabilisation and recovery in China’s property market.

We might be early, but major market bottoms are typically accompanied by the consensus becoming overwhelmingly bearish, conditioned following years of falling prices. The property market is still falling, but the pace of declines could slow as liquidity dries up and as the inventory overhang begins to clear. The new building of residential housing has already dried up.

What the market needs now is for the Chinese government to act more decisively and step in and absorb some of the inventory overhang and reposition it as affordable housing. I believe there is a good probability of this happening sometime over the next six to twelve months. The challenge and motivation for the Chinese government to step up is that consumer spending is not going to recover quickly, whilst housing is still under pressure.

Mr Lam said he anticipates secondary home prices in top-tier Chinese cities to decline another 10% in 2026 and 5% in 2027, unless Beijing introduces major stimulus measures, which is likely now coming next year, in my view. Last week, Bloomberg reported that Beijing is weighing up new measures to turn around the property sector, including subsidising mortgage interest payments nationwide for the first time. One former finance minister in China also recently warned that declining home values will worsen deflationary pressures as consumers save record amounts of cash, which has hit $18 trillion. This dilemma will at some point force the government’s hand.

Mr Lam’s previous forecast of an impending housing recovery was predicated on an easing of residential oversupply after many cash-strapped developers stopped buying land. Last year, housing starts by builders tumbled 63% from the onset of the downturn in 2021.

While the basis of his earlier call remains unchanged, Mr Lam said he expects more prospective homebuyers to stay on the sidelines as the slump in home prices has shaken their long-standing beliefs that real estate is a safe bet. This is to be expected, but house prices in China are rapidly approaching their replacement cost, which is constraining new supply.

Whilst consumers are preferring to rent over buying at some point, this will give way to FOMO when prices eventually inflect higher. We saw this play out dynamically in China’s stock market last year, which exited a bear market. There was a rush to buy from investors parked on the sidelines.

Mr Lam said rental prices could be an early indicator of demand-supply dynamics in the housing market, “as the reading is free of government intervention. After housing rents stabilize, home prices ought to stop declining”. Mr Lam is likely right in that China’s housing market has further to go before stabilisation occurs and prices inflect higher. But I would not rule out government intervention as a circuit breaker to interrupt the cycle sometime next year. Meanwhile, the stock market, which has been one of the best-performing this year, is set to continue next year as consumers continue to invest some of the $18 trillion savings pile into equities and avoid residential property.

Lastly, UBS expects Australian miners to lead a local earnings rebound in 2026. The Australian arm of the investment bank expects a mining-led rebound in earnings, firmer margins and a calmer macro backdrop to support sentiment and boost the ASX200 over the next year or so, after a volatile stretch marked by sharp swings in global rate expectations. I have argued this theme for some time now and anticipate the resources sector to be one significant driver lifting the ASX200 to new records next year.

The AFR reported UBS equity strategist Richard Schellbach now expects the turbulence to ease next year, tipping the index to reach 8900 by the end of 2026. The target implies a rise of nearly 6% from current levels. I believe this target is conservative, and a weakening US dollar could see commodities, iron ore, copper and precious metals all surprise on the upside next year.

The AFR noted that consensus expectations for ASX 200 earnings typically start near 8.5% growth before being cut back to about 4.5% by year-end. Mr Schellbach said that 2026 should prove different as miners drive an upgrade cycle that could lift earnings by more than 10%, with gains broadening beyond resources. UBS sees household spending holding up better than feared and expects lagging healthcare names to also return to growth late next year.

The ASX200 Resources index is bullishly set up to retest the record 2007 highs in the year ahead, in my opinion. Commodities appear to be on the cusp of breaking out on the topside. I expect Fed rate cuts and a weaker dollar could be the catalyst. Resistance above 6,600 on the Resources Index is currently being probed, and we have conviction that a topside breakout will ensue over the coming year. This outcome would serve as one catalyst that drives the broader Australian market and ASX200 index to new record highs.

The investment bank argues that margin pressure, a persistent drag since the pandemic, also appears to be easing. UBS noted that valuations have already de-rated modestly in recent months, bringing multiples back into what it views as a reasonable range relative to the past decade.

The bigger threat, UBS cautioned, is a renewed swing to risk-off sentiment if global growth disappoints. UBS remains constructive on the global artificial-intelligence theme, arguing the cycle still has about two years to run and should continue to support elevated valuations in companies tied to it.

Domestically, UBS expects Australia’s economy to strengthen in 2026, outpacing other advanced economies thanks to resilient consumers, lower interest rates and improving sentiment. With the RBA likely near the end of the cutting cycle and the Fed expected to ease further, UBS said that policy divergence should support a firmer Australian dollar. I believe UBS will be right on the Aussie dollar, but that the RBA will cut at least three more times in the incumbent easing cycle.

Carpe Diem

Sign up to receive full reports for

the best stocks in 2025!

Where to Invest in 2025?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.