KEY CONTENT

- S&P500 and Nasdaq hit record highs this week. The war discount has been erased.

- The US earnings season is off to a strong start.

- Morgan Stanley’s Wilson: AI is boosting margins, not disrupting them. Operating leverage surprises to the upside.

- Michael Burry — the Big Short — has covered his tech short and gone long software (PayPal, Adobe, Salesforce). We added MSFT and META to the Contrarian Fund and topped up tech across managed accounts.

- Central banks are likely to look through the oil spike.

- Hank Paulson warns of a US debt “doom loop”. We discuss. Gold and hard assets are the hedge.

- Gold is holding up well. Our target is $5,000 this year. The March flush-out corrected positioning. Central banks returning to the buy-side.

- ASX 200 within 200 points of record high. Tech surged +7.4% on Thursday. Has tech Down Under turned a corner?

REPORT SPOTLIGHT

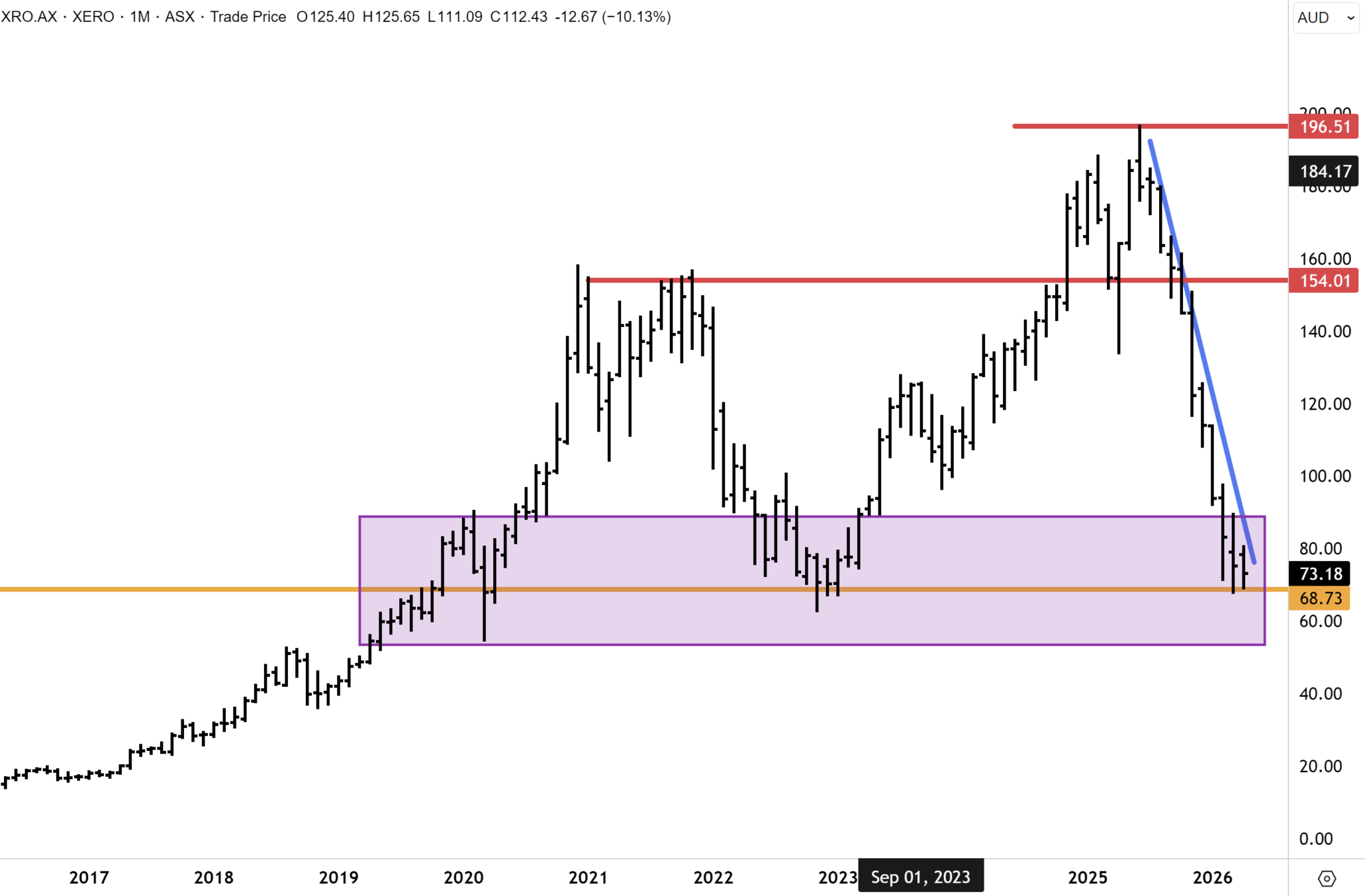

- Xero (ASX: XRO) Buy

WHAT TO WATCH IN THE WEEK AHEAD

- Middle East diplomatic developments, or the lack of them. Oil price movements will likely be closely linked.

- US retail sales and consumer sentiment data.

- US earnings season picks up speed – will early strength continue?

- More Aussie miner quarterly production updates

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join on our Products page.

The market has decided the war is over before the diplomats have. The S&P 500 and Nasdaq made a new record closing high on Wednesday, then extended modestly higher again on Thursday. The VIX is back to pre-war levels. The dominant force this week was the market repricing from “what if this gets worse” to “what does the other side look like,” and concluding the other side looks like a strong earnings cycle, no Fed rate hikes, and a weaker US dollar.

This was largely the playbook I have adhered to throughout the conflict, also noting several times that wars often aren’t an impediment to strong markets for long.

I’ve often said the economy is not the market. It’s a distinction that matters most when fear surfaces, and there has been plenty of that over the past seven weeks. Throughout this period, we have been at our clients’ side – consistent in our view, clear in our communication, and making calls that financial markets were in a correction and not entering a bear market, despite the sometimes-dire headlines…

When Iranian strikes closed the Strait of Hormuz in late February, many investors headed for the exits then or in early March when oil prices spiked. We didn’t. In the week ending March 6th, I wrote, “I have conviction that the most acute phase of the ME shock is now behind the markets. We selectively added to core positions and boosted our total portfolio exposure to copper.”

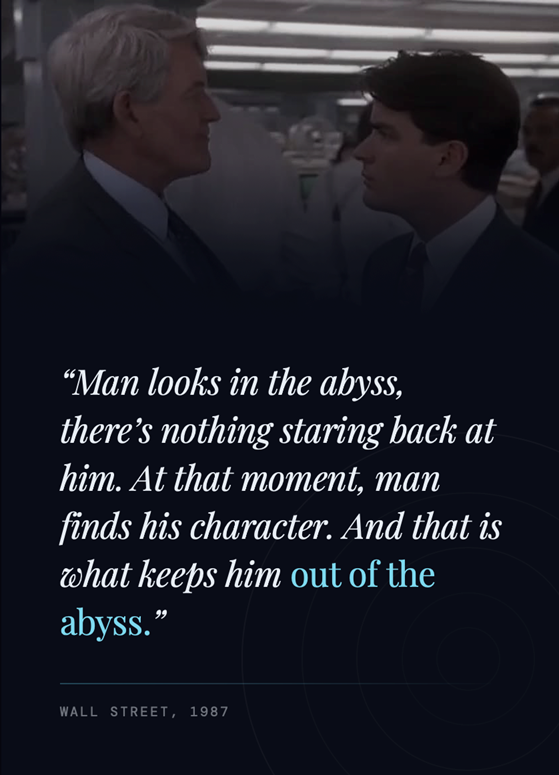

The week ending March 27th was particularly gruelling. I said that week, “The volatility and relentless headlines around the Middle East war – and where it could all go – are trying, as all selloffs and times of panic are. They test our character.”

“One scene from the 1987 film Wall Street always comes to mind during these times. An old timer in the firm says to Bud Fox, just before the police arrive to end his career: “Man looks in the abyss, there’s nothing staring back at him. At that moment, man finds his character. And that is what keeps him out of the abyss.”

In the week ended April 2nd, I noted that Morgan Stanley’s CIO, Mike Wilson, was one strategist who held the line during some of those March pressure-cooker days. And it is ‘pressure’ to hold the line when the markets are tanking and everything coming from the press, brokers & strategists is dire and bleak. It’s hard to maintain a sense of sensibility and objectivity. Mike did well in March, and it’s no surprise that he is the top-rated strategist in the US. We shared a similar outlook and held the line.

The S&P500 and Nasdaq made new record highs on Thursday. It is worth pausing here for a second and reflecting on that outcome…

Other markets have also gained. The ASX200 hit a month high on Wednesday, though a rebounding tech sector has been the big news – more on that later. On Thursday, China/Hong Kong stocks notched up a five-day winning streak as first-quarter GDP growth beat forecasts. In Japan, the Nikkei jumped to a new record high.

The bull market in the FTSE100 is clearly reasserting itself. The rebound off the primary uptrend and surge this week to nearly 10,600 is constructive, and we anticipate a retest of the record highs in the coming months.

Technically, I remain constructive on equities and risk assets generally and have flagged a positive setup on the charts in recent weeks from the S&P500 and international equities to gold & copper. The reporting season is off to a strong start.

With the S&P500 breaking out above last year’s record highs, resistance could now be encountered, but I have conviction that the March corrective drawdown is now in the rear-view mirror. The SPX could undergo some consolidation as the end of the ME war draws closer and as the earnings season unfolds.

The rally might soon resume should the US reporting sector continue to beat on earnings and Mega-cap tech and Mag 7 stocks deliver strong results that push back on AI disruption/capex overspend fears.

The earnings catalyst

Wall Street’s earnings setup is being underestimated. Estimates have been continuously upgraded this year, broadening out through March. BlackRock upgraded US equities, joining Morgan Stanley and JP Morgan, citing resilient corporate earnings and limited economic damage from elevated oil prices. BlackRock noted the tech sector is now expected to post earnings growth of +43% in 2026, up from +26% last year. Morgan Stanley’s Mike Wilson added that markets are “likely further along in the discounting process than appreciated,” and that AI looks more likely to support than compress margins, with operating leverage surprises surfacing in earnings breadth, the median company now growing EPS in the double digits, the fastest pace since 2021.

Michael Burry – who became famous shorting the US credit market before the GFC – has pivoted entirely, establishing long positions in PayPal, Adobe, and Salesforce. His thesis: a “reflexive positive feedback loop” between falling equity prices and stress in bank debt tied to software companies accelerated the selloff beyond what fundamentals justified.

I see a similar opportunity, and we added Microsoft and Meta Platforms to the Fat Prophets Global Contrarian Fund, as well as topping up on tech stocks in our Global and Australian managed account portfolios (reach out to Patrick.ganley@fatprophets.com.au for more information)

Meanwhile, the banks have kicked off the season in strong shape and generally offer a good outlook for broader business health. Citigroup and BlackRock both delivered solid earnings beats, JP Morgan slipped modestly despite record quarterly trading revenues. Goldman reported a solid profit beat, and CEO David Solomon noted that market volatility from the conflict had tempered IPO execution, but the environment remains strong and activity will rebound once conditions stabilise. , Bank of America – the second-largest US bank – reported a jump in quarterly earnings, extending a run of beats. Wells Fargo was the only notable miss.

What’s happening underneath

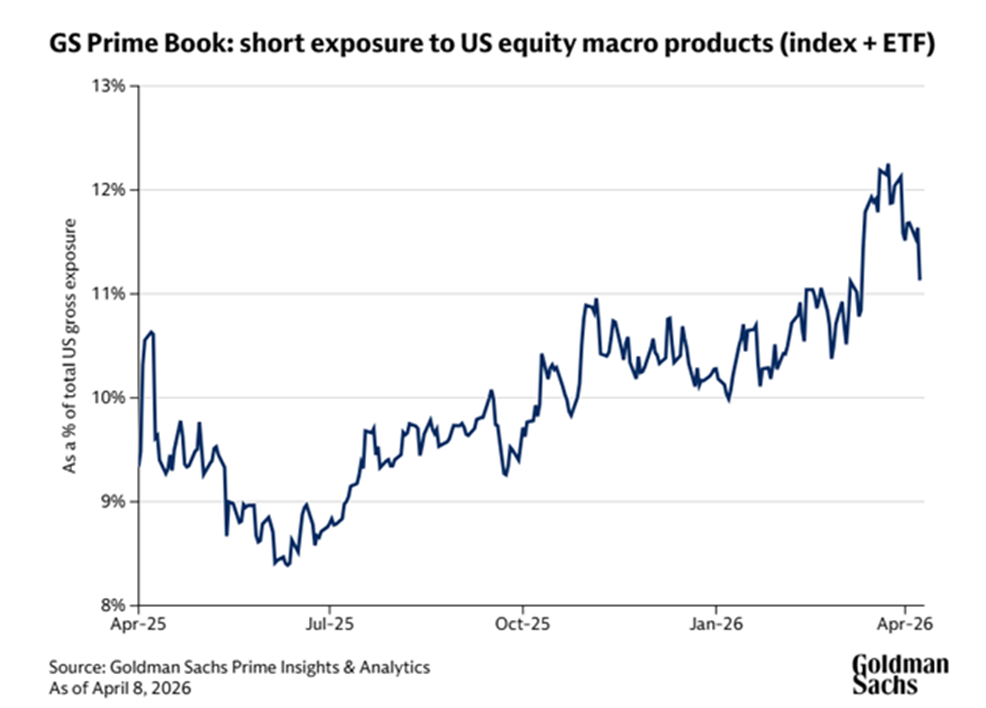

The rally has liquidity fuel, not just narrative. Goldman Sachs noted the ceasefire-driven surge last week saw the largest unwind of short positions on US-listed ETFs since August 2020, concentrated in large-cap equity ETFs. Short exposure has fallen to early March levels, though it remains above recent averages. Goldman expects large-cap tech to rally in the weeks ahead as fund managers increase exposure to their highest-conviction names. Additionally, systematic trend-following traders (CTAs) collectively hold a $30 billion short position on the S&P 500, a potential source of further upside fuel as they flip to the buy side.

The feared second-order effect of the war – a rate hike cycle triggered by an energy-driven inflation spike – may not materialise.

Chicago Fed President Goolsbee noted oil futures markets price the surge as short-lived, limiting the economic impact. JP Morgan concurs, arguing that while an oil spike lifts CPI for a few months, central banks could look through it. We may not see the rate hike cycle many feared. JPM also noted that positioning and sentiment remain bearish — similar to 2022 when a widely anticipated recession never arrived, and markets staged a sharp V-shaped recovery. Their conclusion: “If one has a longer time horizon of 3/6/12 months, one should be using the weakness to buy.”

I agree with JPM but would advocate that the rebound could become more pronounced, led by US markets as earnings season leads to a high beat rate on profits and another round of upgrades from Wall Street analysts. JPM noted that positioning and sentiment remain bearish. “Sentiment among most pundits, which was constructive in the first days of the conflict, has, two/three weeks into the escalation, capitulated into a bearish one – the prevalent opinion became one of expecting things to get worse, oil price was projected to inevitably spike much higher, Pandora’s box was opened, etc. At the same time, investor derisking was getting advanced, and the oversold signals began to appear; one should start adding risk.”

Positioning is still skewed bearish, and the current setup is similar to 2022, when just about everyone was expecting the most anticipated recession to arrive in decades. The market did the exact opposite and bottomed out in October 2022. Similar to today’s setup, the market saw straight through all the bearish rhetoric that was pervasive at the time. The recession never arrived, and the S&P500 and international markets proceeded to rise sharply in what was a V-shape recovery.

We like hard assets, including gold.

Even as equities recover, the longer-duration picture points to continued hard asset outperformance. JP Morgan analyst Jason Hunter noted the S&P 500/Gold ratio has been bearishly consolidating below its breakdown level from earlier in Q1 – a pattern building since 2022, consistent with prior hard asset outperformance regimes of the 1930s, 1970s, and 2000s, each of which lasted roughly a decade.

The downward trend in the S&P 500 Index/Gold ratio points to further outperformance by gold versus the broader US stock market.

Source: JP Morgan.

I am more bullish near-term. The March flush corrected overbought conditions and positioning; central bank buying should resume, and the dollar’s downward trajectory should reassert once the ME war concludes. Gold has regained $4,700, and we have confidence our $5,000 target will be eclipsed this year. The bull market in gold remains intact.

Gold has managed to resume upward momentum and regain the $4,700 level. We have confidence that our target of $5,000 will be eclipsed once again this year, and while it could take some time for the record highs at $5,600 (established on Comex) to be retested, the bull market remains very much intact in our view.

Break the glass

Former Treasury Secretary Hank Paulson this week warned of an existential risk to the US bond market as federal debt approaches $39 trillion. Debt servicing is now close to 4% of GDP, with debt-to-GDP projected to hit a record 108% by 2030. He spoke of the “doom loop” mechanism, which is when investors demand higher yields, increasing interest costs, widening the deficit, forcing more issuance, pushing yields higher still – with the Fed eventually becoming buyer of last resort. Paulson joins Gundlach, Druckenmiller, and Dalio in flagging this structural risk. I share the view that the US dollar will decline sharply over the coming years as spending pressures weigh on the bond market, a primary driver of the bull market in gold and hard assets.

For now, the US10yr bond has been relatively well contained despite the ME war and a sharp rise in oil prices. The 10yr yield has remained confined within an extended range after hitting 20yr highs in 2023. A breakout above the near- term downtrend could see the 10yr rise to 5%, which is a significant resistance level. Technically, this looks to be a scenario that might play out later in the year, or even in 2027. One outcome from the ME war is that the White House has isolated and pushed away international buyers of US treasuries. Global appetite might not return quickly. In the case of China, the country has been a net seller.

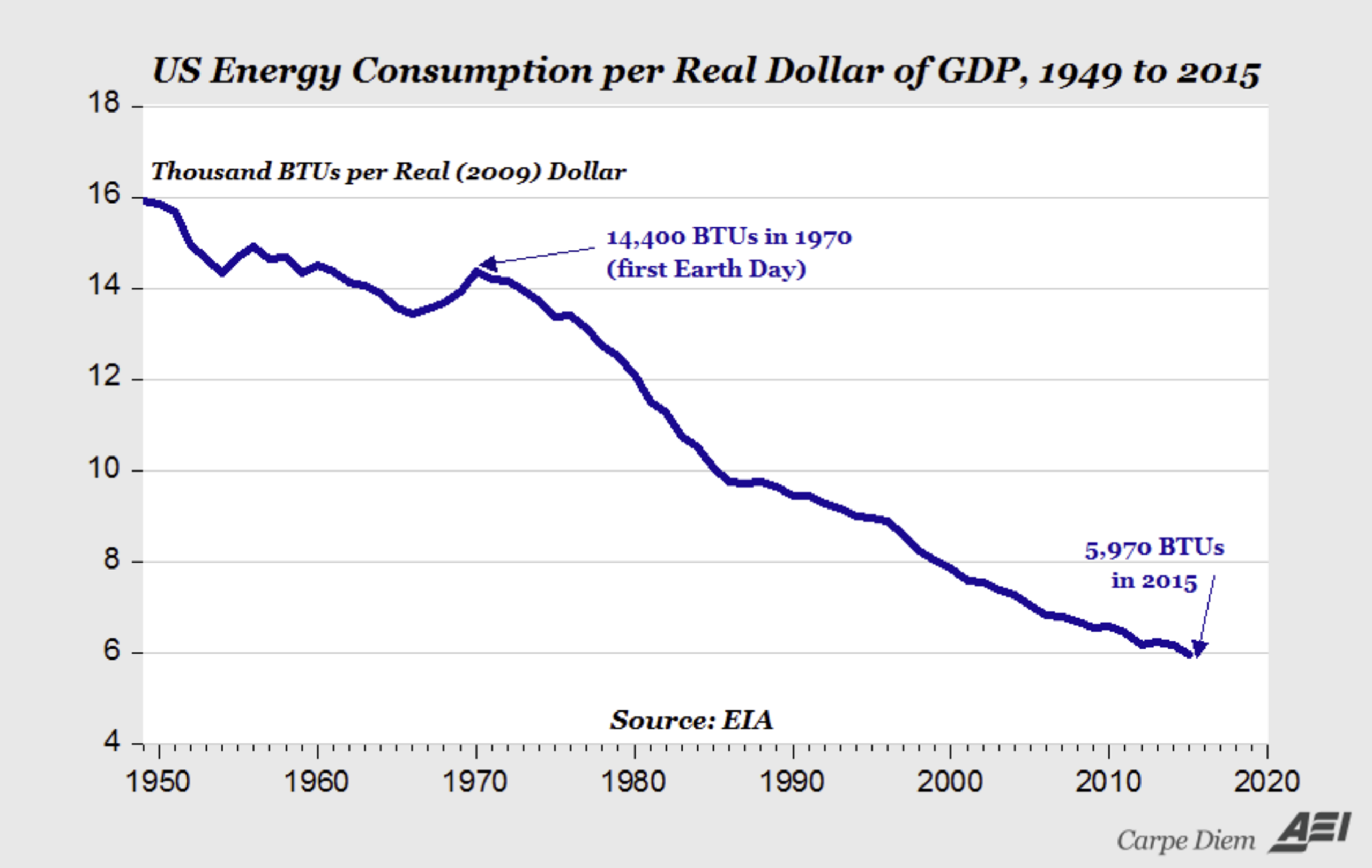

One reason treasuries have been contained through the ME war is that the US, as the world’s largest oil producer, benefits from high prices, and energy intensity has fallen ~47% over the past 30 years, decoupling growth from energy demand in a way that simply wasn’t true in the 1970s.

The ASX200 has rebounded dynamically off key support near 8,300 and rallied to just under 9,000. The benchmark is now just 200 pts below the record high. Similar to the S&P500, the ASX200 could now undergo some consolidation and await further catalysts – an end to the ME war, lower oil prices and direction on Wall Street. Our base case for the index to resume upward momentum and surpass the record highs this year remains intact.

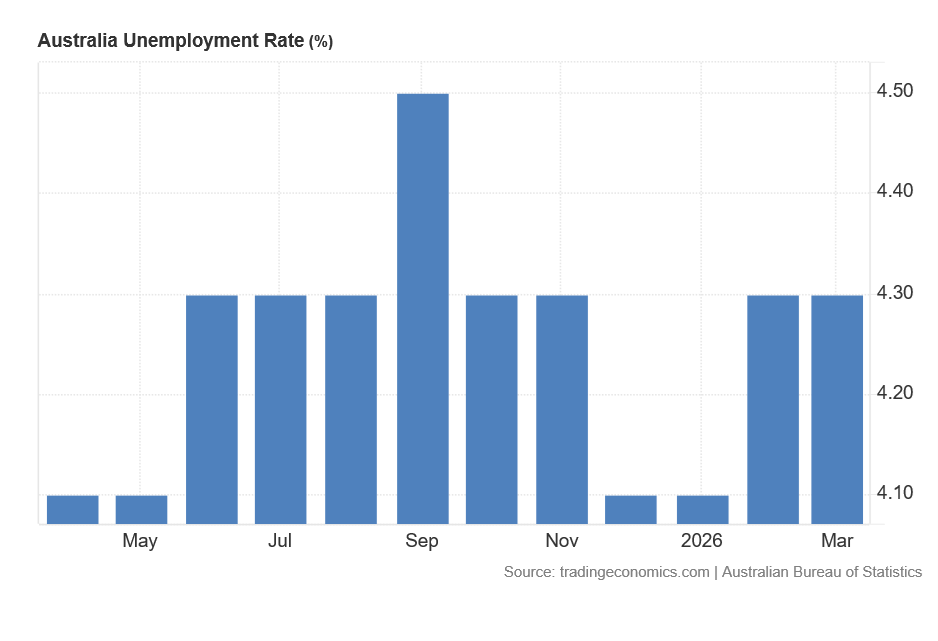

In Australia, job data was firm enough that many economists believe a third-rate hike is on the table this year. We expect that to change quickly if the RBA turns to the view that the energy spike will be transitory. Employment rose 17,900 in March to a record 14.77 million, marginally below consensus and the softest gain since last November’s contraction. The unemployment rate held at 4.3%, in line with expectations, while the participation rate edged down.

It was all about renewed risk for tech on Thursday, as the Nasdaq logged new highs overnight. Although the composition of our local tech sector is somewhat different to the US, shorts are being liquidated, and that is healthy for the group to stage a more meaningful recovery from beaten-down levels. WiseTech Global led majors at +12.4%, while Xero +9% (a stock the research team initiated coverage on early in the week with a buy rating) wasn’t far behind. We see the tech sector as likely having turned a corner.

Xero (ASX: XRO) – Buy

Xero has been sold off alongside lower-quality software businesses, but the underlying franchise hasn’t deteriorated. Sticky customers, 1.09% monthly churn, an 88.5% gross margin, and a Rule of 40 above 44 tell a different story to the price action. ANZ prints an impressive margin; the UK is scaling with regulatory tailwinds; and the Melio acquisition opens a credible path into a US$29 billion SMB payments market. At below 5x NTM revenue against a 10-year average of 11x, the market is pricing Xero like a mediocre SaaS business. It is a premium one.

Xero is a stock that looks to have confirmed an important bottom. The shares have fallen from highs around $200 to find support around $70, which are major levels that were tested back in 2022 and 2020. Our technical base case is that a breakout above $75 will soon ensue, and upward momentum returns when risk appetite for Australian technology companies returns. Once the downtrend is breached (on the upside), we believe Xero would have recovery potential initially towards $100/$120, but plausibly the record highs over a medium-term time frame.

This fatLITE edition is a condensed version of our full weekly fatWRAP, which includes deeper positioning analysis and more targeted investment opportunities. A subscription also includes 4 daily market commentaries during the week and reports on stocks, ETFs and special reports spanning Australasia, Mining and Global Equities.

Have a great weekend.

Carpe Diem

Angus