KEY CONTENT

- US inflation arrived hot on both counts this week – CPI its biggest annual gain in three years, PPI its biggest monthly gain in four years – and Wall Street moved to consecutive record closes regardless. The bond market dissents alone; Angus has flagged a break above 4.6% on the 10-year as the trigger for equity volatility.

- The commodity supercycle is confirmed. Copper hit a record, the Bloomberg Commodity Index broke to fourteen-year highs and is up nearly 40% for the year. Iron ore broke above key downtrend resistance against bearish broker consensus. A pullback on Friday was tactical; the breakout is real. BHP made four consecutive record closes, briefly overtaking CBA as Australia’s largest company.

- The Chalmers budget delivered the biggest overhaul of Australian capital taxation in 25 years – negative gearing gone on established property, the CGT discount replaced. CBA shed more than 10% in a single session. The resources sector ran through it; financials did not.

- The Trump-Xi summit moved as positively as any likely outcome. Chinese equities are in an early-stage bull market.

- Jeffrey Gundlach outlined his macro frame this week: load up on cash, gold, and real assets; the Fed could hike rather than cut; gold heading significantly higher over five years. Angus shares the 1970s supercycle parallel and has positioned for it.

REPORT SPOTLIGHT

- Global X Copper Miners ETF

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join on our Products page.

US inflation arrived hot on both counts this week. The bond market hardened around it. The S&P 500 closed at a record anyway.

CPI posted its biggest annual gain in three years on Tuesday. PPI followed with the largest monthly increase in four years. Two Fed officials floated rate hikes. The US 10-year yield climbed to 4.48%, the 30-year held above 5%, and December rate-hike probability rose from 21.5% to 30% across the week. The bond market collected every piece of evidence it could and signalled its concern clearly. The equity market ignored it. The S&P closed at 7,501 on Thursday – a fresh record. The Nasdaq made its own. The Nikkei broke 63,000 for the first time. Shanghai hit an eleven-year high. Copper printed a record $6.64. BHP made consecutive record closes.

The Chalmers budget reshaped Australian capital taxation in ways that will compound for years. The Trump-Xi summit moved as positively as any reasonable outcome could. The 4.6% level on the US 10-year – the threshold Angus identifies as the trigger for equity volatility – has not fired. Until it does, the path of least resistance is higher for equities.

The Budget

The most consequential domestic event for Australian investors in a generation was delivered on Tuesday night. It was poorly received.

Negative gearing on future purchases of established investment property is gone, effective from budget night. New builds, existing portfolios, and build-to-rent are carved out. The full regime takes effect on 1 July 2027. The 50% CGT discount goes with it, replaced by an indexation method plus a 30% minimum on real gains. Trusts move to the same 30% floor. Pre-1985 assets are pulled into the tax net in 2027.

Under the old discount, a top-bracket Australian paid an effective CGT rate near 23.5%, broadly in line with the US and UK. Under the new regime, the upper bound runs to 47% – top of the OECD table, ahead of Denmark and Norway. Goldman Sachs’ Matthew Ross flagged the consequence: Australia now has one of the world’s most lenient regimes on dividends and one of the harshest on capital gains. It becomes more expensive to invest in growth companies and relatively more attractive to hold fully franked dividend payers. The franking-yield trade, already crowded, gets more crowded. Add the active-to-passive rotation — UniSuper’s sell-down has begun, Mercer is next, transition portfolios estimated as high as $10 billion — and the bias against growth and toward the big franked payers compounds in the same direction.

The rental supply consequence is worse. There is now no incentive for investors to add to the nation’s rental stock outside of new builds – and the developer spread on new product makes that path unattractive for most. Supply contracts, rents rise. Treasury’s modelling has rents lifting by $2 a week on a 35,000-dwelling supply hit over the decade, offset by a $2 billion fast-track program said to add 65,000. Take both figures with a grain of salt. On housing affordability, the government is on the wrong horse.

The ASX 200 traded lower for most of the week before a Thursday tick higher, divided along a heavyweight sector fault line. Materials advanced as the commodity supercycle drove the majors to records. Financials were under pressure as the budget’s tax wedge landed on the dividend trade. Technology, consumer and healthcare absorbed what remained of the budget anxiety. Globally, equities ignored the bond market – the S&P, Nasdaq, Nikkei and Shanghai all set records or multi-year highs. Bond market volatility remains well contained for now.

The commodity complex ran hot. Copper hit $6.64 on Tuesday and held most of it, finishing Thursday at $6.60. The Bloomberg Commodity Index broke above 143, near 14-year highs, up nearly 40% calendar year-to-date. BHP made consecutive record closes. Friday delivered a tactical pullback on USD strength — the dollar index at 98.9, gold off 1% to $4,656, silver down 6% to $84, Bloomberg Commodity Index back to 141.4. The pullback was tactical, and the breakout is real, and the bond market’s dissent is the only meaningful counter-signal on the board.

The Calls

The dominant call: the commodity supercycle remains a durable thesis.

Across the full week, every piece of evidence pointed in the same way. Copper printed a record. BHP made consecutive record closes. Iron ore appears to be breaking out above key downtrend resistance, with the primary uptrend in place since 2017 intact and upward momentum resuming – a sharp contrast to the bearish broker consensus.

JP Morgan’s framing this week was the right one: the short-term driver is Chinese buying with inventories at their lowest level at this time of year in over five years; the long-term driver is data centre and infrastructure demand, structural and durable, and independent of the geopolitical cycle. Scope for extension to $7 per pound remains. Strategic stockpiling — accelerated by both the Middle East war and Covid-era supply shocks — will compound the demand pull as more nations prioritise critical-material reserves the way China already has. The cleanest Australian copper plays are the Global X Copper Miners ETF (WIRE), Sandfire (SFR), Capstone (CSC) and 29Metals (29M). BHP and Rio Tinto carry the iron ore and diversified exposure.

The US bull market is earnings-driven.

Roughly 85% of S&P 500 companies beat first-quarter expectations. EPS growth tracked around 28% year-on-year against a consensus of 14.4% at the start of April — the strongest quarter since 2021. Yardeni raised his December S&P target to 8,250 early in the week. Morgan Stanley’s Mike Wilson followed with 8,000 for December and 8,300 over twelve months. The technology sector sits at a record. The Nasdaq is up 15% year-to-date. Support for the S&P is well defined at 7,000, which limits downside risk into the back end of an earnings season already in the home stretch.

Support for the S&P 500 is very well defined now at 7,000, which mitigates downside risk following the solid earnings season, which is in the home stretch.

The bond market’s dissent warrants watching, not capitulation.

Jeffrey Gundlach’s frame is the clearest macro counter-thesis on the table: load up on cash, gold and real assets; the Fed could hike rather than cut; anyone positioned for two cuts as the working thesis is “on the wrong horse.” The structural pressure from a US national debt approaching $40 trillion is real, and Treasury Secretary Bessent has openly discussed yield-curve management tools that resemble what Japan has been running for years. Gundlach is a gold bull and, like Angus, sees gold heading toward $10,000/oz over the next five years. The 4.6% level on the US 10-year is the line in the sand. Until it fires, the equity market wins the argument.

The China and Hong Kong bull market call is locked in this week.

Shanghai equities reached an eleven-year high. The CSI 300 approached 5,000. The Trump-Xi summit moved as positively as could be expected. A reported 200-jet Boeing order from China, US chip sales to Chinese firms cleared, and the relationship is visibly thawing. The early bull cycle has years to run.

Chinese equities are in a new bull market. The Shanghai Composite index broke out above the primary downtrend last year and ended a multi-year bear market. I believe the early bull cycle in China/Hong Kong will continue for a number of years, following what was a severe domestic slowdown and selloff in the property market.

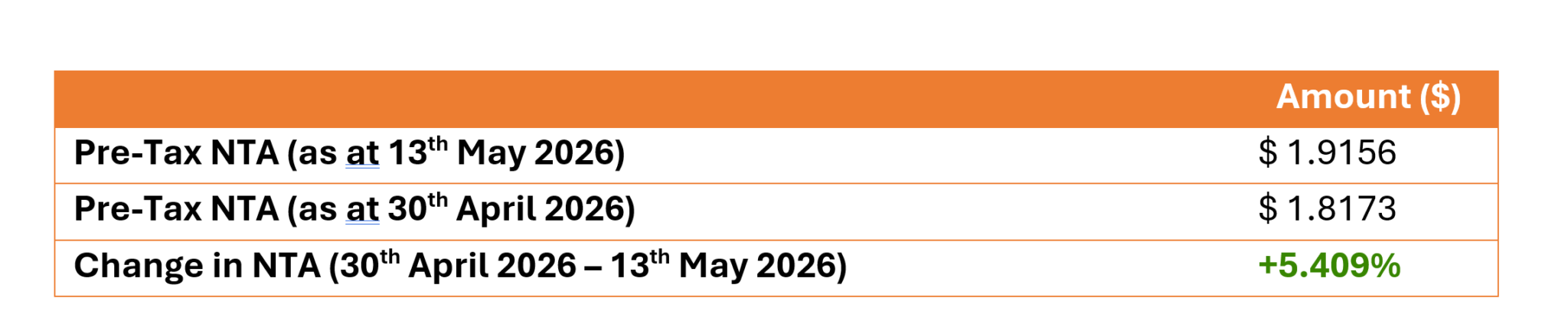

Chinese technology companies trade at a significant discount to their US counterparts with comparable growth runways. The Fat Prophets Global Contrarian Fund (ASX: FPC), which is in the middle of a capital raise, provided an update to the ASX this morning, highlighting an improvement in estimated pre-tax NTA as risk appetite returns to international markets.

FPC has around one-third of the portfolio invested in leading Chinese and Asian technology companies.

The ASX release highlighted a new addition to the portfolio: “On this front, we added Futu Holdings Limited (Nasdaq: FUTU) to the portfolio this week. Futu is a Hong Kong-headquartered fintech company founded in 2012 that operates one-stop digital platforms such as Futubull and Moomoo to deliver securities brokerage, wealth management, and related financial services globally. It enables trading in diverse assets, including Hong Kong, US, China Connect, Singapore, Australian, Japanese, Canadian, and Malaysian stocks, plus derivatives, ETFs, options, margin financing, securities lending, and virtual assets for eligible clients. The company has 29 million users across 200+ countries with 100+ worldwide licenses. Listed on Nasdaq since 2019, Futu emphasises user-centric tech innovation to simplify investing and expand into ESOP solutions, IPO distribution, and private wealth management.”

“We find FUTU’s valuation attractive at 11X PE on consensus estimated earnings for 2026. We also expect the company’s continued operating leverage to drive revenues and earnings over the next few years as operations scale up, amidst a better environment for Asian equity markets, where many clients are domiciled. We see room for multiple to catch up, mainly driven by market share gains in the key Hong Kong, Asian and other markets.”

The Fund has announced a rights issue, which is now open and attracting solid early-stage support. I intend to take up my full rights entitlement for a nominal amount of c$860,000. Underwriting for $1m has also been secured to backstop the rights issue should any shortfall ensue, but existing shareholders can apply for more if they choose. I want to thank all shareholders for their tremendous support over the past several years and all those participating in the capital raise to grow our Fund.

REPORT SPOTLIGHT

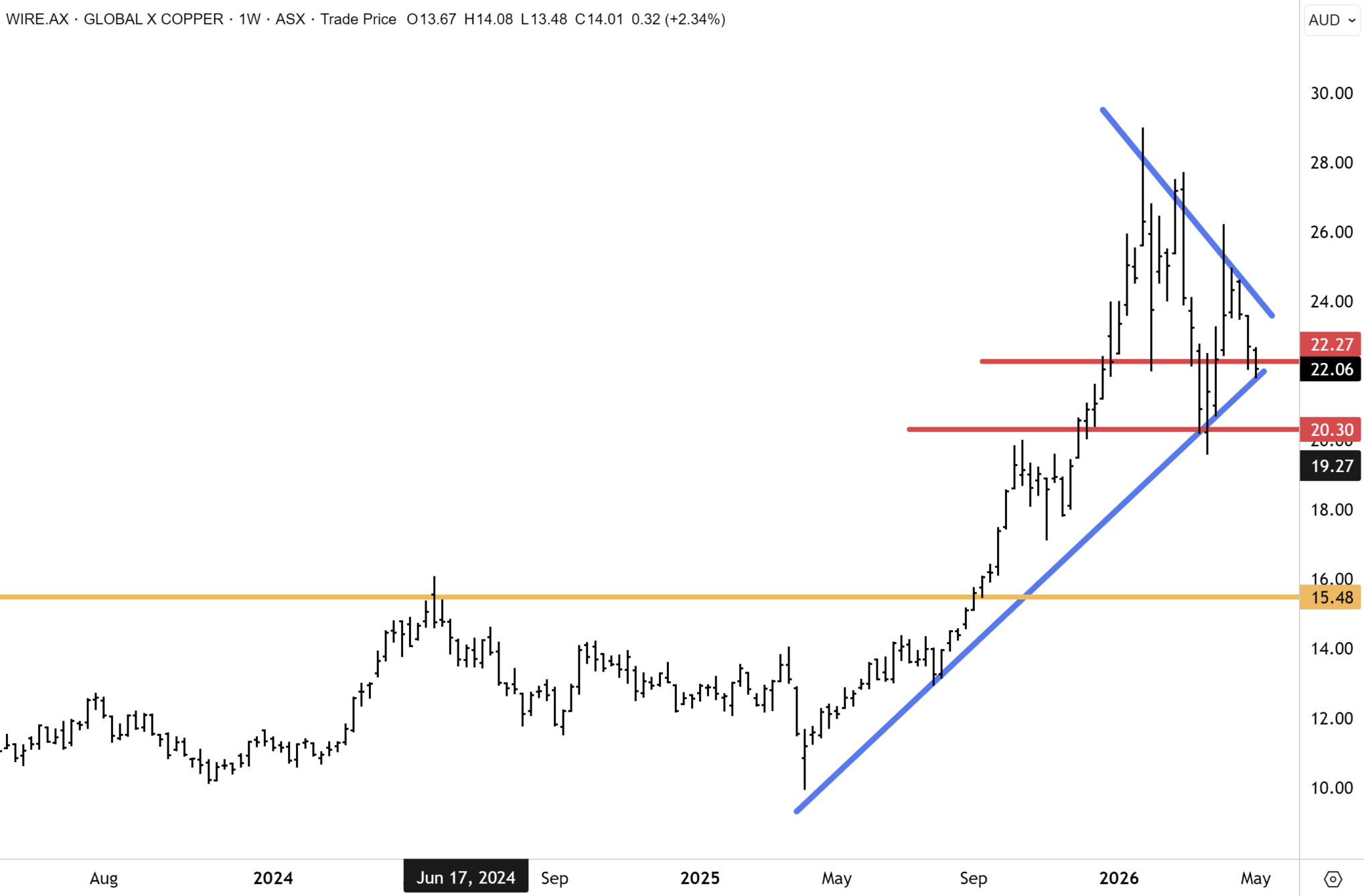

Global X Copper Miners ETF (ASX: WIRE) – BUY

The structural copper thesis has hardened since our last note. Treatment and refining charges have collapsed toward zero, confirming smelters now compete for concentrate rather than the reverse, a signal of genuine tightness rather than a cyclical wobble. JPMorgan had pencilled in a 2026 refined deficit of 330,000 tonnes before the Middle East escalation sharpened supply-line thinking further. AI data centre campuses drawing 50 to 100 megawatts each are forcing copper-intensive grid upgrades ahead of compute build. WIRE provides exposure to a basket of copper miners leveraged to a bullish outlook for copper.

Since our January tech update, the Global X Copper ETF (ASX: WIRE) made new record highs above $29 and has corrected to key support at the one-year uptrend. Following a rebound of this key support, WIRE surged to $26, only to correct back to the uptrend in recent weeks. Constructively, WIRE looks to have established a higher low, and we remain confident that key support will hold. Our base case is that WIRE resumes upward momentum over the coming year when copper prices also recover back to the highs. Our base case remains that WIRE will retest the record highs above $28 by December.

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join on our Products page.

Have a great weekend.

Carpe Diem

Angus