- The market repriced its primary risk. The S&P 500 closed at a record 7,563 and the Nasdaq at 26,917, even as April PCE delivered the hottest inflation print in three years. The bond market rallied anyway. The thirty-year fell back below 5%. Inflation is no longer the primary concern; deal resolution is.

- The desks have arrived. Goldman lifted its year-end S&P target to 8,000, joining JP Morgan, Morgan Stanley, and UBS – all four major houses now sit above the index. JP Morgan simultaneously raised its long-term iron ore forecast to $90 a tonne and lifted BHP and Rio by 10 to 12%. The commodity super-cycle thesis received its broadest institutional endorsement of the year.

- Sell the tweet, buy the molecule. Jeff Currie’s framing was the cleanest of the week: the Iran deal is the tweet; the structural deficit in physical supply is the molecule. Inventories are still drawing down. Any energy selloff on deal confirmation is a level to buy, not a signal to exit.

- Australian housing faces a structural reset. Morgan Stanley’s base case is a 5 to 10% national price decline following budget changes to capital gains tax and negative gearing, with a worst case of near 20%. The RBA tightening cycle appears finished – April CPI printed 4.2%. Both Morgan Stanley and UBS say the same thing as us: overweight resources.

- The records are not as stretched as they look. Goldman’s Ben Snider lifted his 2026 S&P 500 EPS forecast to $340 a share, implying 24% profit growth for the year – and first-quarter earnings already came in at +29%, the strongest expansion since late 2021. The counter-intuitive point: the price-earnings multiple has actually compressed since October, because forward earnings estimates have outrun the index. The S&P trades at 21 times forward earnings, still below last October’s peak. The upside risk is an overshoot above 8,000.

Report spotlight: BHP.

This FatLITE covers the headlines. The full research – complete macro analysis, buy recommendations, and model portfolio positioning – is available to members. We’ve been an independent investment research provider for 25 years. If you’re not yet a member, find out what’s included – and why we back it with a 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

The Verdict

For eight straight weeks, the S&P 500 has climbed a wall of worry, while a significant cohort of investors sat in cash, waiting for the catalyst that would prove their caution right. This week, it pointed the other way. A draft agreement between Washington and Tehran reportedly landed at the White House: a sixty-day ceasefire and a reopening of the Strait of Hormuz. The bond market, despite being handed the hottest PCE inflation print in three years, rallied anyway. The thirty-year yield slipped back below 5%. The S&P closed at a new record of 7,563, ditto for the Nasdaq, at 26,917. The VIX fell to 15.7, its lowest reading since February.

The market has stopped pricing inflation as its primary risk and started pricing the resolution it has spent months waiting for. Goldman Sachs lifted its year-end target to 8,000, joining JP Morgan, Morgan Stanley and UBS; all four major desks now sit above the index. JP Morgan raised its long-term iron ore forecast and carried BHP and Rio higher with it. The commodity super-cycle thesis received its broadest institutional endorsement of the year. Citadel gave the week its name. The pain trade, it argued, is for prices to keep rising.

Commodities told a clean story. Oil fell across the week, WTI ending near $89 even after a mid-week spike on US strikes on Iranian targets, as the market looked past the headlines to the supply a reopening would release. Gold whipsawed hard, trading below $4,400 in Asian hours before recovering to $4,530 by the US close. Copper held around $6.42 and iron ore sat near $105, still refusing the bear market most desks forecast at the start of the year. The dollar firmed modestly to 99.2.

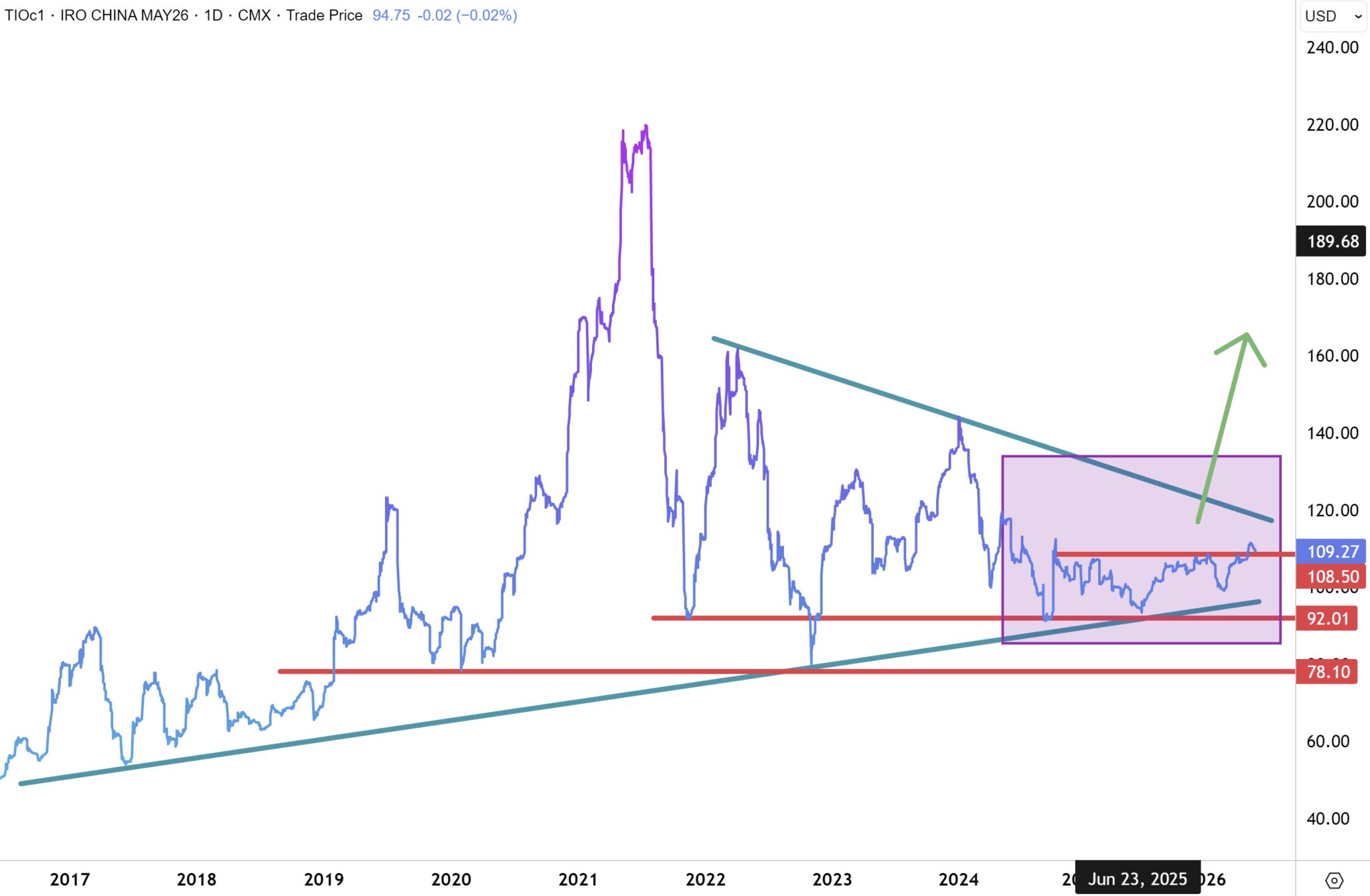

The conviction that strengthened most this week was the one we have long held. We expect the resources sector will be the strongest performer on both the ASX 200 and the FTSE 100 this year, as the commodity super-cycle materialises and copper makes new record highs. This week, the brokers started arriving at the same conclusion. JP Morgan lifted its long-term iron ore price target from $80 to $90 a tonne, citing persistent sector cost inflation, deteriorating ore quality, and less Simandou disruption than the market expects. It raised valuations on BHP and Rio Tinto by 10 to 12% and kept both overweight, with a skew to BHP. The bearish iron-ore consensus held by most investment banks at the start of the year has simply not played out, and others will follow JP Morgan rather than be left explaining why they missed it.

The Fat Prophets Global Contrarian Fund provided an update this morning, which included a rundown on Japanese bank Mizuho Financial Group, which soundly beat earnings estimates this month. Japanese banks are some of the best global beneficiaries of rising bond yields, in our opinion, and a good hedge against other stocks that are more interest rate sensitive.

I want to thank all shareholders for their tremendous support over the past several years and all those participating in the capital raise to grow our Fund. Please reach out to patrick.ganley@fatprophets.com.au if you have any questions about the offer or applying for shares.

The ASX announcement this morning had this to say about gold. “Gold has been volatile recently, but we are of the view that the final stage of a multi-month corrective consolidation is playing out. The US/Iran negotiations could potentially soon reach an agreement that would see a reopening of the Strait. Gold has moved inversely to oil and the US dollar since the outset of the war, and a conclusion might soon draw an end to the ongoing incumbent correction.”

Gold has repeatedly rebounded off the primary uptrend and the 200-day moving average over the past several months since the ME war began. The correction looks to be drawing to an end, and the reopening of the Strait, which instigates lower oil prices and US dollar weakness, might be the catalyst for an upside reversal and resumption of upward momentum.

The second call is the one that survives the deal. Jeff Currie, formerly Goldman’s head of commodities and now at Carlyle, made the argument most clearly: sell the tweet, buy the molecule. A Strait reopening does not immediately resolve the supply shortage, because inventories are still drawing and Iran’s negotiating leverage has compounded with every day they fall. The deal is the tweet. The structural deficit in physical supply is the molecule. Any selloff in major energy names on reopening confirmation is a buying opportunity. Shell sits on well-defined support at 2800p, having posted a 24% rise in quarterly profit to $6.92 billion while its chief executive warned of a cumulative supply shortfall of nearly a billion barrels and growing. Santos and Woodside carry the same trade locally.

The Local

In Australia, April headline inflation eased to 4.2%, below the 4.4% consensus and down from 4.6% in March, with the trimmed-mean measure ticking up only marginally to 3.4%. Money markets halved the probability of a June rate rise to 6% and now price just 20 basis points for the remainder of the year. A June hike is effectively off the table, and with the Budget’s dampening effect still feeding through the housing market, the more likely path is that the RBA is finished tightening for this cycle.

The week’s shape on the ASX was choppy. It opened firm on Monday with materials leading, wobbled on Tuesday as Morgan Stanley’s housing warning and a 13% collapse in ASX Limited on a cost-guidance shock weighed on sentiment, rallied on the CPI print Wednesday, then fell 1.43% in Thursday’s local session as Asian-hours risk-off selling hammered the gold names. That last move requires context. It priced a re-escalation that the US session the same night refuted, and at the time of writing on Friday, the ASX200 was firmly higher, with gold miners rebounding.

Housing produced two institutional calls that deserve attention. UBS framed it as a three-pronged attack on the economy, from higher oil, rising rates, and the Budget’s changes to capital gains tax and negative gearing, and advised clients to overweight mining and healthcare in response. Morgan Stanley went further and called it a structural reset rather than a cyclical dip, with the old high-leverage negative-gearing model compromised by the tax changes and roughly one-third of marginal investor demand at risk, producing a base case of a 5 to 10% national price decline and a worst case near 20%.

Morgan Stanley believes that in the wake of the budget, the economy and property market will face several headwinds and that investors need to focus on the resources sector. We have advocated this strategy for some time, with all our portfolios anchored and skewed heavily towards the mining sector, which could do all the heavy lifting for the ASX200 this year.

Morgan Stanley Australia issued a significant call on the residential housing market this week. The central message is that Australian housing is facing a structural reset, not just another cyclical air pocket. Proposed changes to capital gains tax and negative gearing alter the maths and returns for new investors in established housing, a cohort that represents roughly one-third of marginal demand.

The old household negative gearing investment model of high leverage, near-term cash-flow losses, and reliance on large capital gains has now been totally compromised in the wake of the Labour budget handed down last week. With expected after-tax returns lower and borrowing capacity more constrained, investor demand is anticipated to fall sharply unless rental yields rise meaningfully.

Morgan Stanley argues that the market will restore those economics primarily through lower prices, estimating a base case decline of 5% to 10% will be needed across the nation, which incorporates both the tax shock and the already-soft starting point created by the RBA tightening path, to fully restore investor returns. The worst-case scenario is a more extreme call for falls of up to 20%. While the broader macro backdrop makes a larger 5-10% correction likely, this decline would rank among the largest national house-price drawdowns in four decades.

Australia’s housing market was expensive heading into the budget, in what has become a “crowded” market underpinned by very high immigration and supply shortage. The changes to negative gearing will, in my view, not lead to an increase in supply, at least not over the short term, and could push rents higher. After an extended run since Covid, a period of consolidation for Australia’s housing market is healthy, given the significant outperformance over other international property markets in recent years. I don’t see Australian housing prices falling much more than 10%, given that building costs could soar in the coming years. Developers will need higher prices from incumbent levels to cover higher build costs, which, in my view, will keep housing stock levels constrained.

We note that James Hardie Industries bucked the broader market weakness on Thursday, rising +3.3%. An inflection on the Australian chart looks to be drawing near. A sustained breakout above $32 would potentially point to an inflection. Value investors would be accumulating now.

BHP (ASX: BHP) – BUY

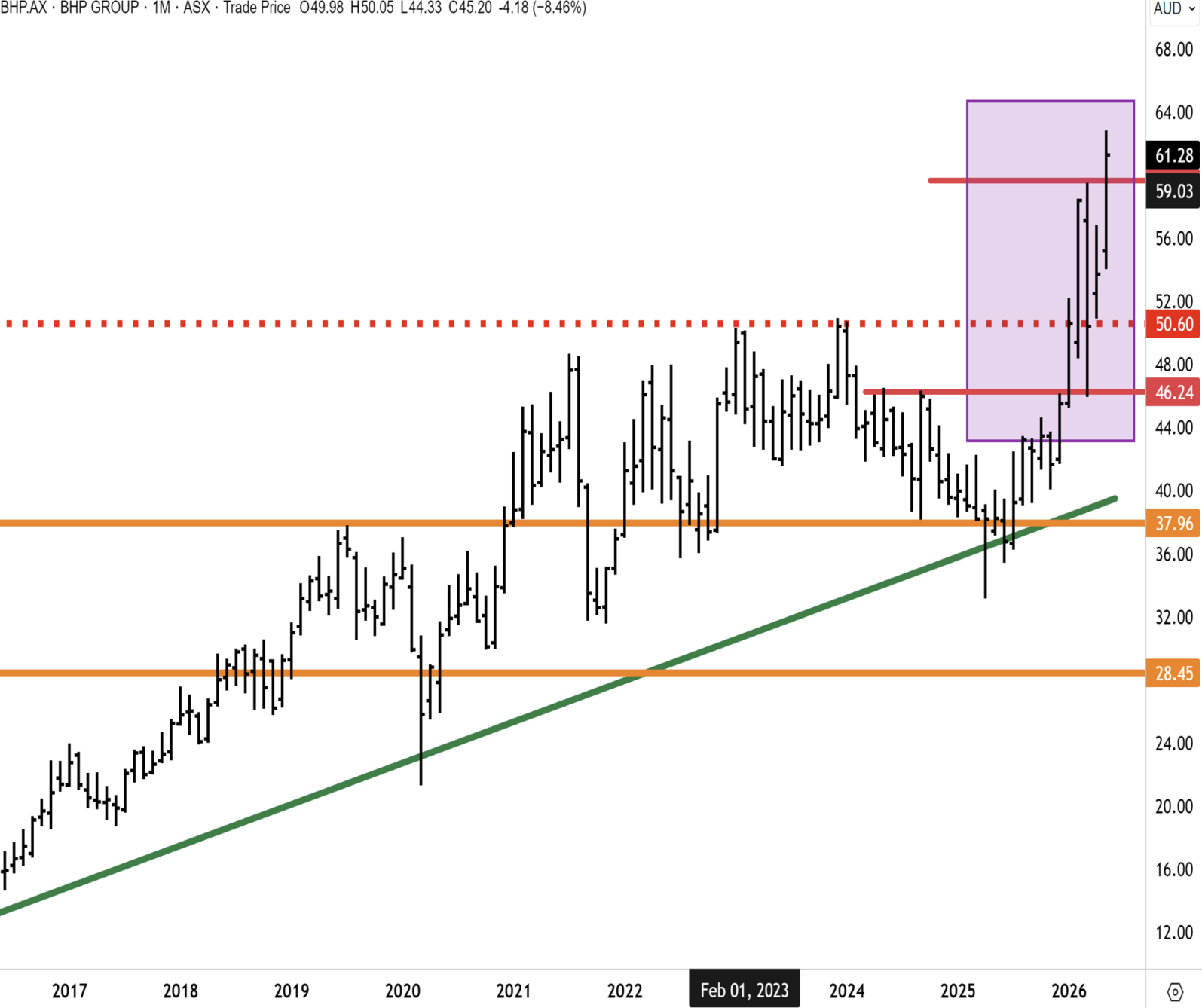

BHP reached a new all-time share price high this month, and the reason is straightforward. Copper has overtaken iron ore as the company’s primary earnings driver. 1H26 profit rose 22%, and the dividend jumped 46% to US$0.73/share. BHP’s copper portfolio, spanning Escondida, Olympic Dam and its broader South Australian assets, gives investors unmatched leverage to the electrification megatrend at scale and low cost. As grids, EVs and data centres drive structural copper demand higher, BHP sits attractively on the global supply curve. Iron ore remains a hefty cash generator, and our contrarian call for more resilience in iron ore pricing than the market consensus here has been on the money.

BHP has made a new record high near $64. Following a successful retest of key support at $50 (being the breakout level), upward momentum has quickly resumed. We have conviction that BHP will extend upwards to new record highs in the months ahead as copper also reasserts upward momentum, iron ore holds up well above $100/ton, and other investment banks join JP Morgan with continued upgrades.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

Have a great weekend.

Carpe Diem

Angus