KEY CONTENT

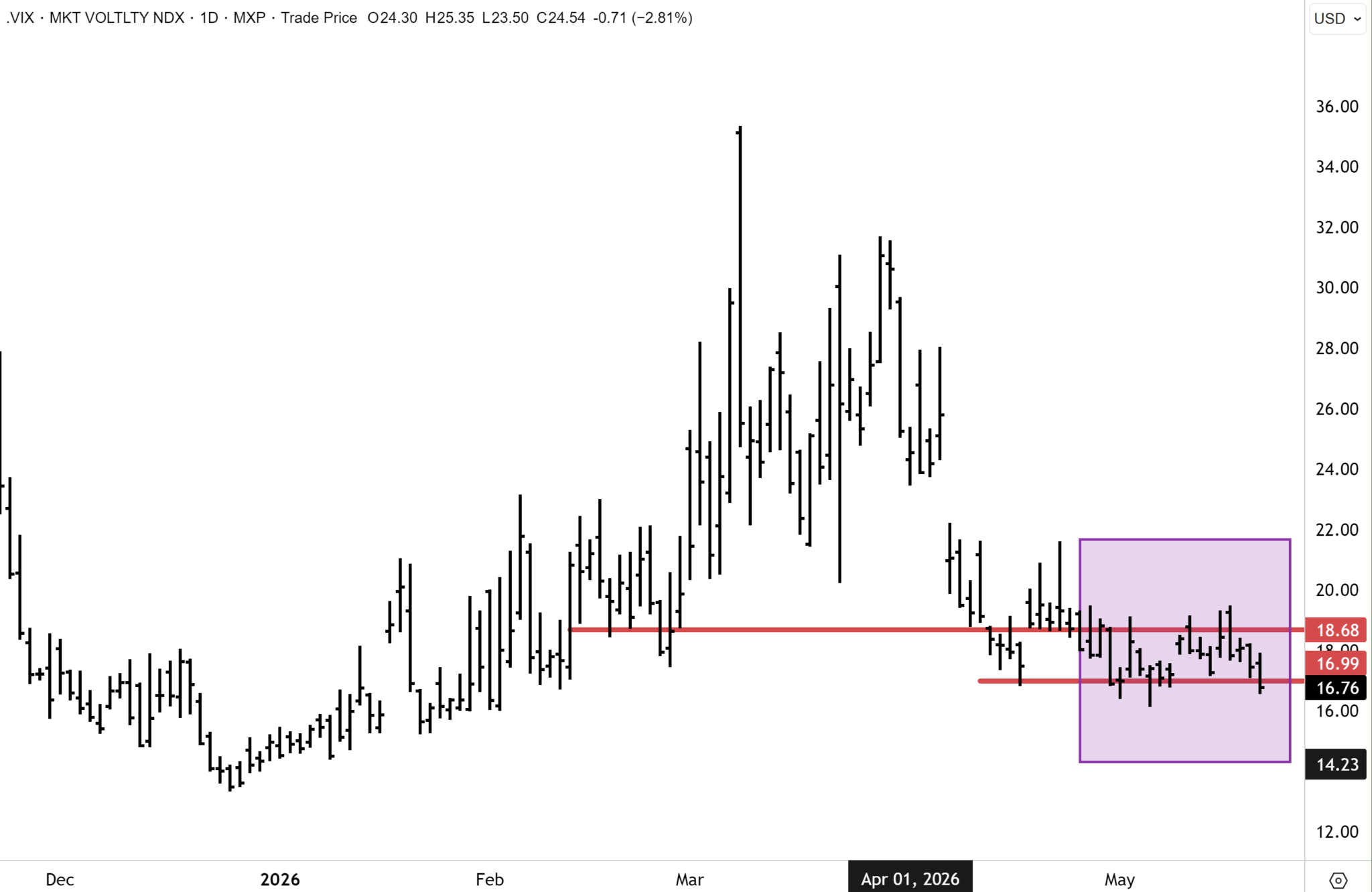

- The bond market blinked first. The 10-year hit 4.66% – the same level that forced the White House tariff reversal in 2025 – then dropped 9 basis points in a single session. The VIX closed at 16.75, its lowest since the Middle East conflict began.

- The structural thesis held. Long resources, energy, gold, copper, Japanese and UK banks, China at a discount – stress-tested by the bond market this week and came through intact.

- Independent confirmation of the supercycle. Jeff Currie, former head of Goldman commodities, calls energy “the biggest asymmetric trade in modern finance” — oil majors at 15.5% free cash flow yields while hyperscalers return none. He sees the supercycle running another ten to twelve years.

- Gold’s correction is in its final phase. Western investors are returning – global ETFs pulled $6.6 billion in April, every region positive. Hard assets are expected to keep outperforming equities into year-end.

- Japan’s largest bank, three consecutive record years. Mitsubishi UFJ – net income up 30%, ROE target lifted to 12%, fresh ¥100 billion buyback. The Bank of Japan rate cycle is still early.

- The ASX surged on bad news. Unemployment hit 4.5% – well above consensus – and the market rallied 1.47% as the RBA terminal rate was repriced sharply lower. Materials +14% year-to-date, Energy +26%. Morgan Stanley 12-month target: 9,250.

REPORT SPOTLIGHT

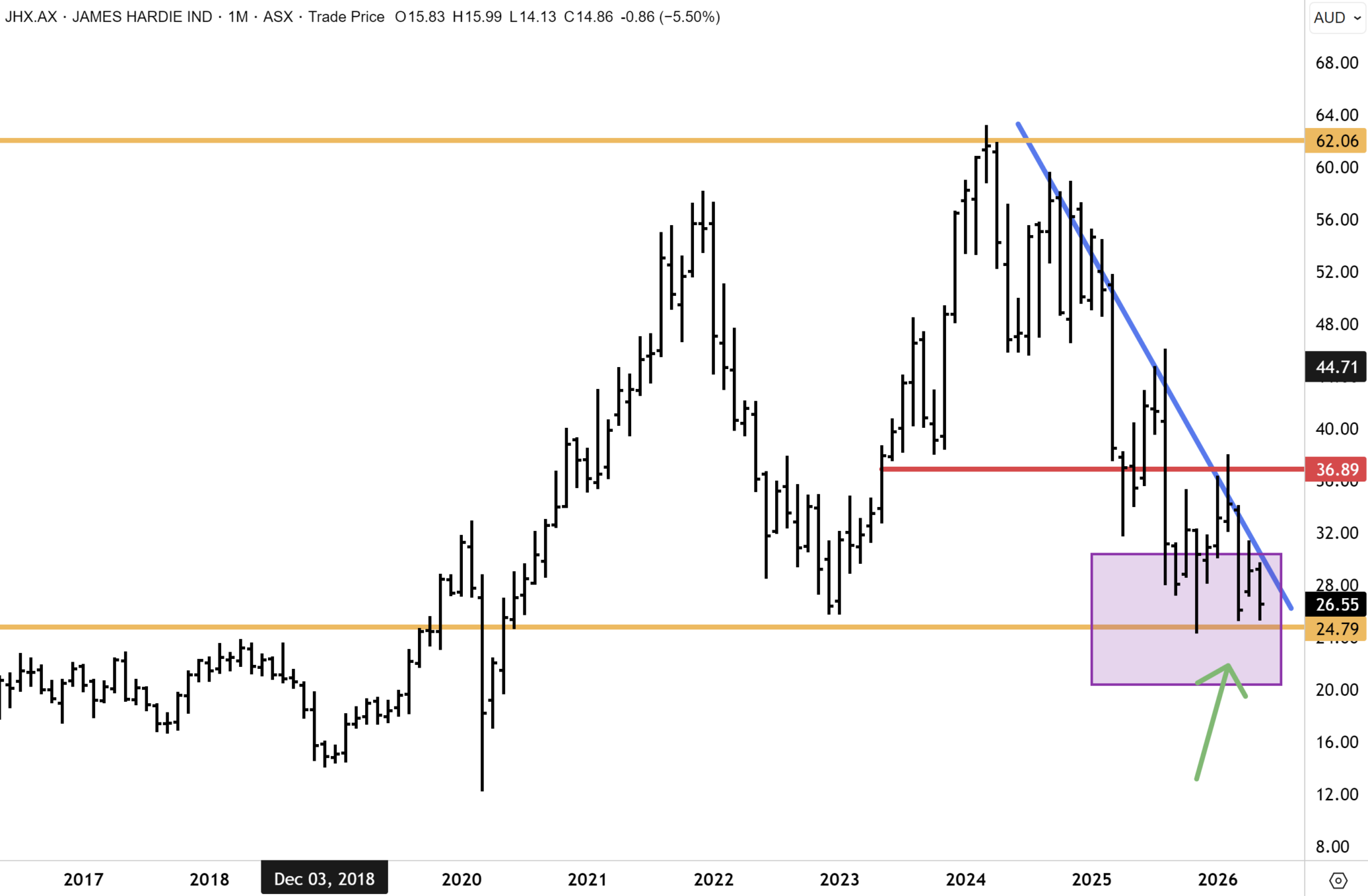

- See how the thesis is moving for James Hardie Industries

This fatLITE covers the headlines. The full research – complete macro analysis, buy recommendations, and model portfolio positioning – is available to members. We’ve been an independent investment research provider for 25 years. If you’re not yet a member, find out what’s included – and why we back it with a 30-day money-back guarantee for new members.

The Verdict

The most important number of the week was not on a stock chart. It was the US 10-year Treasury yield, which punched to 4.66% on Tuesday – its highest in more than a year – as oil-driven inflation reasserted across the yield curve and the bond market began pricing a Federal Reserve rate hike by December at 40% probability. Then on Wednesday, paradoxically, it was a set of hawkish Federal Reserve minutes that delivered the week’s release valve. The 10-year dropped 9 basis points in a single session, Brent crude fell 7%, and the Russell 2000 surged 2.56%. By Thursday, the Dow Jones had printed a new record high, and the VIX stood at 16.75 – its lowest reading since the Middle East conflict began. The S&P 500 closed Thursday at 7,445. The ASX 200, which had opened the week at a seven-week low of 8,505, closed Thursday at 8,621 following its biggest single-session advance in six weeks, driven by an Australian employment report that repriced the RBA terminal rate lower and sent rate-sensitive sectors surging. What the week demonstrated, beneath the volatility, was something more durable. The commodity super-cycle thesis – long resources, long energy, long gold, long copper, long Japanese banks, long UK banks, long China at a discount – ran the bond market’s test and emerged intact.

The Tape

This week, equities absorbed the pressure with considerably more grace than the bond market suggested was warranted. The Russell 2000’s +2.6% surge on Wednesday was the week’s most instructive single move. Small and mid-caps do not lead when the risk-off trade is in control. The market’s internal structure signalled throughout that the earlier panic was a clearing event, not a regime change.

Oil did the most decisive work in commodities. WTI and Brent eased, both responding to diplomatic signals from the Strait negotiations that read as more substantive than earlier in the conflict.

Gold ($4,452/oz) was moderately softer across the week under the weight of a firmer dollar and elevated yields, while copper finished essentially flat at $6.35 per pound. Base metals were distinctly firmer on Thursday, with a +5% surge from tin standing out. While they were volatile across the week, strength is broadening across the base metals complex. Silver and platinum firmed in the final two sessions.

The cross-market pattern of the week was that oil fell because a resolution looked closer. Equities held because the strong earnings picture had already absorbed the conflict’s inflationary effect.

The Calls

The bond market did its best to break the equity rally this week and lost. Remember, the 10-year reached levels which forced the White House policy reversal on tariffs in 2025, the same reaction function we have been talking about for weeks. The VIX closed Thursday at 16.75. The rally was tested, but held.

What makes this week significant is that our structural thesis was stress-tested and came through without revision, intact.

One veteran commodity strategist whom I rate highly is Jeff Currie, who formerly ran Goldman Sachs global commodities division for over a decade. He also believes the world is in the early stages of a commodity super cycle “that might last another decade or more as the artificial intelligence buildout collides with chronic underinvestment in energy and materials capacity.”

Mr Currie said in an interview with Bloomberg this week that “the energy sector presents the biggest asymmetric trade in modern finance because oil companies are returning a 15.5% free cash flow yield while hyperscalers have none. Even with the supply shock now rippling across the globe, the supercycle could run 10 to 12 more years.” I think Mr Currie will be right on this call.

The view here is direct: any weakness in energy names on a Strait reopening and the consequent oil-price correction is a buying opportunity, not a reason to reduce the position.

The copper supply-demand case tightened further this week. Chile – which accounts for nearly a quarter of global mined copper supply – cut its 2026 production forecast by 2% to 5.3 million tonnes, reinforcing the structural deficit that multiple investment banks are already forecasting. We see potential for copper prices doubling over five years against accelerating data-centre and energy-transition demand and constrained supply. The Chile downgrade simply narrows the margin for error. The Global X Copper Miners ETF provides exposure while mitigating the single-producer risk.

In Gold we Trust

Gold’s correction from the February highs above $5,600 is, on the evidence of this week, drawing toward its final phase. JP Morgan’s technical desk arrived at the same destination through the ratio framework: the S&P 500 to gold ratio has sustained its breakdown from the first quarter of 2026 and continues to coil below the 1.50–1.55 level that marked the first-quarter break. By analogy with the hard-asset outperformance cycles of the 1930s, 1970s, and early 2000s – each of which ran for roughly a decade – the current regime is, in JPM’s framing, “relatively young” with no bottom pattern yet forming on the ratio chart. The practical implication: commodities and hard assets continue to outperform equities in the second half of the year.

The Western investor bid for gold is returning visibly – global gold ETFs pulled in $6.6 billion in April, with every region positive and Hong Kong posting a record $732 million in inflows. Holdings are within 1% of the record. The VanEck Gold Miners ETF (US: GDX) captures the mining complex with leverage to the underlying price. Once the headwinds from elevated yields and a firm dollar reverse, and the Strait reopening is the mechanism that delivers both, we see scope for the rally in gold to resume. We remain convinced that gold will close the year above $5,000 and the bull market will resume in the second half.

The Land of the Rising Banks

Mitsubishi UFJ Financial’s full-year result was another bumper set of numbers: net profit up 31% to ¥2.427 trillion for a third consecutive record year, with a return on equity target raised from 9% to 12% and a ¥100 billion buyback alongside a dividend of ¥96 per share. The bank trades at a meaningful discount to global peers despite the clearest structural improvement in its underlying earnings in decades – rising JGB yields unwinding the suppression of near-zero rates that had capped profitability for thirty years. We maintain an overweight position in our Asia and International managed account portfolios.

For readers looking to add exposure to stocks like Mitsubishi UFJ, CMC Markets offers competitive direct access, not just to Japan, but to multiple other international markets.

Onwards and Upwards

China’s equity markets took profits on Thursday after a strong run in semiconductor and AI-related stocks, with the CSI 300 falling 1.4% and the Shanghai Composite declining more than 2%. The pullback is healthy and does not change the bull case. JP Morgan holds a year-end base case of 5,200 for the CSI 300, with the 5,000 level likely retested in the near term. The structural case has three legs: institutional underownership – “uninvestable” was the consensus word two years ago, almost exactly at the low – abundant liquidity as international investors return, and a combination of AI infrastructure super-cycle spending and a green-energy capex build-out. The hyperscalers at the centre of the AI rollout – Alibaba and Baidu – carry accelerating cloud growth and trade at a material valuation discount to US counterparts.

The Local

The ASX 200 opened the week at a seven-week low of 8,505 and closed it at 8,621 after Thursday’s surge of 1.47% – the best single session in six weeks.

The immediate catalyst for Thursday’s session was domestic. Australia’s April employment report delivered a double miss that the equity market received as good news: the unemployment rate climbed to 4.5% – the highest reading since November 2021 and well above the 4.3% consensus – while payrolls fell 18,600 against forecasts for a gain of 17,500. The labour market is softening faster than the RBA anticipated. Money markets repriced the RBA terminal rate from approximately 4.85% at the end of April to around 4.6% by Thursday’s close. Rate-sensitive sectors responded immediately and directly – real estate’s 2.2% advance on the session was a function of the repriced rate profile. Our view is that the unemployment rate has further to go on the upside as government hiring slows and the private sector continues to shed roles. Once energy costs recede with the Strait reopening and inflationary pressure eases, the RBA’s path back to a dovish easing bias opens. The employment print on Thursday was the first data point in that direction.

The mid-week selloffs in gold miners and copper names proved to be orderly position clearing rather than any fundamental reassessment. Materials is now up more than 14% year-to-date, the second-best performing sector on the ASX (pipped by energy at +26%), and Morgan Stanley’s mid-year upgrade this week – overweight resources, 12-month ASX 200 target of 9,250, bull case of 10,325 – provides the institutional view. We see the resources sector as doing the heavy lifting and have multiple buy calls across the sector, including the heavyweights – BHP and RIO. I expect resources to do more heavy lifting this year, with the ASX 200 plausibly still hitting 9,300 by December.

The budget’s negative gearing and CGT changes continue to weigh on the domestic backdrop. The banks remain a cost-out story in our view and will stay defensive, supported by steady and heavyweight dividend power.

The Watch

The Middle East negotiations remain the pivotal event to monitor, along with the flow-on for bond yields. Secretary Rubio confirmed “good signs” in talks by week’s end. The White House is expected to defer the uranium issue under the pressure of cost-of-living polling and mid-term election dynamics – the bond market, the VIX, and oil are all reading it that way. Every basis point on the US 10-year next week is a real-time vote on whether that market consensus is correct.

Watch for Federal Reserve speakers. The minutes confirmed more officials leaning toward a hike than the market had priced, yet bonds rallied on the release. The AUD/USD cross around 71.1c catches a strong bid if December hike pricing continues to fall.

In Australia, the flash PMI data confirmed what Thursday’s employment report suggested – services slipped into contraction for only the second time in three months. Watch the domestic CPI trajectory on Wednesday.

The Spotlight

James Hardie Industries (ASX: JHX) – BUY

FY26 adjusted EBITDA of $1,265.8M came in above the top of the $1,232-$1,263M guidance range, with Q4 adjusted EBITDA up +42% year on year. Free cash flow of $314.1M cleared management’s “at least $200M” target comfortably, with FY27 guidance of at least $500M. Cost synergies from the AZEK acquisition are running well ahead of schedule, with an annualised run rate of approximately $80M against an original FY26 target of $42M. Pricing held across Core Siding and Trim throughout the volume weakness. Net leverage sits at 3.48x, with management targeting 2.0x or below by September 2027. At roughly 11x forward EV/EBITDA in a housing trough, the valuation is undemanding.

Since our last update before the ME conflict, James Hardie has found support above the 2020 breakout level near $25. We have conviction that James Hardie is tracing out an important bottom, with several successful retests of the $25 level failing to breach support. We remain confident that JHX is close to confirming an important inflection and that a major bottom is close to being established. Despite the failed earlier breakout in February, we remain confident that JHX will soon break through resistance and resume upward momentum.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. New members can try it with a 30-day money-back guarantee.

Have a great weekend.

Carpe Diem

Angus