- The Strait of Hormuz may be about to reopen. Oil fell, gold surged, bonds rallied, and equities ran. Four asset classes, one trade, one day. We explain what’s been priced in, what hasn’t, and what the second half looks like from here.

- Morgan Stanley’s Mike Wilson was in Sydney this week. He made a call that cuts across portfolios. We heard him and many others directly – and we have a view on where they are right, and where they have stopped short.

- There is a number in the oil market that, if broken, removes the last argument for higher interest rates. It’s closer than most investors realise.

- Gold had its worst week in months, then a strong rebound. The pattern that formed on the chart has a name and a track record. We explain.

- All four major Australian banks fell on Thursday. A record short position now overhangs the sector. Has the crowd got it wrong?

- This week’s report spotlight covers Downer EDI, where a business transition is underway. Demand drivers are durable: energy transition, defence, population growth and ongoing infrastructure outsourcing by governments and private owners alike.

This FatLITE covers the headlines. The full research – complete macro analysis, buy recommendations, and model portfolio positioning – is available to members. We’ve been an independent investment research provider for more than 25 years. If you’re not yet a member, find out what’s included – and why we back it with a 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

The Verdict

The market got what it needed. Not a resolution, but at least a reprieve. President Trump announced from the White House on Thursday that a US-Iran agreement could be signed over the weekend and the Strait would reopen. Both sides have compelling reasons to reach a deal, which are intensifying as the conflict lengthens. Markets don’t require closure to move higher. They require that the thing most likely to push yields higher, keep the dollar strong, and drain liquidity gets removed from the equation, and on Thursday, it did.

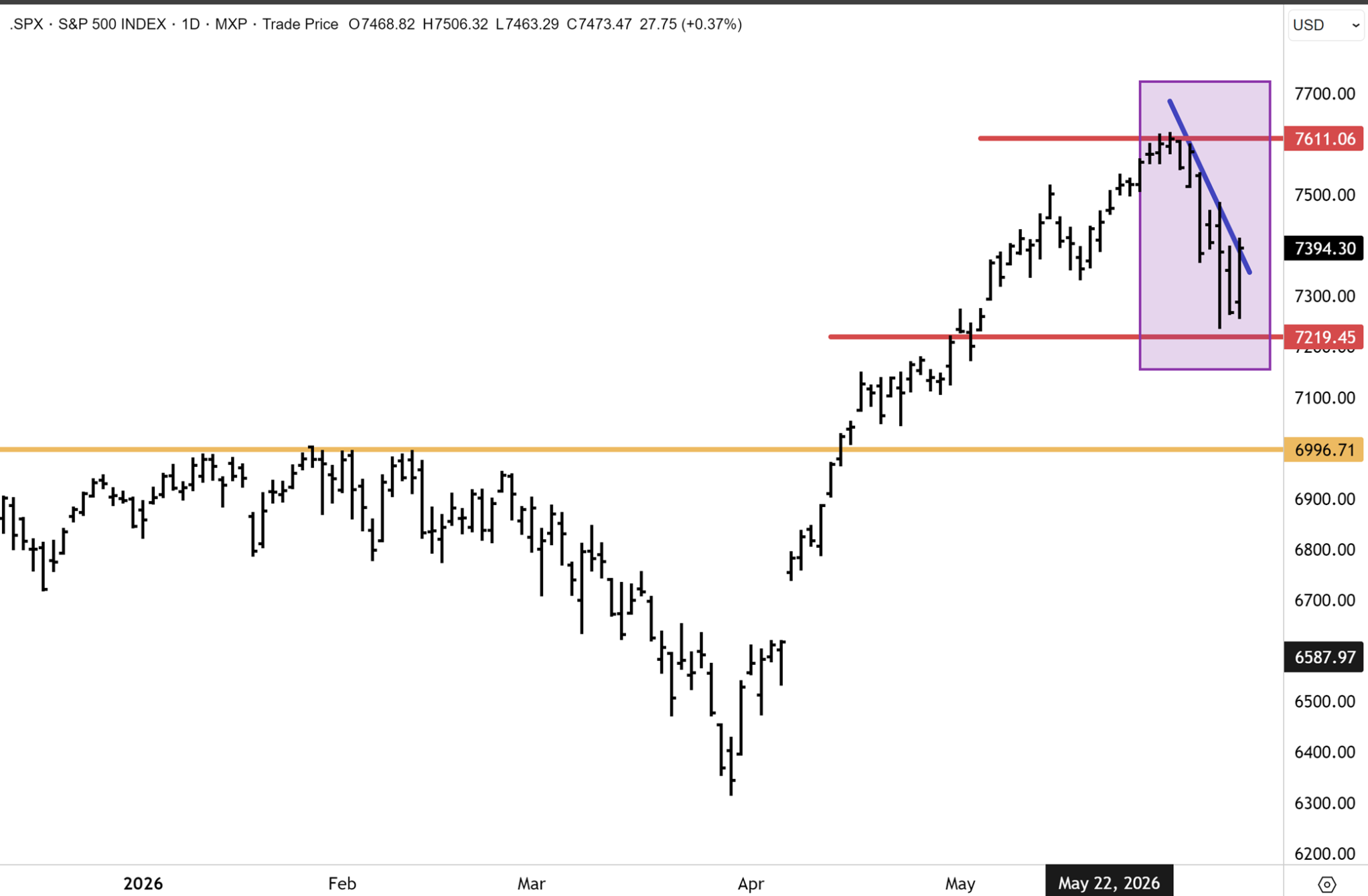

The response was immediate and broad. The S&P rallied +1.75%, the Nasdaq was up +2.54%, and the small-cap Russell 2000 led at +3%. WTI broke down 4%, the ten-year fell back through 4.50% to 4.46%, and gold rebounded 3.5% off Wednesday’s levels, which smelled of capitulation selling. That is not just a relief bounce in one market. Rather, it is the same bet expressed across many asset classes that had been pricing the Strait closed. Around midday on Friday (the time of writing), the ASX200 had rallied roughly +1.9%.

Petraeus and Kerry, at the Morgan Stanley Australia Summit this week, mapped the logic directly. The US is running out of targets, munitions are running low, and no president four months from a midterm election stays in an unpopular war that is being felt intensely in voters’ wallets. A deal was always coming. Thursday moved us closer again.

What changes now is the direction of travel on those three variables. Oil falls, the dollar eases, and yields follow. That is the second-half setup, and investors need to ask if they are positioned for it.

The powerful upside dynamic in the SPX on Thursday might point to the correction from the record highs above 7,600 now being over. A positive debut for SpaceX tomorrow could soon see the US benchmarks retest the record highs. I attended the Morgan Stanley Australia Summit this week, where CIO Mike Wilson flagged a correction of between 5% and 10%. But the market might pull up short of this target (with the lows now being in) should the Strait reopen in the coming weeks.

To trade international shares, you can open an account with our partner CMC Markets, which provides access to 15 global markets. If you join today, you can also receive $300 in free brokerage for domestic trades.

The dominant conviction of the week is one we have held in one form since late February, now arriving at its payoff. The closure of the Strait was always going to end, and its ending was always going to be the catalyst that releases the pressure on oil, the dollar, and bond yields simultaneously. The signal had been building for days. On Tuesday, oil fell sharply even as a US helicopter was shot down, the first notable time since the closure that escalation failed to lift crude, and on Wednesday, WTI managed only a 2.5% gain in the face of an escalation, a muted response where months ago the move would have been violent. By Thursday, WTI broke downward toward the $85 support. A clean break there opens a fast move to the February breakout near $70. That is the number that matters, because oil at $70 removes the last argument for higher rates and is a handoff for strong H2 for equities.

Both WTI and Brent oil are retesting key support levels that might soon be broken on the downside. Brent crude is retesting the $89 support and looks highly vulnerable to a technical downside break in my view, which could see prices quickly retreat towards the mid-$70s should the Strait reopen.

Gold had a week that tested the nerves. The metal fell to $4,085 on Wednesday in trading with every hallmark of capitulation, then rebounded 3.5% on Thursday off the same March and April lows it made earlier in the year. A double bottom appears to have formed, and it matters because the floor is what confirms the next upward leg. The downtrend from the record highs still needs to break on the topside, and it intersects near $4,250, so the work is not finished, and the dust may take weeks to settle.

The structural case has not weakened. The PBOC extended its buying streak to nineteen months in May, the longest since 2015, and central-bank diversification away from the dollar remains intact regardless of the war. JP Morgan and Ed Yardeni both target $6,000/oz by year-end. Our own view is more measured, anticipating that gold surpasses $5,000 by December with a chance of retesting the $5,600 record, and that $6,000 is more plausibly a 2027 outcome. A reopening that weakens the dollar is the catalyst that resumes the cycle. The ASX expressions are the majors that absorbed the selling all week, Northern Star, Evolution Mining, and Newmont. Money was flowing back into the local names on Friday, alongside mid-caps we like, such as Genesis Minerals, Vault Minerals, and St Barbara.

The US correction is now most likely behind us. Morgan Stanley’s Mike Wilson, whom we heard directly at the Summit, made the sharpest point of the week. This year’s drawdown was far more severe in valuation than in price. In other words, PE multiples fell sharply, but this was masked by rising earnings per share estimates.

Mike Wilson set an 8,300 target over the coming six months, argued the earnings recovery is broad rather than concentrated in AI, and flagged the One Big Beautiful Bill as a capex tailwind. His clearest call, and one we share, is rotation. As bond yields fall, leadership moves back toward old-economy cyclicals, financials, and consumer discretionary names.

Finally, Yardeni upgraded the S&P 500 materials sector to overweight, noting it is just 1.9% of the index, so even a small rotation sets it up for an outsized move, against a 2026 earnings growth forecast near 40%. The read-across to heavily resource-endowed benchmarks, the ASX 200 above all, and the FTSE 100 is direct. The Summit I attended this week reinforced it from a different angle, with materials and mining placed at the centre of the AI infrastructure build-out. The local exposures are the diversified majors BHP and Rio Tinto, and the copper names that were sold on profit-taking through the week, 29Metals, Sandfire Resources, and Capstone Copper. BHP’s relative resilience is the tell that the smart money is already positioning.

The ASX trended moderately lower for much of the week, but the composition underneath was anything but quiet, with a tilt towards defensives, banks under pressure and gold miners thrown out with the bath water. That was turning around mid-session on Friday, with the All Ords Gold the top-performing sub-industry (+4.9% at the time of writing) and the banks also capturing bids. The financials and materials sectors are the heaviest weighted, so the benchmark ASX200 was enjoying a strong rally.

It is worth noting that all four major Australian banks fell on Thursday, dragging financials down 1.45% and making the sector the single largest drag on the index. Westpac led the decline at minus 2.6% after disclosing a contraction in investor home lending since the federal budget, with CBA off 2.4%, ANZ 2.1%, and NAB 1.8%. A record short position of around $12 billion now overhangs the sector, built on the most significant changes to negative gearing and capital gains tax in three decades.

This is where we part company with the consensus. The crowd is short the banks, but we are not bearish on them. A reversal of the negative gearing changes is a real possibility at the next election, and mortgage rates may fall sooner than most economists expect. We heard Treasurer Chalmers at the Summit project unemployment holding at current lows, and we think that is too optimistic. The rate is more likely to carry a five-handle within a year, a view Charter Hall’s David Harrison put even more bluntly at 5.5%, and if either of us is right, the RBA will be cutting aggressively by the middle of next year. That is the opposite of a bearish setup for the banks once the budget noise clears.

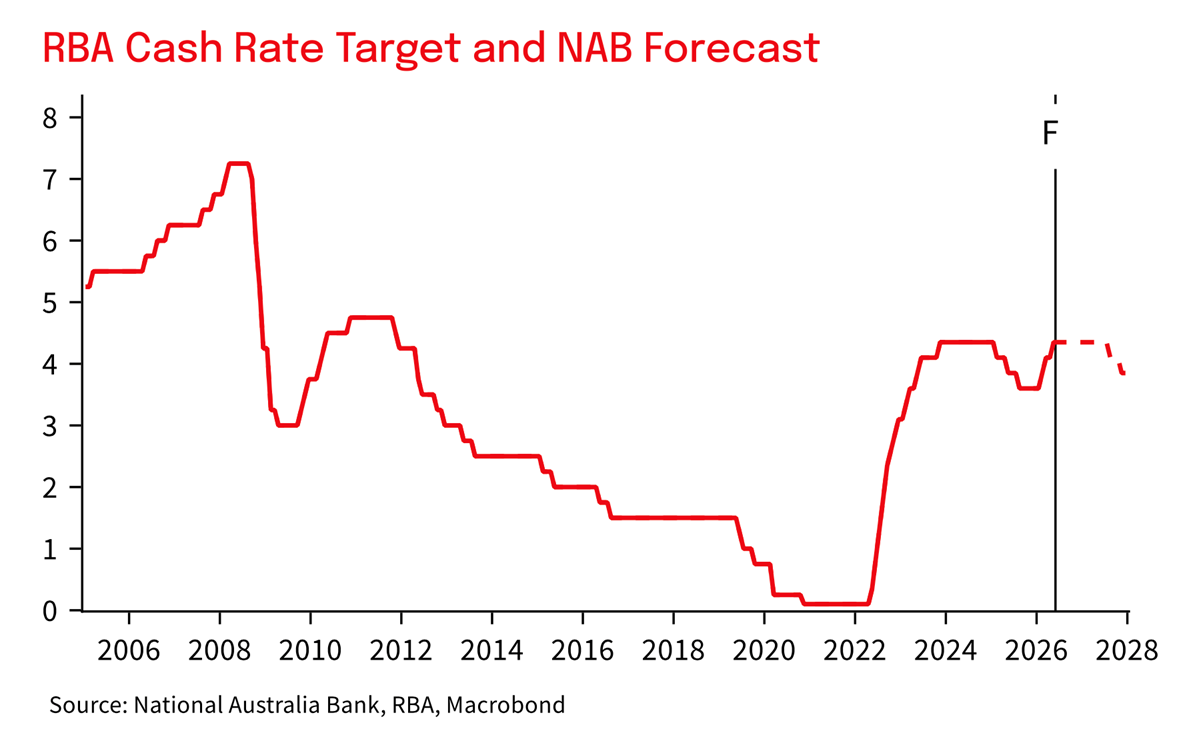

NAB has already walked away from its August hike call, now seeing the cash rate peaking here at 4.35% with the next move down rather than up, a call we share. Chief economist Sally Auld notes the conditions that justified tightening back in February no longer exist, and NAB’s shift reinforces our own view that a commodities super-cycle is underway. The RBA decides on Tuesday (June 16).

REPORT SPOTLIGHT

Downer EDI (ASX: DOW) – BUY

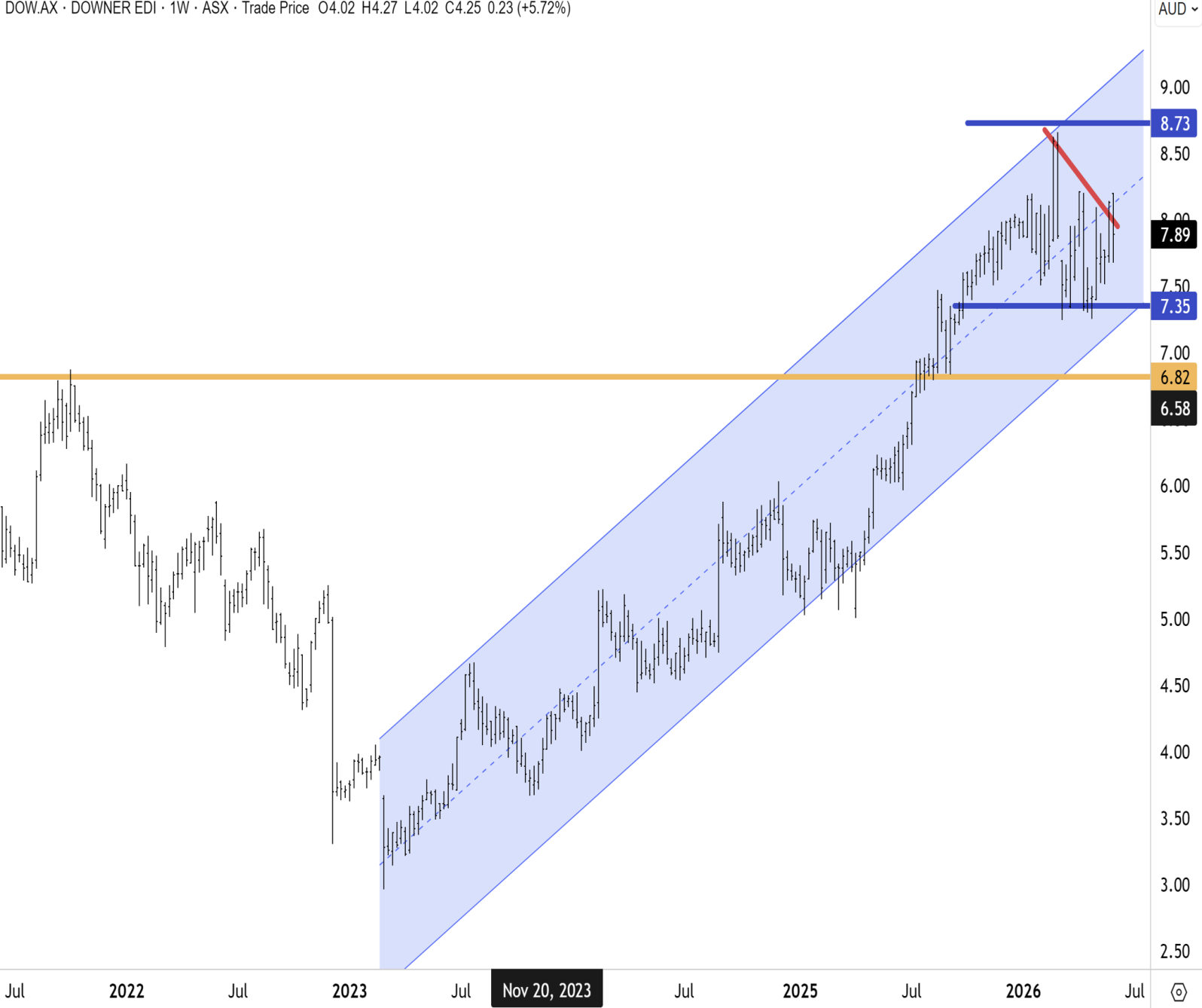

Downer has secured a $310 million contract to maintain Transurban’s key northern Sydney toll roads for up to nine years from July 2026, covering the M2 Motorway, Lane Cove Tunnel and NorthConnex. Combined with existing Melbourne contracts spanning CityLink and West Gate Tunnel, Downer is now Transurban’s primary maintenance partner on both sides of the country. This kind of contract defines Downer’s strategic transformation. Long-dated, recurring, capital-light maintenance work with a blue-chip client replaces the risky fixed-price construction contracts that caused write-downs in prior years. The shift is producing results. Downer now manages 50,000+ kilometres of road networks across Australia and New Zealand, and total shareholder returns have exceeded 33% over the past year. Demand drivers are durable: energy transition, defence, population growth and ongoing infrastructure outsourcing by governments and private owners alike.

Little has changed with Downer on the charts since our last update back in March. Downer made a new high above $8.58 and sequentially pulled back to test and successfully held above key support at $7.20. We remain constructive in our technical outlook for Downer, which continues to rise within an established trend channel. We remain confident that Downer will extend higher this year and into new record territory with the shares retesting overhead resistance above $8. A breakout above this level would mark the resumption of upward momentum.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

Have a great weekend.

Carpe Diem

Angus