- The S&P 500 is within a whisker of record highs – even as 20% of global oil supply sits blocked in the Strait of Hormuz. Markets are voting for earnings over geopolitics.

- Q1 earnings season is running hot: 15.6% growth across reporters so far, the strongest since 2021, with 82% beating consensus. The number is rising.

- The real test starts next week. The Magnificent Seven haven’t reported yet.

- Gold is reasserting its bull market. Three structural engines: US bond market imbalance, central bank buying, and a weakening dollar. Target: $5,000

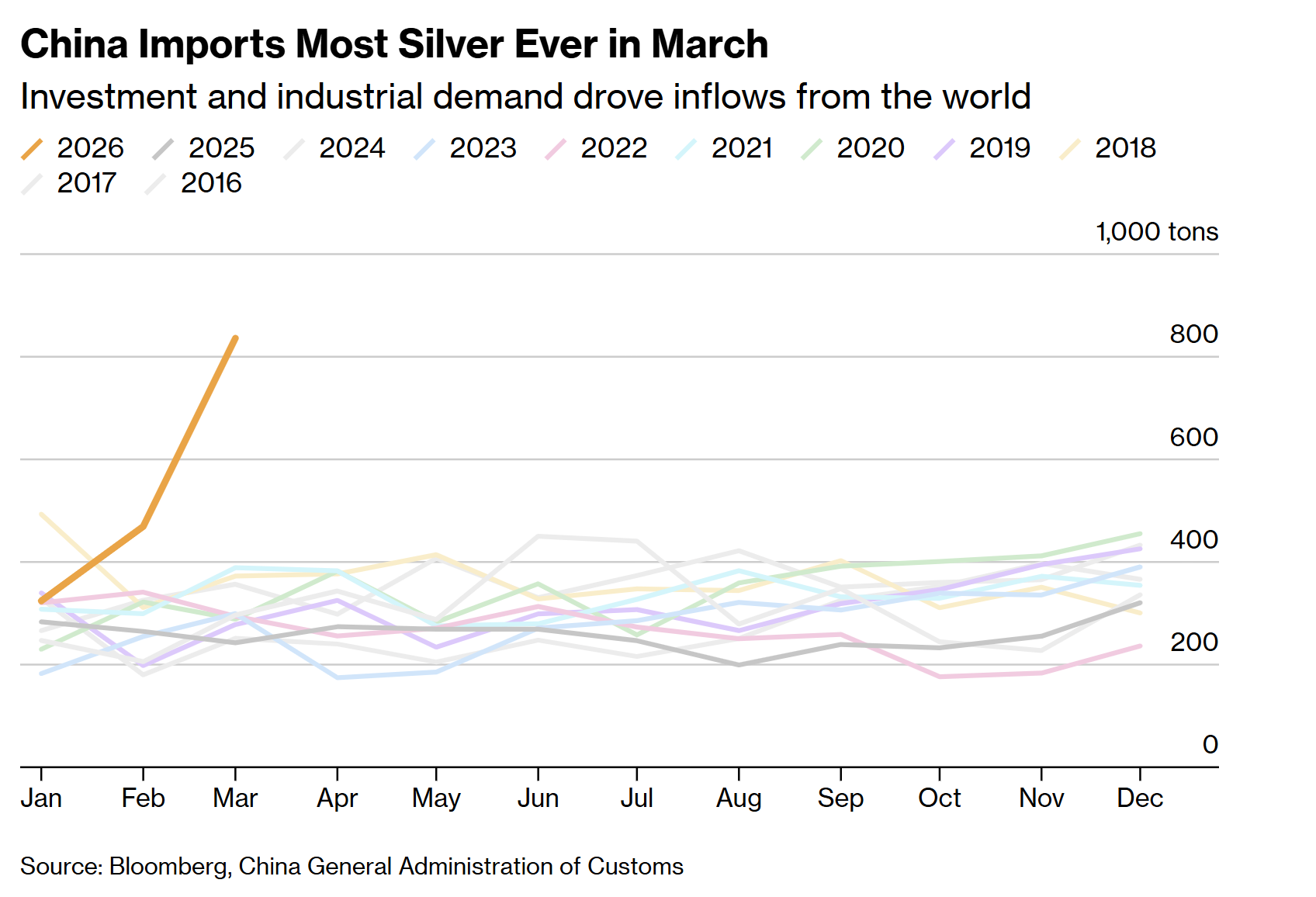

- Silver is in its sixth consecutive annual supply deficit, with Chinese industrial and solar demand driving imports to nearly three times the ten-year monthly average.

- The AI efficiency story is accelerating – two major hyperscalers announced combined cuts of 23,000 roles this week.

- The ASX200 sat out the global rally this week, closing around 8,793. The domestic market hasn’t caught the wave yet.

- Japan’s Nikkei touched 60,000 this week. JPMorgan’s 70,000-year-end target no longer looks heroic.

REPORT SPOTLIGHT

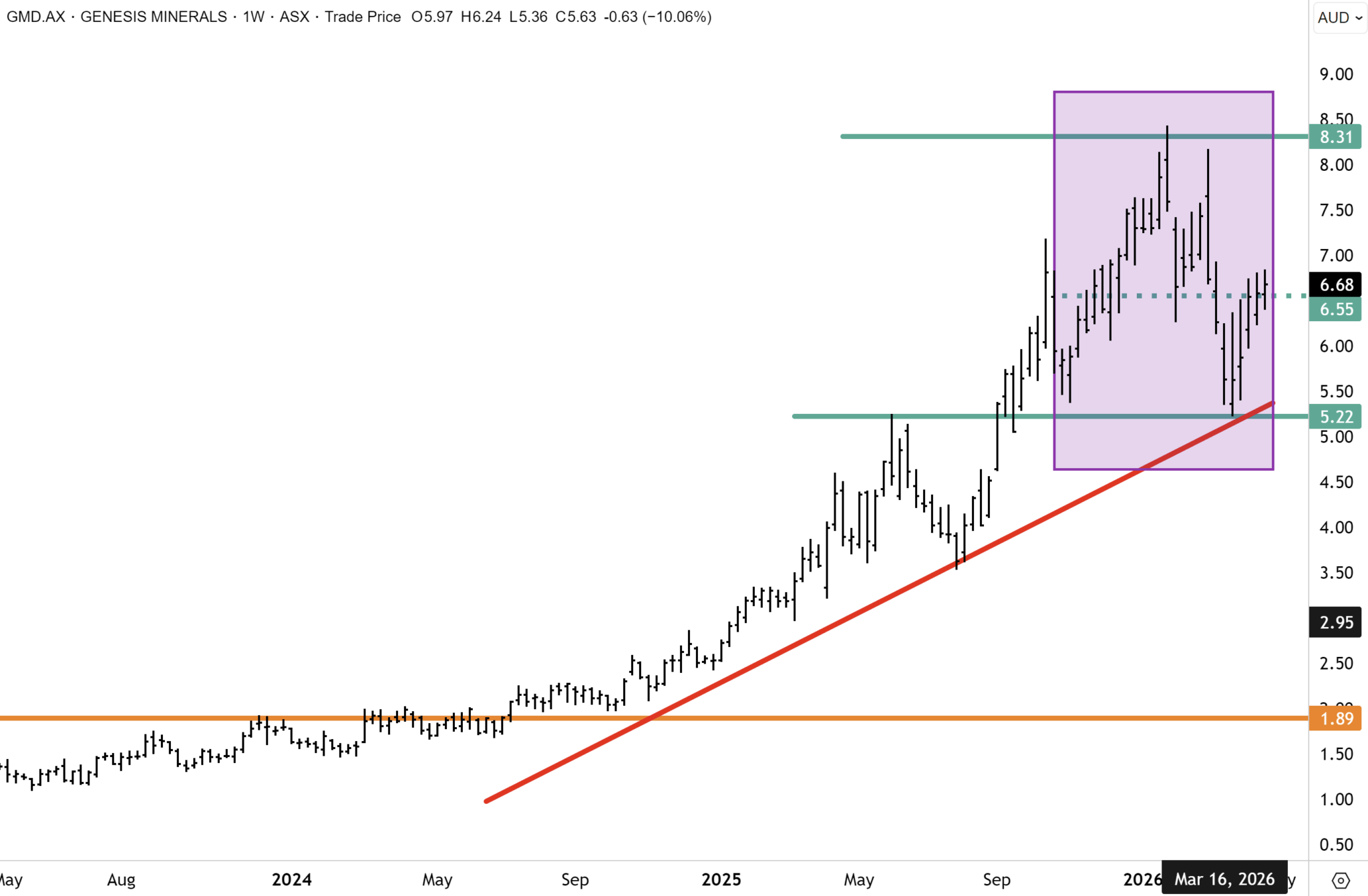

- Genesis Minerals (ASX: GMD) – upgrade to buy

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join on our Products page.

Twenty percent of the global oil supply remains shuttered by a naval blockade that shows no sign of lifting in the Strait of Hormuz, the world’s most important shipping lane. It was reported on Thursday that a senior Iranian government negotiator resigned. Oil surged 4% on Thursday. The S&P 500 closed on Thursday within a whisker of record highs.

Spend a moment with that contradiction. It is a market running its own calculations and deciding on a very different answer to mainstream media headlines. With 123 of the S&P500 companies having reported, earnings are growing at 15.6% – the strongest quarter since 2021, and rising, revised upward from 14.4% at the start of the month. 82% of those companies have beaten consensus estimates. The market is concluding that this is a more powerful force than a naval blockade.

The DXY is rolling over toward 98, with hedge fund positioning overwhelmingly long non-dollar assets. The Bloomberg Commodity Index at 136.5 is building toward another leg. Copper approached record territory before consolidating. Wheat broke higher on fertiliser supply constraints that are not going away. Japan’s Nikkei touched 60,000 this week – a number that would have seemed implausible eighteen months ago – before closing at 59,140 on Thursday. JPMorgan’s 70,000-year-end target, raised this week, no longer requires a leap of faith to accept. We have been Japanese bulls for the past few years. For Australian investors, the week carried an uncomfortable asterisk. While global markets were pricing conviction, the ASX 200 dipped across the trading sessions – down to 8,793 by Thursday. The global rally has not yet found its way home.

The Magnificent Seven – collectively above 30% of the S&P 500 by weight, some deeply discounted from their October peaks – have not yet reported. The sideline cash that watched the recovery without participating in it is waiting. The ignition sequence is running. Whether the launch happens depends on what these companies say next week when they begin reporting.

Goldman wrote over the weekend that “the S&P 500 has staged a powerful rebound from its late-March lows, rising more than 10% to hit fresh record highs,” adding that “we think we move now from macro and geopolitics back towards micro.” This has been the Fat Prophets playbook for several weeks.

JPMorgan remains constructive on equities and sees the Russell 2000 leading, followed by the Nasdaq and then the S&P 500. Within sectors, the bank favours Tech and Cyclicals – with the Magnificent Seven and Semis poised to move sharply higher. Consumer discretionary names, including homebuilders and retailers, represent the best near-term upside within Cyclicals. Financials could see a multi-week rally on strong earnings and a bull-steepening yield curve. Precious metals would likely see a strong rebound as the USD depreciates.

JPMorgan also noted this week that investor interest in AI stocks hasn’t been this high since the first half of 2025. We have conviction that the extensive selloff in US and global technology stocks has ended and that the key players have bottomed. One has to be selective. We are sticking to the highest quality names where value has emerged and where companies carry a large defensive moat. Microsoft, for example, fell 40% from its October 2025 peak to the March trough. We added Microsoft and Meta Platforms to the Fat Prophets Global Contrarian Fund and global managed account portfolios. We also concur with JPMorgan that US homebuilders – including James Hardie – could rebound if the Fed moves on rate cuts later this year. On the geopolitical front, JPMorgan believes the bar to restarting the conflict is particularly high, making the tail risk of military escalation considerably thinner from here.

Sharp correction selloffs within a primary bull market create great buying opportunities. While sentiment can turn acutely bearish during these corrections, it is essential to hold the line. Standing back across a 40-year career, this pattern is predictable. We hold significant conviction that equities and risk assets are in a bull market that could endure for some time.

The second leg of this rally has not started. The first leg – short covering, hedge removal, position squaring – is well underway. The more powerful move, fresh capital deploying into beaten-down quality at reset valuations, has not yet begun. The ignition switch is the Magnificent Seven earnings season, which opens next week.

Thursday’s announcement that Meta Platforms and Microsoft would cut a combined 23,000 positions was initially misread. The market sold both stocks due to AI disruption concerns. That reaction missed the point. The fact that hyperscalers of this size can reduce headcount at this scale points directly to AI efficiency gains flowing through from years of substantial investment – AI is allowing both companies to do more with fewer people. Both stocks have been punished for six months on fears that capex spending was destroying free cash flow permanently. That spending tapers sharply once the AI buildout nears completion. When analysts rebuild their models to reflect a permanently lower cost base and falling capex requirements, the free cash flow picture brightens considerably. With both MSFT and META sharply down from their record highs and valuations now much lower, we see opportunity – and extend that view to beaten-down, high-quality technology companies globally, including WiseTech, Xero, Alibaba, Tencent Holdings and Baidu.

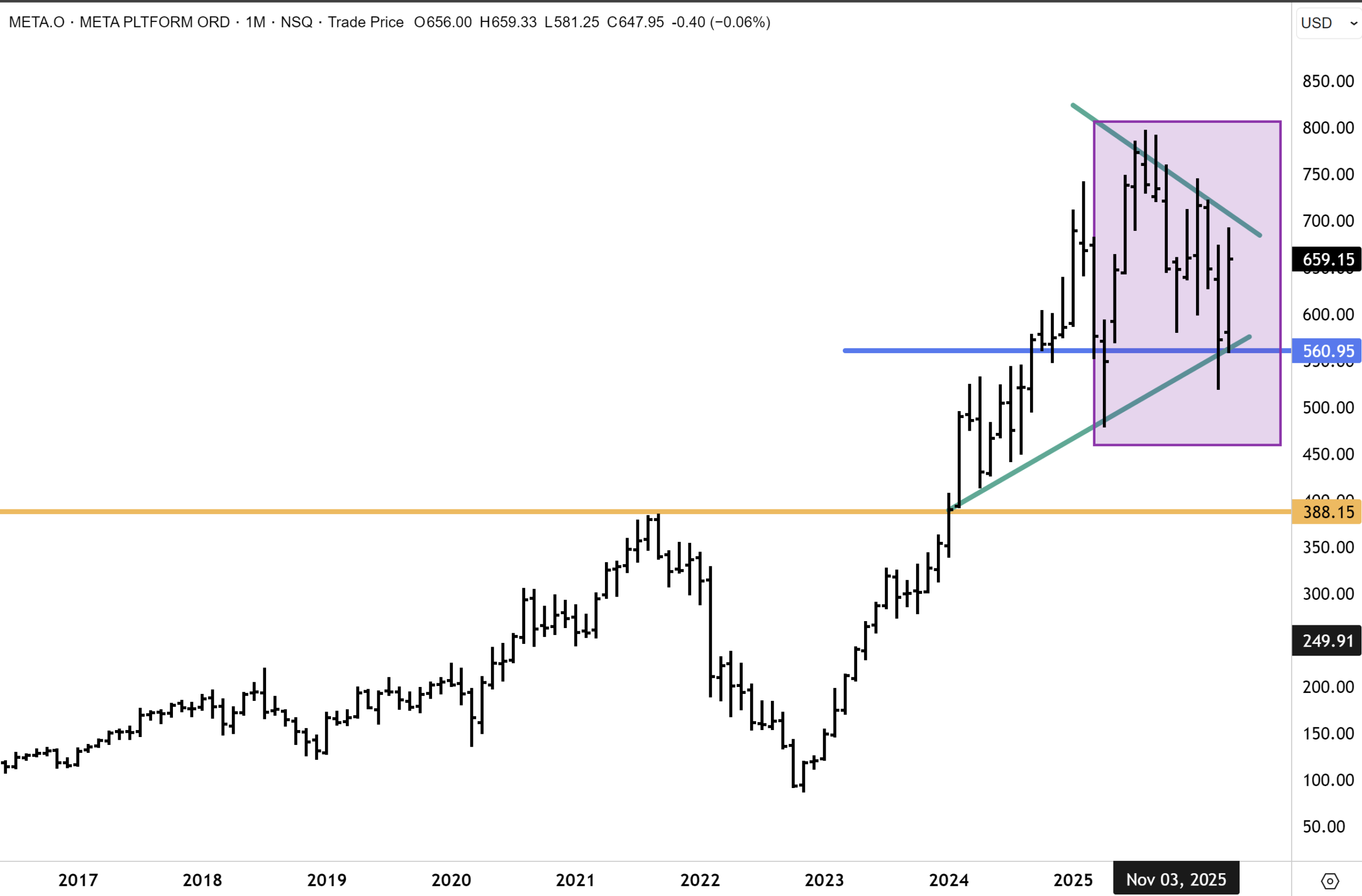

Meta Platforms has resumed upward momentum but remains within its trading range. A topside breakout above resistance at $660 could see the record highs around $800 quickly retested if Wall Street endorses the earnings result and the AI investment narrative.

Meanwhile, Gold is reasserting its bull market, and a retest of $5,000 is the base case within months. From capitulation lows of $4,100 in March, the metal has run to $4,700. Thursday’s slight pullback changes nothing structurally.

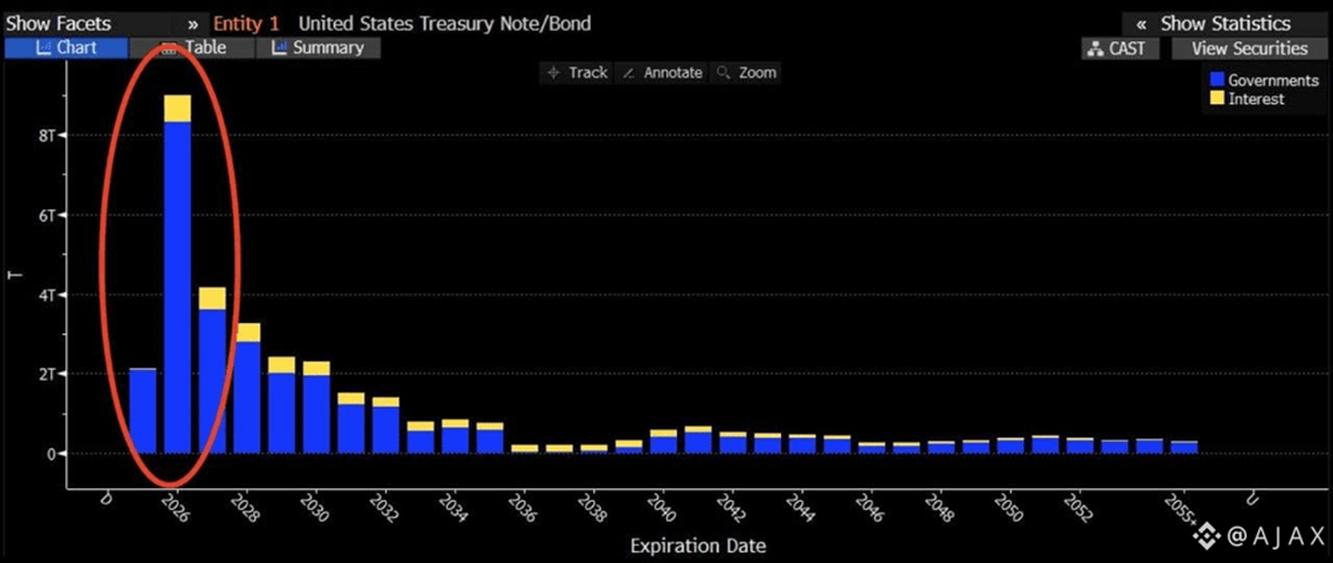

Three engines are running simultaneously that support gold. Mohamed El-Erian’s thesis centres on a fundamental imbalance in the US bond market – a six to seven percent GDP deficit rolling over at higher yields with foreign buyers in structural retreat.

El-Erian has been specific about the pressures: While he views former Treasury Secretary Paulson’s warnings of a “vicious” bond market crash as alarmist, he acknowledges the demand-side problem is real and accelerating. In February, Chinese regulators urged domestic banks to scale back US debt holdings.

Central bank reserve diversification toward gold has been building since 2022 and continues to accelerate. The third engine is the dollar – the DXY breaking below 98, with the next key support at 96. The upward trend in gold appears to be firmly resuming. Our base case is for the $5,000 level to be retested within months.

Silver is the leveraged expression of the same thesis, with an additional structural driver. China imported 836 tonnes of silver in March against a ten-year monthly average of 306 tonnes – driven by retail demand for small silver bars as an alternative to expensive gold, and by solar manufacturers front-loading production ahead of export tax rebate changes. The solar industry consumes roughly a fifth of the annual global silver supply and is overwhelmingly concentrated in China. Global demand for solar is bound to keep rising following the oil shock, and the electrification and AI buildout will require considerably more power over the coming decade.

While global markets have been rallying, the ASX 200 fell this week, closing Thursday at 8,793 – down 0.57% on the day at mid-Friday, about -2% lower over the past trading week. April flash PMIs confirm the economy is holding, with improvements in the headline numbers for each. Manufacturing returned to expansion at 51, Services at 50.3, though Middle East shipping disruptions pushed local input cost inflation to its highest level in nearly four years.

Our copper conviction runs through BHP (see below), Rio Tinto, South32 and Sandfire Resources. The gold bull market is expressed through Northern Star, Evolution Mining, Vault and St Barbara. The energy and uranium thesis sits in Santos, Woodside, Paladin Energy and ATOM. For investors looking for ASX exposure to the AI efficiency and beaten-down quality technology thesis – the same structural shift driving the Meta and Microsoft case – WiseTech Global and Xero have sold off well beyond what their fundamentals warrant and stand as the most direct local expression of that global call.

Genesis Minerals (ASX: GMD) – upgrade to buy

Genesis Minerals posted a record A$252.8m cash build in the March quarter, and we’ve upgraded to BUY. Production of 67,497oz at an AISC of A$2,685/oz keeps the company firmly on track for the FY26 midpoint, while a A$4,070/oz margin at current gold prices confirms this is a cash machine, not just a growth story. The balance sheet (A$599.9m cash, zero bank debt) enters the Magnetic Resources acquisition from a position of strength.

Since our last technical update on Genesis Minerals, the shares endured a sharp drawdown in March along with the gold price and the global gold mining sector. GMD put in an important low of $5.20 at the primary uptrend during the steep March correction after hitting a record high above $8.30. GMD has since rebounded to hurdle resistance around $6.50. We have conviction that GMD’s correction is now over and that upward momentum is now resuming. GMD could quickly retest the record highs in our view, should spot gold advance back above US$5000/oz.

This fatLITE edition is a condensed version of our full weekly Wrap, which includes deeper positioning analysis and more targeted investment opportunities. A subscription also includes 4 daily market commentaries during the week and reports on stocks, ETFs and special reports spanning Australasia, Mining and Global Equities.

Have a great weekend.

Carpe Diem

Angus