Domino’s Pizza (ASX: DMP)

![]()

On the release of 1H23 results Domino’s Pizza’s share price has declined sharply. We digest the results and review our recommendation.

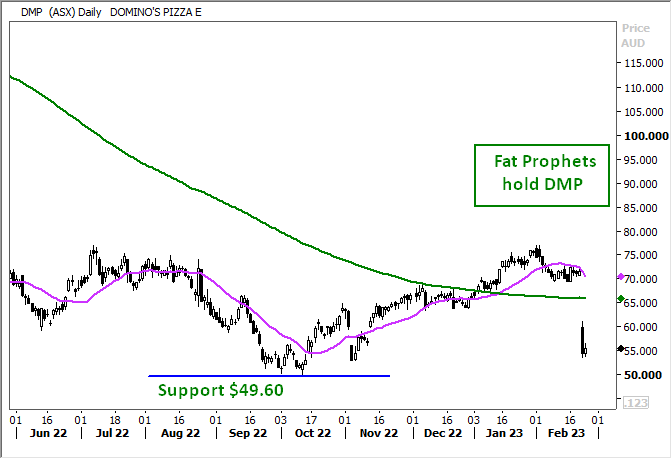

The Daily view of DMP highlights the breakaway gap towards the major support level of $49.60, current price movements remain within the multi month consolidation range between $49.60 and $75.0.

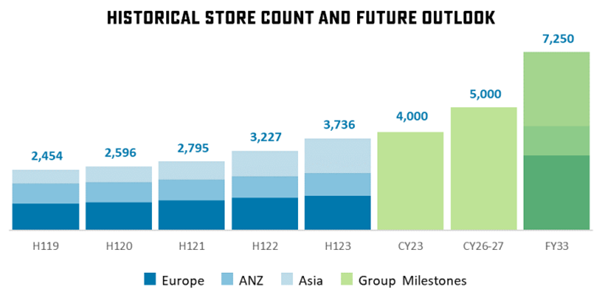

From the beginning when Domino’s pioneered the phone app for ordering pizza they have remained on a consistent expansionary mission to increase store fronts across the globe. Late 2022 Fat Prophets FAT-AUS-1100 reported Domino’s were conducting a A$150m capital raise to buy out the remainder of Domino’s Pizza Germany. The company maintains a 10 year outlook for over 7000 store fronts by 2033. Current projections include over 3000 extra stores or over two times the current market size in Europe and 3000 stores throughout Asia again over two times the current market size.

Source Domino’s

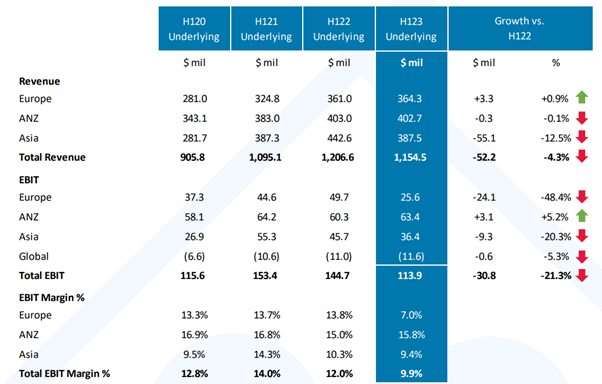

Domino’s 1H-23 revenues in the Euro region have increased 0.9% against the other Australian New Zealand segment -0.1% and the Asia segment revenues declining -12.5% , resulting in an overall 4.3% total revenue decline.

Source Domino’s

Source Domino’s

The overall performance is being impacted by the surge in inflationary pressures particularly in Germany with the latest YoY inflation reading accelerated to 8.7%, with central banks responding by lifting interest rates, the cost pressure on business and the consumer is beginning to take its toll.

Although network sales came in 1.3% higher [subscribe_to_unlock_form] the reduced customer counts has resulted in decreased food volumes leading to higher costs managing inventory.

As a result the company has passed on higher delivery and food production costs with the outcome a reduction in Domino’s customer counts, and a significant move to store pick up against using the delivery service, management have stated this has not met expectations with the decline including online sales of A$1.52b also -4.5% against 1H-22. Same store sales declined an average -0.6% primarily attributable to lower performance in the Japanese market, sales revenue from Japan also being impacted by the 12.6% weaker Yen v’s the AUD.

Net Debt increases by $95.8m vs. FY22, as a result of the Malaysia and Singapore acquisitions and dividend payment, partly offset by $163.2m net capital raising.

Current net debt is A$666.5m resulting in a Net leverage ratio of 2.1% remaining well within the company’s banking covenant. In addition, Domino’s completed a Capital raising of $163.2m net, during H123, to be used primarily to fund the acquisition of remaining shares held by Domino’s Pizza Group plc in the German joint venture this is forecast to complete 2H-23. The earlier capital raising also in part funded the Malaysia and Singapore acquisitions for A$10.1m.

Looking at the Asia segment sales increased 3%, the newly acquired markets in Malaysia and Singapore are performing at expectations, with Management intending to apply high volume marketing mentality to store operations.

Within the Australian New Zealand network sales came in marginally lower by 0.3% to A$687.3m. Going into 2H -23 the company has stated commodity and labour increases are anticipated going out to FY-24 with the focus on short-term energy prices.

The Monthly view of DMP indicates the current price decline has moved back to test the long term up trend line, current price has moved below the 12 month moving average, currently the stock remains with a primary up trend.

In the current economic cycle management remain confident the strategy of building improved performance through marketing to increase customer counts and sales is sound.

We hold the view fast food sales will remain a staple in the global diet and make the point the industry as a whole will be working through this current inflationary cycle. Currently the company is moving prices higher and expanding offerings to maintain customer numbers.

We maintain our Hold recommendation for Members with exposure. Domino’s will remain in the Fat Prophets portfolio.[/subscribe_to_unlock_form]