Fed up with the lockdown

With much of the world still in varying stages of their lockdowns, ‘stay at home’ stocks continue to do well. This includes many of the well branded ‘quick service restaurant’ operators, who are enjoying strong take-away and delivery demand as many people literally get ‘fed up’ with cooking. This has also provided a strong earnings offset in most cases to dine-in operations which largely remain shuttered.

This has certainly remained the case for our two key QSR exposures in the Fat Prophets Portfolio, in Collins Foods and Domino’s Pizza Enterprises. Both have released positive trading updates over the past 10 days, including one from Collins out earlier today. This has continued a stellar rebound in the shares since March – Collins has rallied almost 75% since the March lows. Domino’s which didn’t see as much downside during the pandemic, is up around 27% since the March lows. The market has rightly recalibrated the fact that drive-thru/takeaway account for the lion’s share of turnover, and is thriving amidst the lockdown.

With talk of restrictions easing, can the upward share rerating process continue?

We believe it can, and expect the high quality QSR operators such as Collins and Domino’s however will likely continue their rollout plans, helped by the fact rents are set to fall given the likely closures of some more traditional retail outlets. The lower price point and ‘brand comfort’ of KFC and Domino’s will also come into their own if people look for cheaper ways to eat out and in.

Both companies will arguably talk up the Covid shutdown as a “unique opportunity” to grow and expand into the high street retail vacuum where “choice sites” are becoming available at attractive rents.

We retain buys on both Domino’s and Collins Foods cover off their most recent updates below:

Collins Foods has provided another Covid update earlier today, and it makes for very encouraging reading. The trading period covered is the last five weeks of FY20, being from Monday 30th March to Sunday 3rd May 2020.

Management reports that KFC Australia has continued to show improvements in sales trends. Same store sales (SSS) were down only marginally at -0.9% despite many Food Courts having been heavily affected due to the significant decline in shopping mall foot-traffic. Excluding the net effect of Food Courts, the remainder of the network (predominately drive-thru restaurants) traded positively, with +4.0% SSS growth over prior year. Increased drive-thru and home delivery sales more than offset any negative impact from the current Government ban on ‘dine-in.’

[emaillocker]

KFC drive thru queues in Sydney

Over in Europe ,management reports that the German KFC restaurants continue to trade through take-away, drive-thru and delivery channels whilst certain Government restrictions have reduced dine-in turnover. SSS for the five-week period was -28%, a hefty fall, but a sizeable improvement over the initial sales drop at the onset of Covid-19. Sales continue to strengthen.

In the Netherlands, where dining in is banned, SSS for the last five-week period was -40%. Collins has been impacted by having a high degree of central city exposure, and these areas have been quiet. However, excluding these, the drive-thru restaurants have performed comparatively well, with SSS around -15% over the last five weeks of FY20.

Elsewhere, management notes that Taco Bell (which is in the early stages of a multi-year rollout plan) has seen sales rebound to pre-COVID levels. Sizzler Australia, has also now implemented take-away and home delivery services.

All in all, the update is very encouraging from Collins Foods, with sales in Australia performing very well, and the European operation starting to see an improvement. The expansion plan in the latter is clearly in a holding pattern for now, and we are not surprised to see that a key exec, Newman Manion, has transitioned back to a non-exec role. His appointment was always meant to be temporary and we are not concerned by this. We however continue to see tremendous upside earnings potential with Collins Foods’ European operation (and indeed Taco Bell in Australia), longer term.

The issue in Europe for now is that drive-thru is not as prominent in the overall mix. As a result, management has taken actions to ‘preserve cash’, minimising operational expenditure, and delaying capital expenditure where possible.

A positive for Collins is that Europe is a much smaller part of the pie versus Australia (which has around 6 times the revenue). While the expansion may now go into a holding pattern (and possibly until Covid-19 ‘flattens out’ or a vaccine is produced), the European footprint offers substantial blue-sky earnings potential in our view.

Meanwhile the Australian business is going well, and will likely maintain the previous momentum (robust same store sales growth) once restrictions are removed, and people are ultimately encouraged to go outside more.

Regardless of the timeline for the restoration of dine-in, Collins Foods is well placed in our view. We believe that Collins Foods’ business model is relatively defensive with its digital and delivery channel having built up and making substantial progress (and accounting for the majority of ‘normal’ turnover). It also helps that a number of food delivery apps are readily available to support this channel. This is also as the company’s balance sheet remains strong.

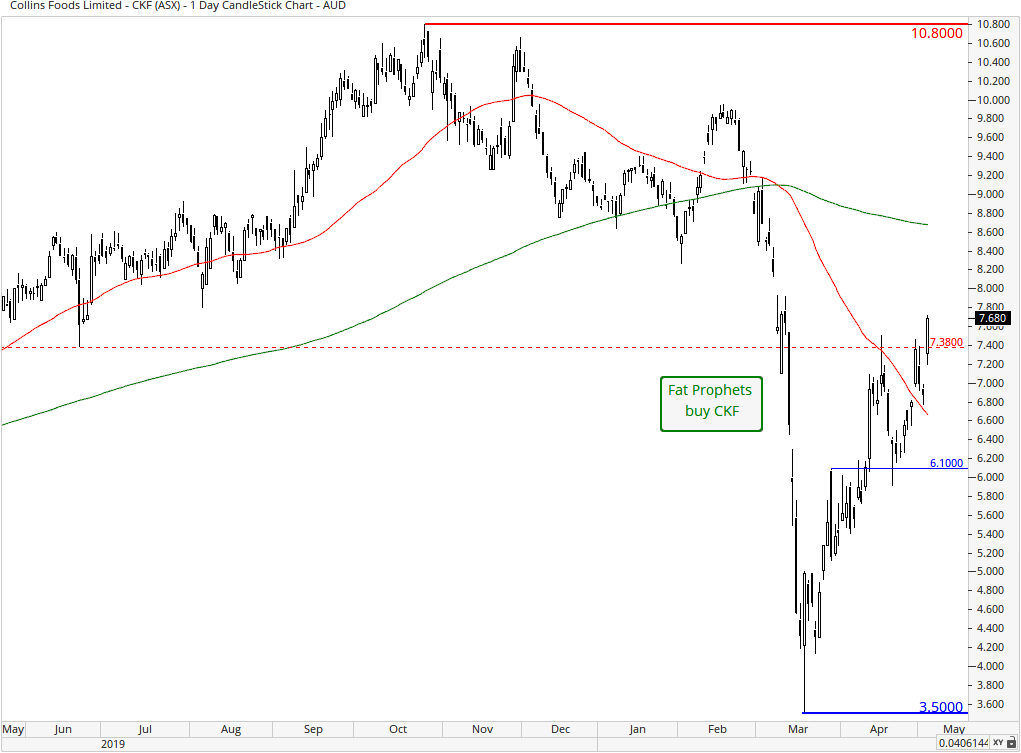

On the daily chart of CKF, the support line on the daily around $7.38 gave way during the virus crisis, and a bearish moving average crossover (where the 50 day (red line) goes below the 200 day (green line)) has evolved. Strong support however was encountered at the multi-year lows around $3.50, and has provided the foundation for a decisive bounce. A move back above the resistance line at $7.38 confirms the tide has turned upwards.

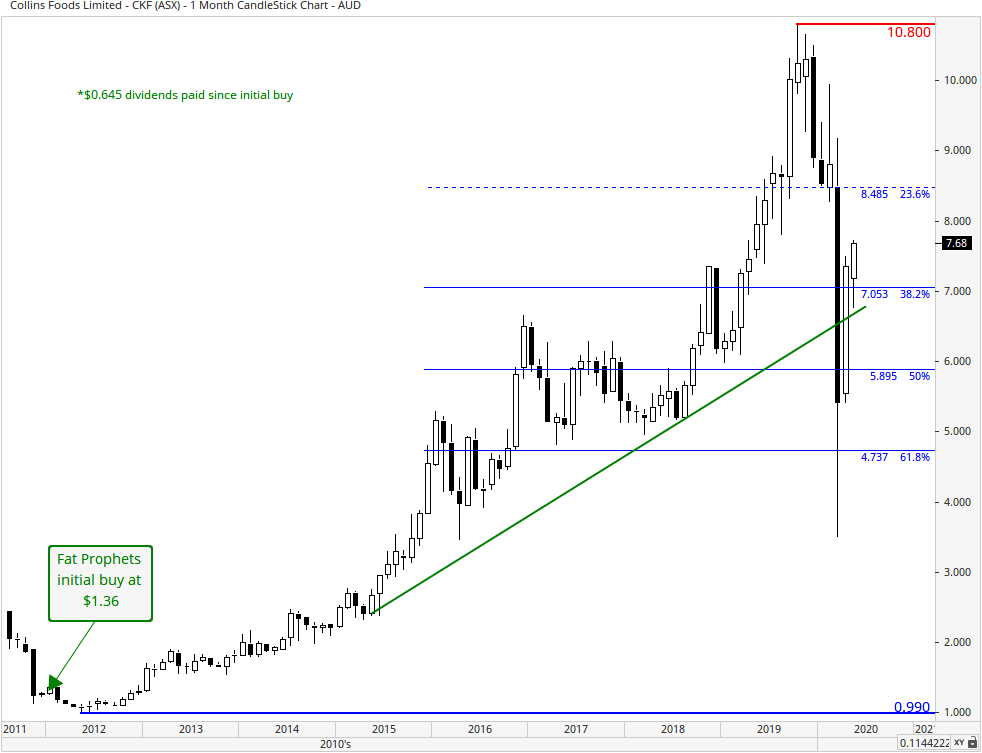

With reference to the monthly chart, support provided by the longer term uptrend has given way during the virus crisis, as did that at the 50% Fibonacci retracement of $5.89. This has since been reclaimed recently, and a move above back above the 38.2% Fibonacci at $7.05 and above the long term support line, confirms that the correction has run its course, and momentum is back with the bullish camp.

We retain a buy on Collins Foods for Members without exposure.

Shares in master franchiser Domino’s Pizza Enterprises have also performed well over the past month. While operations offshore have been impacted by the lockdown, delivery services have mostly continued unabated, and the company is also well positioned with Covid-19 infection and fatality rates plateauing in many countries. This is also while in Australia, delivery and takeaway sales will have been going strongly.

Domino’s released another Covid-19 update on 24th April, and the company reported strong progress across a number of geographies.

Australian performance, of course, has been in full swing during the lockdown as it relates to food delivery, which is the crux of the company’s business model. SSS in Australian have remained ‘consistent’ at a national level. Across the Tasman NZ has had an effective ban on food deliveries (supermarkets the main exception), but this changed last week.

The kiwis have moved to a ‘Level 3’ lockdown and opened up for contactless food deliveries. As we have suggested this has seen a ‘surge’ in pent up demand for well branded ‘take-aways’ such as Domino’s. The company was well and truly prepared for this, and had offered 1,000 new jobs as part of the reopening. Anecdotally there has been strong demand for all things take-away in NZ in the first week of Level 3.

Meanwhile in Japan, food delivery is allowed and companies are scrambling to keep up amidst the pandemic. Domino’s Pizza Japan is aiming to take on 5,000 part-time employee including delivery drivers and 200 full-time employees from April to June. The company has more than 600 outlets in Japan, but it plans to expand to 1,000 over 2025-8. The company’s latest Covid update said that the sales performance in Japan has remained strong. The company is, as is the case elsewhere, pushing the message hard that is delivery measures are ‘safe’ and ‘contact-free.’

Source: Domino’s

Source: Domino’s

In Europe, the story is similar. Delivery is allowed in Germany, and it has been leading the region. Re-openings have also occurred in France in the first week of April, with 70% of the store footprint in the country back up and running. Benelux sales have been more affected by a move away from carry-out sales. With Europe also starting to come out of the worst of the crisis, we believe that well branded delivery companies such as Domino’s should continue to flourish, as people’s sensibilities, and perhaps also pockets, may demand.

The company’s low price point means that its offering is relatively defensive even should consumers emerge from the lockdown with greater caution over the economic outlook and their expenditures. A strong store roll-out plan will also still likely occur over the next few years. And with more traditional retailers (e.g. clothing and other non-food retail stores) likely to come under pressure (and potentially shutter) as the consumer becomes more ‘wallet conscious’, ‘defensive foodies’ such as Domino’s may also benefit from the ensuing downward pressure on commercial rents.

While Covid-19 will have taken some momentum out of sales growth as the Domino’s targets $3 billion in sales this financial year, we continue to favour the stock. Indeed, we continue to see international growth as a key strength. The company has not provided short term guidance, but sees the ‘medium term’ outlook as unchanged, with new store openings up 7-9% this year, SSS +3-6%, and net capex of $60 to $100 million. Liquidity remains strong and Domino’s has undrawn committed debt facilities and cash in excess of $260 million.

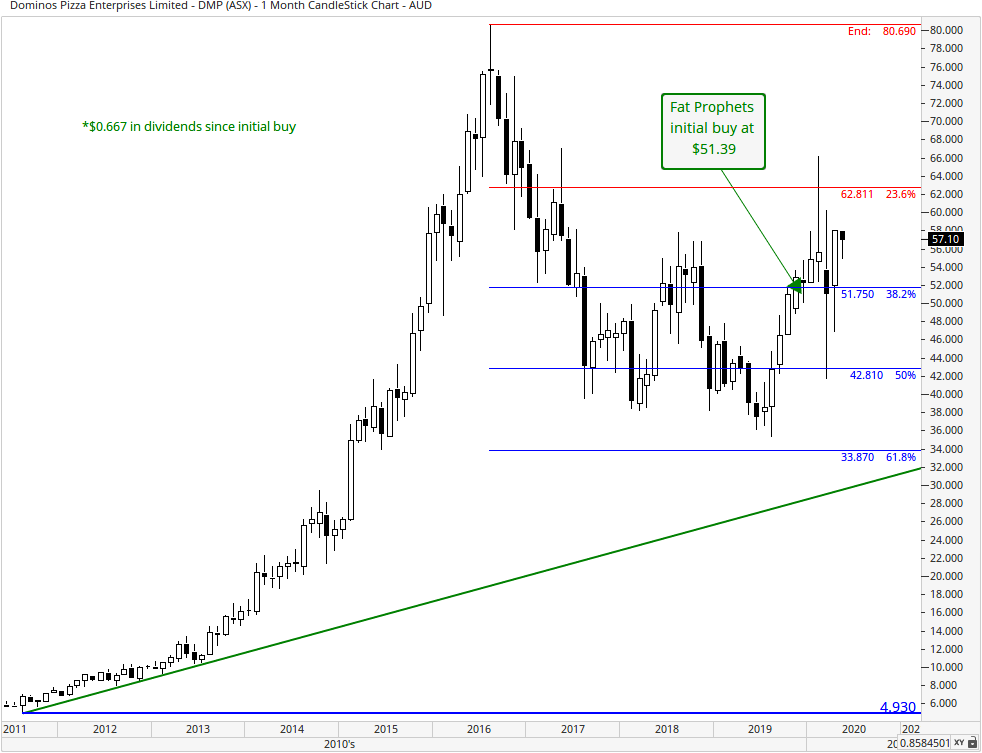

Turning to the charts, and on the daily, DMP staged an upside reversal in August last year, coincident with a bullish moving average crossover (where the 50 day (red line) goes up through the 200 day (green line)). This has seen resistance around $47.85 cleared and provided the basis for further upside momentum.

On the monthly chart, after hitting highs around $80 in 2016, the stock entered a multi-year corrective phase. This appears to have terminated earlier last year, with support at the 61.8% Fibonacci at $33.87 not tested. A move above the 38.2% Fibonacci at $51.75, and towards the 23.6% Fibonacci at $62.81, since our initial coverage bolstered the outlook further, and opened up the way for further gains. This remains the case given the support region around $51.75 (which has recently been tested on the downside) has been reclaimed.

We continue to recommend Domino’s Pizza Enterprises as a buy for Members without exposure.

Disclosure: Interests associated with Fat Prophets hold shares in Colins Foods and Domino’s Pizza Enterprises.

[/emaillocker]