Global stock markets have performed solidly overall in 2024 as the American economy continued to run smoothly, and investors began anticipating a global interest rate-cutting cycle, which has begun playing out across many economies, albeit not in Australia just yet due to stubborn inflation. The Australian economy has proved resilient in an aggressive rate-hiking cycle, but headline GDP figures were bolstered by immigration and elevated government spending, masking a GDP per capita recession. Still, stocks have climbed, and the benchmark ASX 200 set new record highs during the year despite having pulled back slightly over the past two weeks.

As of 17 December 2024, the ASX200 was up approximately +9.5% year-to-date, although there have been wide divergences in the performance at the sector level, which we dive into more detail about later.

The key question on every investor’s mind heading into 2025 is when the RBA will begin its pivot. We believe there is a good chance now that the RBA will ease at the next meeting in February, although our overall view will not change if that is pushed down the road for a few more months. However, we will continue to monitor coming data for inflection points that provide opportunities and pose risks.

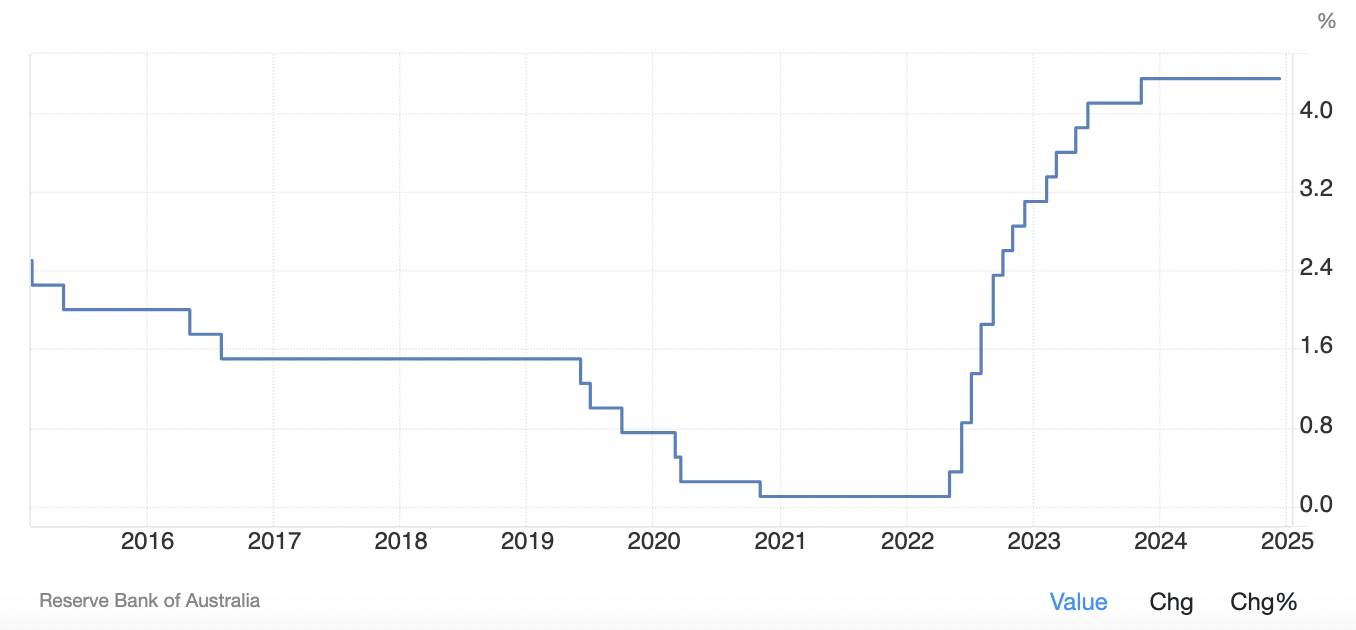

The RBA left interest rates unchanged at 4.35% at its December meeting as expected but removed a reference to possible further rate hikes, which some viewed as a signal that the central bank could be nearer to a pivot. Governor Michele Bullock stated the central bank did not consider a rate hike at the December meeting, but the more dovish tone acknowledged recent softer data, which points to the first cut potentially arriving in February.

The last rate hike (+25bps) in this cycle was implemented by the RBA in November 2023, and the benchmark cash rate stayed at 4.35% throughout 2024, as shown below in this graphic from Trading Economics (note the other graphics regarding the Australian economy are also sourced from Trading Economics).

At the December press conference, Ms Bullock said, “Some indicators softening in line with our forecasts, that said, on balance, some data is a little softer than expected. This has given the Board some confidence that inflationary pressures are declining, but risks remain.”

The removal of language referencing potential future rate hikes sparked speculation about a rate cut as early as February. Commonwealth Bank economist Gareth Aird said the shift marked a “dovish turn,” while Deutsche Bank’s Phil Odonaghoe revised his forecast to join CBA in forecasting a 25bps cut in February at the next RBA meeting, with the potential for four cuts in 2025, up from three previously forecasted.

The meeting followed on the heels of soft local GDP data released in early December, which rattled market nerves by indicating that Australia is teetering ever closer to an all-out recession. Only government spending (and hiring) and immigration stand between the economy and the first serious contraction since the 1990s. The case for the RBA to commence easing grew stronger on the data. At the time, the Australian dollar tumbled to a four-month low, which offered some support to exporters but underscored a soft domestic economy.

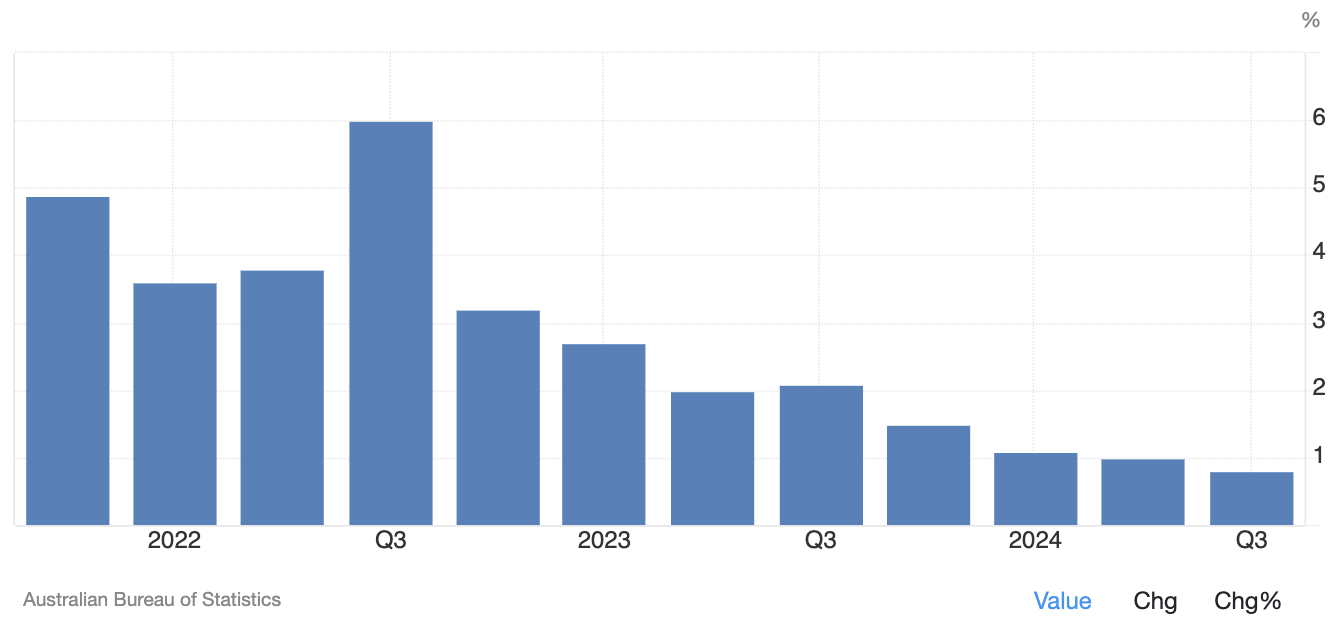

GDP for the third quarter grew just 0.3% quarterly, below expectations of 0.4%. On a yearly basis, the economy expanded by a meagre 0.8%, the slowest pace since the pandemic-interrupted 2020 and in the 1990s and well below expectations of 1.1%. Household consumption was flat, reflecting higher savings and subdued spending, while a fall in inventories subtracted from growth. Fixed investment, however, surged on booming Government infrastructure spending, which isn’t a sustainable factor.

Notably, GDP per capita declined for a seventh straight quarter. Without record government spending and immigration, the headline figures would signal an economy in recession. The big problem is that Australia’s productivity woes aren’t showing signs of any significant improvement, and that needs to be turned around to drive an improvement in living standards. Overall, the data wasn’t great reading.

Australia GDP YoY change – immigration and elevated government spending are masking structural issues.

There are a few key factors that have supported the Australian economy, including the previously discussed immigration and government spending. Retail sales have been surprisingly resilient, as has the jobs market (although that data was supported by hiring in the public sector), and the combination alongside stubborn inflation has seen the RBA stay pat on interest rates longer than most global peers.

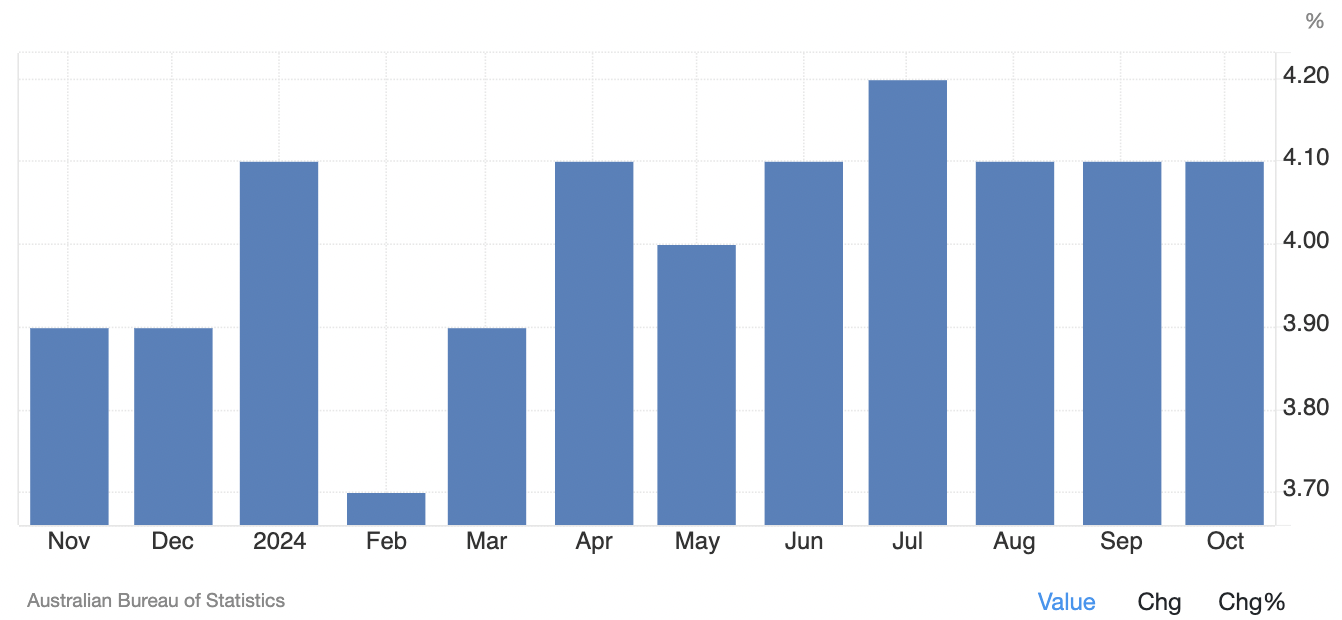

Australia’s unemployment rate fell to 3.9% in November, down from 4.1% in October, defying expectations for the rate to creep higher to 4.2%. This marks the lowest rate since March. Employment surged by 35,600 to a record 14.54 million, exceeding forecasts of a 25,000 gain and accelerating from October’s 12,200 increase. Full-time employment led the growth, rising by 52,600 to 10.07 million, while part-time jobs fell by 17,000 to 4.47 million. The participation rate held steady at 67.0%. Bets on a February rate cut shifted from roughly 70% to almost 50%.

Unemployment rate – the job market is holding up surprisingly well in Australia, primarily due to hiring by the public sector.

Australian retail sales rose +0.6% in October, beating forecasts of a +0.4% increase and accelerating from the +0.1% growth recorded in September. The ABS noted stronger activity ahead of Black Friday sales, with retailers offering early discounts. Sales in discretionary categories like household goods retailing (+1.4%) and other retailing (+1.6%) were particularly robust. However, declines were observed in clothing and footwear retailing (-0.6%) and department stores (-0.3%). Sales rose in all states except for the Northern Territory.

Australian retail sales (MoM) were surprisingly resilient.

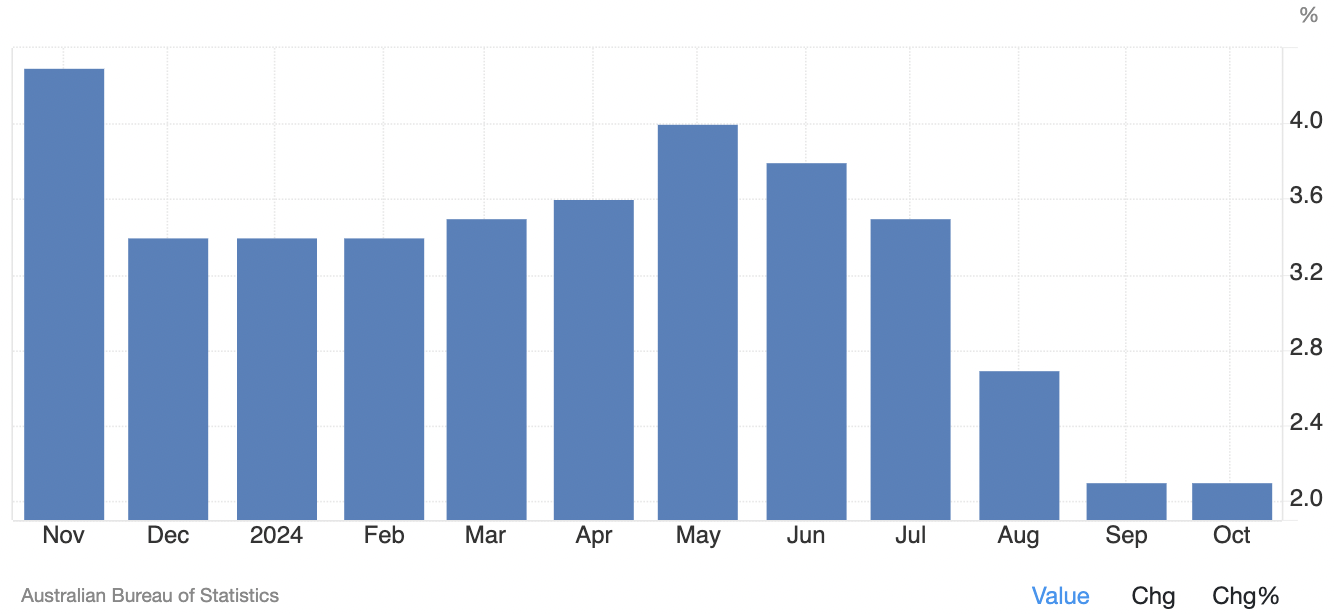

October inflation numbers showed headline annual inflation coming in at 2.1%, flat with September and below the 2.3% economists anticipated, suppressed by government energy subsidies. The concern, though, is that Australia’s CPI could tick up once the government energy subsidies expire.

The headline annual CPI (below) was flat, but the underlying picture was less welcome.

The so-called trimmed mean CPI (think core inflation and the number the RBA more closely watches) jumped to an annual 3.5%, up from 3.2% in September. While food and beverage prices were steady at +3.3%, fruit and vegetables (+8.5% YoY), rents (+6.7%), and insurance costs (+6.3%) are still running hot.

Inflation persisted as a concern throughout the year, and the last-mile challenge combined with a resilient set of headline labour market numbers saw the RBA stick with the 4.35% cash rate throughout 2024.

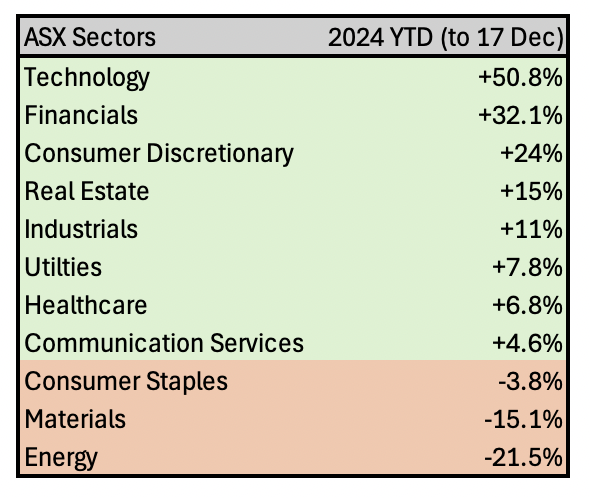

Australia’s YTD market performance (figures are to 17 December)

Despite some downward pressure over the past two weeks, the ASX200 benchmark has delivered decent returns in 2024 amid the elevated interest rate environment and heightened geopolitical tensions. Sadly, the Ukraine war dragged on, and Israel’s conflict widened.

As of 17 December 2024, the ASX200 was up +9.5% year-to-date, although there have been wide divergences in the performance at the sector level. The overall positive performance reflected positive sentiment in the US stock market, which had a significant influence on the ASX, with investors drawing confidence from the performance of US equities, the resilient domestic economy, supported by immigration, consumption and government spending.

The Australian earnings season delivered mixed results, with roughly an equal number of companies surpassing and missing expectations. Rising input costs and higher interest rates continue to squeeze profit margins, contributing to a slight drop in FY24 earnings per share. Looking ahead, FY25 guidance remains cautious, particularly for some of the ASX’s top 20 companies, which are grappling with structural growth challenges.

There was a wide divergence at the sector level. While financials may have lagged the tech sector to take second place performance among the best-performing of the 11 broad ASX sectors, due to their much heavier weighting in the index, they have been the largest upward contributor to overall index performance.

This was driven by the big banks, which staged impressive gains. The big banks posted solid earnings, backed by robust dividends and buybacks. Still, the results were hardly glowing enough to seemingly justify the strong gains made in 2024. The broader financials sector has gained +32%, driven by the +34% rally in the ASX200 banks index (XBK), which was up more than +34%. This was against the backdrop of a FY24 profit pool for the major banks of $29.9 billion, down -5.7% on FY23. The average return on equity decreased by 80bps to 10.9%. However, the banks lifted their payout ratios, with an average increase of 4.6 percentage points to 77%.

Early signs of weakening asset quality (impairments are increasing, albeit from a low base) are emerging as higher interest rates and cost-of-living pressures strain borrowers. Earnings for the ASX200 banks index are expected to remain flat over the next year, but even that may be optimistic. We remained positive on the banks (NAB, ANZ & WBC) with buy ratings for part of the year, which was the right call, before pivoting back to hold recommendations on valuation grounds. We see the bar for outperformance being higher in 2025.

The tech sector roared higher in 2024 to take the top spot on the sector table. Impressive earnings results reported for Q3 added to the momentum spurred by the wave of innovation occurring across the industry, with much investor excitement about the potential productivity improvements, even if Australia’s tech sector lacks the depth of the American market on this front. The relatively small pool of high-quality tech large caps in Australia has seen them receive premium valuations, even compared to American peers. We took advantage of a sell-off in WiseTech Global in October to recommend the stock as a new buy. The stock has since partially recovered, and the outlook remains bright. While the valuation is indeed lofty on a one-year forward basis, the growth we anticipate over the next five years justifies the call.

At the other end of the performance spectrum are the materials and energy sectors, which have declined -15% and -21%, respectively. Beginning with the much larger index-weighed materials sector, the decline has been driven by the base metal resource names, while the gold sub-index has staged a solid +20% gain YTD. We had a bias towards physical gold and the gold miners in 2024, and that has been a decent call, although the performance of the gold miners as a group has lagged the yellow metal. We remain bullish on the gold mining group heading into 2025 as we believe the disconnect can further narrow due to the operating leverage within the group. Northern Star, Evolution Mining, and GOLD were among our buy calls.

BHP, Rio and Fortescue have underperformed, primarily over iron ore pricing fears, which we believe have been overblown. The big support level at $90 per ton has held even during the doom and gloom periods in 2024. Iron ore was trading comfortably above $105 at the time of writing. All these majors sit low on the cost curve, so even price levels around $100 will generate sufficient cash flows to support decent returns for shareholders. Our preference here has been for BHP and Rio, with buy recommendations, as we like the growing contribution from copper slated to arrive in the coming years. Copper is one of our preferred commodity exposures for 2025 due to the favourable demand and supply gap forecast over the next decade. Sandfire Resources and the Global X Copper Miners ETF (WIRE) are purer copper exposures we have recommended.

We note Rio has also undertaken a significant pivot towards lithium in a counter-cyclical move. How this pans out remains to be seen, but historically, that type of timing has been a solid strategy. Lithium demand may be lagging earlier bullish forecasts, but we believe it still has legs, and Rio’s lithium assets (including the proposed Arcadium Lithium deal) are tier 1.

We expect Beijing to have little choice but to step up supportive measures in 2025 and that Trump’s bluster will be more bark than bite after he assumes office. While we do expect tariffs to be imposed, we anticipate these to be lower than feared. The combination of these factors should be supportive of the commodity complex in 2025, which trades at low valuations. We see an asymmetrical opportunity with more upside than downside.

The local energy sector has endured a tough time in 2024 amid significant volatility in oil, gas, and coal prices. Our buy calls on Santos, Woodside and Whitehaven based on undemanding valuations have proved wide of the mark. We see the scope for improved cash flows across these names in the coming years, even under a moderate energy pricing matrix driven by company-specific developments, but our buy calls were too early. Uranium is an area we have been wrong about in 2024, with uranium prices correcting sharply lower after earlier cresting around $110/lb, but from a technical perspective, we believe the downside momentum has dissipated. We expect upward momentum to resume early next year, with the Trump administration likely to make it easier to roll out nuclear power. The growing demand profile is there for future years, particularly from mega-cap tech. Meanwhile, the broader energy transition remains challenging, with investment uncertainty and integration challenges that need to be addressed.

Briefly, on a couple of the other sectors’ performances, consumer discretionary is up +24% YTD, while real estate has advanced +15%. Expectations of a looming RBA pivot provided support for both despite the can being kicked down the road several times. We continue to see value in the real estate sector, with upward property revaluation potential in 2025, should the cash rate reduce as expected. There is the scope for improved underlying earnings dovetailing with an upward re-rating of valuation multiples, such as P/NTA. We have buy recommendations on Stockland, Scentre Group (SCG) and Vicinity Centres (VCX). Stockland and Scentre Group have enjoyed positive gains YTD, while Vicinity has been flat. SCG and VCX straddle the real estate and consumer discretionary sectors.

The Tribe has Spoken.

Thank you to the many of you who participated in our Member Survey for 2024. Our efforts on the Australasian Equities research service have also been awarded a ‘B+’ grade from Members. As usual, there was plenty of dispersion in the comments, and we welcome feedback. This gives us areas to strive to improve upon in 2025.

The four days (occasionally five days if warranted) per week correspondence from Angus Geddes is a key part of our communication with Members and a channel through which Fat Prophets clarifies our views on macro and micro-economic developments and the implications for stock markets. The daily email was separately graded and received an ‘A-’.

Best regards,

Fat Prophets

Disclosure: Interests associated with Fat Prophets hold shares in NAB, WBC, ANZ, BHP, FMG, RIO, WTC, SFR, WIRE, SCG, SGP, VCX, WHC, STO, and WDS.