Solid foundations despite a setback

Even though Evolution Mining faced a challenging December quarter, marked by crimped production at the Red Lake mine in Canada and Mungari in Western Australia, higher gold prices boosted underlying earnings and net mine cash flow metrics. The balance sheet remains rock-solid with an increase in the cash position and lower gearing, while there has been a substantial boost to resources.

The acquisition of the 80% stake in the Northparkes copper-gold mine located northwest of Parkes, in the central west of New South Wales, Australia, looks to be a good one for Evolution. Copper production for Evolution is set to jump, with copper revenues to make up about 30% of Evolution’s total revenue mix going forward. However, this, of course, will be influenced by the pricing of the two metals. Management reported the first two months of Northparkes operation had generated cash and delivered to plan.

The stock tumbled in December and January following the Northparkes announcement and equity raise, followed by the rough December quarter activities report. Gold production was lower than anticipated, and the all-in-sustaining cost (AISC) did not decrease as expected.

We have a bullish outlook on gold and copper. Evolution has high-quality assets in attractive jurisdictions (Australia and Canada), with the scope for existing resources to grow further with more exploration. We view the correction in the shares as an overreaction, with the current valuation appealing to investors seeking gold and copper exposure. We rate Evolution Mining a buy.

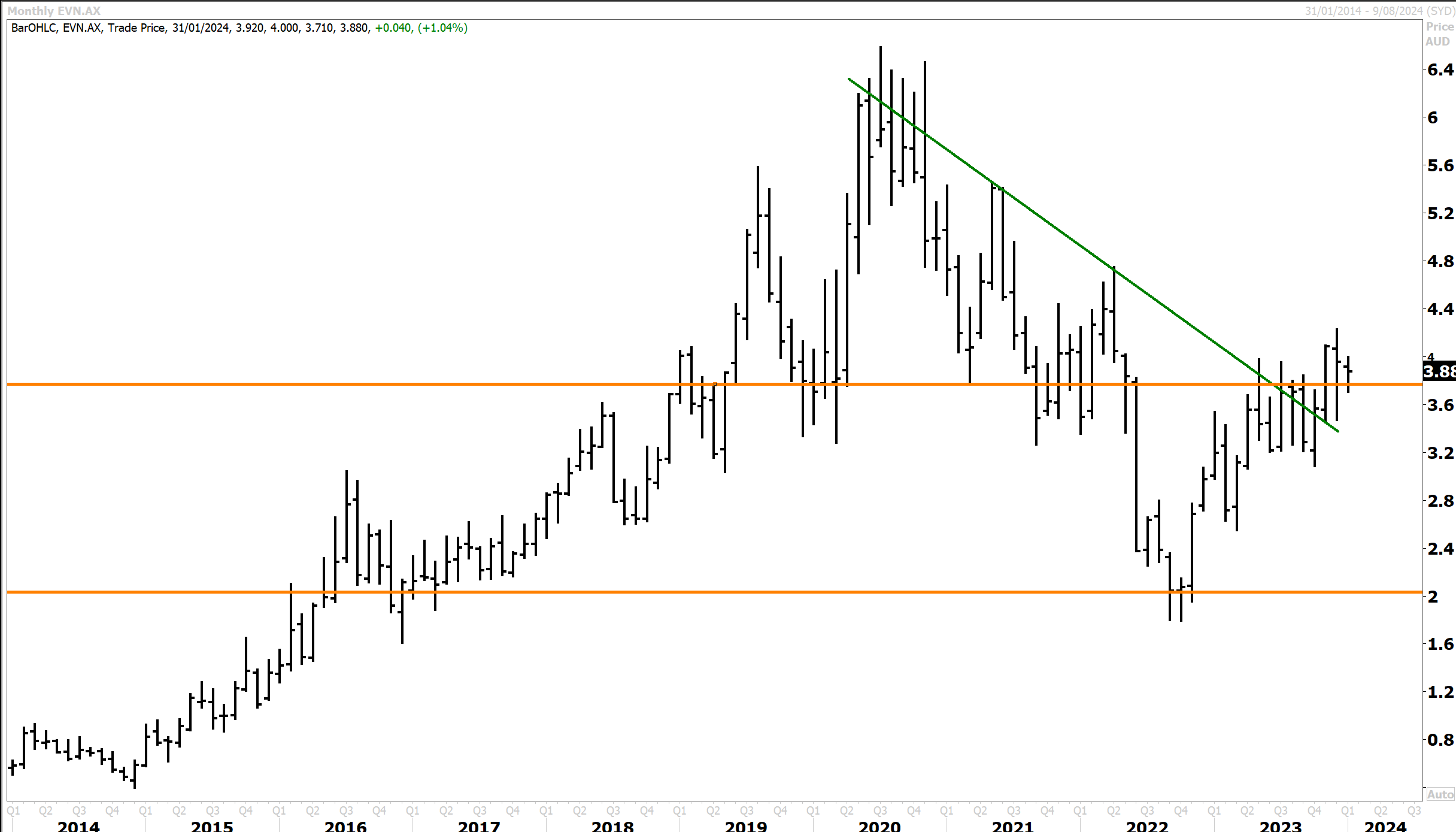

Turning to the technical picture, since breaking out of a primary downtrend in the second quarter of 2023, Evolution followed through on the upside. The bullish technical setup has since suffered a setback, with a fair bit of damage on the charts incurred following the disappointing quarterly production update.

However, despite the setback, EVN looks to be finding support at the key $2.90 level, which could drive a recovery in the coming year. It’s important to keep incumbent bearish sentiment around the stock in perspective, with the A$ gold price likely headed for new record highs this year that will continue to drive cash flow.

1H24 headline numbers (in A$ unless otherwise noted)

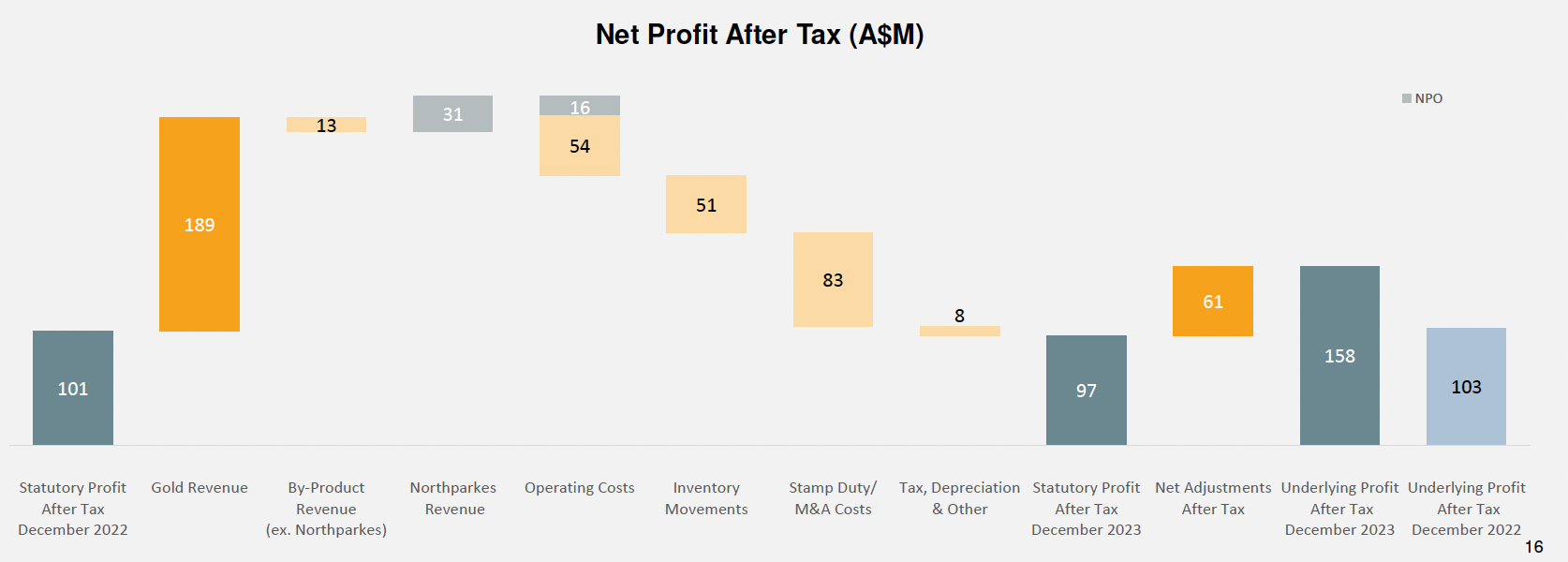

In the first half of FY24, Evolution Mining produced 319,377 ounces of gold at an all-in sustaining cost of $1,615 per ounce, leading to a 53% surge year-on-year in its underlying net profit after tax to $158.1 million. [subscribe_to_unlock_form]The financial improvement was propelled by a 16% hike in gold prices, reaching $3,000 per ounce.

Source: Evolution Mining

Underlying earnings before interest, taxes, depreciation, and amortisation (EBITDA) climbed by 28% to $572.6 million. Evolution maintained its interim dividend at 2 cents per share, fully franked, which was somewhat disappointing but understandable given the context.

The net mine cash flow increased 136% to $203 million after $231 million of investment in growth projects. Operating mine cash flow increased by a more modest 30% to $618 million, while group cash flow improved by $169.3 million to $52.4 million, swinging from the $116.9 million outflow in the prior corresponding quarter. Decreased capital intensity and improved margins thanks to higher gold prices have driven the cash flow improvement. Evolution Mining concluded the quarter with a cash reserve of $191 million and a reduced gearing ratio, down from 32.8% to 29.7%.

Ongoing exploration at Ernest Henry, Mungari, and Cowal, along with the acquisition of the Northparkes copper-gold mine in New South Wales, has led to an 8% increase in Evolution’s gold mineral resources to 32.7 million ounces and a 134% increase in copper to 4.1 million tonnes. Consequently, gold and copper reserves have climbed by 15% (net of depletion) and 100% year-on-year to 11.4 million ounces and 1.3 million tonnes, respectively. CEO Lawrie Conway noted regarding Northparkes, “The feasibility study for the E22 orebody is progressing and we anticipate the outcomes of that study to be available early in the June 2024 quarter, which will inform future mining options at the asset.”

Despite a substantial production shortfall at its Red Lake mine in Ontario in the December quarter, Evolution maintained its annual production targets of 789,000 ounces of gold and 62,500 tonnes of copper at an AISC of $1,340 per ounce, plus or minus 5% for each of those metrics. In our view, at the current valuation level, the market is pricing an expectation these targets will not be achieved.

In summary, we have a bullish outlook on gold and copper. Evolution has high-quality assets in attractive jurisdictions (Australia and Canada), with the scope for existing resources to grow further with more exploration. We view the correction in the shares as an overreaction, with the current valuation appealing to investors seeking gold and copper exposure. We rate Evolution Mining a buy.

Disclosure: Interests associated with Fat Prophets hold shares in EVN.

[/subscribe_to_unlock_form]