TLS

Mobile bill pain for consumers is Telstra’s gain

Telstra shares have been strong gainers year-to-date, extending gains from 2022 thanks to several factors, spearheaded by positive financial traction and the increase in dividends. In our view, there is significant optionality for the monetisation of the InfraCo business, although we may have to wait until late 2023 or beyond for a decision here.

With mobile price increases on the way and all the signs of a more rational pricing market in mobile enabling Telstra to leverage the company’s leading position, we retain our positive stance and buy rating on Telstra for Members with no exposure. We suggest patience and buying on the dips given the solid gains YTD and the (justified) premium price-to-earnings multiple.

Telecommunications has become an essential service and thus should be resilient during a downturn. Meanwhile, there is secular growth in data usage and Telstra has opportunities to grow revenue in newer areas like IoT as we increasingly move to a digital world.

Telstra enjoys a leading position in the oligopolistic Australian telecoms market given the heavy investment in its network. At the time of the interim report, Telstra’s 5G network covered 81% of the population and was on track to hit 85% by mid-2023.

After years of bearing the brunt of the financial hole from the NBN and price wars in mobile, the environment is sunnier for Telstra. The annuity cash flow from the infrastructure leasing deal (i.e., ducts, pits, exchanges) with NBN is indexed to inflation. Meanwhile, Telstra has dramatically simplified its mobile plans (cutting costs) and pushed through price increases, which combined with higher customer numbers has lifted the financial performance for the key mobile segment.

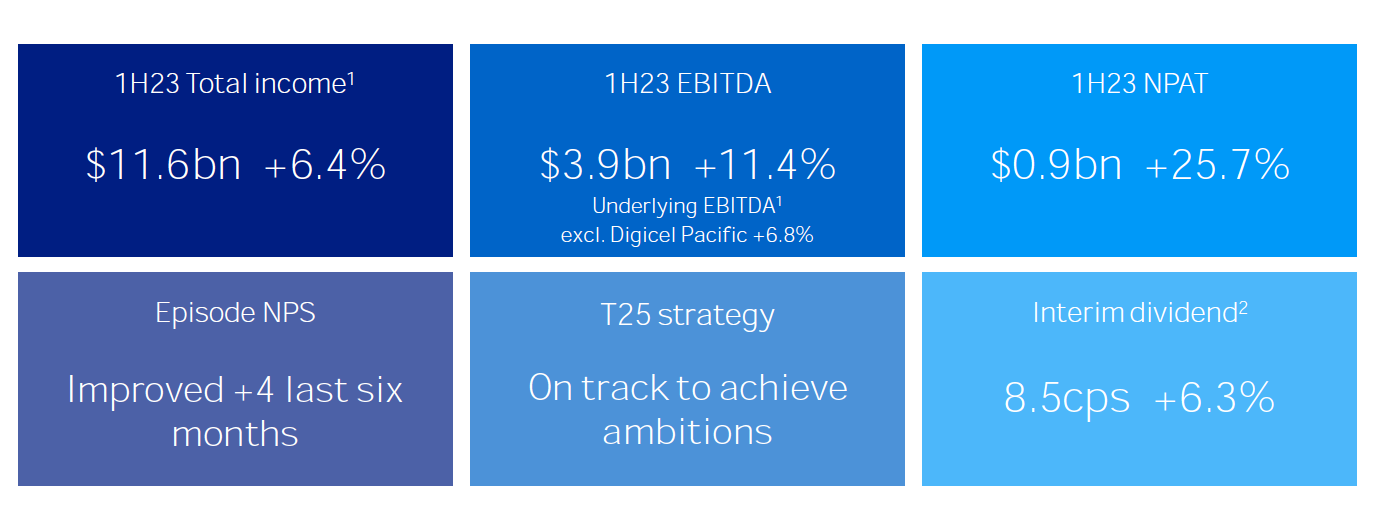

To recap, in 1H23 mobile showed continuing growth, with revenue up more than 9%, supported by higher average revenue per user (ARPU) and subscriptions. Post-paid handheld ARPU was up by 4.5% to $50.47 per month, a welcome development. Combined with more subscriptions, mobile earnings grew by 13.6% to $2.2 billion to be a highlight within the group results.

[subscribe_to_unlock_form]Even higher ARPU is on the horizon as Tesla earlier announced a higher-than-expected 7% increase in post-paid mobile and mobile broadband prices to arrive in early July. That is going to equate to about $3 – $6 dollars depending on your plan. That followed an earlier announcement that pre-paid costs would be lifted by up to a hefty 20% in some cases. More will likely be on the way in the future, as consumers have become used to price rises. In addition, the recent results and commentary from Optus owner Singtel suggest that the more rational pricing environment has legs. Meanwhile, the return of roaming is positive, as is the flow of immigrants back to Australian shores.

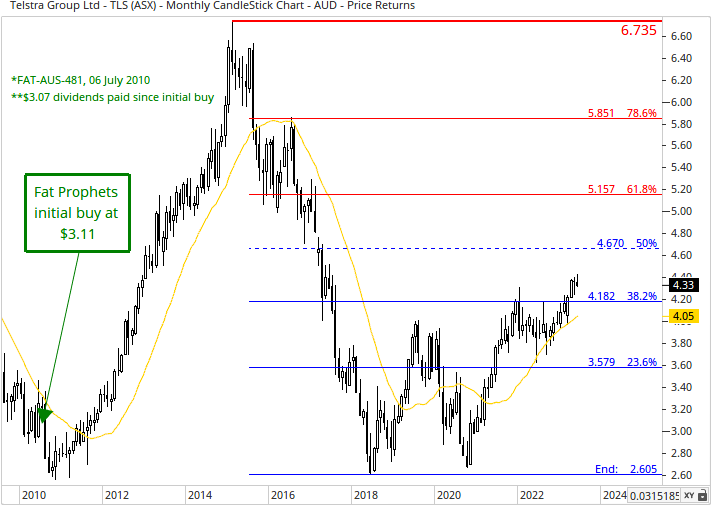

Turning to the charts and TLS shares have been on a robust uptrend since September 2022. The uptrend was also confirmed by a ‘golden cross’ – where the 50-day (red) moving average crossed above the 200-day (green) moving average (shown above) More recent price action, however, shows momentum is slowing down with the share price failing to breach above the 4.40 levels and recent price has inched closer to the 50-day MA. At this point, keep a close eye on TLS to see whether the 4.30 level and 50-day MA will hold.

Summary

The solid performance of the core mobile business helped offset the lacklustre performances of some other areas like Enterprise. International revenue was another highlight though, thanks to the Digicel Pacific acquisition last year. As members may recall, group EBITDA rose 11.4% to $3.8 billion and NPAT surged 25.7% to $934 million.

Source: Telstra

The key win for many was the nudge upwards in the fully franked interim dividend to 8.5 cents per share from 8.0 cents.

Excellent cost discipline has been supportive. Will Telstra return to steady growth in dividends? While only time will tell, we are encouraged by the more rational pricing environment and continued excellent operational execution with material progress in the T25 strategy. These are supportive of a return to modest dividend growth, although we would caution about expecting too much on this front. Nonetheless, we view Telstra as a core position and see significant optionality in the monetisation of InfraCo.

We retain our buy rating for Telstra for Members with no exposure. We recommend being patient and buying on dips.

Disclosure: Interests associated with Fat Prophets hold shares in Telstra.

[/subscribe_to_unlock_form]Fat Prophets has made every effort to ensure the reliability of the views and recommendations expressed in the reports published on its websites. Fat Prophets research is based upon information known to us or which was obtained from sources which we believed to be reliable and accurate at time of publication. However, like the markets, we are not perfect. This report is prepared for general information only, and as such, the specific needs, investment objectives or financial situation of any particular user have not been taken into consideration. Individuals should therefore discuss, with their financial planner or advisor, the merits of each recommendation for their own specific circumstances and realise that not all investments will be appropriate for all subscribers. To the extent permitted by law, Fat Prophets and its employees, agents and authorised representatives exclude all liability for any loss or damage (including indirect, special, or consequential loss or damage) arising from the use of, or reliance on, any information within the report whether or not caused by any negligent act or omission. If the law prohibits the exclusion of such liability, Fat Prophets hereby limits its liability, to the extent permitted by law, to the resupply of the said information or the cost of the said resupply.

Funds Management – In addition to the listed funds FPC, FPP and FATP, Fat Prophets Pty Ltd manages the separately managed accounts, namely Concentrated Australian Shares, Australian Shares Income, Small Midcap, Global Opportunities, Mining & resources, Asian Share, European Share and North American Share. These SMAs are managed under their own mandates by the fund managers, and this is independent to the research reports.

Staff trading – Fat Prophets Pty Ltd, its directors, employees and associates of Fat Prophets may hold interests in many ASX-listed Australian companies which may or may not be mentioned or recommended in the Fat Prophets newsletter. These positions may change at any time, without notice. To manage the conflict between personal dealing and newsletter recommendations the directors, employees, and associates of Fat Prophets Pty Ltd cannot knowingly trade in a stock 48 hours either side of a buy or sell recommendation being made in the Fat Prophets newsletter. Staff trades are pre-approved by an appointed staff trading compliance officer to ensure compliance with the staff trading policy.

For positions that directors and/or associates of the Fat Prophets group of companies currently hold in, please click here.