DMP

Speedbump

Shares in master franchisee – and largest franchisee outside the US – Domino’s Pizza Enterprises (ASX.DMP) continued to be under greater pressure after the release of a ‘strategy update’ wherein management will streamline operations but also exit some unprofitable markets. To be fair, this move was not a complete surprise given the inflationary and other cost pressures coupled with increasing competition post-COVID reopening.

However, DMP’s value comes from being a solid defensive exposure in a portfolio given that we’re not totally out of the ‘recession’ woods yet. The solid value offerings should still make it a worthy choice for consumers should a ‘soft landing’ not materialise (increasingly likely). The company’s solid track record of innovation and operations discipline will also keep it an attractive investment in years to come.

In the meantime, we maintain our Hold recommendation on Domino’s Pizza Enterprises (ASX.DMP) for Members with exposure. DMP will remain firmly held in the Fat Prophets portfolio.

Turning to the charts, DMP shares broke to the downside after the trading update and even hit a new 52-week low at $47.50. However, bottom fishing pushed the stock back up to close a hair below the $44.56 support level. The downtrend is also confirmed by the fact that we see a ‘death cross’ – where the 50-day (red) moving average (MA) crossed below the 200-day (green) MA – back in mid-March.

From this vantage point, the selling pressure is likely to let up in the coming weeks provided no new low is formed – this is also reflected by the fact that the share price has moved substantially far from the 50-day (red) moving average and assuming reversion to the mean, a rebound is becoming increasingly likely.

Now onto the updates:[subscribe_to_unlock_form]

FY23 Trading Update

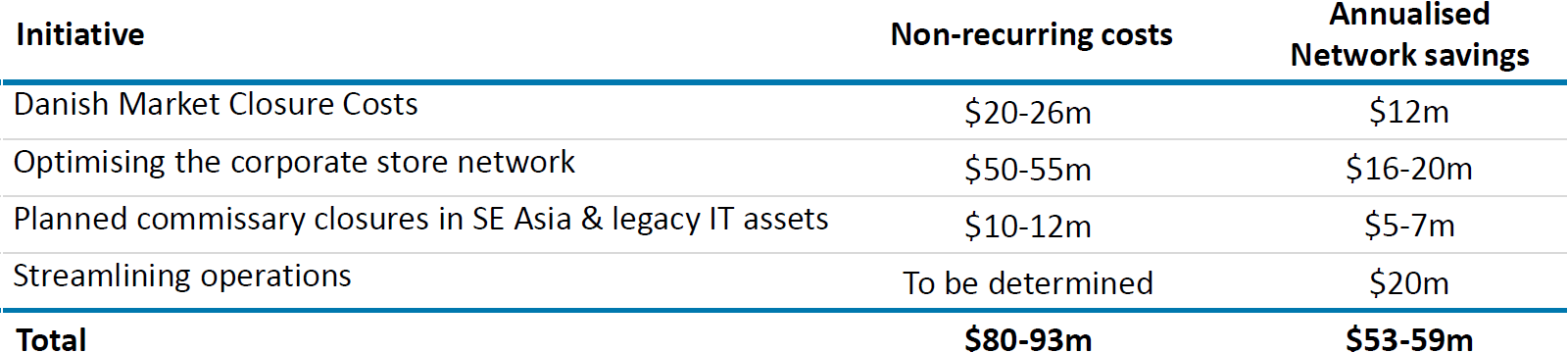

DMP announced a series of strategic initiatives that is expected to result in a short-term hit BUT lead to substantial savings. This update was quite a surprise with many expecting a more moderate change, but, recent trends in the QSR (quick service restaurant) industry do make this sizeable development unpalatable but necessary for long-term health.

First off, DMP announced the plans to exit the loss-making Danish market by the end of the year. A bit of a recap, DMP entered the Danish market in 2019 after the local franchisee struggled to perform in the region after entering receivership amid loss of public trust due to food safety violations.

At the time, this was a no-brainer move considering DMP’s solid track record of turning around operations but, as the saying goes, “you win some, you lose some” and in this case DMP failed to turn around the substantial loss of trust from the public despite drastically improving the quality of operations – even receiving numerous awards for food safety.

With the damage done, DMP has decided to close the 27 stores in the country with upfront costs expected to fall between $20 million and $26 million but this should eventually lead to EBIT improvements of $12 million starting FY24. We also see this manoeuvre to be a prudent one considering that Denmark only accounts for a tiny 0.7% of the company’s global footprint.

The pizza market in Europe has proven to be a tough nut to crack with the UK counterpart Domino’s Pizza Group (also covered in the Global Equities portfolio – for Members without access, please reach out to customer service to upgrade your subscription) having historically struggled in the continental market due to various factors such as higher labour costs, different consumer preferences to highly entrenched local players.

Source: DMP Presentation

Source: DMP Presentation

Next, on the subject of store count, DMP has announced plans to optimise the corporate store network. DMP is a master franchisee which allows the company to run stores or also franchise to prospective external operators – a business that allows for rapid expansion at minimal capital outlay.

So far, DMP has about 3,827 stores while directly operating around 913 stores. The planned change here involves closing around 65 to 70 underperforming locations while transferring about 70 to 75 stores to other franchisees – all measures to reduce operating costs but also free up some capital. The total impact would reduce 15% to 20% of corporate-owned stores with cost savings to hit around $16 million to $20 million per year. There will be upfront costs of between $50 million and $55 million, though.

The third update is the planned closure of legacy commissaries and IT assets in Southeast Asia. One of the factors that support rapid growth for DMP in the past few years was the rapid expansion to Asian markets. The various acquisitions in the region, though, mean that there were entrenched operations and janky IT systems that no longer make sense after integrating to the DMP group.

That said, management is planning to close various commissaries in Asia (Taiwan, Malaysia, Singapore & Cambodia) as well as legacy IT systems which have become obsolete in the wake of ‘new gen’ “OLO” (OnLine Ordering) systems (think: Uber Eats & DoorDash).

The costs here are expected to be around a modest one-off $10 million to $12 million with EBIT benefits of around $5 million to $7 million per year.

Finally, the last strategic initiative is to streamline core operations. The massive change in DMP’s business model in the last few years (from largely Australia-focussed to a global one) has made management rethink the business model. With a more global-centric business, DMP can leverage the much larger scale to unify IT systems to other business practices that can be scaled.

Though this is rather vague, the fact that DMP now operates in multiple regions make changes too complex to cover in one sitting. The most important development, however, is the fact that management expects EBIT cost savings of around $20 million per year starting FY25.

All in all, we’re pleased with these updates from management and cost savings of around $50 million to $59 million should improve margins which have been under pressure on the back of high inflation post-COVID.

Trading Update

Aside from the changes with operations, management also hinted at improving sales trends for the 2H23. According to the report, 4Q23 sales are up 2% on an underlying basis and is better than overall 2H23 result which was flat. The key takeaway here is that the market has now absorbed the price increases and that underlying growth should continue.

Management also kept the long-term store count target of 7,100 by 2033 unchanged.

Disclosure: Interests associated with Fat Prophets hold shares in DMP.

[/subscribe_to_unlock_form]Fat Prophets has made every effort to ensure the reliability of the views and recommendations expressed in the reports published on its websites. Fat Prophets research is based upon information known to us or which was obtained from sources which we believed to be reliable and accurate at time of publication. However, like the markets, we are not perfect. This report is prepared for general information only, and as such, the specific needs, investment objectives or financial situation of any particular user have not been taken into consideration. Individuals should therefore discuss, with their financial planner or advisor, the merits of each recommendation for their own specific circumstances and realise that not all investments will be appropriate for all subscribers. To the extent permitted by law, Fat Prophets and its employees, agents and authorised representatives exclude all liability for any loss or damage (including indirect, special, or consequential loss or damage) arising from the use of, or reliance on, any information within the report whether or not caused by any negligent act or omission. If the law prohibits the exclusion of such liability, Fat Prophets hereby limits its liability, to the extent permitted by law, to the resupply of the said information or the cost of the said resupply.

Funds Management – In addition to the listed funds FPC, FPP and FATP, Fat Prophets Pty Ltd manages the separately managed accounts, namely Concentrated Australian Shares, Australian Shares Income, Small Midcap, Global Opportunities, Mining & resources, Asian Share, European Share and North American Share. These SMAs are managed under their own mandates by the fund managers, and this is independent to the research reports.

Staff trading – Fat Prophets Pty Ltd, its directors, employees and associates of Fat Prophets may hold interests in many ASX-listed Australian companies which may or may not be mentioned or recommended in the Fat Prophets newsletter. These positions may change at any time, without notice. To manage the conflict between personal dealing and newsletter recommendations the directors, employees, and associates of Fat Prophets Pty Ltd cannot knowingly trade in a stock 48 hours either side of a buy or sell recommendation being made in the Fat Prophets newsletter. Staff trades are pre-approved by an appointed staff trading compliance officer to ensure compliance with the staff trading policy.

For positions that directors and/or associates of the Fat Prophets group of companies currently hold in, please click here.