A good vintage

The premiumization trend has been underway for quite a while now and even as a cost-of-living squeeze unfolds for many in Australia and around the world, the results from premium and luxury brands we have seen around the world in recent weeks/months, along with experience in past cycles provide us with some confidence that management expectations at Treasury Wine Estates for resilient demand at the higher-end are justified. The shares have performed robustly year-to-date even amid broader market turmoil and momentum is on the company’s side.

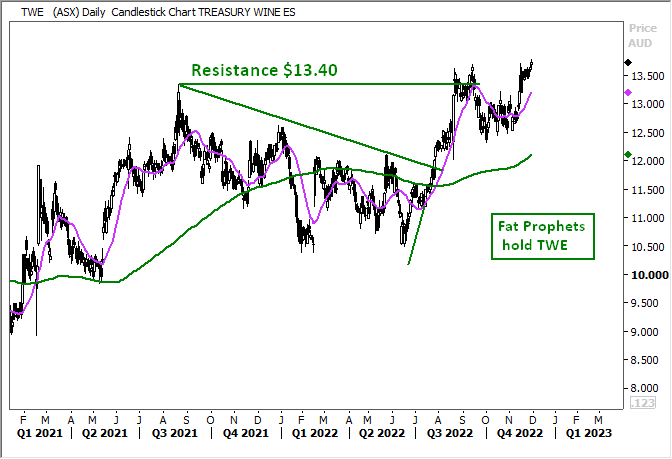

The Daily view to TWE shows the recent price decline below the $13.40 resistance level back into the 20 period moving average. The current price movements remain above the 20 period moving average and above the 200 day moving average.

Another trend unfolding in the wine and broader alcohol industry is for many consumers seeking lower-alcohol, and no-alcohol options. Treasury Wine is growing its product offerings here, including the likes of Matua Lighter, a lower-alcohol version of the Squealing Pig brand and a no-alcohol offering from Wolf Blass, named Wolf Blass Zero. The younger age group is leading the charge in demand for products along these lines and Treasury Wine has invested significantly here and its scale will help with innovation and distribution.

The recent (albeit brief) first-quarter trading update provided by the company was relatively upbeat, with trading conditions and EBIT across the group in line with company expectations and the market reaction was positive. The address from CEO Tim Ford noted, “Demand for Premium and Luxury wine has remained consistent across all of our key markets throughout the first quarter, reflecting ongoing category premiumisation trends. We will continue to closely monitor the consumer and trading environment, confident that the strengths of our brand portfolios, the historic resilience of the category through past economic downturns and the flexibility of our business model leaves us well placed to react to any changes that may arise.”

Management went on to note that the inflation and cost outlook was unchanged from the view outlined along with FY22 results provided in August. Positively, northern hemisphere vintages, including in key regions California and France, were progressing in line with company expectations.

Accordingly, Treasury reiterated being on track to deliver “strong growth and EBITS margin expansion” towards the long-term Group target of 25%. FY23 priorities are summarized in the slide from the company’s AGM below:

Source: TWE

We viewed the $434 million acquisition of Frank Family Vineyards in Napa Velley, California as attractive from both a financial and strategic perspective. The acquisition brings with it one of the biggest luxury chardonnay brands in America, slotting nicely into the company’s portfolio of brands.

We have been satisfied with [subscribe_to_unlock_form] the progress under CEO Tim Ford and improving performance in the American market, long an Achilles heel for Treasury, is part of our investment thesis for the stock. The above acquisition will help with the transition to improving margins by tilting the portfolio towards premium offerings – the Americas business has exited lower-end commercial wines. There remains work to do on improving logistics and distribution channels and time will tell whether management changes are the right team for the job. We are encouraged by the progress we have seen. One of the company’s newer brands, 19 Crimes, was reportedly recognized as the number 1 US market wine innovation for Martha’s Chard in the 2022 calendar year. The brand has a high-profile celebrity relationship with Snoop Dogg.

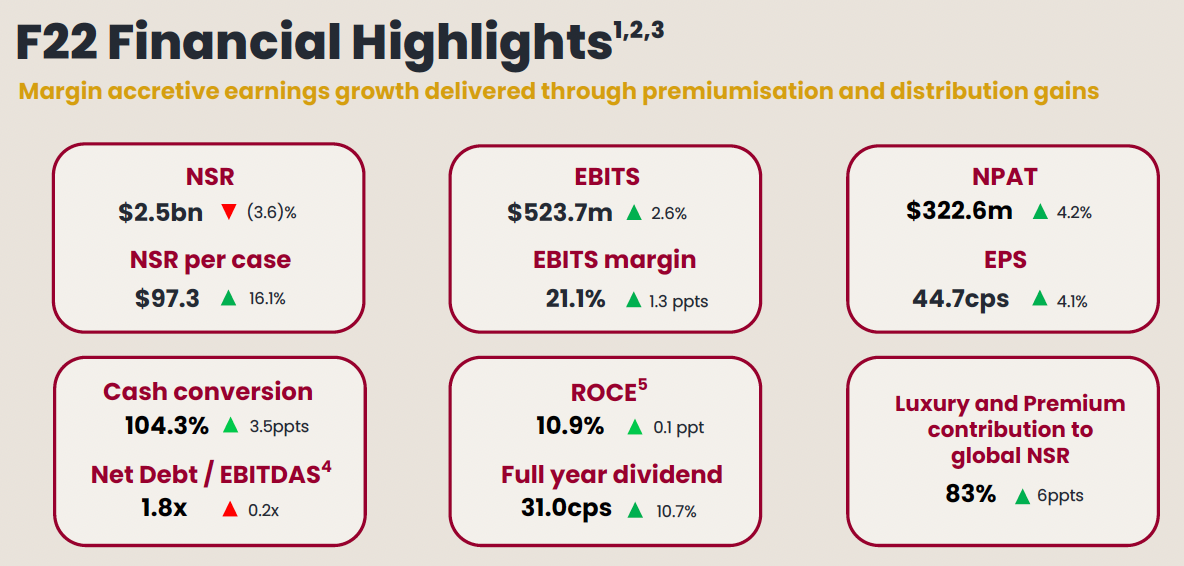

The Treasury Americas segment increased net sales revenue (NSR) 2.5% to $963.4 million in FY22, with EBITS surging 20.5% to $185.6 million, as the EBITS margin expanded 2.9 percentage points to 19.3%. Bolstering this further will assist the company with its 25% group EBIT target. To recap, group EBITS edged 2.6% higher to $523.7 million, even as net sales revenue decreased, driven by a 1.3 percentage point improvement in the EBITS margin to 21.1%. EPS was 4.1% higher at 44.7 cents and the full-year dividend was 10.7% higher at 31.0 cents per share.

Source: TWE

Another plank of our investment thesis is the scope for the China market to eventually return to becoming a solid contributor after the business was devasted by the sky-high margins (+175%) imposed by Beijing. Treasury Wine has been working to fill that gap by steadily diverting sales to other regions, including the likes of Singapore, Thailand and Malaysia. The company has been successful in this regard, reducing reliance on China and improving the overall quality of the business but should some of that business return in the future that would be a positive.

We see some scope for a thawing of relations between Canberra and Beijing going forward, with the meeting between the leaders of the two countries in Bali encouraging. We view this as a call option, but certainly not part of our core thesis for the short-term. Instead, TWE is looking to sell the new Chinese-made Penfolds, retailing at about $50 a bottle.

The monthly view of the TWE price chart indicates a new breakout above the $13.40 resistance level. Currently, price movement remains above the 12-month moving average as the Primary up trend resumes.

Summary

The strategic pivot at Treasury Wine Estates is progressing solidly and the premium and luxury sector is well-placed to be resilient during the economic downturn beginning. The company’s brand portfolio is well placed here, ranging from ‘affordable luxury’ treats like a $20 plus bottle of wine all the way up to the $1,000 Penfolds at the high end. The premiumization at the company continues, with the Napa Valley acquisition slotting in nicely. Momentum is on the company’s side and the shares have been robust performers amid broader market volatility.

We recommend Treasury Wine Estates as a buy to Members without exposure.

[/subscribe_to_unlock_form]