- Kevin Warsh came out swinging on rates – and by Thursday, the market had already started reading him the other way

- The dollar spiked; everything denominated in it fell. This is a distinction we are watching in our investment playbook.

- WTI has broken below key support, and Goldman is cutting its Brent forecast. The IB isn’t alone. There is more than meets the eye – we dive in and outline the playbook.

- Gold’s correction has done its repair work, weak hands have been flushed, and the options market is offering the upside at a discount. The USD is the trigger we are watching. Are you?

- Japanese bank profitability just hit levels not seen in thirty years, and the rate cycle is still early. We are positioned for it. Meanwhile, the state of play for Australian banks has changed significantly.

- Report spotlight: QBE Insurance – we dig into what’s happening under the hood and whether the market is pricing the insurer right.

The fatLITE is the weekly read. Membership is the position. Half price ends June 30. Try it with our 30-day money-back guarantee.

Apply code FP50% at checkout

The Verdict

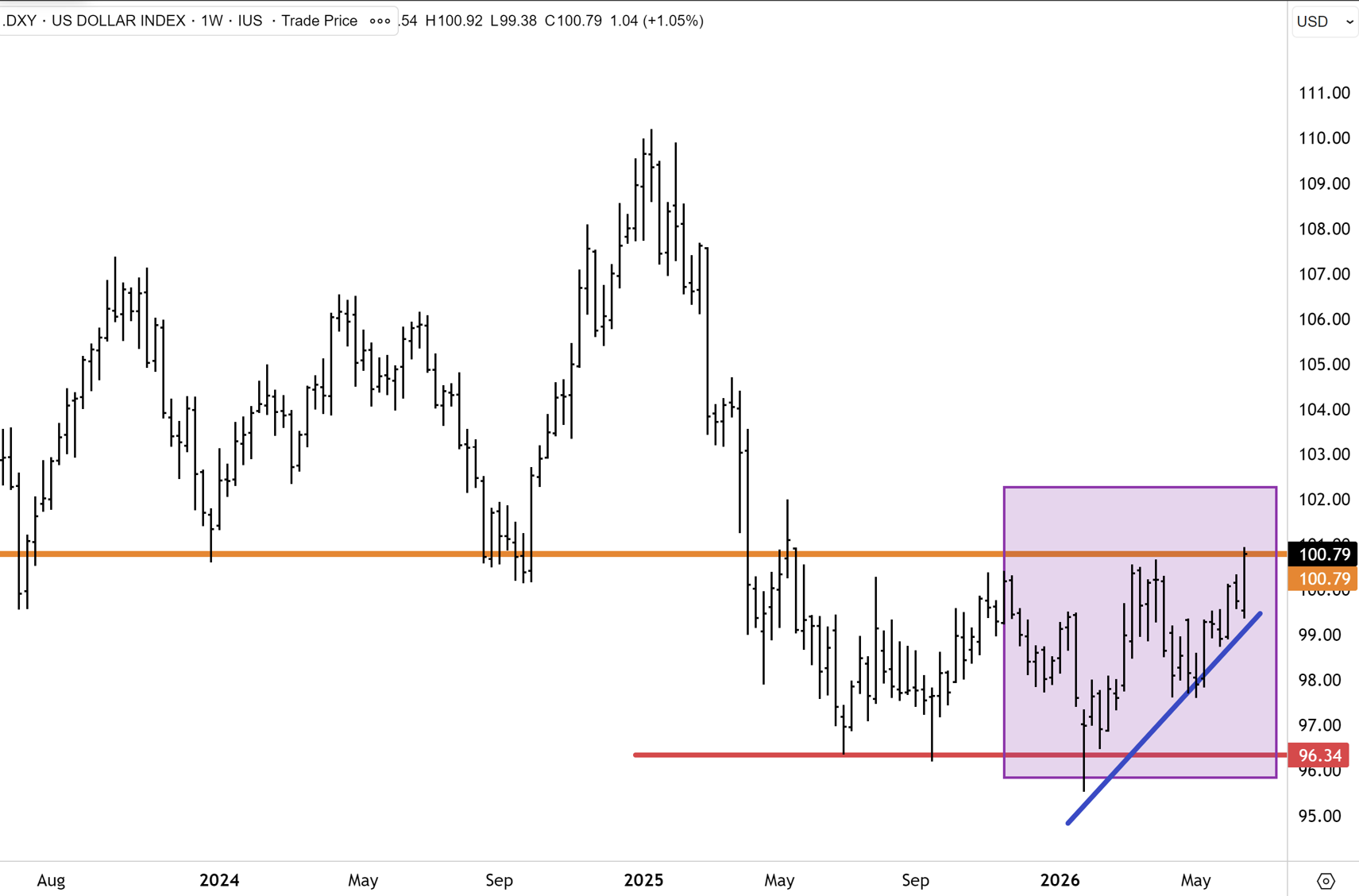

A new Federal Reserve chair gets one opening statement, and Kevin Warsh spent his on Wednesday with the safety off. He held rates, then abandoned the dot plot and forward guidance, repeated “price stability” until the room got the message, and let the market price an October hike it had not seen coming. The dollar did the rest. The DXY pushed to the top of its range near 100.8, and the short end of the bond curve spiked much more than the long end – a ‘bear flattening’ – and equities tumbled sharply during the last hour of Wednesday’s trading on Wall Street. Underneath it, the week reduced to whether the dollar’s move was a trend or a tell.

We read it as a tell. The case for a durably stronger dollar rests on the Fed alone, and the Fed cannot carry it. Monetary policy does not close a fiscal gap this size. The White House wants the dollar lower, not higher, and a chair installed by this administration has no room to hike into a midterm the President’s party is on course to lose. By Thursday, the market had already begun reading Warsh the other way, and the Russell 2000 closed at a record. The second-half book for us is a short-dollar book – think gold, copper, other commodities, the yen and equities. The level that settles the argument is the top of the dollar’s range, and until that breaks, the move is not to fold.

Every incoming Fed chair for forty years has opened by pledging to crush inflation; the format Warsh actually adopted, stripped back, is very similar to Greenspan’s, and Greenspan cut hard the moment markets cracked in 1987. The opening move is rarely the real one.

The commodity complex is not signalling weak demand this week; it is signalling a strong dollar, and that is a very different thing. Given our expectation that the greenback is near its peak, we retain conviction in our H2 playbook, including the commodities super-cycle and a rebound in gold.

At home, the Australian dollar drifted to US70.2c. The ASX 200 reached 8,966 by Wednesday before snapping a four-session run to close the week at 8,911, close to where it began, with gold, energy and technology all turning over beneath the flat surface. Friday morning, the ASX opened soft, with the ASX down ~1% near midday (the time of writing) at around 8,820.

The DXY (US dollar basket) is nearer a peak than a breakout. The rise is being driven by markets pricing Fed hikes, but that pricing runs into three walls. Monetary policy cannot close the US fiscal gap, and the debt trajectory guarantees the Treasury issuance that structurally weighs on the currency. The White House wants a weaker, more competitive dollar, which puts a tightening Warsh in direct conflict with the administration that appointed him. Additionally, consider the midterms, with prediction markets pricing a high probability that the House flips, leaving a newly installed chair no political room to rock the boat with rate hikes before November.

During ‘normal times,’ the market forgets about oil, viewing it as a relic. However, in the past few months, it was back in focus. That time is coming to an end again. WTI broke the $83 support we had flagged for weeks and kept going; the first supertankers transited the Strait carrying eight million barrels, the ceasefire was extended by sixty days and signed, and a genuine race to supply is now underway, with Russian barrels uncapped, Saudi Arabia near maximum, and Iran rejoining the market for the first time in four decades.

Goldman Sachs has already cut its Brent forecast to $80 for the fourth quarter from $90, and others will follow. The path of least resistance is toward $70 and, if the ramp down is quick, the high $60s. Cheaper oil is what drains the inflation impulse, which is what caps the dollar.

However, that same force is subduing the energy names here: Woodside (ASX: WDS) has fallen to its lowest since before the conflict began. Our House view is that this is the start of a contrarian opportunity rather than the moment to act on it. We would let the selling exhaust itself in Woodside and Santos (ASX: STO) before stepping in, not try to catch a falling knife. We will let members know when we become more bullish on these names and flip our ratings back to buys.

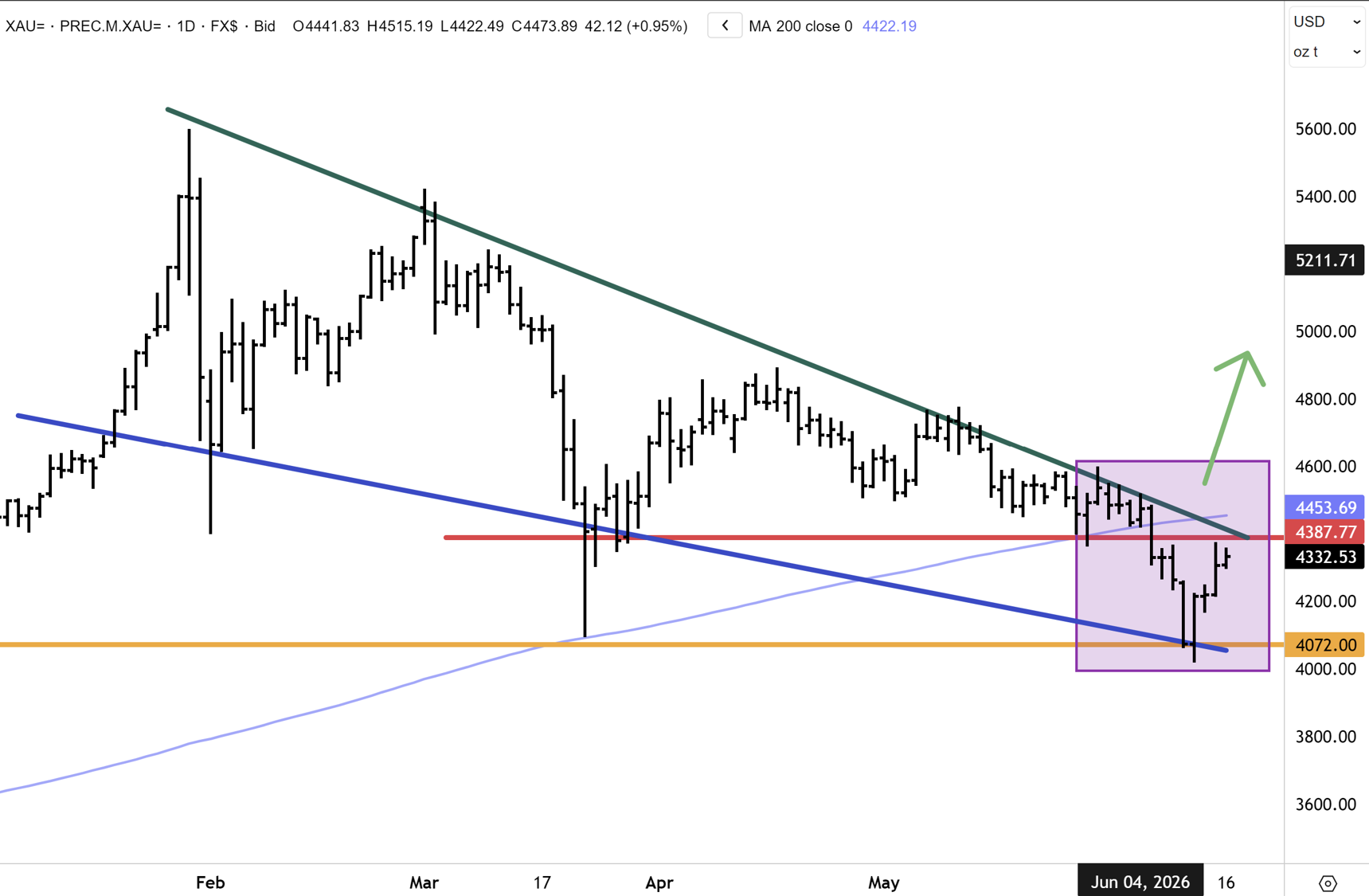

Gold had another volatile week, with an early rebound cut short by the Warsh move, but our conviction through the second half is intact. We continue to read the sell-off since February as a correction inside a bull market, not the end of one, and we expect it to reassert as a risk-on environment draws institutional and retail money back in. A strategist we follow, Stephen Moon, captured it this week: the dovish signals are lining up, the charts are starting to confirm, the weak hands have been flushed, and the trade now needs the dollar to roll over.

That is the catalyst. A rising dollar moving in lockstep with rising oil has been the weight on gold all year, and with oil falling and the dollar near a peak, that should now work in reverse. The level to watch is the 200-day moving average between $4,300 and $4,450; a break back above it would signal the correction is over.

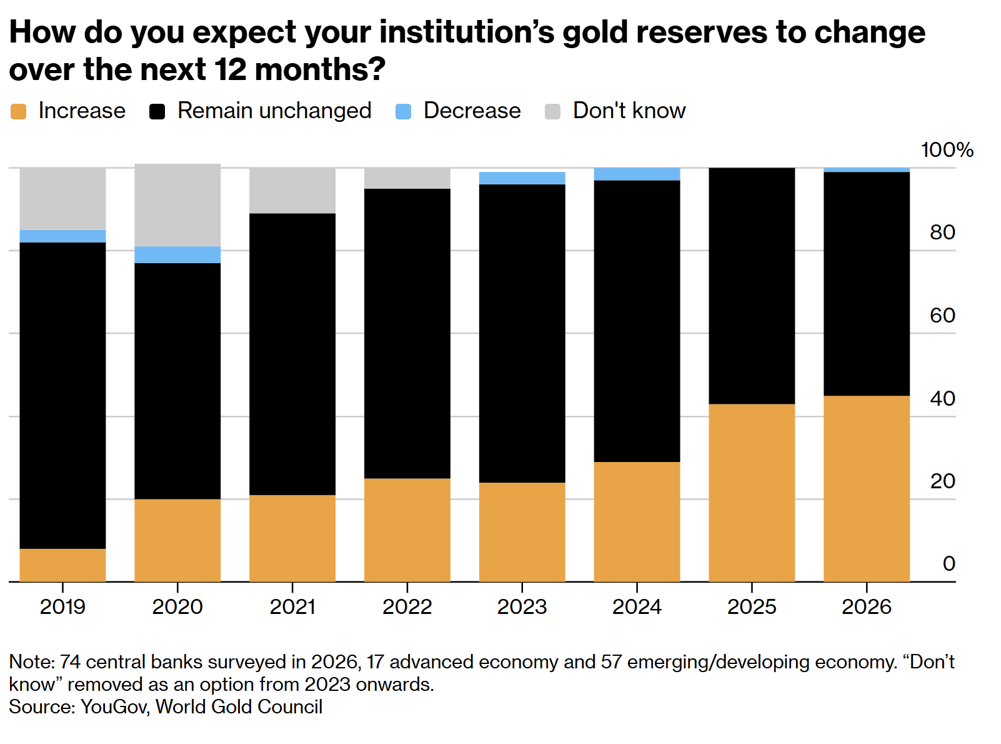

On targets, JPMorgan holds $6,000 and Goldman $5,400 for year-end. Our own view is more measured: $5,000 by December, $5,600 possible, and $6,000 a 2027 story rather than this year. The structural bid is substantial, with a record 45% of central banks in the latest World Gold Council survey planning to add over the coming year.

Northern Star (ASX: NST) has a vocal activist investor on the register in the form of Elliott Investment Management. We outline our preferred choices in the Members section.

The yen weakened through ¥161 to the dollar this week, a level last seen in 1990, but we see it coiling rather than breaking. The Bank of Japan raised its benchmark to 1%, the highest since 1995, and signalled more to come, with the Finance Ministry’s intervention line now in view and the deputy governor making clear it will not fall behind the curve. The weaker the yen runs against rising domestic rates, the more forceful the eventual turn, and that turn arrives when those rising rates start pulling the country’s offshore savings home. Paul Tudor Jones holds the same view, calling the yen an under-owned, undervalued trade where sentiment has grown complacent.

The equity market is already there. Japanese benchmarks made fresh record highs this month, and we expect the bull market to run further. The clearest expression is the banks, where a steepening curve and a rising cash rate are driving net interest margins higher after decades of near-zero rates, with valuations still below their US peers. The TOPIX bank index hit a 30-year high this week, clearing resistance that dates back to the 1990s, with scope toward 900. We recommend multiple ways to participate in the Global Equities Report.

The Local

The week’s domestic set-piece was the Reserve Bank, which held the cash rate at 4.35% with a unanimous board on Tuesday. The decision was widely expected and offered little relief to rate-sensitive sectors. Governor Bullock kept the tightening bias in place, but that is part of the job of anchoring inflation expectations, and whether another hike actually arrives is a separate question. Our view is that the local cycle has peaked and the next move is lower, most likely within a year. House prices are close to freefall and could fall another 5% to 10% over the coming year, weighing on consumer spending and lifting unemployment.

The other domestic story is the banks. The sector carries a record short position, estimated near A$16 billion, built on the view that falling house prices and the budget’s tax changes will choke mortgage demand. We have pared our ratings to hold, but we are not as bearish as the crowd. The property tax changes from July 2027 will cool investor appetite for mortgages, but the majors are also a cost-out story, with technology lowering the cost base and headcount over time. They should not all be treated equally, as Macquarie Group’s (ASX: MQG) run to record highs shows.

Report Spotlight

QBE Insurance (ASX: QBE) – BUY

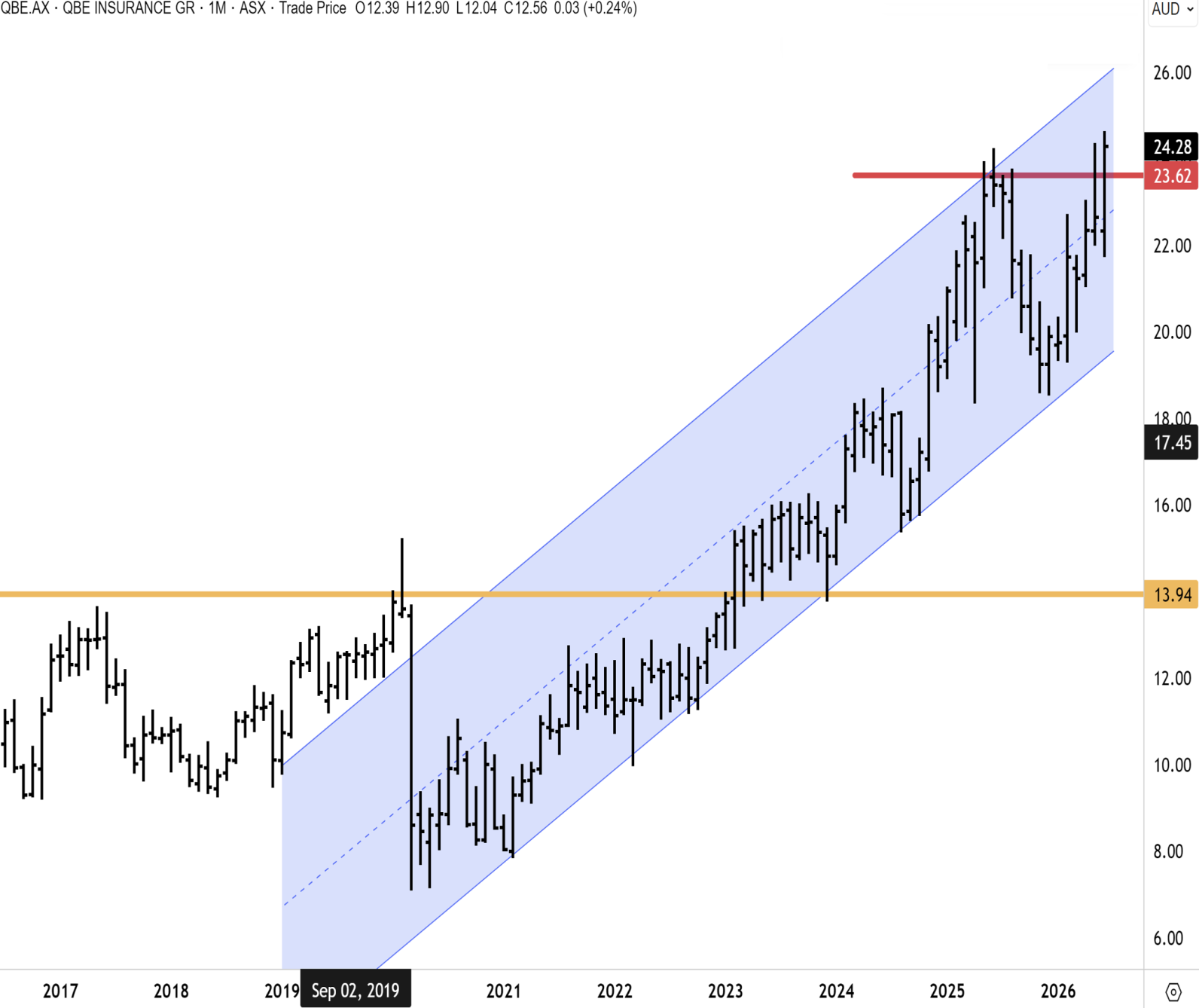

QBE is firing on all cylinders. The group achieved its highest return on equity in over a decade at 18.2%, catastrophe claims are tracking well below internal budgets in early 2026, and premium rates remain ahead of claims inflation across most business lines. This is a business in the sweet spot of the insurance cycle. Adjusted NPAT rose to ~US$1.7 billion, the combined operating ratio improved to 93.1%, and catastrophe claims came in ~US$230 million below allowance in 2024, providing a meaningful buffer heading into 2026. First quarter GWP grew ~11% year-on-year, with catastrophes again running below internal budgets. Pricing remains a tailwind. Renewal rate increases averaged 5.5% across the group in 2024, including 8.4% in Australia-Pacific and 7.3% in North America, on top of several prior years of similar increases. Management describes pricing as “strongly adequate” relative to claims inflation in most lines. Earnings quality is improving. Valuation has not fully caught up.

Upward momentum in QBE has clearly been sustained since our update. QBE is rising in a well-established uptrend channel, with the stock lifting to a fresh decade-long high this month above $24. We have conviction that QBE will continue to move higher this year and soon retest the next resistance cluster at $26 and above.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

Have a great weekend.

Carpe Diem

Angus