- Crude surged on the blockade, stalled at $80, then fell on a day of heavy military strikes. Here is why our call has tightened – and why the invalidation level still matters.

- CPI below consensus. PPI below consensus. The next Fed hike was effectively priced out in 48 hours. The market has caught up with our call. Will it be the same Down Under?

- S&P 500 earnings growth consensus moved up inside the reporting week. Companies did not lower the bar before the season. That signal is worth understanding.

- BHP guided copper production lower on Thursday. Our read inverts the cut: one of the world’s largest producers reducing volumes makes the scarcity case more firmly, not less. We name the stocks we want to own.

- The TOPIX Bank index hit a 30-year high on Wednesday, on the same session that the Nikkei fell. The divergence is a signal, and we outline our positioning.

The fatLITE is the weekly read. Membership is the position.

The Verdict

This past week, the United States and Iran exchanged a barrage of airstrikes. Crude surged and behaved the way a Middle East war week is supposed to, but most other assets downstream refused. On Thursday, escalation of the conflict in the ME failed to sustain the rally in oil, with both WTI and Brent crude lower. Overnight, the S&P 500 finished ~0.5% lower at 7,533, while the ASX200 was flat on Thursday and only moderately lower in the early afternoon on Friday.

A front-end rally in the yield curve, with a rising long end, is a Fed-path repricing with a little term premium leaking rather than a growth scare and not a duration rally. Effectively, it is what the market prices when it decides an oil shock will not reach the inflation data. The data out during the week provided food for thought here. CPI below consensus on Tuesday, PPI below consensus on Wednesday, the next hike priced out inside 48 hours, and second-quarter earnings estimates are being revised higher during the reporting season rather than in the weeks before it.

The reason the war did so little is structural, and it has been building since March. The Middle East supply that ran near 20m barrels a day before the conflict is running near 15m today, while global refining is at peak capacity, Saudi pipeline volumes have risen, and Washington is advancing talks about a Kirkuk to Baniyas route that bypasses the Strait entirely. The market absorbed an oil shock without $150 crude. It is declining to price it so aggressively higher as the round-trip sentiment plays out. Yes, the conflict is unresolved, and the Strait is still contested, but investors are becoming fatigued with the conflict.

The Calls

Our position on crude has tightened as the evidence arrived. On Monday, with WTI up 9% on the blockade, we put resistance above $84. By Tuesday, the number had come in to $81 and $82, with the reasoning made explicit. As global supply rushes to meet demand at those prices, and with refining at peak capacity, we see the range settling between the mid-to-high $60s and $80. By Wednesday, WTI was at $80.29 and visibly stalling, and we named the invalidation without qualification, that a sustained break above $80 is the clearest threat to the disinflation narrative. On Thursday, another heavy exchange of fire in the conflict produced a decline (!) in the price.

There might be more to the latest ME escalation than meets the eye, given Thursday’s decline in both WTI and Brent crude.

Our Fed call follows directly, and we have held it for longer than the market has. CPI printed below consensus on Tuesday, PPI below consensus on Wednesday, and the probability of a hold at the next meeting went from a live question to 83% to fully priced within 48 hours. December remains on the table.

The case against another hike deserves better treatment than it usually gets. Kevin Warsh spoke to Congress on Tuesday and reemphasised a hard line on inflation on the same day the market priced him out. The Chair and the futures curve said different things this week, and the market’s record of reading this Chair is not clean. Our view is that a chair will be reluctant to move ahead of the midterms and that the inflation impulse has lost its engine.

Next up, the earnings picture is doing a lot of work. Aggregate second-quarter S&P 500 earnings growth was running at a consensus of +23.7% at the start of the week and +24.8% by Thursday, which is the estimate revising higher during the reporting season rather than in the weeks before it. Companies did not window-dress guidance lower into the quarter. The pre-season bar-lowering that reliably precedes a wave of manufactured beats was largely absent, and its absence is a genuine signal about what management teams expected to report. Underneath it, the macro backdrop has cooperated, with solid retail sales, manufacturing activity and low jobless claims. Then, we also have a housing sector that remains subdued and rallied anyway.

JP Morgan’s trading desk described the inflation print as better than Goldilocks, and believes that rotation and broadening leadership are underway, and has been telling clients since the second half of March to use Iran-driven dips to add. Morgan Stanley has separately reemphasised its view that the rally will continue broadening. Both carry S&P 500 targets above 8,000.

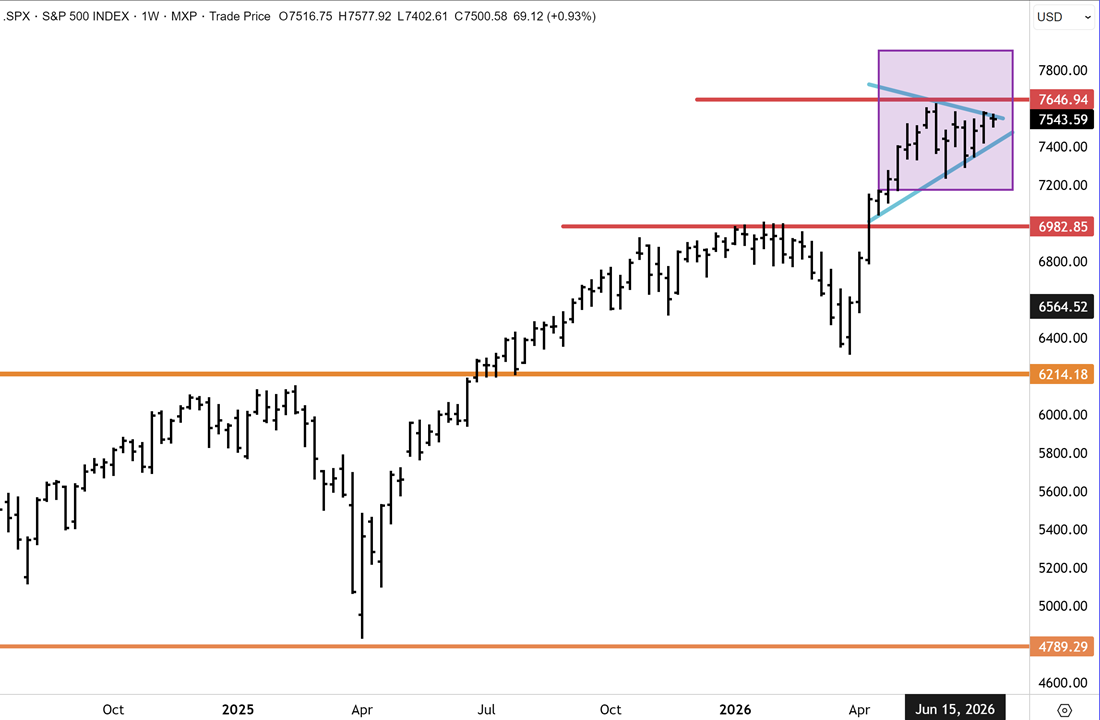

Our own view is that the setup favours a topside resolution of the contracting range the S&P 500 has traced since April, with earnings as the catalyst, and we expect many benchmarks at record highs by December, though with inevitable corrections along the way.

Japanese banks have long been one of our conviction bets, and we don’t see the rally as over as the BOJ continues to normalise policy. The TOPIX Bank index reached a fresh 30-year high above 760 on Wednesday, even as the Nikkei 225 fell 1.9% on the same session. The divergence is a strong signal: the index fell, and the banks rose, because rising Japanese rates are a tailwind for net interest margins at exactly the moment the broad market is pricing a risk-off day. We remain overweight Japanese banks and financials across our portfolios.

The Local

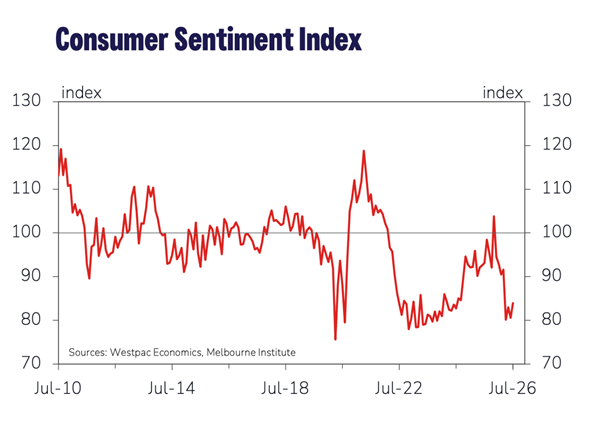

It was a real grind in the Australian market this week, with the Benchmark drifting lower most days and only holding up flat on its better days. Local data was sparse, but consumer and business confidence surveys both improved in July. The Westpac-Melbourne Institute Consumer Sentiment index climbed to 83.9, reversing June’s pullback, as household views on finances and employment improved but were still subdued. The NAB Business Confidence index rose to -5 from -14 in May, the strongest reading since February, but still in negative territory. Both measures remain below neutral, and neither shifts the RBA calculus materially ahead of the August meeting, although I don’t see another rate hike given the downward pressure on Australian housing since the budget. The renewed surge in oil prices is a complicating factor, but fuel costs have come down, setting the RBA meeting up to be a close-run decision for policymakers. Local job data lands on Thursday, and we will be watching that closely.

Most of the local action happened below the surface this week, with significant sector rotation many days, though it wasn’t that consistent, and some of the noise cancelled each other out. The energy sector was the logical winner, with a decent, albeit unspectacular advance over the past week, followed by gains from discretionary, financials and communication services. On the flipside, tech was quite hard hit, and traders took profits on healthcare after a fledgling recovery over the past two months. Staples were out of favour, and materials faced headwinds, though held better than many would have thought.

There were interesting developments in the gold mining sector – read on below in the Report Spotlight section for the synopsis.

Meanwhile, the Big Australian (BHP) did a share price round-trip on Wednesday and Thursday, before succumbing to another decline on Friday amid broader market stress. The pressure stemmed from guiding FY27 copper production to between 1.65Mt and 1.8Mt, down from 1.95Mt in FY26 and roughly 2% below consensus, on an unexpected mechanical failure at Olympic Dam and anticipated ore grade deterioration in Chile. New chief executive Brandon Craig also flagged an impairment of around US$2.3bn against the Jansen potash project, which is 84% complete and on schedule for first production in mid-CY27. The write-off is the oldest move in the book, and it is the right one; Jansen has had several cost blowouts already, so a new chief executive takes the legacy charge early.

Our read is that one of the world’s largest copper producers, lowering its volumes, makes the scarcity case more firmly, and copper prices will have to head materially higher to induce the necessary supply response to meet demand that is set to exceed supply over the coming years. We remain bullish on the broader copper complex, with BHP and Sandfire Resources among our buy recommendations in the space.

Report Spotlight

Genesis Minerals (ASX: GMD) – Hold

Genesis Minerals has locked in its acquisition of Vault Minerals on its original terms – Regis Resources walked away rather than overmatch, pocketing a break fee for its trouble. The deal logic for Genesis is compelling. Tower Hill ore will now flow through Vault’s King of the Hills mill instead of a greenfield plant that no longer needs to be built, saving the merged entity hundreds of millions in avoided capital. Total synergies claimed run to A$2 billion over the long-term. The balance sheet entering the merger is strong, with substantial net cash and liquidity headroom. Scheme approval is targeted for late in the year, but could slip into 2027.

Genesis Minerals has continued to correct lower with the downtrend in line with the US$ gold price, but constructively has held above the May lows around $4.60. GMD is holding above the primary uptrend, which intersects at just above $5. Whilst we have confidence that GMD’s consolidation is nearing an end, a topside break above $5.60 and clearance of this year’s downtrend would add conviction that upward momentum was resuming.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Have a great weekend.

Carpe Diem Angus