Prices Take Some Back

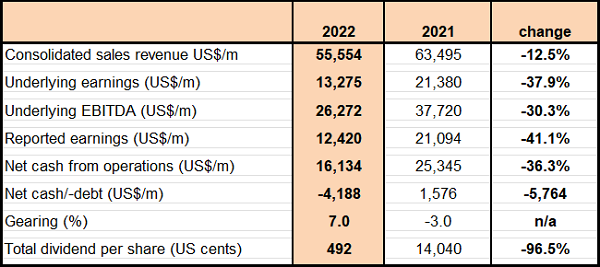

Rio Tinto has revealed a reversal in its numbers for 2022, following falls in underlying and statutory earnings, and across all its reporting lines. While the balance sheet continues to be a key standout feature it was regeared but remains pristine. Shareholders saw the annual dividend near halve while no special was paid. The following table shows a summary of Rio Tinto’s key 2022 reporting lines (EBITDA – earnings before interest taxation depreciation amortisation):

Source: Rio Tinto

Despite the falls, we rate the result as satisfactory, given prices primed the numbers, while we gave weight to Rios’ operations delivering and clawing back just a tad on the pricing impact. We believe Rio set the table with its 2021 record results to endure a turn around and are only disappointed that a longer term value view was not considered at that time i.e. an on-market share buyback. We are also comfortable that 2023 guidance numbers were unchanged from Rios’ 2022 operational result.

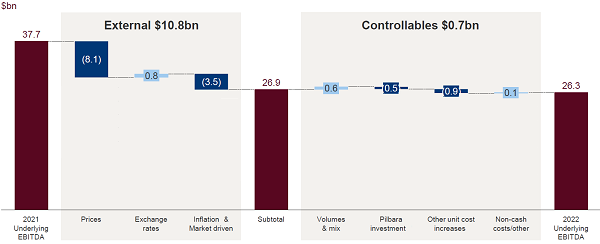

Underlying EBITDA, that better reflects the ongoing operations by removing unrelated to 2021 one-offs and segments for sale, reported a 30.3% year-on-year (yoy) fall, to US$37.7 billion for 2022. The factors impacting underlying EBITDA are shown in the following chart (in US Dollars):

Source: Rio Tinto

Lower prices for Rios’ product offerings, as Members can see from the above chart, drove the result, subtracting US$8.1 billion in 2022 (2021: +US$17.5 billion). The move in commodity prices reflected a stronger US dollar over the year that pressured prices while trading conditions remained relatively robust. This result reflects the cyclical nature of resources, and the lack of control Rio has over prices.

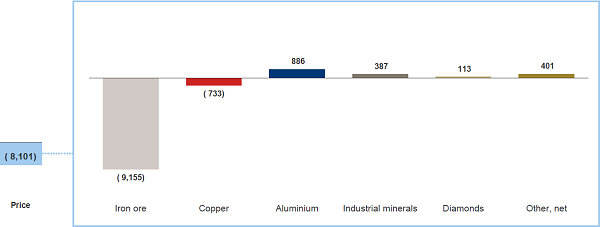

[subscribe_to_unlock_form]The negative US$8.1 billion pricing impact was driven by all of Rio’s key product offerings, with segment contributions shown in the following chart (US$/m):

Source: Rio Tinto

Iron ore and Rio’s key product offering was the primary drive, as Members can see from the above table, subtracting US$9.2 billion (2021: +US$11.6 billion). Rio saw its 2022 average realised iron ore price fall 26% yoy, to US$106.1 per tonne. The negative US$700 million (2021: +US$1.9 billion) contributed by copper was a result of a 5.0% fall yoy in Rio’s average realised copper price, to US$4.03 per pound. A feature was the US$900 million added by aluminium on a 14.9% yoy rise in Rios’ aluminium price, to US$3,330 a tonne. We have a positive view across the broad commodities spectrum for 2022, previous government spending programmes continue to ripple into the global economy, China reopens from its COVID zero policy and sticky inflation are all tailwinds. We expect a weaker US dollar, influenced by debt that continues to spiral higher and narrowing interest rate differentials to peer currencies will see the greenback as a major tailwind in 2023 for commodities.

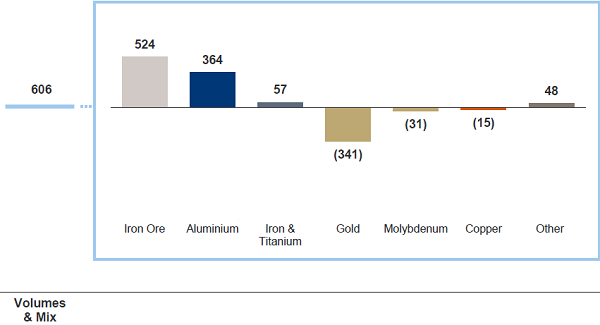

The factors controlled by Rio in the above EBITDA chart, shows Volumes and Mix and a feature of the result, contributed positive US$600 million, compared to negative US$583 million yoy. The contributors to the result are shown in the following chart (in US$/m):

Source: Rio Tinto

For Rios’ key product offerings, pleasingly, as Members can see from the above chart, the majority were in positive territory, with iron ore and aluminium standouts, while copper dragged in 2022. Iron ore was a positive US$524 million compared to negative US$894 million from a year earlier. Aluminium made a positive US$364 million impact compared to a positive US$258 million from a year earlier. Copper was a negative US$15 million swinging from a negative US$169 million in 2021. Briefly, we considered Rios’ operational result for 2022 was upbeat with some hidden gems. We expected 2022 operations would deliver a negative impact on Rios’ financials.

Net operating costs rose 6.4% yoy, to US$34.8 billion, with inflation and market driven costs had a US$3.5 billion negative impact on Rios’ EBITDA line in 2022. Energy costs of US$2.1 billion and general inflation pressures of US$2.0 billion were key contributors. Controllable costs had a negative US$900 million impact on the EBITDA line. On unit costs, Rio reported a 14.5% jump yoy in its Pilbara iron ore costs, to US$21.30 per tonne and is guiding 2023 to be in the range of US$21.00 to US$22.50 per tonne. Copper C1 unit costs surged 49.7% yoy, to US163 cents per pound and is guiding 2023 to be in the range of 160 cents to 180 cents per pound.

The daily chart movements of RIO show resistance has developed at the $128.00 level with the price declining to test the initial breakout level at $116.00. Current price movements remain below the 20 day moving average and above the 200 day moving average

On revenues of US$55.6 million representing a 12.5% yoy fall, Rio reported a fall of 37.9% yoy in underlying net earnings, to a US$13.3 billion and reported net earnings of US$12.4 billion, representing a 41.1% fall yoy. Underlying net earnings excluded US$820 million of US deferred taxes, movement closure estimates of US$178 million and a gain of US$331 million on the sale of the Cortez royalty. We consider these exclusions acceptable adjustments to reconcile Rios’ underlying 2022 net earnings result to net earnings.

Capital expenditure for 2022 fell 8.1% yoy, to US$6.8 billion and was split US$600 million to growth, replacement US$2.2 billion and US$3.9 billion to sustaining. We have no concerns over its modest capital spending programme.

Rio is forecasting capital expenditure of US$8.0 billion for 2023. Rio has provided guidance for 2024 and 2025 in the range of US$9.0 billion to US$1

Net operating cash flow fell 36.3% yoy in 2022, to US$16.1 billion. Weak commodity price movements drove the lower result for the year. Rio used this cash flow to sustain its operations and ultimately reward shareholders.

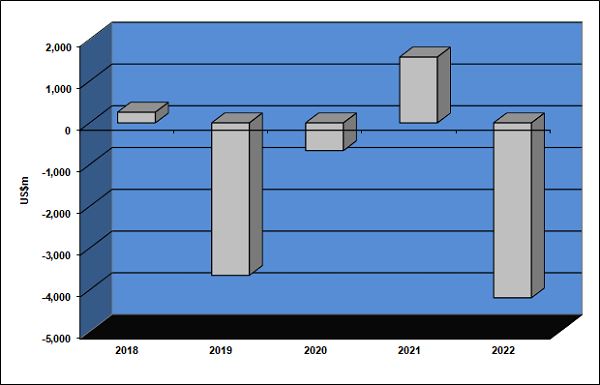

Rios’ balance sheet geared up in 2022, with a move back to a net debt position from a small net cash position in 2021. As of 31 December 2022, Rio reported a net debt of US$4.2 billion compared to a net cash of US$1.6 billion from a year earlier. The following chart shows net debt:

Source: Rio Tinto

As a result, Rio’s gearing ratio rose 1,000 bps to 7.0% as of 31 December 2022 from -3.0% from a year earlier. This read is substantially below Rios’ targeted range of 20% to 30% and proves it with the opportunity to regear if value from such spending warrants this action. Cash as of 31 December 2022 stood at US$6.8 billion and gross debt at US$11.1 billion. We have no concerns over the structure of the balance sheet.

Shareholders saw a cut in the dividend for 2022 to US$4.92 per share fully franked, which was well below the US$10.40 per share paid for 2021 but did include a US$2.47 special dividend. Rio indicated that its total cash returns to shareholders for 2022 was determined on a 60% payout ratio for the year. This years’ payout level is at the top end of the Boards’ targeted range of 40% to 60% of underlying earnings. We are pleased with the US$8.0 billion paid to shareholders in 2022.

With in the monthly view of RIO, significant support at $86.00 is identified, while the underlying chart price remains within an up trend and the price remains above the 12 month moving average

Rio Tinto experienced lower commodity prices in 2022, that delivered a softer set of financials for the year. We are pleased Rio Tino was able to deliver on the operational front in 2022 that was a partial offset to the negative pricing impact. We believe commodity prices will remain firm over 2023 and will continue to deliver a tailwind for Rio Tinto. With the share price sitting just below record highs this view may already be captured in the share price.

Consequently, we continue to recommendation Rio Tinto as a hold.

Disclosure: Interests associated with Fat Prophets hold shares in Rio Tinto.

[/subscribe_to_unlock_form]