In the nick of time

Nickel has not been spared from the ravages of the COVID-19 pandemic. The measures taken globally by governments to combat the spread of the virus were blunt; halt person to person contact. Populations went into “lockdowns” as 2020 rolled out and economic activity went into a nose-dive. The following chart shows real global Gross Domestic Product (GPD) growth highlighted is the Global Financial Crisis:

Source: International Monetary Fund

[emaillocker]

As Members can see from the above chart, global GDP growth has collapsed into negative territory in the early part of 2020. This collapse occurred as key economies including China, the United States, the European Union, Japan the United Kingdom and a host of countries including Australia, literally shutdown.

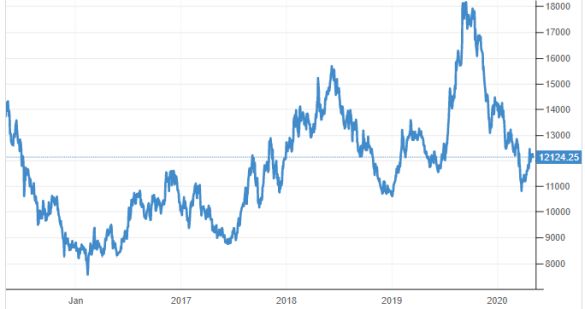

Commodity prices were swept along in the turmoil, as demand “actual” and “forecast” collapsed. The nickel price was swept into the maelstrom. The following chart shows the nickel price (in US Dollar per tonne):

Source: Trading Economics

The nickel price had recently, as Members can see from the above chart, caught investor attention on the back of its use in lithium batteries. The source of this interest was the pending electric vehicle (EV) revolution with a lithium ion battery powerplant and the nickel content in these batteries. The arrival of the COVID-19 pandemic in very late 2019 and its presences still quick drove the nickel price down.

Already, as Members can also see from the above chart, the nickel price has recovered from recent lows, as the grip of the pandemic in some countries is already loosening. Many countries are now planning and implementing COVID-19 exit strategies.

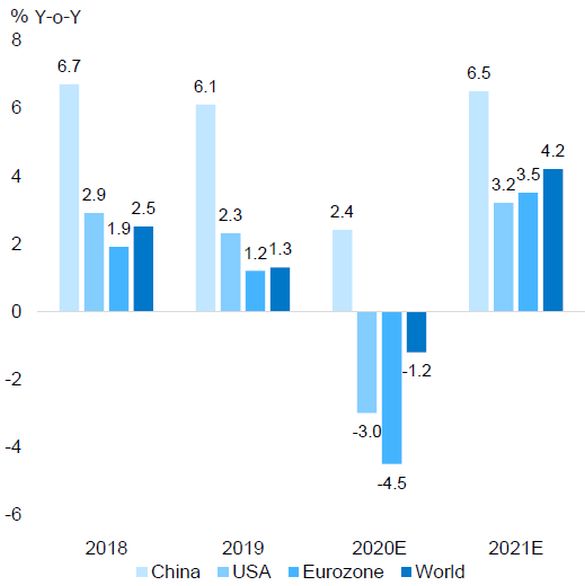

The price recovery in nickel is under way as forecasts for global GDP growth improves, and the shape of its steep dive and recovery gains investor confidence. The following chart shows real global GDP growth forecasts including key economies:

Source: Reuters consensus

There is no doubt that Global GDP growth will be negative in 2020 being the peak year for the COVID-19 pandemic. The recovery is however forecast to be a classic “V” recovery. There are still risks in the pandemic, as countries move toward restarting economies, with the biggest being a second wave, given there is no readily available vaccine, so caution, in our view, is warranted.

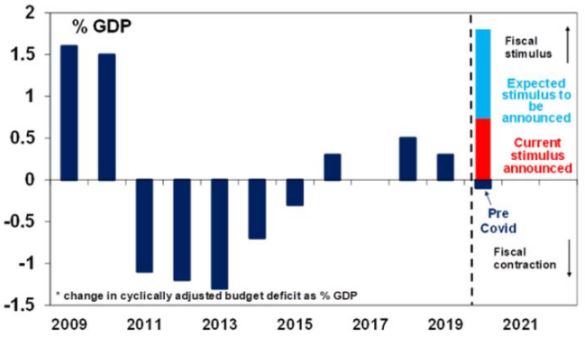

The driver of this classic recovery is the concerted efforts by governments and central banks to “spend their economies back to life.” Governments cumulatively are spending trillions on stimulatory packages – Donald Trump alone is seeking a further US$2 trillion of spending. As a percentage of GDP, government fiscal spending for 2021 is forecast to turn negative. The following table shows forecast fiscal spending by the G20 countries as a percentage of total GPD:

Source: Bloomberg

G20 government fiscal spending in light of the COVID-19 pandemic is forecast to rise by circa 200 basis points to a positive 1.75%. This is a significant reversal in government spending that will, we believe, shape the global recovery and also act as a medium to longer term tailwind for commodity prices, including nickel, as this spending rolls out into each country’s economy. Adding to this tailwind are the actions of central banks in lowering and sustain at low levels cash rates. Cheap debt will allow economies to leverage recovery spending with higher dollar amounts.

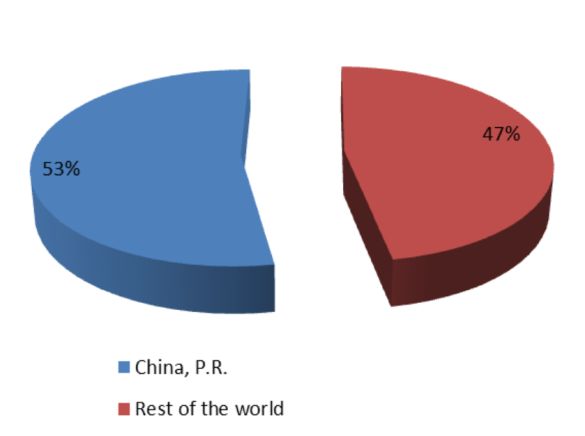

A key takeaway with the consensus forecasts is that for China, the country first impacted by COVID-19, is the first looking to the light at the end of the tunnel. Although China’s GDP growth is forecast to slow significantly, it is expected to maintain growth. This is heartening, as China is the biggest consumer of nickel by far. Nickel demand was circa 2.4 million tonnes in 2019. The following chart shows China’s 2018 appetite for nickel as a percentage of total demand:

Source: International Nickel Study Group

With China moving toward normal life, post its brush with the COVID-19 pandemic, we would expect China’s demand for nickel to return. With nickel primary used in steel and China’s steel industry returning to post COVID-19 levels, bodes well for nickel demand out of China. Currently, some 70% of nickel is used in the manufacturing of stainless steel, with 5% going into batteries. The other usages are in alloys 8%, plating 8%, castings 8% and other 1%. The minor usages will play only marginable role in demand. We expect in the near-term that the steel industry will be the main driver of the nickel price, and we are of the opinion this industry has a robust future, given the expected government spending on infrastructure.

We recently reviewed the lithium market and the coming EV revolution. Our view on this market, has not changed, even with the advent of the COVID-19 pandemic. The production of auto batteries to power EVs will play a major role in nickels future. The reason the EV revolution is crucial to nickel is that a current EV battery requires some 50 kilograms of nickel for some 60% of a batteries content. There are battery applications being developed with that could see nickel usage increase to between 80% and 90% content. Nickels availability and cheaper price makes it an ideal substitute in batteries for the likes of cobalt and lithium. Members can view our Lithium report here.

With demand for nickel in a recovering, from the COVID-19 pandemic, global economy starting to look more secure, supply will also play a key role. We do expect to nickel production to remain robust over the years ahead. The nickel market was on our estimates in surplus in 2019 with nickel production coming in around 2.43 million tonnes, to give a surplus of 50,000 tonnes on demand of 2.38 million tonnes. In 2021 we expect nickel production will grow by around 4% on 2019, to 2.53 million tonnes, with COVID-19 have only a minor impact of production. Demand however will be impacted and although we expect a “V” shaped recovery in the global economy, demand will fall around 3% on 2019, to 2.3 million tonnes. The surplus will grow to 230,000 tonnes in 2021. We expect this surplus will shrink in 2022 and 2023 and beyond, as the first of several mega battery factories come on stream. We do however remain circumspect around the industry’s ability to sustain the supply of nickel.

We believe the US Dollar will play a role in driving commodity prices higher with a view that the US Dollar should weaken. A key factor is building for this to occur. The aforementioned US fiscal spending programmes will swell already high debt levels, from the current circa US$23 trillion and spiral higher to put pressure on US Dollar. We see a weak US Dollar as a tailwind for commodity prices including nickel over the remainder of 2020 and 2021.

With the COVID-19 pandemic on the wane in China and many governments throwing major spending programmes at their economies, an inflection point for commodity prices including nickel is here. We do however remain cautious over the ability of supply to react. We will continue to seek out quality producers in the vein of Western Areas and Independence Group, which are both already in the portfolio, that have a low-cost profile and long-life production potential.

Disclosure: Interests associated with Fat Prophets hold shares in Western Areas and Independence Group.

[/emaillocker]