On Thursday, Wall Street rotated away from big tech and toward value and small caps, shaking off an Oracle-led slide. The dovish Fed backdrop is fuelling a breadth expansion beyond the Mag 7 favourites.

The S&P 500 added 0.21% to 6,901, while the Nasdaq fell 0.25%. Leadership continued to rotate towards the other benchmarks as the Dow Jones made a new record high at +1.34% to 48,704. The Russell 2000 also made a new record high, up +1.21% to 2,590. Oracle plunged almost 11%.

Oracle’s decline raised concerns in the market around AI rollout, burning cash faster than profit generation. Another growing concern is that the hyperscalers providing compute power will soon become commoditised, with more competition and capacity leading to margin and price pressure.

Oracle shares plunged to the bottom of the S&P500 table. Capex totalled $12 billion in the quarter, triple the outlay a year earlier and about 50% above consensus, and the company lifted FY capex guidance to $50 billion from the $35 billion previously projected.

More concerning is that Oracle is having to rely heavily on debt for this. Another wrinkle is that OpenAI represents much of Oracle’s future AI revenue plans, and investors are rightly questioning how the ChatGPT developer will meet the $1.4 trillion in future commitments it has made. Oracle’s debt has exploded to $100 billion, and the cost of insuring Oracle’s debt against default (think credit default swaps) has jumped.

Oracle’s fiscal second-quarter revenue climbed a moderate 14% YoY, while net income rose to $6.14 billion from $3.15 billion, but this was mostly driven by a $2.7 billion pre-tax gain from the sale of the stake in chip designer Ampere.

After surging 60% a new record high above $340, Oracle has crashed back to earth, hitting key support at $194 on Thursday.

The data weighed on the broader AI theme exposures and tech, but traders quickly put that money to work in other segments, as shown by the pressure on the Nasdaq, but solid gains in the Dow and the Russell 2000.

The dovish tilt by the Fed this week removed one last important hurdle for the US stock market. I continue to see the rally underway, taking the key US benchmarks into new record territory over the coming weeks with a strong finish to 2025 and a decent start in the new year. The weaker dollar should also sustain a risk-on rally in other asset markets, including precious metals & commodities, international equities and emerging markets.

While several prominent bears have begun circling the US stock market and economy, I continue leaning into a more bullish view, and the rally underway could continue for some time and well into next year. On this front, Morgan Stanley strategists have called it well this year and advise investors should “tune out the noise and brace for more growth ahead”.

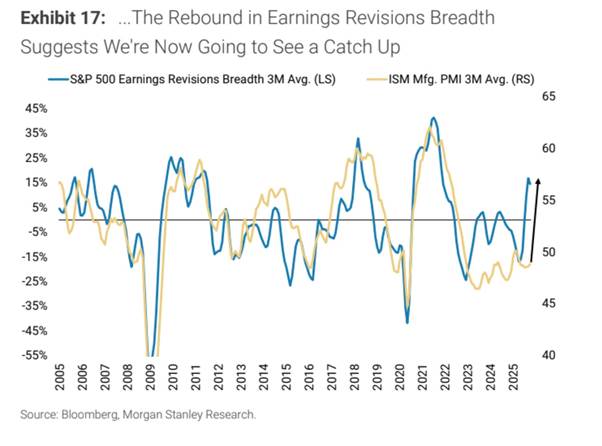

The labour market is under growing pressure in the US, and with layoffs now running at the highest level in decades and the unemployment rate on the rise, pressure will be maintained on the Fed to continue easing. This environment is conducive and supportive for equities. There has also been a significant rebound in earnings revisions as companies and Wall Street raises forecasts, as noted by MS.

Source: Morgan Stanley

In a recent interview, Andrew Pauker said that “earnings revisions breadth for the S&P 500 troughed at negative 25% in April, it’s now around positive 15%. We typically only see these types of rebounds in early-cycle environments. This is a clear sign to us that business confidence is improving.”

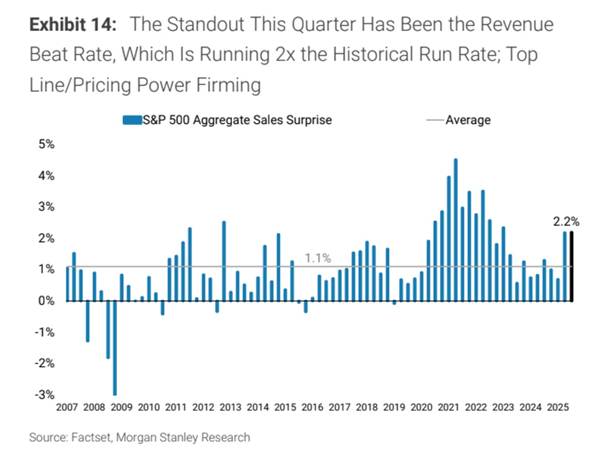

MS also cited that wage growth has slowed, giving profit margins room to expand, and that consumer demand appears poised to accelerate higher. One signal for this is that companies are starting to exhibit higher pricing power, meaning they can increase prices without significantly impacting demand. As noted above, another support will come from the Fed cutting rates, and I expect two more cuts next year as the labour market slows. MS expects the S&P 500 to rise 14% in 2026, to 7,800, with not tech, but cyclicals and consumer discretionary names outperforming. Morgan Stanley joins other investment banks, including HSBC, Bank of America, and JPMorgan, in calling for the outperformance of cyclical stocks next year. (as noted earlier, like James Hardie, US:JHX, and Zillow, US:Z, in the US, which are poised to benefit from a recovery in the US housing market as rates head lower).

Source: Morgan Stanley

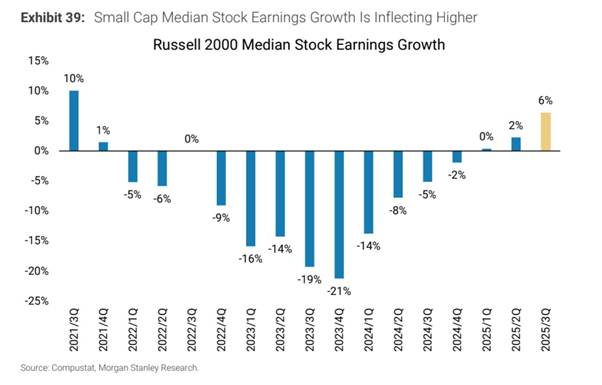

This week, the Russell 2000 broke out to new record highs following a multi-year consolidation. I see this rally and rotation into small/mid-caps continuing into next year, where the Russell 2000 and Russell 3000 are much more sensitive to lower interest rates. We are also likely to finally see rising earnings growth for the median stock in the Russell 2000. MS pivoted to the Small/Midcaps several weeks ago.

Source: Morgan Stanley

Another high conviction view we have for 2026 is that the US dollar will resume this year’s decline, which has been the biggest in 30 years. Precious metals could put in another strong year with many global investors and financial institutions still having little to no exposure to the sector. On this front, Goldman Sachs noted that “American investors barely own any of it, which means gold could have more room to run.

Goldman noted that even with gold hitting repeated highs, “US ownership hasn’t budged much. Gold ETF exposure is still six basis points, or 0.06 percentage points, below its 2012 peak since the launch of gold ETFs in the mid-2000s, according to Goldman’s analysis published on Wednesday. The low gold allocation is simply because ‘portfolio growth’ has outpaced gains in gold prices and volumes over the past decade.” This is a decent point, and I would argue that total global exposure to silver and other PGMs, including platinum, is even lower.

Goldman analysis showed that “while gold has surged to new all-time highs in 2025, the rally hasn’t translated into meaningful increases in actual US ownership. Gold ETFs make up just 0.17% of private US financial portfolios as of the second quarter — a microscopic slice of the roughly $112 trillion Americans hold in stocks and bonds.” While bonds have done better in recent weeks, I am bearish over the medium to longer-term outlook and see the asset class as being one of the worst performing, looking ahead towards the end of this decade. Precious metals are a natural hedge to a weaker bond market, and we have already seen central bank diversification into gold. This trend will likely continue.

Goldman’s analysis found that “fewer than half of large US institutions managing over $100 million hold any gold ETF position at all. Among those that do, allocations typically sit between 0.1% and 0.5%. For major long-term investors, only about 0.2% of their portfolios are in gold.” And Goldman also noted that at the retail level “despite the social media buzz around Costco gold bars and US Mint coin sales, physical gold demand in the US is tiny compared with ETF flows — just 11 to 15 metric tons year-to-date, versus roughly 400 tons of net ETF buying. The gap between those recommendations and reality is exactly could push gold’s next leg higher.”

I have made this point many times this year, and precious metals, despite their record-breaking run this year, are still underowned by global investors – and are therefore likely still a long way from an eventual top. The correction that played out several months ago served to work off overbought conditions and over positioning, eliciting many bearish commentators who predicted the end of the bull market. That group has since been proven wrong. Bull markets rise on a “wall of worry” and expire on euphoria and hype. We have yet to see precious metals become overly crowded at the top. Even the major central banks that have been buying (China) have a long way to go before gold reserves held equal the median by other major economies.

Silver this year has also blown past most forecasts (including ours) at the beginning of the year. The market appears to be now repricing silver amidst rising demand estimates, given that the metal is increasingly being linked to the build-out of AI infrastructure. Surging industrial demand and persistent supply tightness have also been another driver. Veteran Wall Street strategist Ed Yardeni this week said that silver’s explosive rally can’t be understood without acknowledging its growing importance to the AI economy. “As AI data centre construction accelerates and chip demand rises, silver has effectively become another AI play.”

As digitalisation and AI adoption accelerate, so too does the demand for critical materials involved in their applications. Commodities and metals in particular are critical to the rollout of infrastructure. Silver is a critical metal used in the AI buildout. Data centres increasingly rely on next-generation chips (such as GPUs and TPUs) equipped with high-performance semiconductors that use silver in their internal connections and packaging. As AI moves into autonomous vehicles, manufacturing and humanoid robotics, the broader electronics ecosystem is set to draw even more heavily on silver-rich components.

Meanwhile, following decades of under exploration with few new mines being brought into production, the silver supply remains very tight. We have seen inventories at the key metal trading hubs in Shanghai and London fall to historically low levels. Demand for silver has exceeded actual supply for many years now. This gap has historically been plugged by above-ground supply, but this inventory is drying up.

In the US, there is also now a growing chance that the White House could soon classify silver as a rare metal and impose tariffs. This has kept inventories and stockpiles in the US elevated.

I see the bull market in precious metals continuing next year, aided by US rate cuts, and potentially another decline in the dollar. Bonds have also been weaker around the world, and therefore, central bank buying of gold and silver should also continue.

On this front, PIMCO (one of the world’s largest bond fund managers) expects gold and silver to continue doing well, with central banks holding more gold as opposed to Treasuries. As we saw in the 1970s, bonds delivered sharp losses for investors who owned them at the beginning of the decade. I am expecting a similar cycle to play out in the coming years as governments ramp up spending and deficits widen, which ultimately need to be funded through more bond issuance.

Silver has soared to new record highs after breaking out above the old 2011 ceiling at $49 (which now becomes key support) in a dynamic fashion.

The RBA left the cash rate on hold at 3.6% this week. Money market trades have turned decidedly pessimistic on rate relief following recent ‘hot’ inflation prints. The blue line below illustrates how Australian sovereign bond yields have jumped across the curve from levels a month ago (represented by the green line) and how they compare to a year ago (orange line).

While only time will tell, we remain of the view that the jump over the past month could prove to be a classic overreaction. The recent hot inflation prints contained some ‘noisy’ data that could easily settle in the coming few months. Right now, the message from the RBA is that it will remain data dependent, which is understandable.

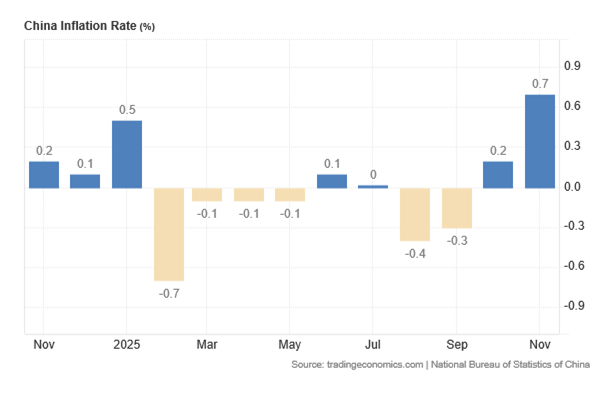

In China, the latest consumer and producer price data were mixed. Headline consumer prices rose 0.7% in November, accelerating sharply from October’s 0.2% and the strongest reading since February 2024, broadly in line with market expectations. This is encouraging given the more concerning deflationary fears that dominated markets a few months ago.

The improvement in the CPI was driven in part by the long-awaited turn in food prices. Core inflation held at 1.2% for a second month, the highest level in 20 months and a sign that underlying price momentum has stabilised. On the other hand, factory-gate prices painted a more challenging picture. The 2.2% annual fall in the PPI reflected a faster decline driven by a deeper 3.6% slide in durable goods.

Positively, headline CPI picked up

In London, stocks were muted this past week. Domestic data reinforced a cautious tone. BRC-KPMG figures showed UK retail sales growth easing to the weakest pace in six months in November, with total sales up just 1.4% YoY versus 1.6% in October and 2.3% in September. The softer backdrop came despite still-elevated inflation and was attributed to “pre-Budget jitters” that dampened Black Friday enthusiasm.

Separate Worldpanel data showed grocery inflation stuck at 4.7% in the four weeks to 30 November. Retailers are leaning heavily on discounts ahead of Christmas. Survey evidence suggests around one in five households continues to struggle financially, underlining the squeeze on discretionary demand.

Of course, the economy and the stock market often diverge. The FTSE100 is trading close to record highs seen in November, and UK blue-chips continue to look relatively inexpensive versus many international peers.

Japan’s rising bond yields are dragging the cost of borrowing up for the entire world. This dynamic has also been a saving grace for the US dollar recently, though we continue to have conviction that structural forces will hurt the greenback over the coming quarters.

Meanwhile, speculation is building that the Bank of Japan will raise rates at the December 18-19 gathering. Mid-week, the 10-year Japanese government bond yield added 1.5bp to 1.965%, reaching the highest level since June 2007, though it has pulled back a bit as we head into the weekend.

Carpe Diem!

Angus

Sign up to receive full reports for

the best stocks in 2025!

Where to Invest in 2025?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.