- In the US, PCE inflation printed above 4% for the first time in three years – and the bond market eased anyway. We explain why that’s the signal, not noise.

- We’re holding a contrarian position that the data went against this week. We outline the playbook on both sides.

- Gold retested $4,000. What the setup needs next.

- The US dollar broke above its one-year range this week – and we think it’s nearing the last move before the reversal. What flips it.

- Australian housing auction clearances have collapsed to 40%, and the first crack just showed up in bank credit. What it means for the RBA and the markets.

- Report Spotlight: A blue-chip income stock (BUY-rating) that the market sold off for no reason of its own – a circa 5.7% grossed-up yield, the capex cycle finally behind it, and cash now flowing to dividends and buybacks.

The fatLITE is the weekly read. Membership is the position. Half price ends June 30. Try it with our 30-day money-back guarantee.

Apply code FP50% at checkout

The corner is set – oil falling, the inflation rationale draining away, the mechanism intact. The market is simply scoring the round the other way. We don’t think it lasts the distance, and we are content with our positioning heading into H2. The Fed’s preferred inflation gauge printed above 4% for the first time in three years, traders added a second rate hike to the strip, and the bond market held its full pricing of the first. On this week’s data, the consensus case for a hawkish Fed is defensible, and the tape said so clearly. The Nasdaq tracked toward its worst month since March 2025 as mega-cap and AI names came off, while the Dow and the Russell 2000 held or gained, sitting near a record high at the time of writing. The ASX 200 finished lower, down 0.68% on Thursday to 8,748, as materials and financials dragged on broad commodity weakness; Japan’s Nikkei round-tripped to a fresh record close on Micron’s read-through, while Hong Kong’s Hang Seng fell to a one-year low.

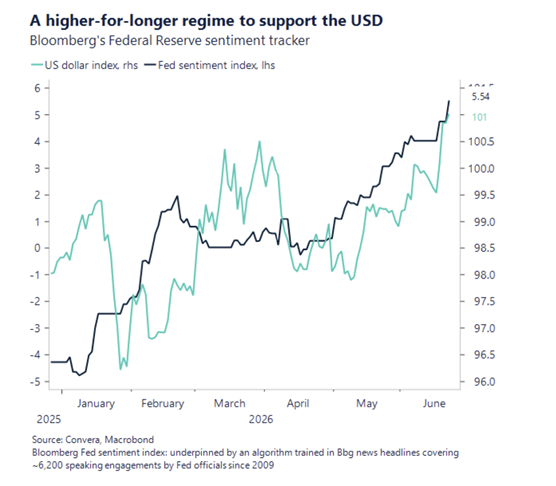

We take the other side of the Fed rate bet, though we acknowledge it is a contrarian position. The case rests on oil: crude has collapsed as Strait of Hormuz traffic normalises, and the same energy base effect pushing inflation above 4% today becomes a drag over the months ahead as crude heads toward the $60s. Four months from the midterms, we do not expect Kevin Warsh to hike into a softening economy. The week gave the view modest support and no confirmation. The PCE print landed in line rather than hot, and the bond market’s response was telling: the two-year eased to 4.12% and the ten-year to 4.39% on a print that should, on the hawkish reading, have pushed them higher. We read the easing yields as a tentative sign that the trade is getting crowded, not as the market changing direction. The dollar broke above its one-year range to 101.6 mid-week and then dipped to 101.45 on Thursday’s data, holding most of the move; the Australian dollar steadied near 69c, the yen slid to a 40-year low near ¥162.

The pivot in this thesis is the US dollar, which broke higher on the hawkish repricing and dragged gold, commodities and emerging markets down with it. Our wager is that it reverses when the hike bets leave the yield curve. It has not reversed yet, and resource-weighted portfolios have felt the punch.

Our central conviction is that the rate hikes the market has priced are not coming. The market disagrees, and it disagreed more loudly this week. One 25bps Fed move was fully priced for September, traders added a potential second for December, and the May PCE deflator rose to 4.1% year-on-year, above 4% for the first time in three years. Inflation is elevated and, on Austan Goolsbee’s reading, core is trending the wrong way. Meanwhile, Q1 GDP was revised up to 2.1%; the labour market held; and a resilient economy gives the Fed the room to move if it chooses.

We don’t see that happening, and one key reason is the oil reversion. The print that pushed inflation above 4% was driven by energy, and energy prices are now collapsing as Strait of Hormuz traffic normalises. The same base effect lifting the year-on-year figure today becomes a drag over the coming months as crude heads toward the $60s. New Chair Kevin Warsh has stripped all forward guidance from the FOMC statement, a signal that the path is not committed, and we do not expect him to hike four months out from the midterms into a softening economy.

Morgan Stanley’s Seth Carpenter, a former Fed official, framed the puzzle over the weekend: the tariff boost to prices is largely complete, oil is sharply lower, and the risk of second-round energy inflation has receded markedly, so the Fed’s 3.3% core forecast for 2026 looks high. We concur, and the implications are significant if the Fed holds this year and begins easing next year.

The dollar is the mechanism that carries this call into multiple other assets. It broke above the top of a one-year range this week on the hawkish repricing and a residual US-exceptionalism bid, running from 101 to just above 101.6 before easing to 101.45 on Thursday’s data. The resistance cluster above 102 was not cleared. Our view is that the breakout is built on the hikes, and that it reverses when the hikes leave the curve, with the Trump administration’s open preference for a weaker dollar adding to the ceiling. We want to be precise about the state of play: the dollar has not turned. It dipped on one print and holds most of its gain, and dollar sentiment sits high, which is the kind of crowding that tends to precede a reversal rather than guarantee one. Every commodity, gold and emerging-market call below is, at root, the same bet on this one instrument, and that bet is offside until the dollar rolls over.

Gold is the clearest case of the strong dollar at work, and metals positioning has been on the wrong side of it this week. Gold slipped over the week to around ~$4,000 at the time of writing, the lowest since November. Silver and platinum also lost ground. The constructive reading is that the correction has done real work. The overbought conditions built from the record $5,600 high have unwound, crowded positioning has cleared, and the complex now screens oversold against a dollar at a sentiment high.

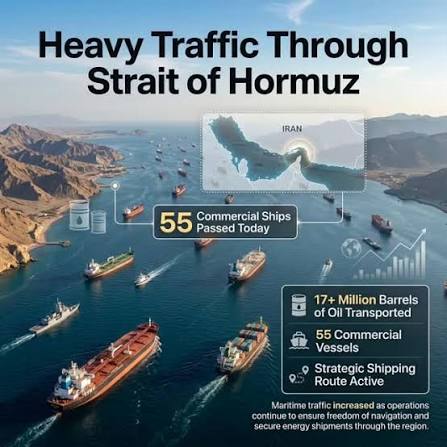

Oil is the engine under the inflation and rate thesis. WTI fell from $74 on Monday to below pre-war levels by Thursday before rebounding 2% to $71.80 on the report of an Iranian attack on a vessel in the Strait; Brent followed to $75. The supply picture is structural and points lower. JPMorgan’s Natasha Kaneva estimates June flows through the Strait at 5.1 million barrels per day, up from 2.9 million in May, and Persian Gulf exports have recovered to at least 75% of pre-war levels.

Iran is set to rejoin global markets in full with sanctions lifted for the first time since the 1970s, the UAE is leaving OPEC unconstrained, and China arrived at the reopening with stockpiles near full after reportedly cutting imports by roughly a third during the war. Our target for crude is the mid-to-high $60s, and if it gets there, the inflation shock that gave the hawks their argument is largely unwound. The Thursday bounce is the standing caveat: the path lower is not a straight line, and a Hormuz incident can spike the price at any time.

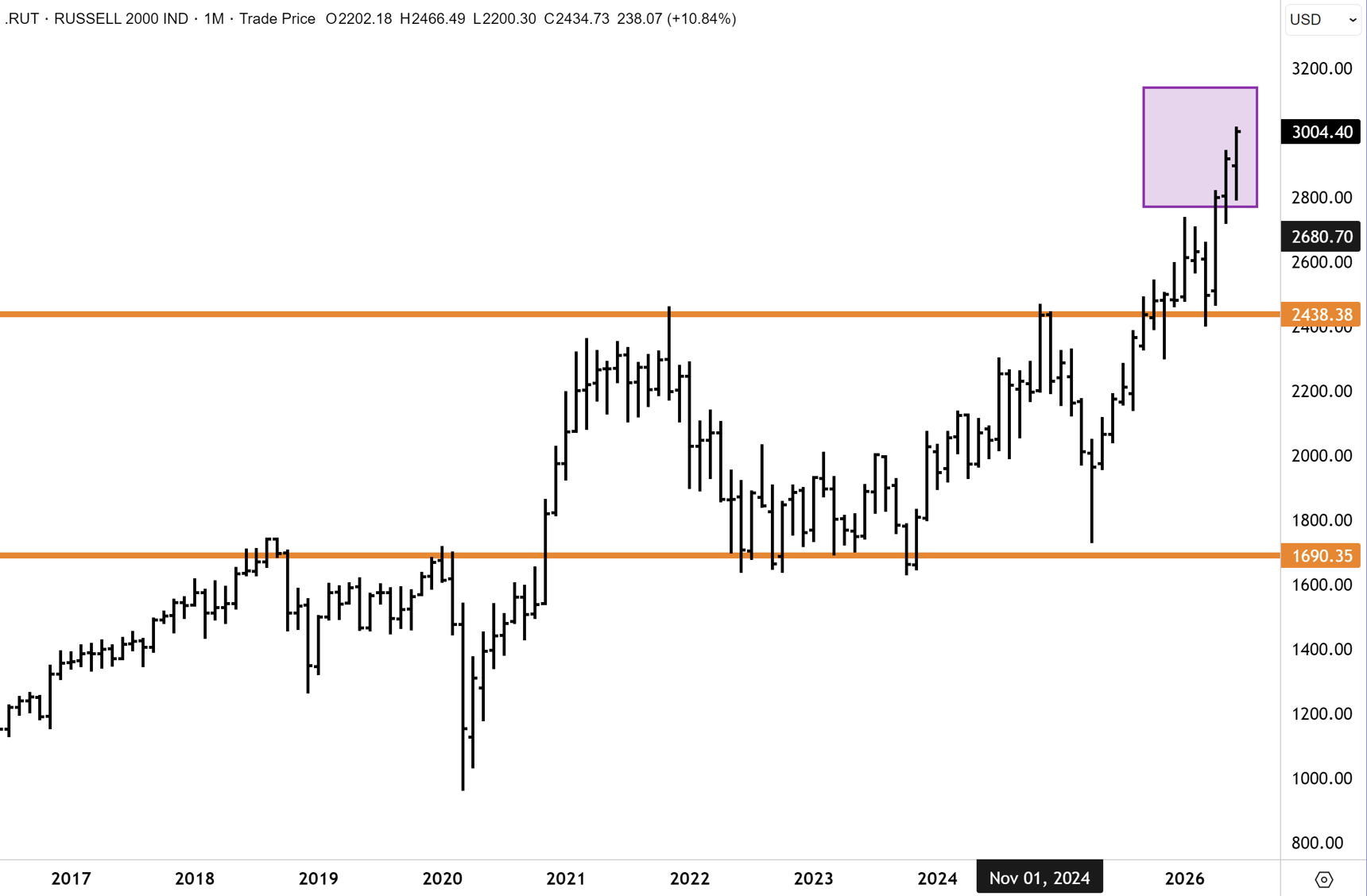

The structure of the US market sent a steadier signal this week when you look under the surface– think rotation, not a rupture. The Russell 2000 closed at a record high above 3,000 on Monday, the same session the S&P 500 and Nasdaq fell on technology rotation, and a small and mid-cap record against a declining Mega-cap index points to a broadening rather than a top. Tuesday’s AI flush looked alarming, with the KOSPI limit down 10%, but Micron then reported earnings well above estimates, and the chip names recovered, and capital kept moving into homebuilders, airlines, industrials and banks while the Nasdaq headed for its worst month since March 2025. We read this as rotation, not the end of the bull market, with the qualification that crowded momentum and AI names carry real drawdown risk if July earnings disappoint. That season, three weeks out, is the test.

The China and emerging-markets recovery thesis held its shape and is hostage to the same US dollar. The case is unchanged: China’s leading internet platforms hold dominant positions across cloud, payments, advertising, gaming and consumer ecosystems, and generate improving free cash flow at valuations that do not reflect the earnings trajectory. Mainland shares rallied on Micron’s read-through, but Hong Kong closed at a one-year low, with Alibaba off 4.4% and Tencent off 1.7%. Offshore China is the most dollar-sensitive corner of the complex. The thesis turns when the dollar turns. A local vehicle is the iShares China Large-Cap ETF (ASX: IZZ).

If our readers take one key idea from this week, it is this: we are betting that the rate hikes now in the curve do not survive a falling oil price, and that when they come out of market pricing, the dollar reverses and gold, commodities, the Australian producers and emerging markets turn upward together. We were offside this week. We hold the view because the mechanism, cheaper energy feeding through to lower inflation into a Fed that does not want to hike before the midterms, is sound.

The Local

The local market spent the week on the wrong side of the US dollar. The ASX 200 finished lower, down 0.68% on Thursday to 8,748, with the two heavyweight sectors that drive the index, materials and financials, both falling as the commodity complex sold off and the banks gave back ground. The bid turned defensive: healthcare rose 2.6% on Thursday as US-dollar earners gained from the stronger greenback, with staples and discretionary firmer on a household-spending number that beat before the detail undercut it. The Australian dollar held near 69c. This was the global picture that landed hard locally, and the trend was lower over the week for the benchmark ASX200.

An important domestic development sat underneath the index. Auction clearance rates have collapsed to 40%, among the lowest readings in decades, with nearly a quarter of listings withdrawn, and the trigger is policy. The Budget’s abolition of negative gearing has landed in the middle of an RBA tightening cycle. Morgan Stanley models a 10% national price fall in its base case and 20% in its worst, a decline that would rival the early 1990s; SQM Research sees Sydney down 9% and Melbourne 7% this year. JPMorgan called the falling clearance rates an ominous signal for the second half and noted the precedent: the Hawke government abolished negative gearing in July 1985 and reinstated it in September 1987 when the politics turned.

Angus wrote, “For the record, I am bearish on Australian housing for all the obvious reasons, but see a bottom next year as the market begins to price in a potential change in the Federal government and a reversal of key policies around negative gearing.”

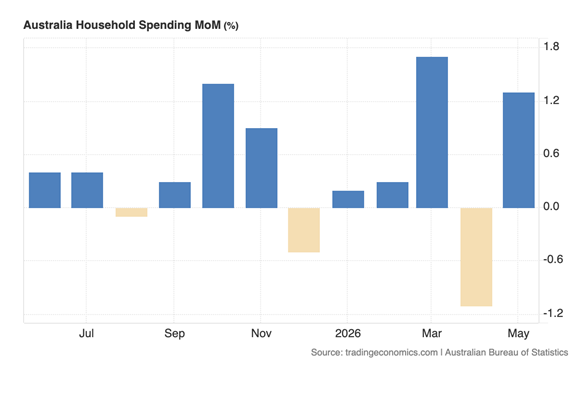

On that note, May’s job figures that released on Thursday, looked impressive on the surface. headline May employment and household spending beat expectations, though the devil is in the details. On the job front, 40,300 jobs were added against a forecast of 30,300, and the unemployment rate eased to 4.4% from April’s 4.5%. However, part-time positions accounted for the bulk of the gain at 35,200, while full-time employment contributed a modest 5,200. ANZ noted the two-month profile – a sharp rebound following a revised 40,700 loss in April – points to a flatter underlying trend rather than a genuine acceleration in hiring. Household spending also surprised to the upside, rising +1.3% in May against a +0.6% consensus, snapping back from April’s -1.1% decline. ANZ cautioned that distortions from transport-related refunds tied to earlier flight disruptions flattered the headline, making the underlying pulse softer than it appears.

Despite the headline beats, ANZ maintained its view that the RBA would look through single-month volatility, citing recent CPI outcomes and broader evidence of easing momentum as reasons to hold steady in the near term. We concur, but acknowledge that bond markets were less patient, pricing a meaningful probability of an August rate increase at the short end of the curve.

REPORT SPOTLIGHT

Telstra (ASX: TLS) – BUY

Defensives got sold when the Middle East ceasefire came through, and Telstra went with them, without the company-specific news to justify it. That’s the opportunity. The capex cycle that consumed free cash flow for years is now firmly behind the company, and the growing cash flow is being deployed as dividends and buybacks. The forward yield is circa 5.7% grossed up, and dividends should grow at a mid-single-digit pace over the next few years, funded by mobile ARPU momentum and an AI-driven cost-out program. Spectrum repricing risk is real, but at 8.3x NTM EV/EBITDA for a structurally improving free cash flow profile, the selloff has created a genuine entry point.

Telstra’s recent selloff over the past few weeks has all the hallmarks of investor rotation away from defensives following the conclusion of the ME war. The ASX200 has also underperformed since the budget. However, we maintain a technically bullish stance on Telstra, given that the company is a dominant Australian provider of mobile services, which is an essential service to customers. Similar to the banks, AI will also underpin greater efficiencies, and with CAPEX winding down, Telstra is also a future cost-out story.

Telstra has encountered resistance at the 12-year highs above $5.60, which has been the catalyst for a corrective reset. Support is well defined now at $5 and below. We remain of the view that Telstra definitively exited a primary downtrend last year, which had been in place since 2000. We maintain conviction that Telstra has finally breached above a 25-year primary downtrend into a new bullish cycle. We believe there is nothing suspicious about the recent correction, which is a pattern playing out in other major telcos, including BT Group, Vodafone and Orange in the UK and Europe. Following the incumbent consolidation phase, we believe upward momentum will soon resume and that this year’s highs could be retested by December.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

Have a great weekend.

Carpe Diem

Angus