Strong skew expected in the second half

Legacy Archive of Australian Financial Research & Market Publications by Fat Prophets

This archive contains more than 4,000 legacy financial publications — including Australian stock reports, market analysis, market commentary, market predictions, special reports, and portfolio income reports — originally published under Fat Prophets’ flagship Australasian Equities Portfolio and prepared by Fat Prophets’ in-house equity analysts under the supervision of Fat Prophets Chief Investment Officer Angus Geddes.

These publications were originally released exclusively to Fat Prophets members between 2003 and 2017 and reflect the firm’s independent research process, including fundamental analysis, technical analysis, and contemporaneous market views at the time of publication.

Fat Prophets has made this historical research archive publicly accessible to promote transparency, preserve a documented record of past market analysis and investment thinking, and provide investors, researchers, and readers with valuable educational and historical financial content.

Please note: This archived material is provided strictly for educational and historical reference purposes only. It reflects market conditions, economic data, company information, forecasts, opinions, and analysis as they existed at the time of original publication and may no longer be current or applicable. This material does not constitute current investment advice, financial product advice, or a recommendation to buy, sell, or hold any financial product or security.

To explore more current insights and discover the benefits of full membership, including access to Fat Prophets’ latest research, model portfolios and investment recommendations, visit our Products page.

Legacy Content

Shares in Equipment Financier Silver Chef (ASX, SIV) have drifted lower following the release of the company’s interim result. While the result wasn’t a bad one, with both revenues and the company’s rental asset base growing strongly on 1H16, the impact of the fraud event (covered in FAT-AUS-800) last November and a rise in bad debts weighed. Management are confident in the outlook for the second half of the year however, with this reflected in their decision to pay out 100% of the 12.9 cents earned per share over the period in dividends.

As a recap, last year Silver Chef announced that it had been a victim of a fraud event. This involved certain customers colluding with vendors to defraud the GoGetta business of $4 million worth of assets across a number of low dollar value contracts. At the time it was flagged that this would result in a one-off after tax impairment charge of $2.2 million in 2H16, with this since increasing slightly to $2.3 million. In our view this matter was appropriately dealt with, with management responding swiftly and implementing additional fraud protection procedures.

On an underlying basis NPAT fell 9 percent on the comparable period in 2015, to $6.9 million. Management are forecasting a strong skew in FY17 earnings towards the second half of the year, with underlying earnings guidance maintained at around $23 million – $25 million. Some of the recent weakness in the share price following the announcement could be attributed to investors being sceptical that Silver Chef will be able to achieve this 233 percent growth in underlying earnings in the second half.

Silver Chef will remain held in the Fat Prophets Portfolio.

We suspect that hitting the FY17 guidance will be a challenge given the underlying performance in the first half. If Silver Chef can succeed in this however, the share price is likely to see a positive re-rating.

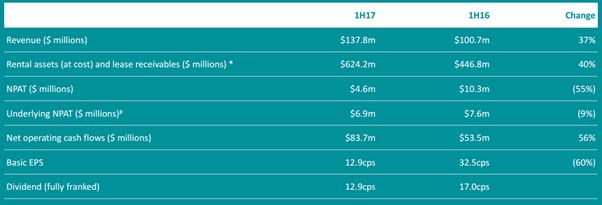

The Half Year Result to 31 December 2016

Source: Silver Chef

Turning to the 1H17 result and revenue was up 37 percent on the previous comparable period to $137.8 million in line with a 40 percent rise in rental assets and lease receivables to $624.2 million. Growth in the asset base was supported by the $7.5 million equity raise in September last year.

The Australia and New Zealand Hospitality business performed strongly over the six month period, with this region’s asset base growing 27 percent on the previous year

underpinned by a solid performance in the coffee and franchise channels. The New Zealand business was a standout, with a 33 percent increase in its rental asset base on 1H15, significantly improving its contribution to group earnings. Performance out of Canada was also stellar, with originations up 49 percent year on year, and the rental asset base up 54 percent on the previous quarter to $22.3 million. Silver Chef continues to invest for growth in this market, growing brand awareness by strengthening its existing sales team in Toronto and expanding into Quebec.

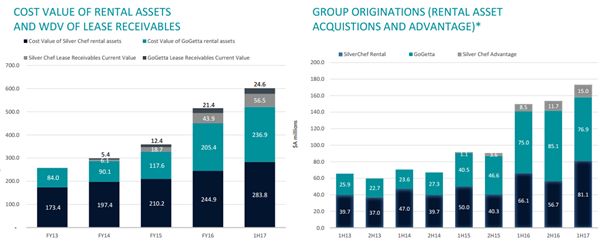

Source: Silver Chef

Bad debt and impairment charges were higher than historical averages

in the GoGetta business over the six-month period due to management working through contracts written prior to the tightening of credit policy in March 2016. This was the primary contributor to lower underlying earnings compared to 1H15, but this trend is expected to correct as the GoGetta portfolio matures and the Company improves its credit controls. As such bad debt is forecast to be proportionally lower in 2H17 as historical problem contracts are worked through.

As a result of last year’s fraud incident, the company has significantly increased its investment in internal audit and risk management resources, as well as implementing advanced identity verification software

. Silver Chef has also engaged anti-fraud consultants and re-assessed and re-accredited a material portion of its GoGetta equipment vendor network to ensure vendor quality. We are comfortable with the actions that the company is taking to ensure an incident such as this doesn’t happen again.

GoGetta will remain a significant segment of the business however, accounting for 44 percent of group originations in 1H17. As previously flagged by the company, FY17 is expected to be a year of consolidation for the GoGetta business as the company works through a structured plan to maximise recovery on outstanding arrears an improve returns on capital deployed. Continued strong demand for the GoGetta product gives management confidence that this segment will return to growth following this period of consolidation.

Source: Silver Chef

In terms of funding, as at 31 December 2016 Silver Chef held a $400 million senior debt facility with $80 million in capacity available to support future growth. This compares with total assets of $507.7 million. In addition, the company has received support from two major Australian banks and is in the advanced stages of finalising commercial terms for a securitisation warehouse facility. This is expected to be available in the first half of FY18, with the objective to fund new originations of Silver Chef and GoGetta rental contracts, and to purchase the Company’s book of finance leases.

Looking ahead, FY17 guidance remains unchanged, with underlying earnings expected to be between $23 million to $25 million

. Management expect second half earnings to be driven by improvements to the average contract life and effective rental yields as the portfolio matures, and growth in Canada. As the GoGetta portfolio matures revenue is expected to rise as the portfolio reweights towards contracts originated after the 1 percent increase in rental rates in May 2016. Further gains are expected from a modest level of overhead savings due to ongoing system efficiencies.

On the daily chart, the bearish moving average crossover present since December 2016 is suggestive of momentum to favour the downside (where the red 50-day moving average crosses below the green 200-day moving average). Positively, the rapid decline in share price has resulted in the RSI to venture into oversold territory. This is an indication of short-term downward momentum to be on the exhaustion trail. Coupled with the psychologically significant $7.00 whole number cleared, this bodes well for a period of strength to follow over the medium-term

Turning to the charts, and with reference to the monthly, prices have entered a corrective phase of the overall technical cycle. At present, prices are in flirtation-mode with the 50% Fibonacci retracement region of $7.31. Should the bears remain in control, then an additional layer of support is situated at the 61.8% Fibonacci retracement of $6.15 over the medium-term. As downward momentum is clearly in play, it is important that a basing formation unfolds over the months ahead as this would assist with price stabilisation.

S

ummary

Silver Chef’s interim result demonstrated strong growth in both revenues and the company’s rental asset base, but the impact of last year’s fraud event and a rise in bad debts weighed. Management are confident in their outlook for the second half of the year however, with FY17 guidance of underlying earnings of $23 – $25 million maintained and 100% of the 12.9 cents earned per share over the half year to be paid out as a dividend.

The fraud event resulted in a one-off after tax impairment charge of $2.3 million in 2H16, and a rise in bad debts saw NPAT fall by 55 percent on the previous year to $4.6 million. While the fraud incident was unfortunate, we are comfortable with the actions the company is taking to ensure an incident such as this doesn’t happen again.

Management are forecasting a strong skew in FY17 earnings towards the second half of the year, with underlying earnings guidance maintained at around $23 million – $25 million

.

The shares are trading on a FY17 PE of 10.6 and a dividend yield of 5.9 percent. We currently have a hold rating on Silver Chef, on the back of the long-term growth story and the company’s offshore expansion prospects. Having taken profits previously, we are comfortable remaining with the stock.

Silver Chef will remain held in the Fat Prophets Portfolio.

Disclosure: Silver Chef is held with the Fat Prophets Concentrated Australasian Share, Income, and Small & Mid-Cap Models.