In Bunnings we trust

Legacy Archive of Australian Financial Research & Market Publications by Fat Prophets

This archive contains more than 4,000 legacy financial publications — including Australian stock reports, market analysis, market commentary, market predictions, special reports, and portfolio income reports — originally published under Fat Prophets’ flagship Australasian Equities Portfolio and prepared by Fat Prophets’ in-house equity analysts under the supervision of Fat Prophets Chief Investment Officer Angus Geddes.

These publications were originally released exclusively to Fat Prophets members between 2003 and 2017 and reflect the firm’s independent research process, including fundamental analysis, technical analysis, and contemporaneous market views at the time of publication.

Fat Prophets has made this historical research archive publicly accessible to promote transparency, preserve a documented record of past market analysis and investment thinking, and provide investors, researchers, and readers with valuable educational and historical financial content.

Please note: This archived material is provided strictly for educational and historical reference purposes only. It reflects market conditions, economic data, company information, forecasts, opinions, and analysis as they existed at the time of original publication and may no longer be current or applicable. This material does not constitute current investment advice, financial product advice, or a recommendation to buy, sell, or hold any financial product or security.

To explore more current insights and discover the benefits of full membership, including access to Fat Prophets’ latest research, model portfolios and investment recommendations, visit our Products page.

Legacy Content

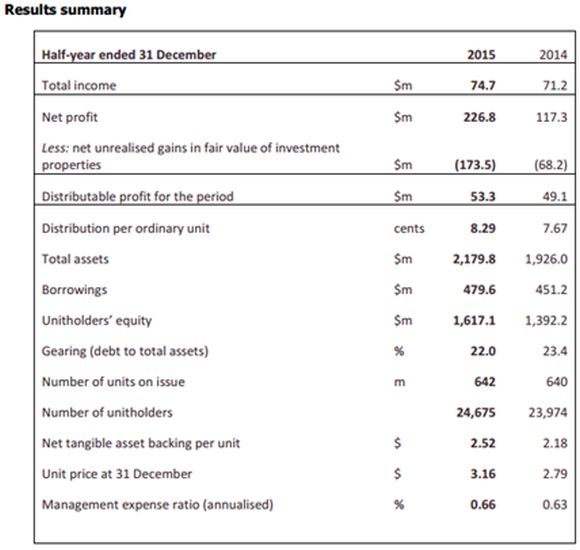

BWP Trust (ASX: BWP) released its FY16 interim report in February, showing the Trust continues to generate sound income growth and returns from its property portfolio during the first half of the financial year. The value of the portfolio grew by $179.3 million to $2,160.5 million after the revaluation, while rental income generated from the property portfolio also had a steady increase of 2.5 percent on a like-for-like basis in 2015

BWP Trust also boasts strong capital management ability, demonstrated by lower cost of debt and extended weighted average duration of its debt facilities. Management expects the position will be further strengthened as they plan to continue to benefit from the low interest rate environment and increase utilisation of existing debt facilities.

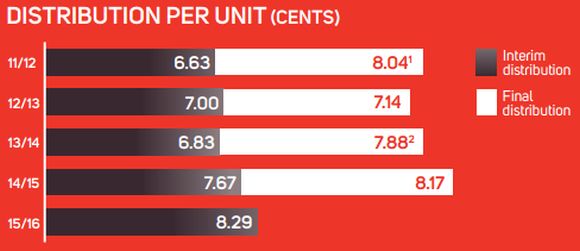

We are also encouraged to see BWP Trust is able to maintain its 100 percent pay-out ratio and has declared a distribution of 8.29 cents per unit during the first half year. This is up 8.1 percent from the previous corresponding period. In our view, the Trust has been able to fund future growth through debt due to its favourable liquidity position.

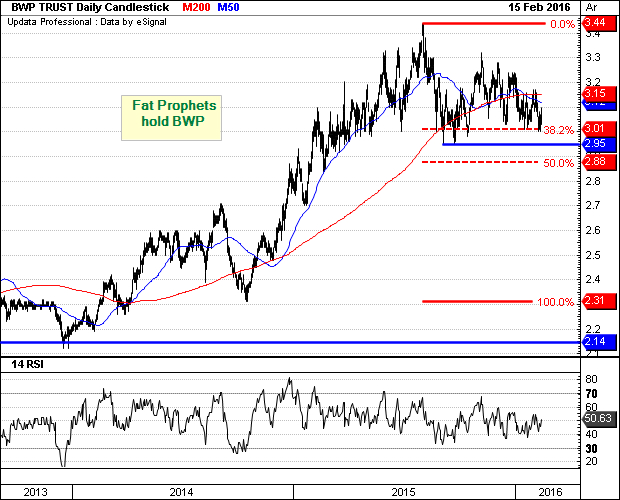

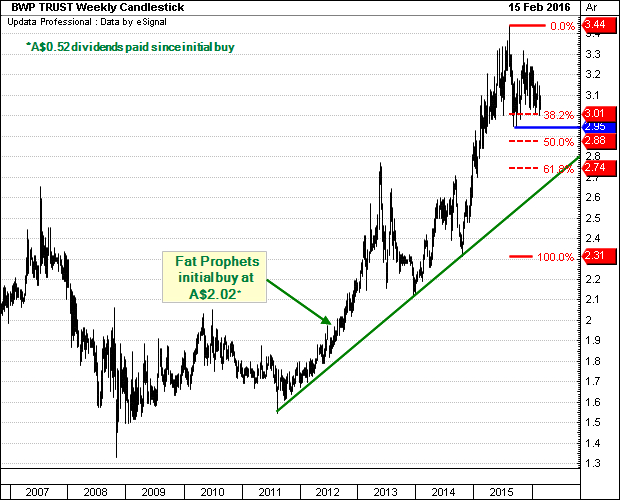

Turning to the charts, a break above both the 50 and 200 day moving averages (above $3.15) is required in order for bullish momentum to follow. Should this scenario unfold, then this would increase the probability of a re-test of resistance at the August 2015 high of $3.43.

Half year results

For the six months ending 31 December 2015, BWP Trust reported total income of $74.7 million, up 4.9 per cent or $3.5 million over the previous corresponding period. This is largely attributed to rental growth from both the existing property portfolio and store expansions completed during the period. The Trust also generated a distributable profit of $53.3 million, representing an increase of 8.5 per cent on the previous comparable period due to a lower average cost of debt.

Source: BWP Trust Interim Results

BWP has developed an optimised investment property portfolio through active divestments, acquisitions and developments. During the first half of FY16, the entire property portfolio has been revalued and the results show that the value of the portfolio grew by $179.3 million to $2,160.5 million. While the Trust’s weighted average capitalisation rate for the portfolio has decreased from 7.33 percent in FY15 to 6.81 percent in1H16 after the revaluation, but a lower capitalisation rate has resulted in a net revaluation gain of $173.5 million at 31 December 2015.

Source: BWP Trust Interim Results

In addition, the strong investment property portfolio allowed the Trust to generate steady rental growth of 2.5 percent on a like-for-like basis in 2015, slightly dropping from the previous 2.7 percent growth. In our view, the drop in rental growth was driven by a subdued market and low levels of inflation, we believe there is clearly upside to this over the medium-term. It is worth noting that the Trust has maintained its 100 percent occupancy rate during the first half of FY16.

The completed store expansions have also generated solid additional rental income and contributed strongly to the Trust’s income growth in 1H16. In August 2015, the Trust completed a $4.6 million expansion project on its Lismore Bunnings Warehouse, which is expected to increase annual rental by approximately $0.3 million to $1.3 million. Furthermore, another $4.6 million expansion of the Trust’s Rockingham Bunnings Warehouse was also finished during 1H16. This will boost annual rental income by approximately $0.3 million to $2.0 million. To further optimise its investment property portfolio, the Trust has entered into a conditional contract with an unrelated party to sell the Cairns property that was vacated by Bunnings in 2015, and the transaction is expected to be completed by the end of March 2016.

During the second half of FY16, there were 47 leases to be reviewed in line with the consumer price index (CPI) or by a fixed percentage increase, while there are also five market rent reviews of Bunnings Warehouses, of which one relates to the year ending 30 June 2015, to be completed by the end of this financial year. Therefore, we expect the Trust’s property income to grow and contribute incrementally to the annual results.

In addition, BWP Trust boasts strong capital management ability, demonstrated by lower cost of debt. In 1H16, the Trust increased utilisation of debt facilities to benefit from the low interest rate environment in Australia. As a result, its weighted average cost of debt dropped from 5.79 percent in 1H15 to 5.06 percent in 1H16, while weighted average duration of the debt facilities also extended from 3.3 years to 3.7 years. This further leads to a 7.4 percent decrease in finance costs to $12.3 million during the period.

Management expects the cost of debt will further decrease to approximately 5.0 percent at the end of FY16 as they plan to continue to increase utilisation of existing debt facilities during the second half. We believe this is likely to be achieved given its low gearing ratio (debt to total assets) of 22.0 percent. The ratio currently sits in the Trust’s preferred range of 20 to 30 percent, reinforcing its healthy liquidity position.

BWP Trust’s leverage to any near-term increase in CPI or market rental rates is boosted by the Trust currently having 79.2 percent of its borrowings subject to interest rate hedges, this is marginally higher than the Board’s preferred range of 50-75 percent. Furthermore, the differential between BWP Trust’s weighted average lease expiry profile of 6.4 years at 31 December and its debt maturity profile for interest rate hedges of 2.66 years is also positive, in our view.

Interim distribution

Based on its strong operation and strong balance sheet, BWP Trust is able to maintain its 100 percent pay-out ratio and will distribute $53.3 million profits, 8.29 cents per unit, to its unitholders on 25 February 2016. This represents an 8.1 percent increase from the previous corresponding period. The Trust has been able to fund future growth through debt due to its favourable liquidity position.

Moreover, management also advised the distribution reinvestment plan allocation price for the six month period ending 31 December 2015 of $3.09 per unit.

Source: BWP Trust Interim Results

Corporate Governance

In August 2015, BWP Trust announced John Atkins, Non-executive Director, resigned from the Board to take up the position of Agent General for Western Australia in London. In addition, the Trust also announced that that Erich Fraunschiel has succeeded John Austin as Chairman following Mr Austin’s retirement at the end of 2015. Mr Fraunschiel has extensive experience not only on the board, but also investment banking and venture capital investment. We believe the current diverse backgrounds in commercial property, private property funds, investment banking and accounting has provided the Trust with a strong set of knowledge to support its strategies.

With reference to the weekly chart, a period of consolidation is likely over the medium term. Support is initially expected at $3.00 (key psychological level), followed by the $2.95 region, which is made up of the 38.2% Fibonacci retracement (measured from the October 2014 low of $2.31 to the August 2015 high of $3.44) and horizontal support (September 2015 low). The longer-term uptrend remains intact, and thus we would view the current period of softness as corrective in nature.

Summary

We continue to like BWP Trust given its optimised investment property portfolio, which is underpinned by a high quality tenant in Bunnings. The value of the property portfolio grew by $179.3 million to $2,160.5 million after the revaluation conducted during 1H16. In addition, the strong investment property portfolio allowed the Trust to generate a steady rental growth in 2015.

Currently, we believe a subdued market and low levels of inflation limit the growth of rental income, and there is clearly upside to this over the medium-term. It is worth noting that the Trust has maintained its 100 percent occupancy rate during the first half of FY16.

BWP Trust also boasts strong capital management ability, evident by the lower cost of debt and extended weighted average duration of their debt facilities. Management expects the position will be further strengthened as they increase utilisation of existing debt facilities.

We are also encouraged to see the Trust is able to maintain its 100 percent pay-out ratio and has declared an interim distribution of 8.29 cents per unit, up 8.1 percent from the previous corresponding period. We believe the Trust has been able to fund future growth through debt due to its favourable liquidity position.

With the stock trading at around 17.7 times FY17 earnings and 1.3 times book value we are comfortable holding.

Accordingly, BWP Trust will remain firmly held in the Fat Prophets Portfolio.

Disclosure: BWP Trust is held within the Fat Prophets Australian Share Income and Australian Small & Mid Cap Models.