A green light from the referee

Legacy Archive of Australian Financial Research & Market Publications by Fat Prophets

This archive contains more than 4,000 legacy financial publications — including Australian stock reports, market analysis, market commentary, market predictions, special reports, and portfolio income reports — originally published under Fat Prophets’ flagship Australasian Equities Portfolio and prepared by Fat Prophets’ in-house equity analysts under the supervision of Fat Prophets Chief Investment Officer Angus Geddes.

These publications were originally released exclusively to Fat Prophets members between 2003 and 2017 and reflect the firm’s independent research process, including fundamental analysis, technical analysis, and contemporaneous market views at the time of publication.

Fat Prophets has made this historical research archive publicly accessible to promote transparency, preserve a documented record of past market analysis and investment thinking, and provide investors, researchers, and readers with valuable educational and historical financial content.

Please note: This archived material is provided strictly for educational and historical reference purposes only. It reflects market conditions, economic data, company information, forecasts, opinions, and analysis as they existed at the time of original publication and may no longer be current or applicable. This material does not constitute current investment advice, financial product advice, or a recommendation to buy, sell, or hold any financial product or security.

To explore more current insights and discover the benefits of full membership, including access to Fat Prophets’ latest research, model portfolios and investment recommendations, visit our Products page.

Legacy Content

Consolidation has been the key theme for the Australian telecommunication market during the past year. While TPG Internet finalised the transaction to acquire iiNet, M2 Group and Vocus Communications received regulatory approval from the Australian Competition and Consumer Commission (ACCC) to complete their $3 billion merger. Regarding the latter, the commission essentially concluded that the proposed deal would not significantly boost vertical integration between wholesale and retail telecommunications services providers, and will therefore not result in adverse changes to the competitive landscape.

Furthermore, while the ACCC did recognise that there was somewhat of an overlap between Vocus and M2 in the supply of retail and wholesale fixed broadband services and fixed voice services, it was of the opinion that the two companies do not directly compete with each other given their focus on different customer segments. M2’s businesses are weighted towards the residential (via the Dodo and iPrimus brands in Australia and Slingshot/Orcon in New Zealand) and small business markets, while Vocus focuses on the enterprise and government segment. This further indicates the complementary nature of the tie-up.

In addition, the ACCC has marked the merger of Vocus with M2 as the last big fixed line transaction in the Australian telecommunications sector. The commission is happy to see a new industrial landscape, with four big players unlikely to consolidate the sector any further, although noted that it will continue to closely monitor future developments.

As the fourth-placed player in Australian broadband market, M2 faces increasing challenges from industrial giants who have greater resources and scale to develop the market. The combination of Vocus and M2 Group will certainly create a business with superior scale. The merged company will combine Vocus’ telecommunications infrastructure and corporate customer base with M2’s demonstrated expertise at the consumer and SME end of the market. The new company will also be primed to leverage the National Broadband Network, which is being built across Australia and the UFB in New Zealand. Vocus boasts over 1,600km of metro fibre in Australia, and over 4,300km of intercity fibre in New Zealand.

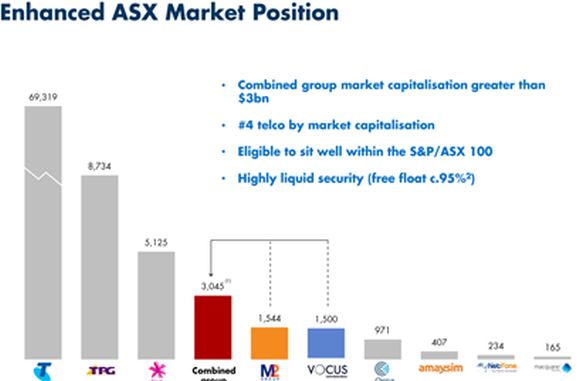

The merged company will firmly establish itself as the fourth-largest integrated telecommunication company in Australia and the third-largest in New Zealand, with forecasted revenues of around $1.8 billion and EBITDA (earnings before interest tax and depreciation) of around $370 million in FY16 (before synergies). The Company also narrows the gap with market leading players such as Telstra, TPG, and Spark, thus enabling it to contribute to the future innovation and growth of the sector.

Source: Asian Investor Presentation

In addition to the strategic merit, the deal will deliver cost synergies to the company’s shareholders. As indicated in the recent presentation to Asian investors, management advises that the combination of Vocus and M2 Group is expected to result in $40 million costs synergies per annum (albeit at a one-time cost of $20 million). This will not only include savings from network optimisation and consolidation by leveraging infrastructure assets, but also the savings from the removal of duplicated public company costs as M2 will delist from the ASX in early 2016. Vocus is targeting these synergies to be fully realised by the end of FY18.

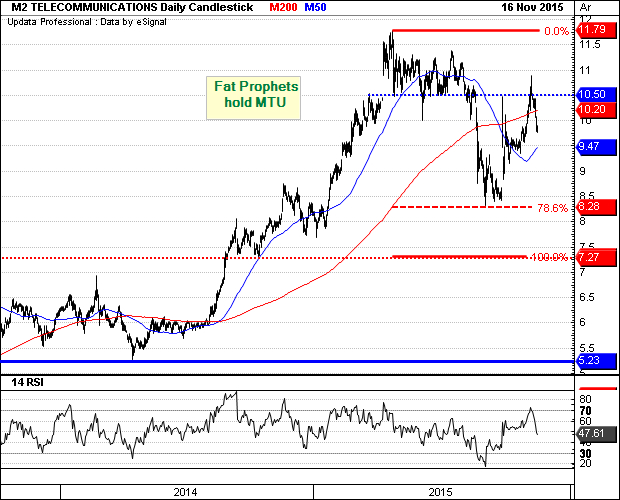

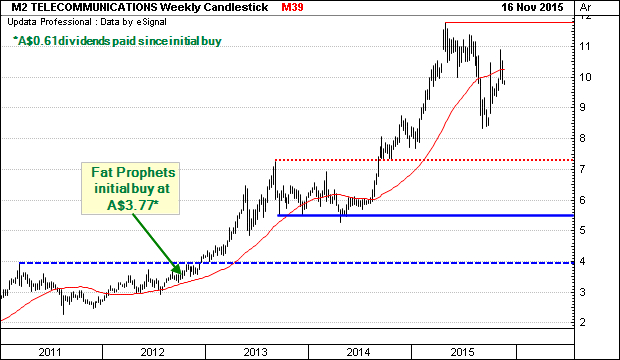

Turning to the technical outlook and the charting set up is quite positive. Following the bullish double bottom formation at 38.2% Fibonacci retracement, prices rotated to the upside, with current levels printing a series of interim higher lows below resistance of $4.39. However, with the bearish divergence currently in play, we would not rule out some form of a pullback in the interim.

From the longer term perspective, the momentum has stalled since prices hit all-time highs of $11.79 earlier this year. With the downside limited to support at $7.27, we envision further consolidation at current levels before the long term uptrend begins re-emerging.

Summary

The ACCC has passed the green light to Vocus’ acquisition of M2, with the commission believing that the deal will not significantly boost vertical integration between wholesale and retail telecommunications services providers. Given their focus on different market segments, the ACCC also concludes that Vocus and M2 do not compete with each other, which further highlights the complementary nature of the tie-up.

In addition, the commission has marked the combination between Vocus and M2 as the last big fixed line transaction in the Australian telecommunications sector. The commission is happy to see a new industrial landscape, with the four big players unlikely to consolidate the market any further, although this will continue to be monitored closely.

However, M2 shareholders are the ones who make the final decision and they will receive a scheme booklet in late 2015, with a vote scheduled for early 2016. We will be following developments closely and will alert Members of any action needed. For now we recommend that those holding M2 shares sit tight.

Accordingly M2 Group will remain firmly held in the Fat Prophets Portfolio.

Disclosure: M2 Group is held within the Fat Prophets Concentrated Australian Share, Australian Share Income and Australian Small & Mid Cap Models.