Predator becomes the prey

Legacy Archive of Australian Financial Research & Market Publications by Fat Prophets

This archive contains more than 4,000 legacy financial publications — including Australian stock reports, market analysis, market commentary, market predictions, special reports, and portfolio income reports — originally published under Fat Prophets’ flagship Australasian Equities Portfolio and prepared by Fat Prophets’ in-house equity analysts under the supervision of Fat Prophets Chief Investment Officer Angus Geddes.

These publications were originally released exclusively to Fat Prophets members between 2003 and 2017 and reflect the firm’s independent research process, including fundamental analysis, technical analysis, and contemporaneous market views at the time of publication.

Fat Prophets has made this historical research archive publicly accessible to promote transparency, preserve a documented record of past market analysis and investment thinking, and provide investors, researchers, and readers with valuable educational and historical financial content.

Please note: This archived material is provided strictly for educational and historical reference purposes only. It reflects market conditions, economic data, company information, forecasts, opinions, and analysis as they existed at the time of original publication and may no longer be current or applicable. This material does not constitute current investment advice, financial product advice, or a recommendation to buy, sell, or hold any financial product or security.

To explore more current insights and discover the benefits of full membership, including access to Fat Prophets’ latest research, model portfolios and investment recommendations, visit our Products page.

Legacy Content

M2 Group (ASX, MTU) has grown astutely by acquisition over the years but the shoe was firmly on the other foot on Monday. The company announced that it was ‘merging’ with Vocus Communications, which has itself has only just started integrating its most own recent acquisition, Amcom Telecommunications. The Vocus and M2 tie up will create the fourth largest telecoms company in Australia, and third largest in New Zealand, with a market cap of around $3 billion. Shares in M2 rallied 13 percent on Monday on the back of the announcement.

While touted as a ‘merger’ of equals, the deal looks to provide more of a kicker for M2 shareholders. Vocus has offered 1.625 of its shares for each M2 share. At the time of the offer this represented a 25 percent premium to M2’s share price on Friday, and will be implemented via a scheme of arrangement.

The market seems to have taken the view that Vocus is getting less of a ‘rub of the green’ as part of the deal, with M2 shareholders ending up with 56 percent of the enlarged company. M2 shares were also the top riser on the ASX200 on Monday while Vocus was the top faller.

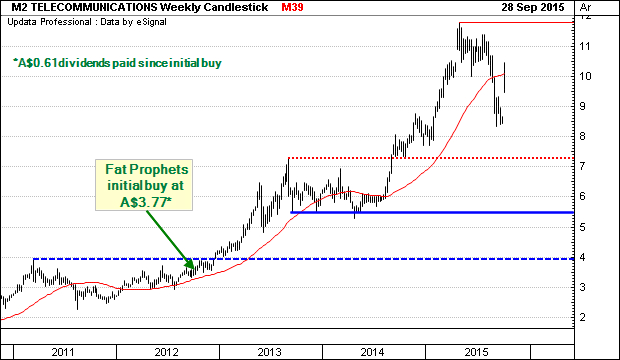

We recommended selling out of Vocus two weeks ago in FAT-AUS-739. Our view has been that the valuation of Vocus has become somewhat stretched, and unlike many other telcos the shares don’t have a lot of yield support. The weight of acquisitions has also dragged on Vocus’ share price, and we note that the recently purchased Amcom (previously held in the Fat Prophets Portfolio) operations have been starting to come off the boil as a result of its WA resource company customer base facing stiff headwinds. We believe that the company is banking on buying into ‘better’ growth with the M2 merger.

The combination of Vocus and M2 Group will certainly create a business with superior scale. The new company is expected to have combined revenues of around $1.8 billion and EBITDA (earnings before interest tax and depreciation) of around $370 million in FY16 (before synergies). The deal is unanimously supported by both boards, and is subject to M2 shareholder, court, and regulatory approval.

Source: Vocus investor presentation

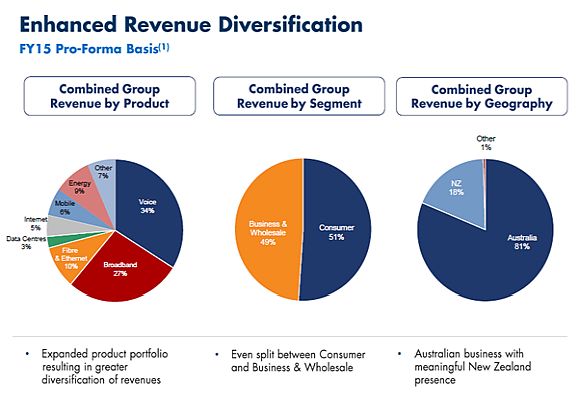

The deal has strategic merit and will deliver a vertically integrated behemoth. It combines the telco infrastructure and corporate clientele of Vocus with M2’s expertise at the consumer (via the Dodo and iPrimus brands in Australia and Slingshot/Orcon in New Zealand) and SME end of the market. The company will also be primed to leverage the National Broadband Network which is being built across Australia and the UFB in New Zealand. Vocus boasts over 1,600km of metro fibre in Australia, and over 4,300km of intercity fibre in New Zealand.

Management have also noted that the two companies have ‘closely aligned challenger cultures’ and are expecting substantial revenue synergies through the expansion of their product offering, and enhanced distribution capabilities.

There will also be significant savings at the bottom line. Cost synergies are set to reach a run rate of up to $40 million a year (albeit at a one-time cost of $20 million). Vocus is targeting these to be fully realised by the end of FY18.

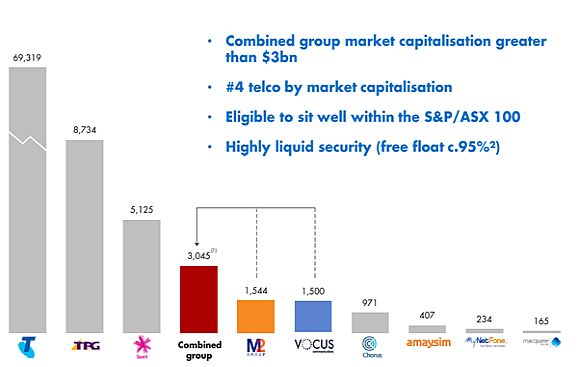

The company’s market cap should also sit well within the ranks of the ASX100, which will likely bring it onto the radar of more index trackers. It will firmly establish itself as the fourth largest player in Australia behind Telstra, TPG, and Spark. And given these players will remain ahead of the merger entity, we believe this should also quell any objections from a regulatory perspective.

Source: Vocus investor presentation

In terms of new management M2 also looks to be getting a slight tilt as well. While there will be four directors from each of M2 and Vocus, Geoff Horth (head of M2) will step up as the CEO of the merged group. David Spence, the Chairman of Vocus will maintain that position, with Craig Farrow of M2 his deputy.

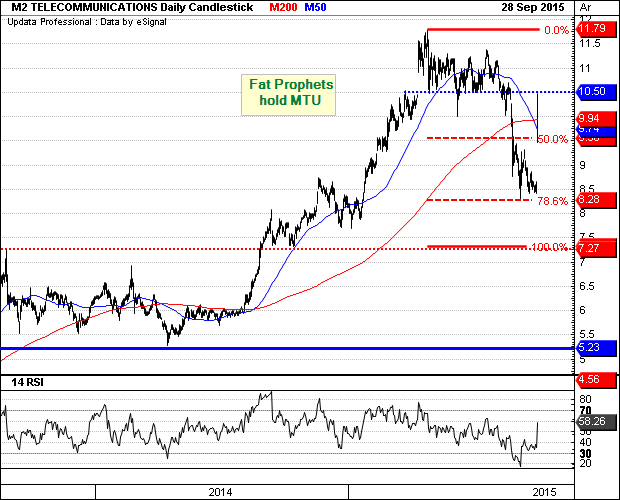

Turning to the charts and the technical outlook has undergone a major turnaround as prices have broken out from the previously set trading pattern. Last week’s bearish outlook has been cancelled out by yesterday’s announcement of the merger with Vocus. Underpinned by strong fundamentals, the shares have gapped up towards the $10.50 region, and higher levels are likely to be on the way as the merger becomes more of a certainty, or indeed should another suitor enter the fray.

Summary

The proposed merger between Vocus and M2 is a good outcome for M2 shareholders in that it has sparked a positive re-rating. The deal highlights the attractiveness of the company’s business model and indeed its modest valuation. We also however wouldn’t rule out another player joining the scramble for scale that we are seeing in the telcos sector. There is $15 million break fee payable by M2 in such an event but that would pale into insignificance if a materially higher price were forthcoming.

The move by Vocus (and share price reaction) though further highlights our logic for exiting the stock a few weeks ago, and why it has been forced to cede some ground.

M2 shareholders will receive a scheme booklet in late 2015, with a vote scheduled for early 2016. We will be following developments closely and will alert Members of any action needed. For now we recommend that those holding M2 shares sit tight.

Accordingly M2 Group will remain firmly held in the Fat Prophets Portfolio.

Disclosure: M2 Group is held within the Fat Prophets Concentrated Australian Share, Australian Share Income and Australian Small & Mid Cap Models.