Higher commodity prices drive record profit

Legacy Archive of Australian Financial Research & Market Publications by Fat Prophets

This archive contains more than 4,000 legacy financial publications — including Australian stock reports, market analysis, market commentary, market predictions, special reports, and portfolio income reports — originally published under Fat Prophets’ flagship Australasian Equities Portfolio and prepared by Fat Prophets’ in-house equity analysts under the supervision of Fat Prophets Chief Investment Officer Angus Geddes.

These publications were originally released exclusively to Fat Prophets members between 2003 and 2017 and reflect the firm’s independent research process, including fundamental analysis, technical analysis, and contemporaneous market views at the time of publication.

Fat Prophets has made this historical research archive publicly accessible to promote transparency, preserve a documented record of past market analysis and investment thinking, and provide investors, researchers, and readers with valuable educational and historical financial content.

Please note: This archived material is provided strictly for educational and historical reference purposes only. It reflects market conditions, economic data, company information, forecasts, opinions, and analysis as they existed at the time of original publication and may no longer be current or applicable. This material does not constitute current investment advice, financial product advice, or a recommendation to buy, sell, or hold any financial product or security.

To explore more current insights and discover the benefits of full membership, including access to Fat Prophets’ latest research, model portfolios and investment recommendations, visit our Products page.

Legacy Content

A huge contribution from higher commodity prices helped BHP Billiton towards a mammoth annual profit. The company has an immense store of world class resources to apply its burgeoning cash flow towards, requiring a multi-decade approach to capital allocation. Emerging economies remain important in the near term, but global demand will support commodity pricing for an extended period.

“Chinese steel production growth alone was responsible for US$11.1 billion of earnings growth…”

BHP Billiton announced a record annual net profit (before exceptional items) of US$23,648 million, an increase of 85.9% on last year. The final dividend was increased to US 55 cents per share bringing the full year dividend to US 101 cents per share, up 16.1% on last year.

The company completed its expanded US$10 billion capital management program over the year, but no new capital management initiative was announced with this result. We are not perturbed by this as the company has continued to make progress with its five year US$80 billion investment plan and has also made some acquisitions during the period that provide a productive use of the company’s capital.

The largest of these was the US$15.1 billion (US$12.1 billion of equity) acquisition of Petrohawk Energy announced in July. BHP also acquired HWE Mining (for US$735 million) which already provides contract mining services to the company’s West Australian Iron Ore operations. Both these acquisitions were made in the FY12 year and have not impacted the FY11 financial result.

Since 2004, BHP Billiton has repurchased US$22.6 billion of shares representing 15% of the company’s issued capital. Including dividends, returns to shareholders are more than US$48 billion since the company was formed in 2001.

The balance sheet remains in excellent condition with US$10.1 billion in cash as at 30 June 2011 and gross debt of US$15.9 billion. Gearing of 9.2% at balance date will clearly increase as a consequence of the new acquisitions (approximately 27% post Petrohawk) but considering the 78.1% increase in operating cash flow in FY11 to US$30.1 billion, we are not overly concerned about debt issues just now.

Earnings expansion

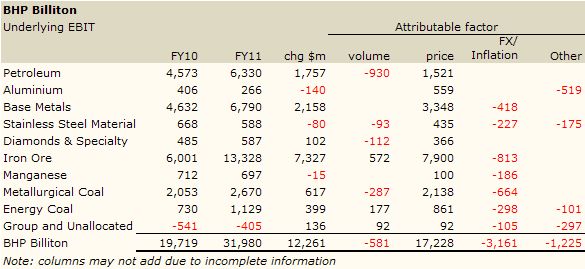

Most of that spectacular rise in cash flow was driven by the growth in underlying operating earnings.

The table (in US Dollars) above demonstrates the large impact that higher commodity prices had on the 62% increase in underlying EBIT across the every division.

In particular, iron ore prices contributed easily the biggest gain, assisted by the company’s transition to shorter term, market based pricing. That decision actually led to an US$8.5 billion gain but was offset by US$648 million of price-linked costs.

The average oil price increased 28% to US$93.29 per barrel across the year. Natural gas and LNG prices also increased 17% and 22% respectively. The combination contributed US$1.5 billion to the Petroleum division EBIT.

The average aluminium price increased 19% to US$2,515 per tonne while the alumina price increased 21% to US$342 per tonne.

Base metal prices were also higher with nickel up 24% during the period. Higher diamond prices added US$254 million to EBIT while higher titanium prices added US$112 million.

Hard coking coal prices were up 48% over the year contributing over US$2.1 billion to the result.

The table also reveals how the devaluation of the US dollar and inflation detracted from the underlying EBIT outcome by US$3.1 billion. These factors are outside of the company’s control.

Of course, not everything went perfectly from an operational perspective last year – it is unrealistic to expect so. The moratorium on deepwater drilling in the Gulf of Mexico was lifted during the year but impacted on activity in this very important region.

Lower copper grades were mostly responsible for a slightly tarnished performance at Escondida, but this will be overlooked for the massive 129% upgrade in resource announced recently.

The disruption to coal production in Queensland by flooding and cyclone Yasi chopped metallurgical coal production by 13% for the year. Reconditioning the mines from the water inundation, plus damage to infrastructure is taking longer than anticipated, placing pressure on unit costs.

As a general observation, higher input costs are beginning to emerge as an on-going issue across all operations. Raw materials, labour and electricity prices in particular are placing pressure on operating efficiency and margins. Chief executive Marius Kloppers noted that labour had become more expensive and less efficient, but these issues are mostly within the company’s control.

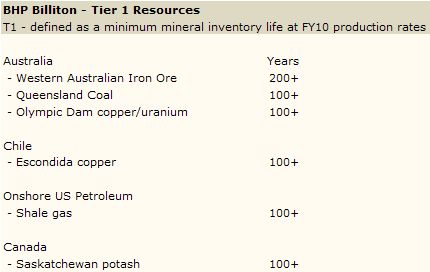

Treasure trove

Happily, BHP faces the far more daunting task of how to find, develop and mine its vast treasure trove of global ‘tier one’ assets.

During the year, the company approved 11 major projects worth a combined US$12.9 billion (BHP share) of investment. That is in addition to the US$11.6 billion spent on the business in FY11. Among the approved projects is a collective US$8.35 billion allocated to various iron ore projects. Metallurgical coal gathered US$2.5 billion of new projects and just over US$1 billion was approved in Petroleum.

BHP completed US$1.2 billion of existing projects and still has US$11.6 billion to be spent on already approved projects including US$3 billion on the Worsley alumina expansion and US$3.3 billion on various Australian petroleum projects in Bass Strait and the North West Shelf.

The company will spend about US$20 billion on capital expenditure in FY12, a gigantic number.

Perhaps the only real issue for investors to watch more closely from here will be the potential for project delays and cost escalation in the capital expenditure program. The company has talked more frequently of longer lead times for equipment and scarcity of other resources such as skilled labour. It is to be expected that very large projects, as all BHP projects tend to be, will always be challenging to deliver completely on time and budget.

A secondary factor will be several projects being undertaken over the next 5-10 years that will individually have lower rates of return but form a crucial step in the broader projects to which they contribute. These include the outer harbour expansion project at Port Hedland (Pilbara iron ore), the pre-stripping of overburden at Olympic Dam (assuming the expansion is approved), and potential port and rail infrastructure for Queensland coal.

While the Queensland rail idea is a recent ‘thought bubble’, it is a distinct possibility that would mirror the total logistics infrastructure of the Western Australian iron ore business.

We view the Olympic Dam expansion as a virtual certainty. The pre-stripping required to turn the resource into a giant open pit operation would necessitate removing something like 1 billion tonnes of earth each year to allow the mine to expand.

The following table is a simplification of the company’s resource base but indicates the premier position it occupies as the world’s largest mining company:

In summary, BHP has an enormous pipeline of world class resources that have very long asset lives. Each will require multi-decade development plans, not just years. In that sense, the allocation of capital (human and financial) requires constant revision, but always with a target for extracting an optimised return on the invested capital.

Outlook

BHP’s view of the world economy is positive in the long term but recognises the ‘near term challenges’. More specifically, the company is very positive on the emerging economies of China, India and elsewhere that are contributing a greater share of global economic growth.

This reality is spectacularly displayed by the company’s remark that growth in Chinese steel production (and therefore demand for iron ore and coking coal) during the year was responsible for US$11.1 billion of BHP’s increase in underlying earnings.

The temptation is to say that BHP’s earnings growth is almost solely reliant on China’s continuing urbanisation. The two are not independent but it would be wrong to characterise BHP’s prospects as entirely linked to China. We estimated China still only represents approximately 28% of BHP’s total revenue.

We also concur with BHP’s view that in addition to emerging market demand, progressively higher cost sources of new supply will continue to place upward pressure on commodity prices. Some of the near term supply constraints have been affected by temporary factors such as weather and these will abate.

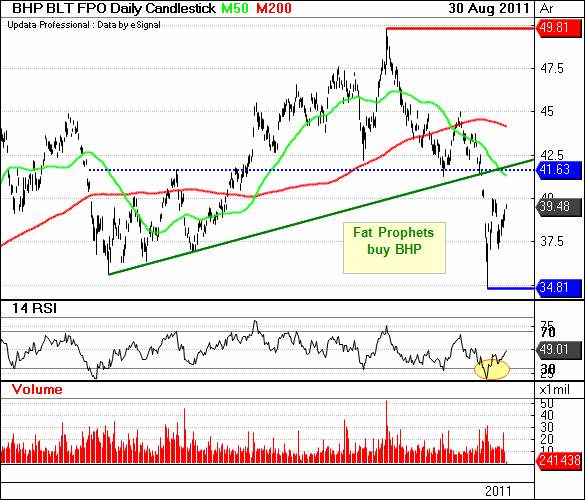

Since breaking out from the broader ascending triangle in October 2010 at $41.63, strong upward momentum followed. The recent high printed was $49.81 in April. Prices have since retraced sharply lower, only to find support at the $34.81 level. The oversold RSI is suggestive of buyers to emerge in the near term. Resistance is indicated at the confluence of the previously breached uptrend line and 50 day moving average at the $41.65 region.

With reference to the weekly chart, BHP found firm support at the $35 region, which coincides with the May 2010 low. Prices are currently testing the technically important 200 week moving average, which will now act as resistance at the $39 region. Prices need to close above this level in order for the longer term uptrend to continue.

Summary

It’s hard to go past BHP Billiton as a core portfolio stock. It offers compelling long term value below $40 and we continue to recommend the stock as a buy to all Members.