A sensible voting option

Legacy Archive of Australian Financial Research & Market Publications by Fat Prophets

This archive contains more than 4,000 legacy financial publications — including Australian stock reports, market analysis, market commentary, market predictions, special reports, and portfolio income reports — originally published under Fat Prophets’ flagship Australasian Equities Portfolio and prepared by Fat Prophets’ in-house equity analysts under the supervision of Fat Prophets Chief Investment Officer Angus Geddes.

These publications were originally released exclusively to Fat Prophets members between 2003 and 2017 and reflect the firm’s independent research process, including fundamental analysis, technical analysis, and contemporaneous market views at the time of publication.

Fat Prophets has made this historical research archive publicly accessible to promote transparency, preserve a documented record of past market analysis and investment thinking, and provide investors, researchers, and readers with valuable educational and historical financial content.

Please note: This archived material is provided strictly for educational and historical reference purposes only. It reflects market conditions, economic data, company information, forecasts, opinions, and analysis as they existed at the time of original publication and may no longer be current or applicable. This material does not constitute current investment advice, financial product advice, or a recommendation to buy, sell, or hold any financial product or security.

To explore more current insights and discover the benefits of full membership, including access to Fat Prophets’ latest research, model portfolios and investment recommendations, visit our Products page.

Legacy Content

The Independent Expert (IE) report said shareholders should vote for the NBN deal. We agree.

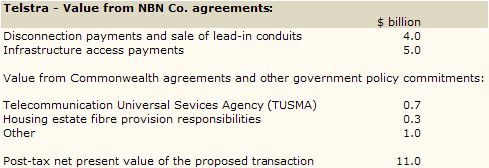

When the full NBN deal was finally announced back in June, we examined it in detail in FAT529. Most of the headline items had been well publicised, such as the $11 billion net present value of the deal as compensation for the disconnection of Telstra’s copper network and transfer of its customers to the NBN wholesale platform over the 10-year build-out of the new network.

At that time, Telstra made it clear that the NBN was government policy and it was faced with a choice of whether to co-operate or not. The findings of the IE report confirm that Telstra’s ‘co-operation’ scenario is indeed the most sensible choice for the company and shareholders to follow as the alternative would result in a disastrous sequence of corporate castration.

The IE report broadly agreed with Telstra’s calculations of the value to the company by co-operating with the government on the NBN deal. The value can be broken down into the following elements:

The Independent Expert needed to examine and assess the alternatives available to Telstra and its shareholders relative to the NBN deal that had been conditionally agreed to with the federal government. The IE report looked at several options including voting against the NBN deal which would have entailed a ‘compete’ scenario (with the NBN).

The ‘compete’ scenario was overwhelmingly rejected on the basis that the regulatory consequences to Telstra would have been too draconian. In particular, the government could have carried out its threats to prevent Telstra from acquiring spectrum required for future 4G mobile services and the functional separation of its businesses. Either would have been a disastrous outcome in the long run for Telstra, in our opinion, and fortunately has been confidently rejected by the IE report as well.

The ‘co-operate’ scenario then, is logically the best way to go for Telstra and under the IE report’s base case set of assumptions, delivers an outcome that is at least $4.7 billion better than any alternative outcome. The base case assumed by the IE is that the NBN is built and Telstra migrates its customers and infrastructure to the NBN Co. as per the deal.

At this point in the discussion, it would be tempting to think that the NBN deal was done and dusted as far as Telstra was concerned. The only outstanding matter is the ACCC approval of the structural separation agreement and that can hopefully be finalised with some careful attention to the necessary amendments.

NBN lite?

What intrigued us with the IE report was the heavy attention paid to the possibilities ahead if there was to be a change of government. The telecommunications policy of the incumbent government is well established, but if the Opposition was to win the next election, the IE report notes the future of the NBN could be called into question, at least in its current planned form.

The last sign-post we had in regard to the Coalition’s telecommunications policy was discussed in FAT487 which was just before the last federal election. At that point, the Coalition was talking about a $6.3 billion alternative NBN with much greater private industry participation and mix of technologies to achieve a similar outcome. No doubt this policy will continue to evolve along with the political landscape, but it would be reasonable to assume that the NBN would be substantially curtailed under a Coalition government.

If that was to happen, the IE report looked at what it would mean for Telstra in terms of the incremental net present value. In the case that Telstra shareholders vote for the current proposed transaction and the NBN is subsequently terminated on 30 June 2014 (a hypothetical date chosen by the IE), shareholders would be $11 billion better off compared to the $4.7 billion incremental net present value as discussed above.

In our view, this scenario is not entirely realistic as we would expect a Coalition government to be faced with a partially built NBN, be legally committed to the infrastructure lease payments for the next 30 years plus the new Universal Service Obligation payments ($230 million p.a.) and other commitments already agreed with Telstra.

It does seem logical that the NBN would be immediately reviewed and subsequently watered down into some form of fibre-to-the-node alternative – a far cheaper option.

NBN slow

Also of interest from the IE report was the different set of assumptions used in its base case scenario for the NBN. The IE report suggested the NBN will take two years longer to build than the current plan due to the sheer scale of the project which would be afflicted by the usual delays and problems associated with very large projects. This was simply a call on the practicality of the project and makes sense.

Additionally, the IE report said it had different expectations for the penetration of mobile-only households and mobile broadband usage. Both factors are relevant and will have an important bearing on the take-up rates of the NBN itself.

Wireless substitution is an established trend that is the de facto competitor to the NBN.

The IE report assumes that by the end of the NBN rollout (2024 under the IE base case assumption), mobile-only premises will have a 27.5% share of the voice market. That is, 27.5% of Australian households will have no need for the services of the NBN to make phone calls.

The IE report also assumes that 14% of Australian households will also use wireless broadband services by 2024, also avoiding the NBN.

These assumptions do not appear overly ambitious in our view and could have a big impact on the assumed take-up rates built into NBN Co.’s business model.

If the early internet service provider (ISP) retail pricing is an indication of what can be expected in areas where the NBN eventually takes over as the wholesale supplier, then many potential NBN-plus-ISP customers will be looking very closely at the wireless alternative services available from Telstra (and others).

Telstra will of course be competing vigorously for both fixed and wireless customers but will be ambivalent as to which platform a customer chooses. The NBN Co. will not as the government has committed it to a single technology platform.

It seems Telstra has received the better deal in terms of the fees paid for advice. The Independent Expert (Grant Samuel) was paid a fee of $2.8 million for the report.

In comparison, the federal government paid the KPMG McKinsey consortium $25 million in 2009 for its Implementation Study for the NBN.

Telstra is testing support at the 50 day moving average. Should prices lift from current levels, we would expect a retest of resistance at the $3.17 level in the near term. Downside support on the other hand is located at the technically important 200 day moving average of $2.89.

With reference to the weekly chart, the upper border of the downward channel is currently capping prices. A sustained break above this level would open up targets towards the 200 week moving average of $3.49 over the broader term.

Summary

The Independent Expert’s report on the NBN deal soundly supports the Directors recommendation to vote for the deal. We agree with this conclusion.

The report provides credible analysis that says Telstra shareholders will be better off to the tune of $4.7 billion by supporting the proposed transaction.

Shareholder approval of the NBN deal at the October 18 AGM would leave the ACCC approval of the structural separation undertaking as the only outstanding ‘condition precedent’ for the deal to be completed.

Telstra now has a degree of regulatory certainty within its grasp. With the instability of the last two and a half years almost behind it, the company can look forward to planning and executing its earnings growth path utilising its advanced digital network platforms in mobile and broadband as well as its national fibre-optic network.

We believe the company is fundamentally cheap under $3.00 per share and Members without exposure should buy at this level. The stock is further supported by the excellent gross dividend yield of 13.2%.

The Directors of Telstra are recommending that shareholders vote for the proposed transaction as it represents the best outcome under current government policy. The Independent Expert (IE) report on the ‘Proposed Transaction’ says the advantages outweigh the disadvantages. The financial benefits vary according to different scenarios modelled by the IE report but shareholders are being presented with a deal that recovers some real value for the “nationalisation” of its wholesale business and infrastructure.