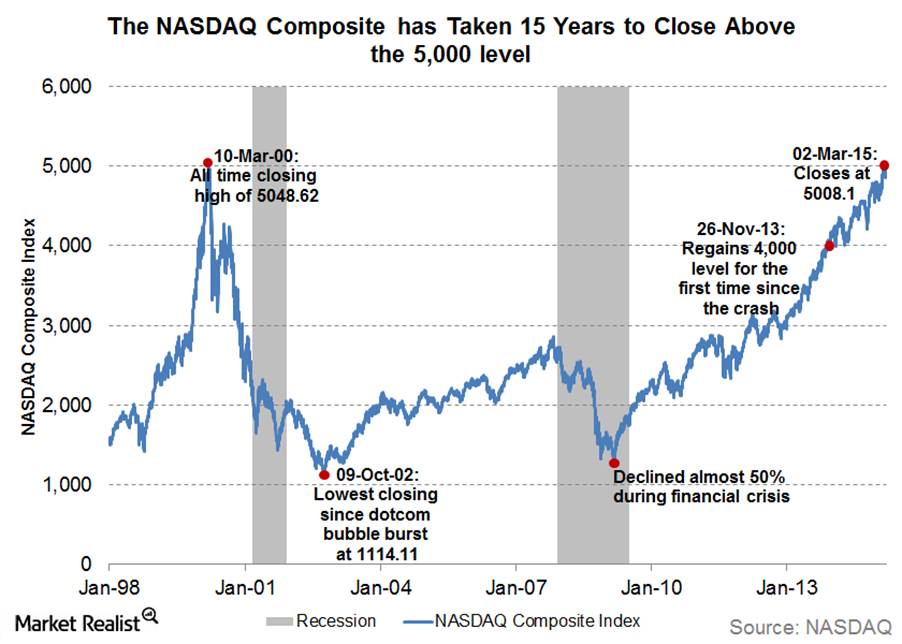

Echoes of 1999. History doesn’t always repeat, but “often rhymes”

As “animal spirits” around AI have gathered steam in recent weeks, the bull market has rolled on, which has elicited a number of warnings of a speculative bubble that could rival the dot-com craze of the late 1990s. In 2000, the Nasdaq technology index topped out and then entered a sharp decline that ended in a spectacular wave of bankruptcies.

Legendary hedge fund Paul Tudor Jones said during an interview on CNBC this week that markets feel exactly like 1999 – “it might not be a replay exactly but all the ingredients are in place. The Billionaire hedge fund manager went onto say he “believes the conditions are set for a powerful surge in stock prices before the bull market tops out. My guess is that I think all the ingredients are in place for some kind of a blow off. History rhymes a lot, so I would think some version of it is going to happen again. If anything, now is so much more potentially explosive than 1999.”

Amongst a few other hedge fund managers, I closely follow Paul Tudor Jones comments. There may well be significant more upside in US and international equities before the benchmarks begin to top out. I also believe there is further downside risk for the US dollar – which topped out in January this year and commenced a significant decline.

Over the past week, the US dollar has continued to wrestle with the primary uptrend – and a downside break has not yet been confirmed. I remain of the view this will likely happen and coincide with rate cuts from the Fed.

The hedge fund founder and CIO at Tudor Investment said today’s market is reminiscent of the setup leading up to the burst of the dot-com bubble in late 1999, with dramatic rallies in technology shares and heightened speculative behaviour. Mr Jones said the circular deals or vendor financing happening in the artificial intelligence space today also made him “nervous.” This is a fair point and back in 1999, leaders of the Dotcom bubble such is Cisco bought key stakes in some of its customers.

However, Mr Jones highlighted that the key difference between now and 1999 “is US fiscal and monetary policy. The Federal Reserve had just begun a new easing cycle, whereas rate hikes were on the way before the market top in 2000. The US is now running a 6% budget deficit, while in 1999, the budget had a small surplus. That fiscal monetary combination is a brew that we haven’t seen since, I guess, the postwar period, early ’50s”. Easier monetary policy potentially sets the stage for higher asset prices in my view. Every bull market ends but the question is at what stage? Opinion seems to be divided on this front. Still, Paul Tudor Jones is positioned for further upside and is not calling the top yet.

The longtime investor highlighted the tension at the heart of every late-stage bull market — the eagerness to capture outsized gains and the inevitability of a painful correction. “You have to get on and off the train pretty quick. If you just think about bull markets, the greatest price appreciations always occurs during the 12 months preceding the top. It kind of doubles whatever the annual averages, and before then, if you don’t play it, you’re missing out on the juice; if you do play it, you have to have really happy feet, because there will be a really, really bad end to it.”

Mr Jones emphasised he wasn’t predicting an immediate downturn and believes the bull market still has room to run before it reaches its final phase. “It will take a speculative frenzy for us to elevate those prices. It will take more retail buying. It’ll take more recruitment from a variety of others from long short hedge funds, from real money etc.”

Mr Jones advocates owning a combination of gold, cryptocurrencies and Nasdaq tech stocks between now and the end of the year to take advantage of the rally fuelled by the fear of missing out. We are positioned in a similar way within the Fat Prophets Global Contrarian Fund, which holds a combination of precious metals, Chinese tech and AI names, and Japanese banks (as a hedge against inflation and rising domestic Japanese rates).

Turning back to Mr Tudor Jones views on the market, other well known veteran analysts including Mr Ed Yardeni have similar observations but slightly different. Mr Yardeni said this week that “when the tech bubble in the stock market inflated during 1999, we don’t recall as much chatter about a bubble as we are hearing today. From a contrarian perspective, it is comforting that there is a bubble in bubble fears.” The fact that business media airwaves and market participants are cognisant of the 1999 bubble points to the bull cycle having further to run. Mr Yardeni noted that the Google search index for “AI bubble” rose to 100 on October 2nd versus a being at zero in mid-September.

“We are counting on another better-than-expected earnings reporting season for Q3 over the next few weeks to support the stock market’s rally to record highs. In addition, we expect that the AI and cloud companies won’t disappoint either.” I would also add that today’s expensive US tech sector valuations differ in nature with the ‘irrational exuberance’ of the tech bubble of the 1990s and 2000s where capital expenditures have been funded out of free cash flows underpinned by high profitability.

Back in 1999, companies were floated with no earnings. New equity was raised at nosebleed prices, that drove the bubble higher. But I have a sharp preference for Chinese AI and technology companies – which have much lower valuations and are still well down from record highs four years ago. Chinese equities have only recently exited a severe bear market – so I see a comparatively favourable risk/reward skew.

No sign of “bubble trouble” yet with the Hang Seng Tech Index. The HS Tech Index is still down around c40% from the 2021 prior bull market peak.

Goldman Sachs chief strategist David Kostin also said this week, that US companies are set to enjoy “a better-than-expected earnings season as a robust economy and a solid outlook for AI have left estimates looking too low”. Mr Kostin expects Mag 7 technology heavyweights to also beat expectations. Over at Morgan Stanley, CIO Michael Wilson is also among the more bullish forecasters on US earnings and sees the potential return of inflation next year “boosting pricing power and corporate profits.”

The bottom line, is that as earnings season approaches, expectations could be exceeded driving stocks higher in December. Solid earnings growth combined with expensive valuations could see the rally in US equities broaden out in the months ahead. As the seasonally weaker September/October months draw to a close, markets are about to enter seasonally the strongest period of the year. For now momentum seems to be the order of the day in equities and other asset markets.

Turning to gold, spot prices are approaching $4000oz with some warning of a major top. Gold has been among the top performing assets classes this year, as have silver and platinum. Returning to Ed Yardeni, he wrote on Monday that

gold’s record breaking rally could last through the rest of this decade, and “ultimately pushing the precious metal to $10,000oz”. I concur with Ed Yardeni that the bull market cycle in precious metals has much further to run in terms of where the US dollar is likely headed. This points to the bull cycle in PGMs have much more to run in terms of time.

Mr Yardeni’s price target implies the price of gold rising 151% over the next five years – which he believes will outperform the S&P500 where he holds a 10,000 price target underpinning a +50% increase. We saw a similar dynamic playout in the last commodity bull market when gold ran higher from $250 in 2000 to a peak above $1800 over close to 12 years.

Underpinning Yardeni’s bullish gold forecast are several factors. Economic and geopolitical forces have shaken up the status quo in recent years, “causing investors to flock to safe-haven assets like gold.” This includes the narrative around DJT’s tariffs, attempts to undermine Fed independence and lower interest rates, and China’s housing woes pushing Chinese consumers into gold.

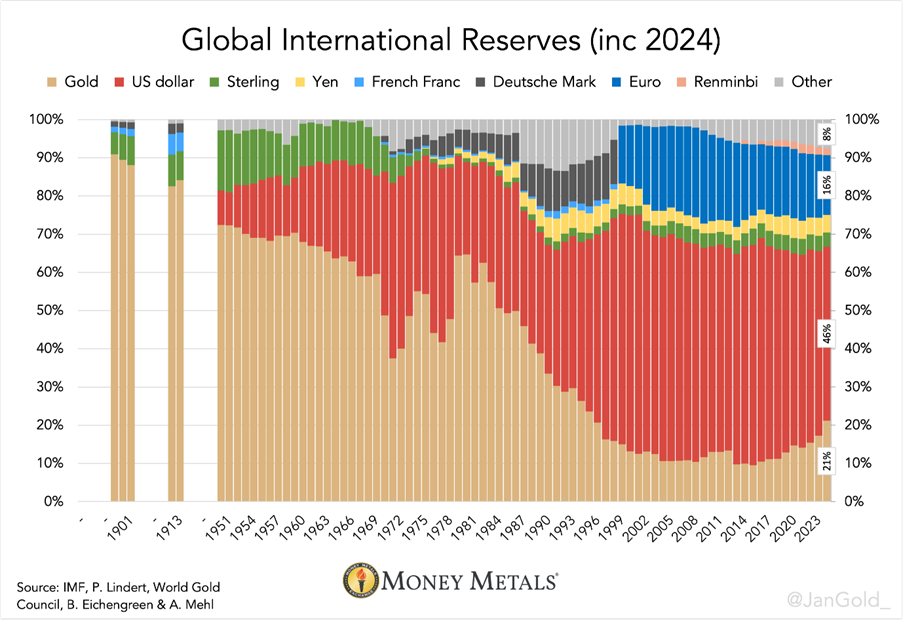

He is also an advocate of central bank buying continuing “Our bullishness is supported by the ‘Gold Put,’ provided by central banks that are increasing the percentage of their international reserves in gold. “Gold looks on track to shatter the $10,000 mark if it keeps up its current pace. So far, so good. Gold already looked to be within “shouting distance” of our year-end price target of $4,000 an ounce for 2025.”

| Source: Yardeni Research

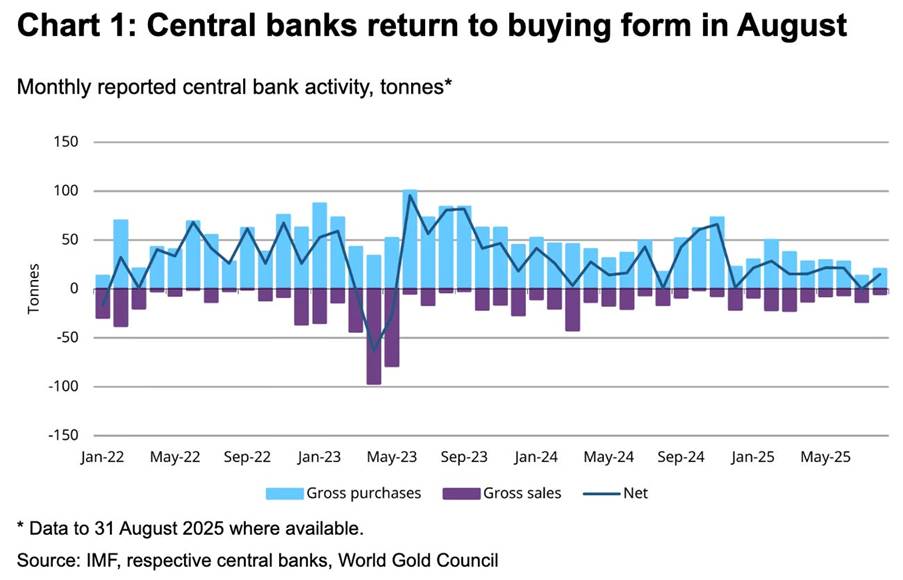

I agree with all Ed Yardeni’s points and have often expounded the same narrative. I would also add that a bear market underway in the US dollar – which has yet only really begun – could have much further to go where gold will be seen as the ultimate hedge. Central banks have been aggressive gold buyers in recent years, one of the factors supporting bullion’s latest leg up. And according to the latest update from the World Gold Council, central banks around the world added a net 15 metric tons of gold to their reserves in August. Kazakhstan, Bulgaria, and El Salvador ranked as the largest buyers that month. The key point here is that most developed economies are not buying gold yet – but this could change next year – particularly if the US dollar and the global bond market comes under renewed pressure.

|

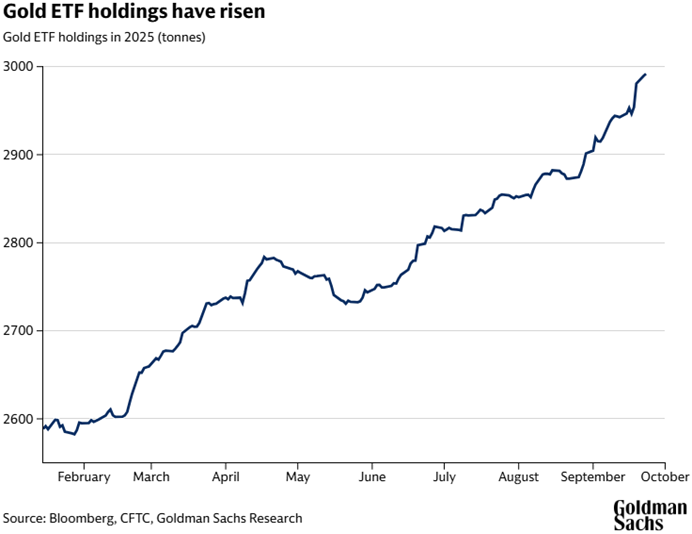

Individual and institutional investors have also shown high interest in gold as a safe haven this year, but I would expect these flows to also accelerate given still low global positioning.

Lights Out

As the bull market rolls on defying seasonal weakness in September, and so far again into October, investors seem to be complacent around the US government shutdown and the absence of official data where markets are now operating in the dark with the “lights out”. For example, the key labour market data which was due last Friday wasn’t released. With a rate cut priced at more than a 90% probability at the upcoming FOMC meeting on the 28th/29th October, this raises scope for a negative surprise to markets. Stocks and risk assets have had a strong run, and a correction if it were to arrive later this month would not be a surprise.

However, any corrective selloff should it arrive would likely prove ephemeral and transitory. Liquidity levels remain abundant and with monetary policy set to ease next year, most investors will not want to fight the Fed. The still significant cash and liquidity amassed on the sidelines likely be deployed during any market setback.

As of October 2025, the total cash and liquidity parked in US money market funds has reached a record high of approximately $7.37 trillion, continuing a strong upward trajectory over the past year.

The chart below illustrates the growth in assets from October 2024 to October 2025.

The Russell 2000 is a good benchmark to look at given the recent breakout and run to the topside which is now seeing the record highs above 2500 being tested. Resistance could intensify over coming weeks, particularly if uncertainty around the rate cut in October (that almost a near consensus now sees being delivered) begin to be priced in. This could trigger a selloff in the major benchmarks, and the Russell 2000 would likely lead on the downside back to the big support level at 2330. However, given not much is likely to get in the way of forthcoming rate cuts from the Fed later this year, I would see this as a buying opportunity.

Morgan Stanley CIO Mike Wilson said in a note this week that “our conversations with investors over the past several weeks indicate that our rolling recovery/early cycle thesis remains out of consensus.” In other words, a lot of institutional investors remain somewhat sceptical about the bull run in US stocks continuing given high valuations. Mr Wilson questioned this week whether valuations were justified? “Many of our conversations with clients have also centred around the AI capex boom, with investors asking if there are parallels to the late 1990s and if we’re toward the ending stages of a valuation bubble. We see some important differences relative to this period.”

Morgan Stanley makes a valid point, and I think there are some key differences. As Paul Tudor Jones said yesterday on CNBC, the current market feels more like 1999, before the Nasdaq surged 50% and not mid 2000 when the bubble eventually burst. As mentioned yesterday, many dotcom companies raised huge amounts of capital at very high valuations with unproven business models and little in the way of cashflow and earnings. These companies were the ones totally crunched when the bear market arrived.

Today’s boom in AI is being led by Mag 7 names which have established businesses, big balance sheets and where CAPEX is being funded out of cash flow – not capital raising. Valuations are high, but the AI boom has different characteristics. We are seeing a faster delivery of economic and efficiency gains delivered to earnings for the Mag 7 with stocks such as Microsoft, Meta and Alphabet standing out. The upcoming report season could validate this further.

Morgan Stanley also cited other factors and pointed to the “free cash flow yield for the median large cap stock is almost triple what it was in 2000. It’s also worth noting that the market multiple, when adjusted for profit margins, looks much more reasonable than it did during this period (currently trading at almost a 40% discount). Free cash flow generation, operational efficiency and strong profitability are all characteristics of a higher quality index than what we saw during the late 1990s.” This is very true.

Mike Wilson also noted that “the macro/earnings regime we believe we’re heading into in 2026 is also supportive of valuation. Perhaps most importantly, our “run it hot” thesis means that higher inflation is structural, which makes equities and gold key inflation hedges.” Equities are indeed an inflation hedge as gold is.

I have a similar view to MS and see inflation heading higher next year as the Fed cuts aggressively, but this will boost corporate profit margins in a similar fashion to what occurred post the pandemic and when huge amounts of fiscal stimulus was deployed. But this cycle could be very different given the vulnerability of the US dollar – which could fall markedly later this year when the trajectory of Fed easing becomes clearer when the government shutdown ends.

Moving on to Japanese banks, where they were left behind this week in the wake of the big rally in both the Nikkei and TOPIX post the election. The perception in markets is that bank stocks could react negatively over coming months given the incoming new PM has been an advocate (like her predecessor Shinzo Abe) of loose monetary policy. The fear is that the government will want to back away from letting the BOJ normalise monetary policy and raise the cash rate gradually (which is rocket fuel for bank earnings).

I think these fears are overblown and that Japan and the BOJ now have no choice to raises rates or risk inflation becoming out of control. Financial and bank stocks overall are should have a very strong upcoming reporting season and confirm that the sector is in great shape and generating strong earnings. I would be buying the banks on any near-term dip – should it emerge in October, and particularly if the yen were to weaken further.

While a rate hike will likely be off table in October, I don’t think this changes the narrative around rates being lifted gradually into year end and throughout 2026. This is the best setup for the banks, which will see deposit rates increase at a slower pace whilst mortgage and loan rates will adjust upwards quickly.

The upcoming reporting season in November should confirm profit growth and better shareholder returns via buybacks and dividend hikes. I would take advantage of any near term weakness (if it emerges) and accumulate the majors banks such as Sumitomo Mitsui Financial Group, Mizuho and Mitsubishi UFJ as well as some of the bigger regional players. We own many of these in our Asia and International managed account portfolios and in FPC.

Ken Griffin

Turning now to gold, Citadel founder and billionaire hedge fund manager Ken Griffin said this week that “investors are starting to view gold as a safer asset than the dollar, a development that’s “really concerning”.

“We’re seeing substantial asset inflation away from the dollar as people are looking for ways to effectively de-dollarize, or de-risk their portfolios vis-a-vis US sovereign risk. We’re definitely on a bit of a sugar high in the US economy right now.”

Billionaire hedge fund manager Paul Tudor Jones (see yesterday’s note) and Ray Dalio also made similar comments this week. Mr Dalio said that “gold is certainly more of a safe haven than the US dollar and the metal’s record-setting rally echoes the 1970s, when it surged during a time of high inflation and economic instability.”

Asked whether he agreed with the view of Citadel’s Ken Griffin that gold’s rise reflected anxiety about the US currency, Mr Dalio said that “gold is a very excellent diversifier of the portfolio. So if you were to look at just from the strategic asset allocation mix perspective, you would probably have as the optimal mix something like 15% of your portfolio in gold. I see gold as a strong store of value at a time of rising government debt burdens, geopolitical tensions, and the erosion of confidence in the stability of national currencies…gold’s resurgence mirrors the early 1970s, when it also rose in tandem with stocks.” I cant argue with any of these points – and members will know I have been a proponent of these views for some time.

Mr Dalio also said the speculation around AI has the hallmarks of a bubble and drew parallels to “past innovation booms, from the late 1920s, when patent activity and technological breakthroughs fuelled speculative excess, to the dot-com era of late 1990s.” The AI boom does have similar factors in common with other bubbles, but there are some differences as well. And while all booms eventually end with a bear cycle, I am leaning into what Paul Tudor Jones said yesterday, that the AI run could go on for some time.

Mr Dalio said he continues to see opportunities to seize on the benefits of AI, either through companies that will use it to produce large efficiencies or those who will provide platforms for the technology – but “I would be wary of betting against the megacap tech companies despite his reservations about valuations. I wouldn’t want to be short the super-scalers.”

Meanwhile, Goldman Sachs raised on Monday its December 2026 gold price forecast to $4,900 per ounce from $4,300, citing “strong Western exchange-traded fund (ETF) inflows and likely central bank buying. We see the risks to our upgraded gold price forecast as still skewed to the upside on net, because private sector diversification into the relatively small gold market may boost ETF holdings above our rates-implied estimate.” I have been making the point that accelerating demand from retail and institutional investors would emerge this year and add to the bull run in spot prices. This is now playing out.

Goldman expects central bank buying to average 80 metric tons in 2025 and 70 tons in 2026, saying emerging market central banks are likely to continue the structural diversification of their reserves into gold. Western ETF holdings are expected to rise as the US Federal Reserve is seen lowering the funds rate by 100 bps by mid-2026. In contrast, noisier speculative positioning has remained broadly stable. Following the large September increase, the level of Western ETF holdings has now fully caught up with our US rates-implied estimate, suggesting the recent ETF strength is not an overshoot.”

Meanwhile, China’s central bank added gold to its reserves in September for the eleventh straight month, official data from the People’s Bank of China (PBOC) showed on Tuesday. China’s gold reserves rose to 74 million ounces at the end of September. The PBOC gold reserves were valued at $283.29 billion at the end of last month, up from $253.84 billion at the end of August – which is still low as percentage of total reserves compared to many other central banks. There is plenty of scope for the PBOC to continue buying – which I believe they will – along with other central banks.

In May 2024, the PBOC halted its 18-month-long gold purchasing spree. However, the central bank resumed its gold buying six months later in November 2024, and I think they will continue into next year – particularly if the US dollar heads lower later this year – which is our base case. Finally, the World Gold Council said this week that central banks around the world expect gold holdings as a proportion of their reserves to increase over the next five years, while expecting their dollar reserves to be lower.

The first innings

With gold above $4000oz (and A$6,100oz in Australia) debate in the business media is running high about the sustainability of the rally. I believe that a risk off correction if it ensure, would see all asset markets selloff including gold. However, I don’t envision the end of gold’s bull market anytime soon. We might only really be in the “first innings”. One interesting observation is that for all the hype around artificial intelligence and big the surge in chip stocks this year, gold miners have actually been the better performer this year. Gold, PGMs and the actual miners actually outperforming the gains in mega-cap tech for the first time in a while.

While it is clear that rising participation amongst retail and institutional investors is behind the rally, on average most portfolios have little or know exposure. This points to rising demand and the reallocation trade continuing for some time. But near term bullishness around precious metals – and AI – points to a correction arriving at some point that will check the advance. As one investment strategist commented in the AFR yesterday “gold and gold miners are one of my most bullish medium thematic calls. Gold has safe haven appeal, while gold miners are also set to benefit from margin expansion and valuation re-rating.” This is true, but increasing bullish commentary such as this also points to “overbought conditions” so I would not be surprised of a corrective pullback in coming weeks.

Gold has surged more than 45% this year, touching a series of new all-time highs and on track for the best year since 1979. Even the big bull market in commodities during 2000 to 2011 did not see gold notch up a gain of this magnitude. But unlike back during the cycle, central bank buying has been behind the rally this year with increasing participation from retail and institutional investors. The expected rate cuts, undermining of Fed independence, and a growing trend of de-dollarization has also differentiated the rally this year.

I am more relaxed in terms of the actual miners themselves. Valuations are less stretched than during the 2000-2011 bull run for the precious metals sector and also relative to technology shares. The MSCI gold miner index trades at around 13X forward earnings estimates, slightly below the average for the last five years. In contrast, the chip index is at a lofty 29 times, well above the five-year average. If gold stays near record territory, the cash-flows and profits for the PGM sector could surprise on the upside with elevated margins. In Australia, the reporting season for the sector could be spectacular given spot prices are now above A$6,100 in local currency. For this reason, I am prepared to weather a correction and see pending dollar weakness as being the next catalyst for gold

Behind the rally has been a growing aversion to large reserve currencies, notably the US dollar, but others such as the euro in recent weeks where France is likely to get into a lot of fiscal trouble given the political upheaval and backlash to any form of fiscal austerity measures. This trend is likely to go on. Investors are coming to the conclusion that many fiat currencies are problematic and not a long term, stable store of value. So there are deep fundamental drives behind the rally in gold this year – similar to what we saw in the 1970s.

One strategist, Eurizon, noted this week that “the rally has been driven by a common factor. Reserve currency issuers at central banks have been printing money like mad, pushing investors to look for alternatives. If the reserve managers continue to divest from not just the dollar but all fiat monies, gold could continue to march higher. If central banks’ gold holdings match those of dollars, all else being equal, gold could reach $8,500. Why not?” While I agree with these sentiments, this might also point to a near term top approaching which could coincide with a risk off move. However, I was wrong about a correction materialising in September and could be equally wrong in October.

Also this week, some high profile and world leading hedge fund managers have talked up golds prospects. This week we heard from Paul Tudor Jones advocating gold and bitcoin. Ray Dalio recently referred to gold as “certainly more of a haven than the greenback, while Citadel founder Ken Griffin said the bullion’s rise reflected something troubling about the US dollar.

Meanwhile gold is set to become Australia’s second-biggest export, overtaking coal and LNG. Revenues from gold mining will jump to $60 billion in the FY through to June 26 up from $47 billion last year according the Department of Industry, Science and Resources. Luckily for Australia, the surge in gold will partially offset expected revenue declines in other commodities. I am more of an optimist on commodities and where they are headed over the medium to longer term including iron ore).

Australia is well positioned to benefit from the bull run in gold, being one of the world’s leading producers. Output is projected to rise from 340 tons in 2025/26, to 369 tons the following year.

Turning to the broader equity markets, JP Morgan strategists have become more cautious on the US and developed market, but more bullish on emerging markets or “EMs”. The strategists argued back in July that “Chinese equities in particular appeared interesting. We are encouraged that Chinese stocks, especially A shares, are up meaningfully over the past months. We expect better emerging market performance this year on a likely peak in trade headwinds vs China, on potentially stronger emerging market currencies [and a weaker dollar] central banks easing and given increasing China policy support.”

The bank noted that “this comes after years of very weak relative EM equity performance, which coincided with USD strength. EM look cheap and under-owned, while EM central banks are set to ease policy. Within EM, we continue to be bullish on China Tech. I have a similar view which was emphasised last year. However, the magnitude of the rally in China tech surprised me given the rapid pivot to AI. This also caught out a lot of global macro investors who still remain underweight, which points to the rally continuing for some time.

JP Morgan also said this week that valuation divergence remains extreme between the US and international markets. I have pointed this out many times this year, with US total market cap now around 70% of the global total. This is high by any standard, especially considering US GDP only accounts for 28%. JPM concluded that “the potential resumption of the rotation into International markets, post the last 6 months pause, could work even if US were to see stagflation fears materialize. To be clear, there is not likely to be any decoupling, and Eurozone was typically a high beta on the way down, but International markets might not underperform, as would historically be the case, in the event of renewed market volatility. This is because USD might not trade as a safe haven, which would typically be seen during derisking.”

This is a fair point and given the valuation differential (and improving growth prospects) I still see international equities being a relative safe harbour vs the US. In the case of China/Hong Kong and tech stocks, the risk/reward skew is also more favourable than US counterparts, with valuations significant lower and the growth runway is possibly just as good.

JPM strategists said this week that “China’s housing slowdown was one of the drivers of our long-held cautious view on Chinese activity. However, we believe that we may be close to an inflection point. To be clear, we are not expecting Chinese activity to ramp up to levels seen pre-Covid, but, in our view, any stabilization will go a long way towards getting investors comfortable with owning the region again.” I have also been of the view this scenario of an inflection in the property market could soon playout, which would provide a major boost to commodities, copper and the mining industry generally.

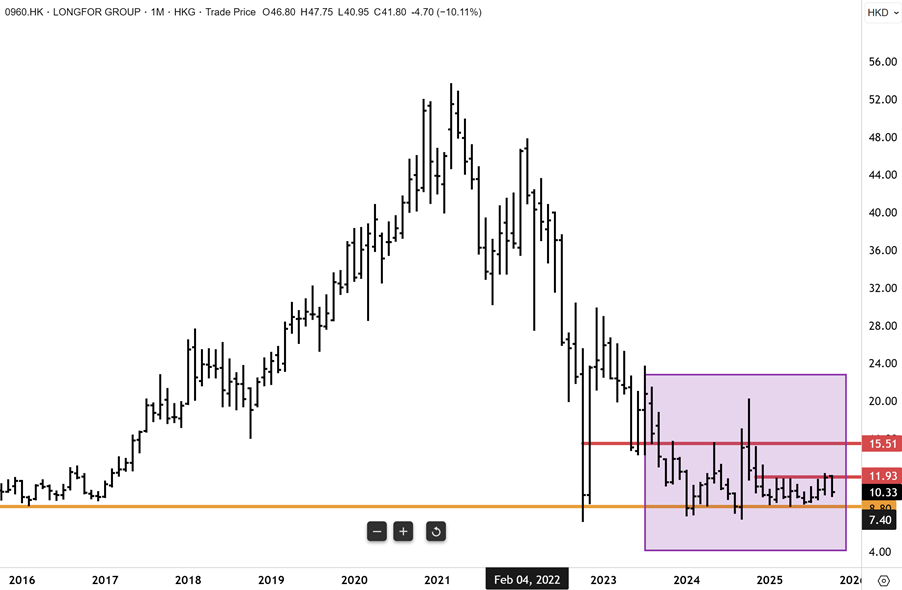

One stock I am keeping a close eye on is Longfor, one of the last major Chinese property developers still standing in relatively quite robust health. An inflection point in the shares could soon be approaching…

Carpe Diem

Sign up to receive full reports for

the best stocks in 2025!

Where to Invest in 2025?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.