- Oil surged, the US-Iran ceasefire was declared ‘over,’ and the Strait is back in play. Yet, the DXY barely moved, and the VIX yawned. Angus’s read on what the non-reaction means for the second half is in The Verdict.

- Samsung beat lofty expectations this week, and its stock fell, prompting a global slide for peers. That’s the signal the rotation trade has been waiting for. The chipmakers enter earnings on the highest bar in the room. We name what picks up the baton – including an exposure trading at about half the S&P 500’s multiple.

- One major commodity is correcting toward strong support, and the structural case for record highs by year-end has never been cleaner. Goldman put the demand numbers on the table this week. A major Australian miner’s pullback is the entry.

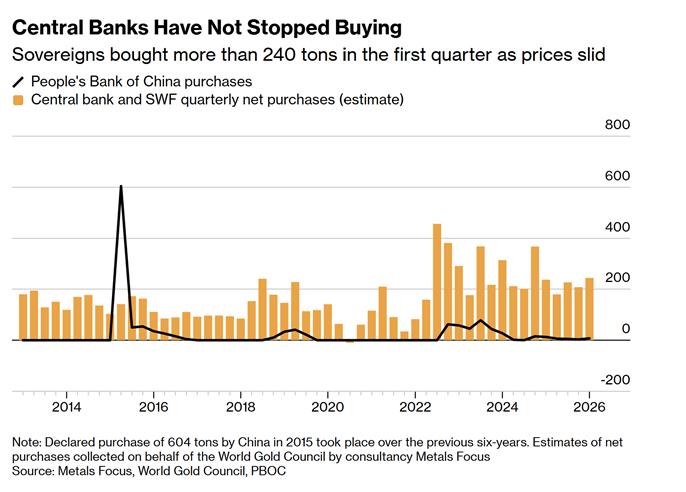

- Bloomberg declared a three-year bull market over this week. We take the other side. One country’s central bank bought for a twentieth consecutive month in June – its largest single purchase since October 2023. The metal held above a key level all week.

- A live bidding war broke out on the ASX this week for a gold miner. Two suitors – one with more complementary assets, one with A$1.2bn cash and no debt. The rational move is to wait. We break it down in the Spotlight.

The fatLITE is the weekly read. Membership is the position.

The Verdict

The most important thing the market did this week was refuse to trade the war. Across the week, the tape was handed a case for a dramatic risk-off repricing. The US revoked Iran’s oil export waiver after fresh tanker attacks in the Strait of Hormuz; the US President declared the ceasefire over from a NATO summit in Turkey; and by Thursday, the two sides had exchanged a second day of strikes. Crude rallied hard early in the week, before fading by Thursday. The US 10-year yield climbed back to near the ‘danger zone’ of 4.6%. Gold was sold and tested the $4,000/oz handle, before recovering modestly. Many ingredients for a dollar bid and a volatility spike were present.

None of it stuck. By Thursday’s close, WTI had given most of the move back to $71.80, the 10-year had eased to 4.55%, and gold had recovered to $4,130/oz. The S&P 500 finished at 7,543, six points above where it began the week. European, Chinese and Japanese stocks had solid sessions on Thursday. An exception was Australia, which endured a slow grind down, though the hurt was contained. Two instruments that typically would have registered the fear more markedly did not. At the time of writing, the dollar index sat at 100.9 against Monday’s 100.8, and the VIX stood at a sedate 15.8.

To trade international shares, you can open an account with our partner CMC Markets, which provides access to 15 global markets. If you join today, you can also receive $300 in free brokerage for domestic trades.

The week’s real signal was what did not move rather than what did. A reopened conflict that the dollar and the volatility surface opt not to price is a market that has recategorised the Strait from regime risk to background noise. The market reaction has faded with each iteration of this conflict, which is what should happen once the incentives are clear. With the November midterms approaching, Washington wants cheap oil, and Tehran wants the export revenue that only an open Strait delivers, so each flare-up is bound in terms of the market risk. Accordingly, the market didn’t blink and spent the week looking past the headlines toward the catalyst that will set direction as the second half gets underway – the June-quarter earnings season, which we expect to broaden solid earnings growth well beyond the chipmakers.

The Calls

Our dominant read coming out of the week is that the greenback has become the master variable, and that the dollar would not rally on this week’s setup is one of the most informative pieces on the board. The bear case for risk assets is straightforward and widely held – higher oil revives inflation, higher inflation keeps the Fed hawkish, a hawkish Fed supports the dollar, and a firm dollar pressures gold, commodities and the offshore earnings of the US multinationals. The links in that chain were tested this week. The dollar index effectively went nowhere meaningful across four sessions, and the futures market’s lone remaining Fed hike has now been pushed out to December, beyond the midterms. Our position is that it is far from certain the Fed will tighten at all and that the case rests almost entirely on the oil path, with oil already well below its highs.

Another conviction we have is the rotation, and it has strengthened. The chipmakers have carried the S&P 500 to double-digit gains this year, but the rate of change in their upward earnings revisions could have peaked, and they enter the reporting season on a high bar. One need only look at Samsung, which reported stellar numbers earlier in the week, blowing past market expectations, only for the stock to fall sharply and drag down peers across the region.

Beneath that surface, expectations for the old economy remain subdued. The airlines and transports, the US homebuilders, the regional banks and healthcare have all lagged, and it is those sectors, together with the beaten-down Mag 7 hyperscalers now trading on their cheapest relative valuations in over a decade, that we think broaden the rally into year-end. Morgan Stanley, Goldman Sachs and JPMorgan have each moved the same way, arguing for capital to rotate from chips back toward the hyperscalers and for the rally to widen in the second half. Here, among the choices we like, are the US homebuilder proxy James Hardie and the Chinese hyperscalers, where Alibaba and Tencent trade at a far steeper discount than their US peers.

The week’s third conviction is copper, and it is one we would be adding to amid the weakness. Goldman set out the structural case cleanly: copper demand is shifting from cyclical to strategic, with grid and power infrastructure alone driving more than 60% of demand growth to 2030, alongside defence, electric vehicles, renewables and data centres, and with Western grid investment increasingly treated as a matter of national security. The supply side cannot answer quickly, because mines are getting deeper and grades are lower. A new greenfield project can take fifteen to twenty years from approval to the first commercial pour.

It will likely take a much higher copper price before a supply response is elicited and fresh capital is committed to new greenfield mines. In our view, copper needs to surmount at least $8 a pound to spur a meaningful supply-side response.

Copper has risen within a consistent uptrend since mid-2025. Whilst the correction is continuing from the record highs above $6.60, we believe support is well defined at $6 and below. The technical setup for copper remains constructive, and we anticipate upward momentum to resume in the coming months and the record highs to be retested by year’s end. The latest bout of weakness in major copper producers such as BHP, therefore, opens up a buying opportunity in my view.

Turning to precious metals, gold is at another technical crossroads. The correction that commenced at the record highs is still underway, but downside momentum looks to have dissipated in recent weeks. On the hourly three-month chart below, gold has not been able to break out above the downtrend. Since May, this downtrend has been quite consistent.

The durability of the bull market came under direct attack. A widely read report from Bloomberg declared the three-year run over, pointing to roughly $18 billion of ETF outflows since the January peak near $5,600. We think that mistakes the marginal buyer. Retail and ETF flows have unwound the crowded positioning of February, which is healthy, but the structural bid is official, not private. China’s central bank extended its buying to a twentieth consecutive month in June with its largest single addition since October 2023. Meanwhile, a record share of the central banks surveyed by the World Gold Council intend to add over the coming year.

Against that backdrop, the metal held above $4,000 all week and traced a series of higher reaction lows, rallying into Thursday’s risk-on tape rather than breaking with it. A topside break of the corrective downtrend would confirm the inflection, and it would most likely coincide with the dollar weakness we expect in the second half. Goldman holds a $4,900 year-end target; ours is $5,000.

The Local

The ASX 200 spent the week grinding lower in an orderly fashion, closing at 8,762.5 for a loss of about 0.8% across four consecutive down sessions before a decent recovery began playing out on Friday, with a circa +0.55% gain at the time of writing (midday AEST). The local market was tracking the global story, rather than major stories at home.

More broadly, we expect the materials sector to be a key driver helping the benchmark index move higher over H2. Our copper call lands on BHP, where the pullback is, in our view, an opportunity to accumulate rather than a reason for caution. Rio Tinto fell after Morgan Stanley cut its target to $149 on aluminium concerns, a level now beneath the market price. However, we would note that Rio’s own capital is increasingly pointed at copper, and expect it to stay disciplined on any M&A after its August result. Sandfire Resources and Capstone Copper are high-beta pure-play expressions.

The iShares China Large-Cap ETF (ASX) has pulled back year-to-date, but the investment case has strengthened, not weakened, through the correction. IZZ’s underlying basket – weighted to state banks, platform internet, and consumer champions – now trades at around 10.65x forward earnings, roughly half the S&P 500 multiple, into consensus profit growth of 14–15% for MSCI China, with technology nearer 20%. Two structural forces are compounding: Chinese technology firms have demonstrated they can compete at the AI frontier at a fraction of US capital intensity, and Beijing’s anti-involution campaign is engineering margin recovery across key industries. Global active funds remain structurally underweight China.

Report Spotlight

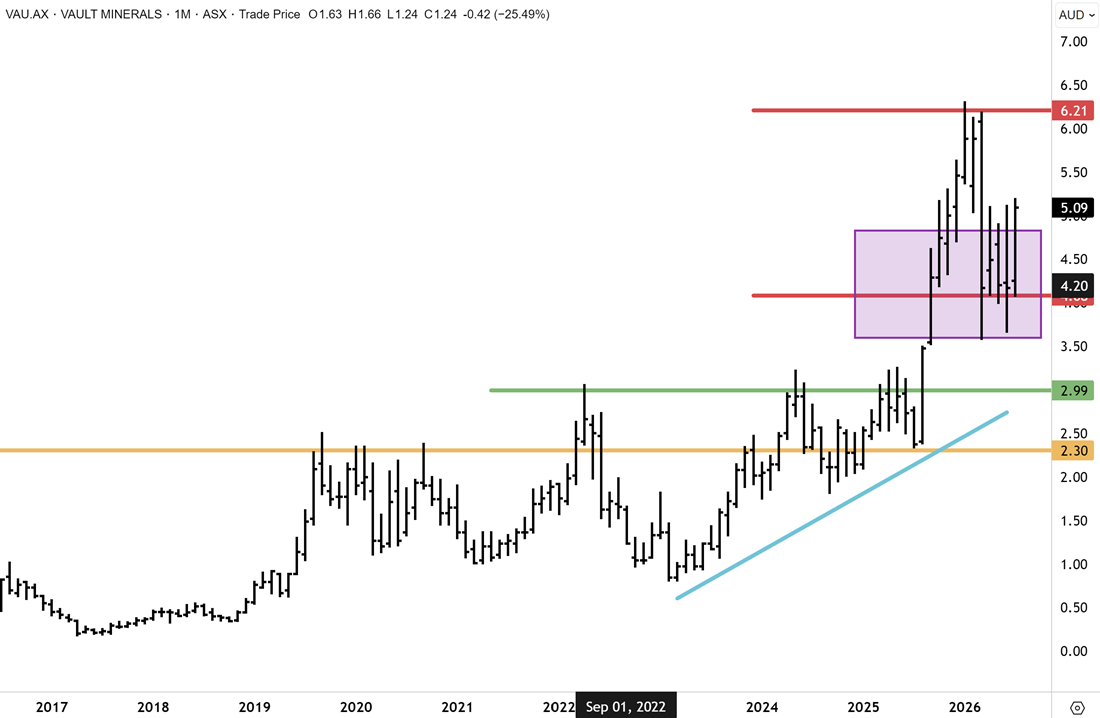

Vault Minerals (ASX:VAU) – HOLD

Vault Minerals shareholders are sitting in the middle of a live bidding contest, and the rational move is to wait. Genesis Minerals gatecrashed the agreed Regis Resources scheme on 6 July with a rival offer – cash plus scrip – that Vault’s board immediately deemed superior. The premium is relatively slim, and because both bids contain scrip at the core, it moves daily. The more interesting question is whether Regis responds: it holds A$1.21bn in cash and bullion, carries no debt, and has a strategic imperative to compete. Genesis holds the stronger asset-combination hand through the King of the Hills proximity synergies; Regis holds the balance sheet to force another round. We maintain our Hold on VAU.

On the technical picture, since our last update, Vault has dynamically rebounded off key support to retest resistance above $5.10. We had conviction several months ago that Vault would not break below this support, which has played out. Our base case remains that upward momentum resumes in spot gold once the US dollar turns lower, which is our base case with oil prices now receding and removing inflationary pressure on the bond market. With the latest takeover for Vault, we expect risk appetite to continue making a return for Australian gold miners, and that upward momentum will continue this year.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Have a great weekend.

Carpe Diem

Angus