- Payrolls landed at 57,000 jobs against a consensus near 110,000, the dollar rolled back, and year-end hike odds fell from two-in-three to a coin toss. Why we’d spent the week arguing that the hawk the market feared was made of paper.

- Goldman, Morgan Stanley and JPMorgan all cut their oil forecasts to around US$80 inside a single week. Our read is still more bearish, and there’s one level in crude that decides where the bond market goes from here.

- Copper corrected to support near US$6.10 as the dollar rallied, while the AI power build-out that underwrites the demand case didn’t move an inch. Where that leaves the metal, and the miners levered to it.

- 82% of central banks now hold physical gold, up from 71% a year ago, and the Aussie gold miners rallied more than +7% on Friday. Where our year-end gold number sits against UBS and Goldman.

- National home values fell -0.4% in June, the steepest drop since December 2022, and the major banks took a hit before turning higher on Thursday. Why the crowd may have the Australian banks wrong.

- Report Spotlight: a major ASX resources name has just agreed to sell a business line for up to US$5.6bn, flagged a fully franked special dividend, and jumped nearly 10% as it rebuilds itself around copper. Where we stand.

The fatLITE is the weekly read. Membership is the position.

A question hovered over the market, and on Thursday, a closely watched data point provided valuable clues. For weeks, the market had been deciding what to make of Kevin Warsh, and it had settled on hawk. A new Fed chair guarding his credibility, a dollar breaking higher, the yen at a level last seen in 1986, and the emerging-market complex handing back a year of gains. What the market never checked was what the hawk was made of.

We spent the week arguing that this was a correction inside a dollar-down regime rather than the start of a tighter one, because the machinery underneath it, cheaper oil and cooling inflation, was pulling the other way. Thursday’s payroll data settled the argument in our favour. The economy added 57,000 jobs against a consensus of near 110,000, and the response was immediate. The dollar rolled back below 101, the short end of the bond market rallied, gold jumped 2%, and the odds of a year-end hike fell from roughly two-in-three to a coin toss.

The Calls

We see Warsh as more of a paper hawk. Thursday’s payroll works in our favour. Our base case remains that the Fed does not raise before the midterm elections and that the risks to inflation keep receding. The recent stronger dollar has weighed heavily on a range of risk assets, including precious metals, copper, commodities and emerging markets, but this has all the hallmarks of a correction in my view. Meanwhile, the US dollar index has risen, but the advance looks sluggish and might soon run out of puff, despite the recent breakout.

If the dollar is the market’s current headline, oil is the mechanism that can rewrite it. Crude fell to a four-month low this week as transit through the Strait recovered toward three-quarters of its pre-war rate, and the market’s anxiety flipped from too little supply to too much. The move was fast enough that many of the sell-side capitulated on forecasts inside a single week. Goldman Sachs cut its fourth-quarter Brent call to US$80 from US$90 and its 2027 average to US$75, Morgan Stanley trimmed to US$80 through 2027, and JPMorgan moved to US$80 in the fourth quarter and an average of US$64 next year.

Our read is more bearish still. With the US and Russia pumping at record rates, Saudi Arabia exporting record volumes and Kuwait lifting its force majeure, and demand structurally leaking to electric vehicles, US$64 may prove optimistic rather than aggressive, and regional production could be back at pre-conflict levels by December rather than early 2027.

This matters for what it does to the rate path. Cheaper energy is the deflationary force that removed the last justification for the hikes the market had priced, and it did as much as the payrolls print to turn the week. We are watching how crude holds. A break below US$68 feeds directly into the bond markets, where the hawkish case still rests, while resistance above US$80 now looks firm enough to cap any bounce.

Copper remains a conviction call for us and faced crosscurrents. The metal has recently taken a hit from the dollar and will keep taking its short-term direction from the currency. However, what does not turn on the dollar is the demand case. The physical build-out behind artificial intelligence and the power infrastructure it requires is a multi-year source of demand that a month of dollar strength does not touch, and supply remains genuinely tight. JPMorgan’s path toward US$15,000 a tonne on the LME rests on exactly that combination, and we agree with it.

Gold is the dollar trade viewed from another angle. On Wednesday, the yellow metal rose while the dollar rose, breaking a six-week mirror image. On Thursday, the soft payrolls sent it 2% higher, and the Australian gold miners rallied with it – the gold sub-sector on the Australian bourse had rallied by more than +7% on Friday, around midday.

The crowded February positioning has washed out, and the metal was heavily oversold. Official flow is steady, with this week’s OMFIF survey finding 82% of central banks now hold physical gold, up from 71% a year ago. On price targets, we keep our house view distinct from the investment banks. UBS sees US$5,200 over twelve months and Goldman US$4,900 by December, while our base case is a move back toward US$5,000 by year-end.

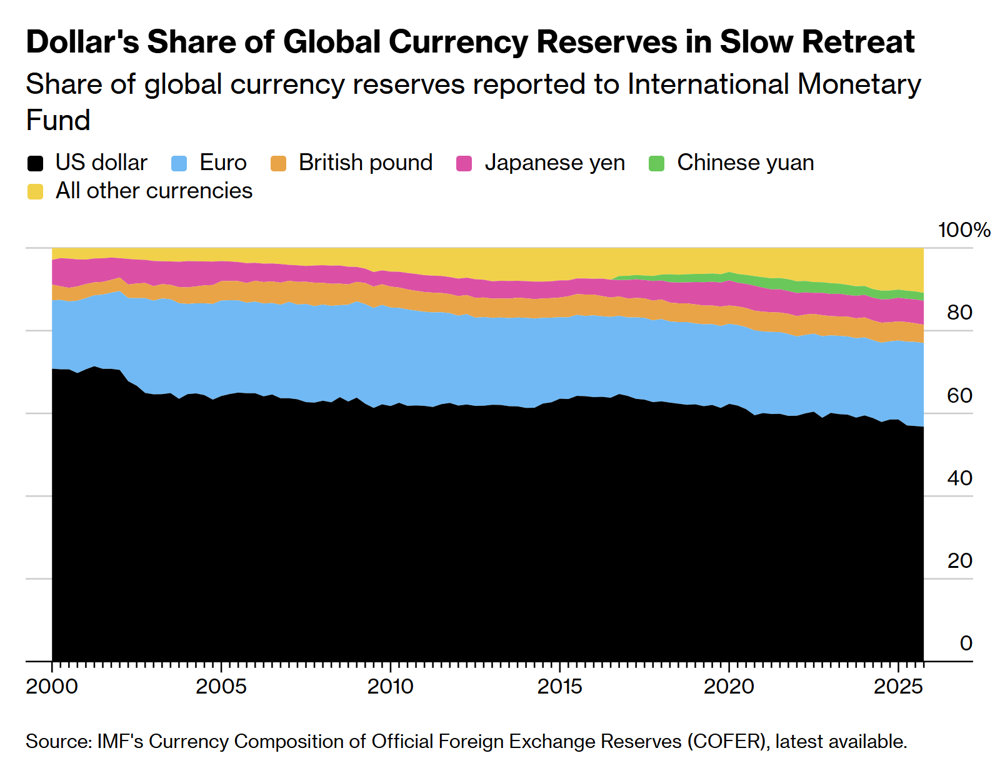

Meanwhile, the yen sits near a four-decade low, with a US administration that has always wanted a cheaper dollar. The precedent worth recalling is the 1985 Plaza Accord, when the United States, Japan, West Germany, France and the United Kingdom agreed to drive an overvalued dollar down together, and the dollar then lost close to half its value within a year.

To trade international shares, you can open an account with our partner CMC Markets, which provides access to 15 global markets. If you join today, you can also receive $300 in free brokerage for domestic trades.

Japan’s FX currency chief suggested this week that intervention was an effective strategy and flagged close communication between Tokyo and Washington over foreign exchange as the yen hovers near a four-decade low. I think a far more likely outcome is that the Bank of Japan might soon be forced to hike rates again. A theme we have conviction in is the Japanese banks, prime beneficiaries of an orderly normalisation in rates.

The RBA held at 4.35% in June, and the minutes from the central bank released this week confirm the board is in wait-and-see mode. Two risks dominated the discussion. The Middle East conflict and what the minutes called “persistently weak productivity growth.” Conditions are “probably somewhat restrictive,” CBA’s Belinda Allen sees “minimal indication” of an imminent move, and markets were pricing roughly 50/50 odds of one more 25bp hike by year-end.

The labour market is the real swing factor. April’s jobs data was soft beneath the surface, and our view is that unemployment could push through 5% over the next year as SMEs cut headcount and AI starts eating into labour demand.

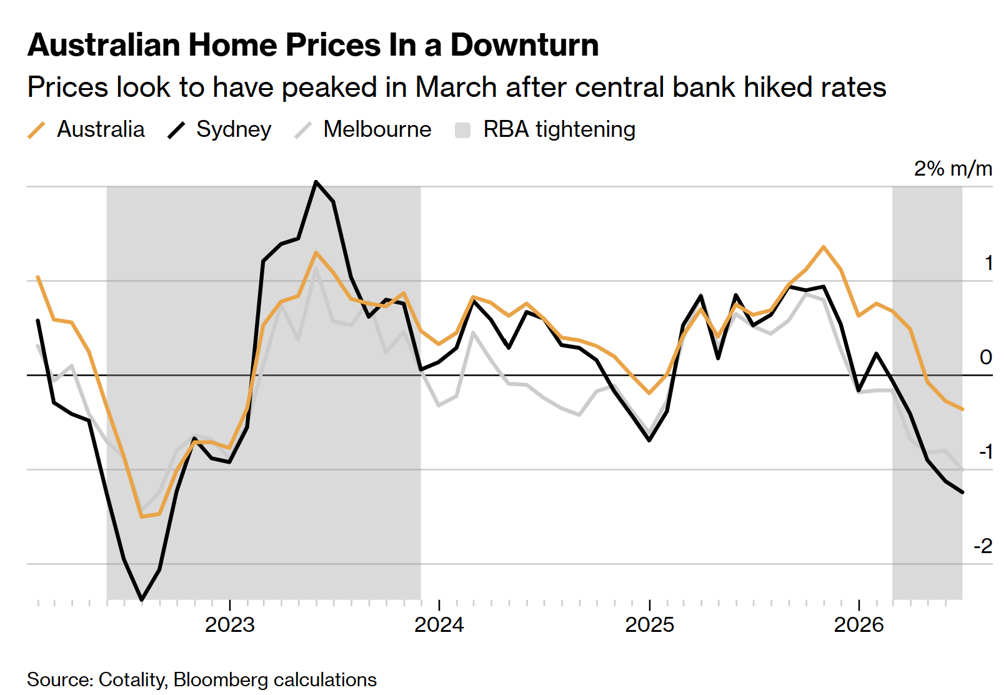

Housing data landed hard this week. National home values fell 0.4% in June, the biggest monthly drop since December 2022. Sydney dropped 1.2%, Melbourne 1%, while Perth (+0.7%) and Darwin (+1.4%) bucked the trend.

New Labor legislation curtailing negative gearing and abolishing the CGT discount has hit auction clearance rates hard, and buyers will demand bigger discounts to clear current stock. With over half the country holding residential property, falling prices mean a wealth-effect hit to spending, not just a headline for renters finally catching a break.

Despite the gloom, we still see the ASX200 above 9,000 by December, with resources doing the heavy lifting. The Resources index should retest 2007-breakout highs near 8,375, with support at 7,300 and 6,400.

In our view, the bottom line is that the RBA is underestimating how much housing-driven wealth destruction could slow the economy, and rising unemployment, not sticky inflation, is shaping up as next year’s real policy problem.

The big banks were also topical this week in the Australian market. They took a hit after the housing data hit the tapes. However, they were back on the ascent on Thursday, as a broker upgrade to NAB anchored a strong session for financials. I was interviewed on the Australian business streaming channel Ausbiz this week and said the resources sector would help the ASX200 surmount 9,000 this year. I also mentioned that I am not bearish on the banks over the medium to longer term, despite significant headwinds from the budget and cancellation of negative gearing.

The funds management industry is running a record short position on the Australian banks, which might lead one day to a significant short-covering rally. National political expectations around the durability of the budget policies being sustained over the long term might soon reverse. Not only is there precedent for a reinstatement of negative gearing under the Hawke Government in the 1980s, but it’s been part of the Australian economy that extends back to the 1930s.

Banking on a recovery

A break below key support at 12,300 would add to the bearish narrative around the Australian banks and bring on a deeper correction within the sector. However, the stock market looks ahead to where financial conditions will be in six to twelve months. Should support levels hold, and upward momentum resume, many bearish investors and analysts on the Australian banking sector could soon be scratching their heads.

Report Spotlight

South32 (ASX: S32) – HOLD

South32 has agreed to sell most of its aluminium value chain to Alcoa for up to US$5.6 billion, including US$3.1 billion in cash, US$1.0 billion in Alcoa shares and US$750 million in assumed debt, while shifting ~US$1.2 billion of rehabilitation liabilities to the buyer. Shares jumped 9-10% on the announcement.

The strategic rationale is clear: on completion, roughly 85% of pro forma group EBITDA will come from base and precious metals, positioning South32 squarely behind electrification, infrastructure and decarbonisation demand. Annual overheads are expected to fall by ~US$125 million as the portfolio simplifies.

Growth capital is already being redeployed. South32 approved a US$725 million expansion of Sierra Gorda in Chile, lifting processing capacity by 25% and copper equivalent production to ~30% from FY2030-31. Shareholders benefit directly: a US$500 million fully franked special dividend has been flagged, with further returns to be considered post completion.

Completion is targeted for the second half of 2027, pending multi-jurisdiction regulatory approval, meaning execution and commodity price risk remain live for some time yet.

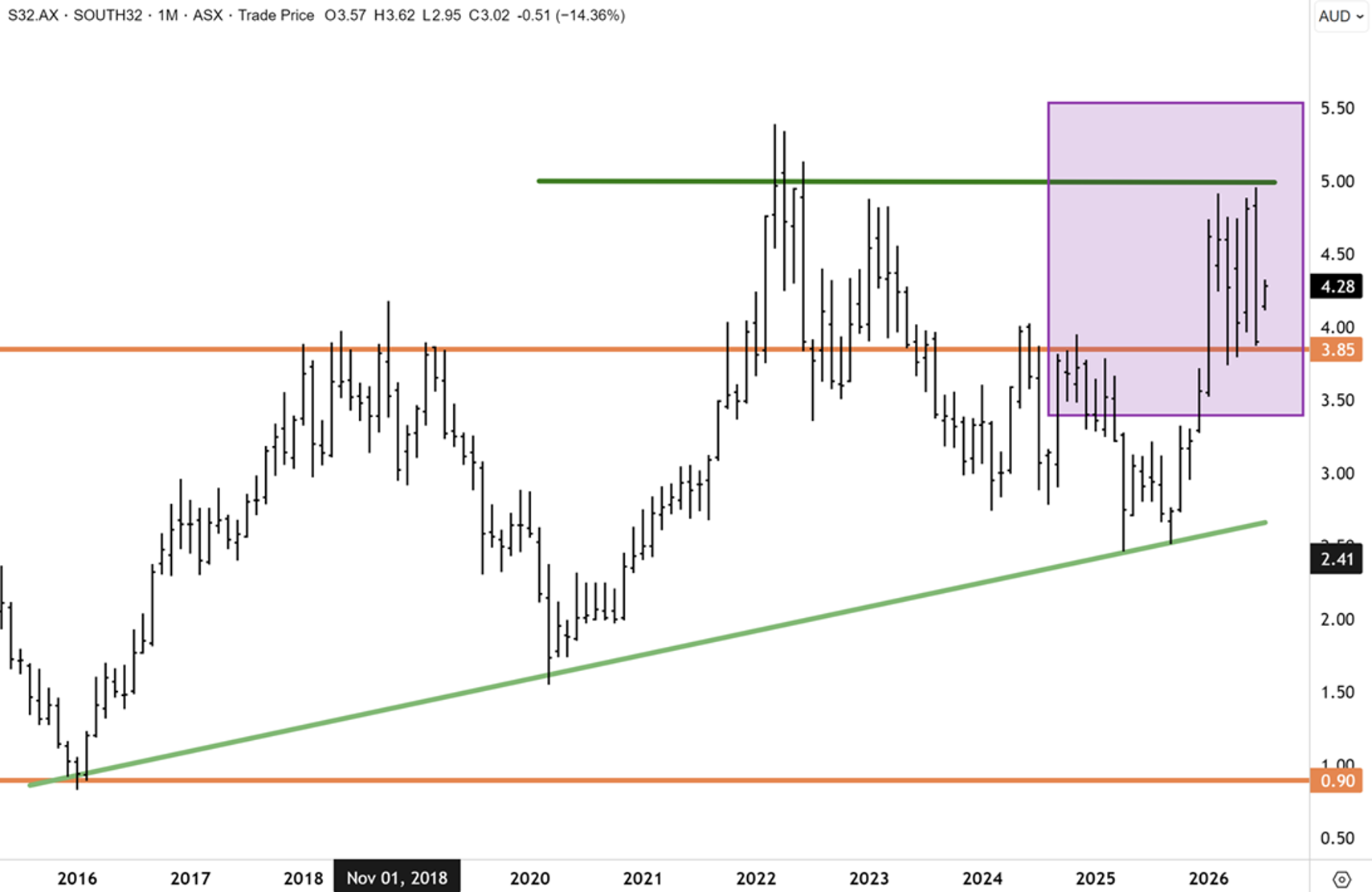

South32 has, since our last update, staged a decent upward dynamic off key support at $3.85 to close yesterday at $4.32. Whilst South32 remains rangebound below the four-year highs, we believe it is only a matter of time before the stock advances above overhead resistance at $4.80/$4.90 and, in time, establishes new record highs. We maintain a bullish outlook for commodities and base metals, where S32 is well-positioned across a range of base metals, and we will now have a more committed focus on copper.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Have a great weekend.

Carpe Diem

Angus