- Is BHP the world’s biggest AI infrastructure trade? JP Morgan’s copper demand model has an answer that reframes how you think about the stock. It’s not the number you’d expect.

- Australia’s biggest iron ore producers are asking the government for help. CMRG now controls approximately 70% of China’s inbound iron ore purchasing power. The man who blocked the BHP-Rio merger in 2010 says he’d think differently today.

- Sydney home values are down 2.1% from their peak. Melbourne is down 3.2%. The RBA just lifted rates again, the budget changed the investor calculus, and Morgan Stanley has a forecast that hasn’t made the headlines yet.

- Gold jumped 1% on Thursday the moment oil dropped. The mechanism that the Strait has been suppressing reversed in real time. JP Morgan’s year-end target hasn’t moved.

Report Spotlight: Collins Foods (ASX: CKF) – Eight new KFC restaurants in Bavaria, closed this week. Already earnings accretive. The full report has the technical setup and what we think happens next.

This FatLITE covers the headlines. The full research – complete macro analysis, buy recommendations, and model portfolio positioning – is available to members. We’ve been an independent investment research provider for 25 years. If you’re not yet a member, find out what’s included – and why we back it with a 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

The Verdict

Nothing broke in the markets this week. For fourteen weeks, the bond market has absorbed a closed Strait with what Angus calls “significant patience” as Fed hike odds climbed from 9.1% to 41.8% in a month. Gold held above the $4,400 structural floor. Copper ran to a Comex record. A software breakout and a semiconductor surge ran independently of the geopolitics.

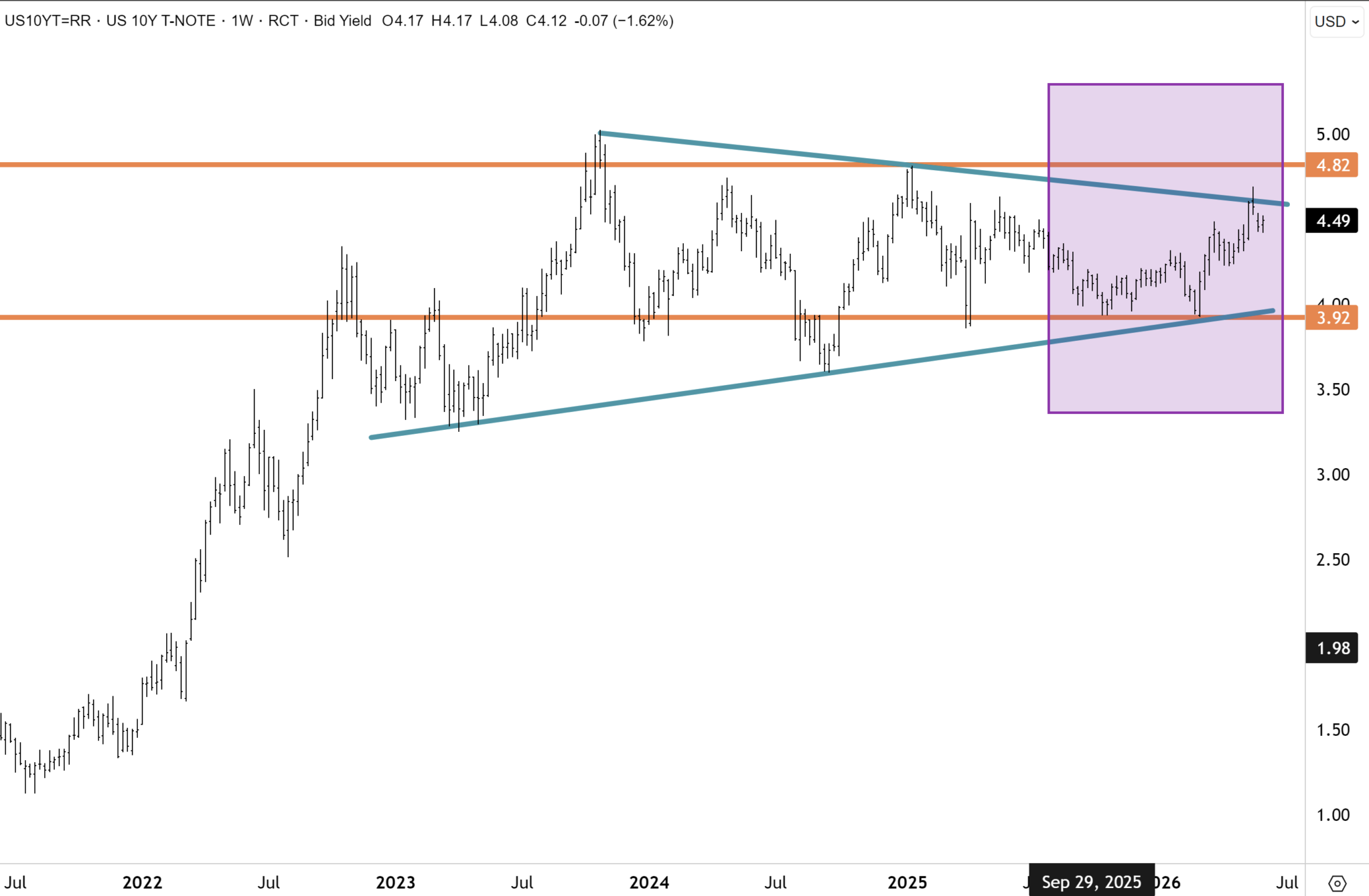

The long end of the US yield curve has demonstrated significant patience around inflation and elevated oil prices. However, comfort levels and pain thresholds in the bond market will get increasingly stretched the longer the Strait remains closed.

Thursday brought the first release. A US-mediated Israel-Lebanon agreement (though rejected by Hezbollah) sent oil down nearly 3%. The dollar eased, the 10-year dropped to 4.47%, and gold rose 1% to $4,509. The equity tape continued to broaden. The Dow surged 1.73% to a record. Healthcare and financials led. The Russell 2000 added 1.5%. NYSE advancers beat decliners at nearly 2:1 as investors rotated from technology positions into more neglected sectors. The Strait is still shut. The ultimate deal the market is waiting for is not yet signed. The string is still drawn. Pressure on the US to find a resolution continues to intensify as time to the midterms narrows. That is the week’s verdict.

To trade international shares, you can open an account with our partner CMC Markets, which provides access to 15 global markets. If you join today, you can also receive $300 in free brokerage for domestic trades.

Gold: the first confirmation. Gold has been biding its time since the February record at $5,600, moving sideways in a $4,470 to $4,520 range recently, while the inverse correlation with oil and the dollar suppressed conviction. The mechanism is that the Strait closure pushed oil higher, which pushed the dollar higher, which weighed on gold. Thursday, with ceasefire progress sending oil down nearly 3%, that relationship reversed. Gold rose 1% to $4,509 as the dollar eased to 99.44. The 200-day moving average near $4,400 remains the structural floor; a downside break would see risk capped near $4,100, a level we view as a worst-case scenario.

JP Morgan’s commodity strategists this week characterised the gold trade. The bull market is pausing, not reversing. The structural drivers – dollar debasement, US fiscal risks, geopolitical tensions – remain intact, but investor conviction in the near-term trajectory of gold is fragile while the Strait remains closed and energy-driven inflation keeps the Fed repricing risk intact. The bank’s base case is that a Hormuz reopening, which JP Morgan continues to assume in June, begins unwinding the USD and real yield strength that has been capping gold and pushes prices toward the $4,900 to $5,100 technical resistance band. Despite a near-term demand downgrade, JP Morgan’s year-end target holds at $6,000 per ounce as demand re-accelerates in the second half.

Angus concurs with the overall thesis/direction. The correction from $5,600 is well advanced. A $5,000 price is readily achievable by year-end on a resolution, and a retest of the record highs follows within twelve months.

Plenty was happening in the local sector, as famed activist investor Elliott Management acquired at least a A$1bn position in Northern Star and pushed for changes. St Barbara, debt-free with $504 million in quarterly cash and key support at 55 cents holding, targets a 90-cent retest on the resumption of the uptrend – both were amongst the research team’s coverage this week. On platinum, JP Morgan notes deficits persist with China-related tightness risks and targets $2,400 per ounce toward year-end alongside gold’s renewed rally. We like platinum for similar reasons and recommend exposures across our different research products (Impala Platinum and the ASX-listedGlobal X Physical Platinum Structured ETF).

Copper and BHP: the AI infrastructure trade, made physical. Copper printed a Comex record of $6.67 on Wednesday as LME copper traded above US$14,000 a tonne. Profit-taking pulled it to $6.54 by Thursday, but left the week’s most important analytical question on the table. The question came from JP Morgan: Is BHP a data centre AI play? JP Morgan’s case rests on the earnings composition. Copper now constitutes 54% of BHP’s FY26 EBIT. BHP has re-rated 42% year-to-date against the ASX 200’s 1% gain and, as JP Morgan notes, that re-rating has occurred without iron ore moving materially, with the metal down 4% on the year and copper itself only modestly higher at 13%. The bank concludes that the BHP move is being driven by sector rotation and by global investors playing the AI and data-centre thematic through the world’s largest copper producer. On the forward demand picture, JP Morgan estimates data-centre copper demand growth in 2026 at approximately 470,000 tonnes, rising to around one million tonnes annually by 2030. That annual growth increment, the bank notes, is roughly equal in size to BHP’s Escondida mine, the world’s largest copper operation, added to global demand every single year.

We have long had a bullish call on BHP, Rio Tinto and the pure play copper producers. New greenfield mines take 15 to 20 years from discovery to production. The market will be constrained for decades, we think copper is heading into a $7 to $8 per pound range, and BHP at current valuations remains undemanding relative to pure AI technology plays. A price of $100 per share is plausible within the super-cycle.

Copper has entered a supercycle that might endure for five to ten years. The scope is open on the long-dated chart for upside extension, and it is only a matter of time in my view before copper enters a new range between $7 and $8 a pound.

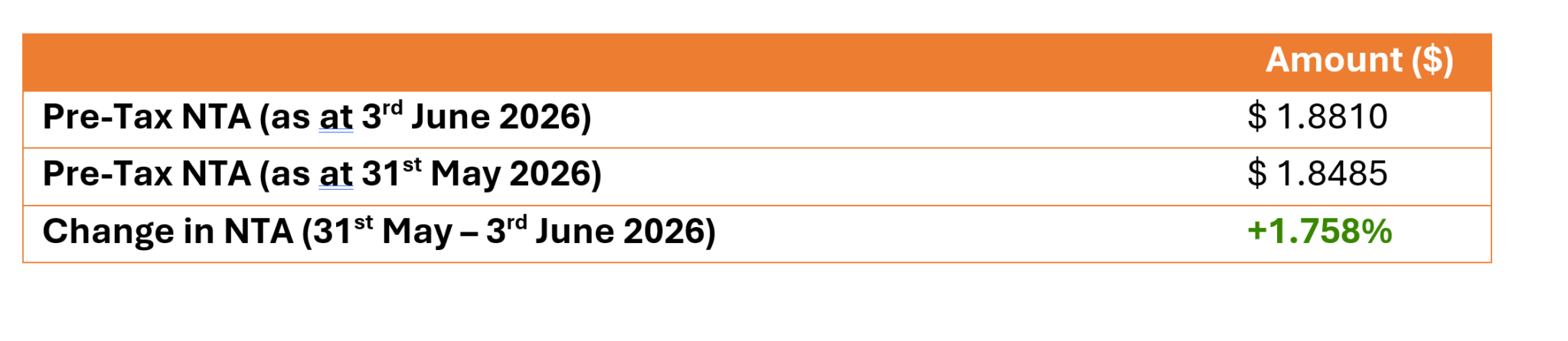

Finally, the Fat Prophets Global Contrarian Fund (ASX: FPC) provided an update to the ASX on Friday morning (5 June). Estimated pre-tax NTA improved nearly 1.8% to just over $1.88. The Fund’s rights issue concluded this week, and we were encouraged by the response. Thank you to all shareholders who participated. We appreciate the support. There was a modest shortfall, which is still available on the same terms as shareholders applied for the new shares, which come with an attaching free option. Please reach out today to patrick.ganley@fatprophets.com.aufor more information.

The Local

The week’s most significant domestic story was structural, not price. Australia’s largest iron ore producers formally called on the Albanese government to help counter China Mineral Resources Group, which now controls approximately 70% of China’s inbound iron ore purchasing power. Graeme Samuel, who blocked BHP and Rio Tinto’s proposed iron ore merger in 2010, told the AFR that cooperation between the two majors would be “more acceptable today” given the international pressures. The ground has shifted.

The bear case against the big miners centres on Simandou: Guinea’s mine is now running at approximately 70% of template capacity and dispatched 2.2 million tonnes in May, which pushed iron ore to $101.50, a two-month low. Rio Tinto’s iron ore chief Matt Holcz addressed this directly at the Perth mining summit. The price has held above US$100 for seven consecutive years. The market needs to replace approximately 800 million tonnes of production over the next decade as older mines exhaust. Simandou at full capacity represents just one-sixth of that replacement, and the two ore grades serve different customers and co-exist. Meanwhile, UBS calculates that China’s apartment inventory overhang has already declined from a peak above four million units to approximately one million, and that the remainder clears within one to two years. A new residential construction cycle follows, and it is steel-intensive. We continue to be very bullish on BHP and Rio Tinto, with huge cash flows from iron ore funding expansion in other metals, like copper. Accordingly, the weakness on Thursday and at the time of writing on Friday (about midday) in the iron ore names is an opportunity for patient investors.

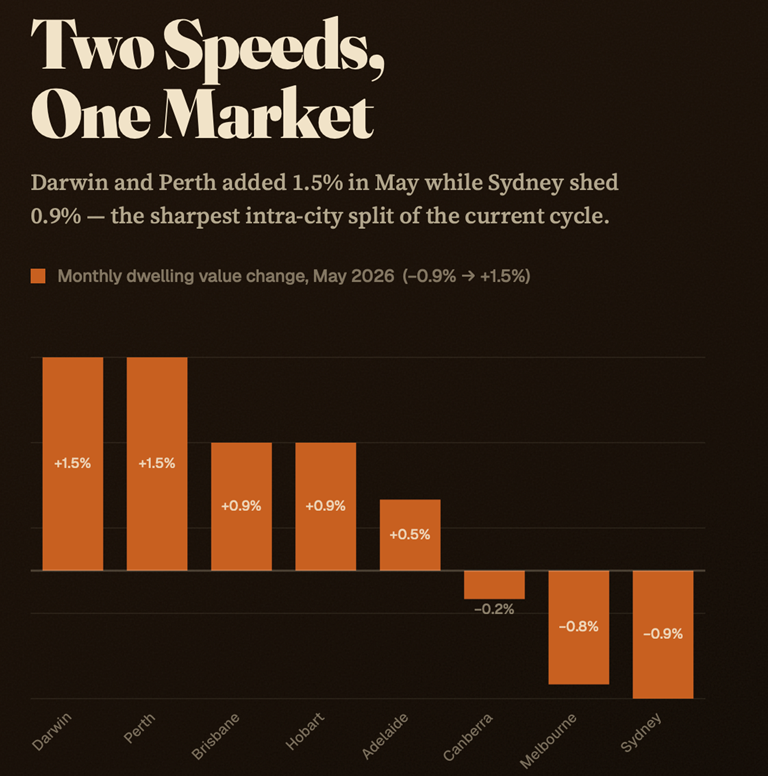

Turning to the Australian housing sector, it’s only been a few weeks since the budget, and the market is already slowing down. Cotality’s May Home Value Index landed flat at the national level, but underneath, cracks in the cycle are widening. Sydney fell 0.9% and Melbourne 0.8% in May. Sydney now sits 2.1% below its November 2025 peak; Melbourne is 3.2% below a peak dating back to March 2022. The ACT joined them, down 0.2%. However, other capitals are still rising. Perth and Darwin led at 1.5%, Brisbane and Hobart added 0.9%, while Adelaide rose 0.5%.

But the pace is slowing everywhere. Even the regional bid ( +0.6% combined) printed its smallest monthly gain in a year. The five-year split tells the wider story. Perth values are up 91.4% since May 2021. Melbourne is up just 3.3%. The macro is squeezing from both sides. The RBA lifted the cash rate 25bp to 4.35% in May, citing sticky inflation and oil-price uncertainty. Headline CPI eased to 4.2%, but trimmed mean ticked up to 3.4%. Borrowing capacity has been shaved at the moment that buyer sentiment is sagging.

Then there’s the Budget and the changes to negative gearing and CGT. Existing property holdings are grandfathered, but the marginal-investor calculus has changed hugely. I wrote recently about a grim forecast from Morgan Stanley, warning that these changes could spur a 10% decline in home values, which, if it eventuated, would be the sharpest decline in four decades. The bottom line is that the budget has sharpened a downturn that was at the early stages. Sydney and Melbourne are leading. The rest of the country is on a delay timer. Expect softer mortgage volume growth at the Big Four (CBA, WBC, NAB, ANZ), but no major stress on the lending books. Residential developers with new-build and build-to-rent exposure, Mirvac (MGR) and Stockland (SGP), are relative beneficiaries. We are keeping a sharp eye on employment.

Collins Foods (ASX: CKF) – BUY

Collins Foods has closed its acquisition of eight KFC restaurants in Bavaria for €31.1 million, lifting the German network by ~50% to 25 restaurants across three states. The timing matters: these stores are already generating higher margins than the existing German estate, making this immediately earnings accretive rather than a speculative build. The strategic logic is compelling. Bavaria, centred on Munich, is one of Germany’s wealthiest and most densely populated regions. Combined with existing territories, Collins Foods now operates across three states, representing more than half of Germany’s population and ~54% of the national GDP. Yet Germany has just one KFC per 1.8 million people, a fraction of McDonald’s penetration, pointing to a long runway ahead. Yum! Brands has explicitly backed the transaction and expanded Collins Foods’ development agreements, signalling confidence in the company as a credible long-term growth partner in continental Europe. Full-year profit guidance of mid-to-high teens growth remains intact.

Despite the correction this year, Collins Foods has managed to hold above the primary uptrend in place now for a decade. Downside momentum is constructively dissipating. We hold conviction that CKF is close to resuming upward momentum with the stock oversold. Our base case remains in place for Collins to soon rebound and retest the next resistance cluster near $10. The next catalyst for the stock is the upcoming profit result due to be released in a few weeks. Support remains well defined at the primary uptrend, which now intersects around $7.85. We are confident that upward momentum will resume this year, and still believe it is plausible for the record highs to be retested within 18 months.

Everything in this fatLITE is the surface. The full reports, macro commentary, model portfolio, and buy recommendations are members-only. Try it with our 30-day money-back guarantee.

Join today with our EOFY Offer – 50% Off All Memberships – Apply code FP50% at checkout.

Have a great weekend.

Carpe Diem

Angus