KEY CONTENT

- One of the most successful macro investors of the past forty years outlined this market on Thursday. His reference point: October-November 1999. His runway call: two more years.

- Australia’s March trade balance swung to a deficit this week for the first time since 2017. The reason wasn’t economic weakness. Capital goods imports surged on a wave of data centre investment – the AI thesis is now hitting the official national accounts.

- This week, Paul Tudor Jones, Ed Yardeni, and Morgan Stanley’s equity strategist landed independently on the same structural conclusion. That kind of convergence is rare. What each one is seeing, and what it means for positioning, is in The Calls.

- Iron ore held at elevated levels this week while China’s property sector continued to contract. That divergence has a specific explanation – and it reframes the commodity super-cycle thesis against the consensus view.

REPORT SPOTLIGHT

- Capstone Copper (ASX: CSC & Toronto: CS) – BUY

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join on our Products page.

The Middle East was the interference. The underlying was already running.

What resolved this week was not the bull case – that was already running. What was resolved was the interference. Ten weeks of Middle East escalation, ceasefire speculation, and energy-price pressure waves had been playing over the top of two structural cycles that never actually paused. An AI super-cycle that Paul Tudor Jones this week benchmarked to October 1999, with “another two years to run,” and a commodity super-cycle now underpinned not by China’s construction demand but by the global abandonment of just-in-time inventory as a viable supply chain model. The S&P 500 hit a fresh record at 7,365 on Wednesday before a healthy Thursday consolidation; Japan’s Nikkei blazed to a new all-time high above 63,000 on its first session back from the Golden Week holiday; the ASX held most of its week’s gains into Friday. Three of the most credible macro voices in markets – PTJ, Ed Yardeni, and Mike Wilson – aligned on the same structural call this week.

Futures pointed to a softer Friday open regionally. The “boy who cried wolf” dynamic – the consistent flux between war and peace signals – produces regular moments of renewed anxiety.

The underlying bid held and accelerated. The two largest asset-class moves of the week – oil down, commodities ex-energy up – are telling the same story from opposite directions.

The risk with any week that ends with markets near record highs and a geopolitical crisis apparently resolving is that the narrative captures the resolution rather than what was underneath it. The Middle East conflict did not create the bull case for US equities, commodities, and international markets – the bull case was there before the first shot was fired in the Strait. What the conflict did was play over the top of it, loud enough that most participants couldn’t hear the underlying. This week, the volume came down.

The most consequential input of the week came not from markets but from Paul Tudor Jones. In our view, one of the three finest macro investors of his generation, PTJ, outlined the current cycle by reference to the productivity miracles that have historically defined extended bull markets: the early-PC revolution that lifted Microsoft and Apple in the 1980s, and internet commercialisation in the early 1990s.

He drew the direct line to now: “The debut of Claude AI could be thought of as analogous to Microsoft’s release of its Windows operating system, which eventually allowed the internet to be used for commercial purposes.” His verdict on where that places us: “If you look at multiples and earnings, we’re kind of where we were in October-November of 1999. We’ve got another two years to run.”

The Convergence

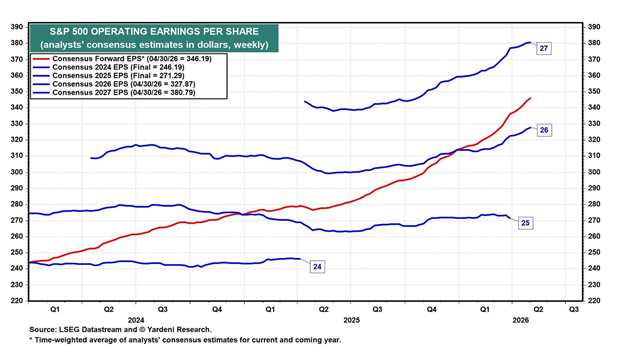

That framing triangulates with Ed Yardeni’s Buzz Lightyear Theory – AI as the fourth factor of production, where land, labour, and capital are all scarce but data is not – and with Morgan Stanley’s Mike Wilson, who this week confirmed the Q1 earnings beat rate as the strongest in four years, with median S&P 500 EPS growth running at 16% against expectations of roughly half that. Three highly-rated macro voices in global markets aligned on the same structural call this week, independently, with the same conclusion. That convergence is the editorial centre of gravity for this week’s edition.

Ed Yardeni said, “The stock market balloon is climbing higher, and the burners are firing. It isn’t all hot air that is lifting stock prices. It’s also earnings revisions, which are increasing for 2026 and 2027.” Over 80% of S&P 500 companies that reported through May 1st exceeded profit estimates, with the index tracking aggregate Q1 earnings growth of 28% year-on-year – double the 14% expected at the start of April.

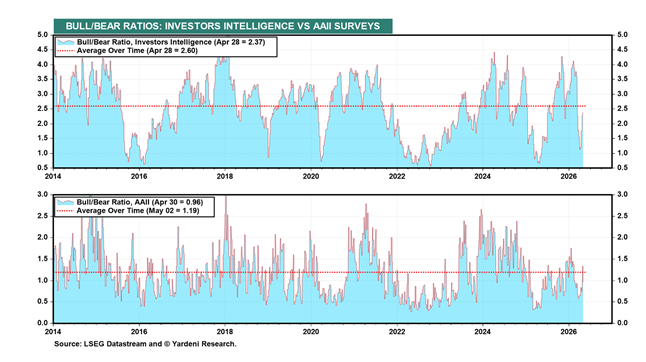

The bull/bear ratio has recovered from March’s depressed readings but remains “rising-but-still-below-average,” which Yardeni has described as exactly the profile of a bull market with room to run.

The Fed parallel is also worth noting: if incoming Chair Kevin Warsh holds rates steady in the face of rising inflation – as the Fed did too long in 1999 – PTJ believes “more fuel could be added to the market rally.” Futures are pricing no Fed move this year.

Within equities, the AI capex names confirmed the structural thesis mid-week. AMD surged 17% to a record high on data centre chip demand, Corning gained 14% on a new Nvidia partnership for AI optical connectivity, and Datadog jumped 30% on a raised full-year forecast with positive read-across to CrowdStrike and Palo Alto Networks.

The real-economy confirmation was hard to ignore. Australia’s March trade balance swung to a $1.84 billion deficit, the first since December 2017, on capital goods spending up 36.8% on a wave of data centre investment. The AI cycle is in the balance of payments. And the same week, PTJ called two more years of AI-fuelled gains, a conference of the top 50 US computer scientists found that 60% now believe AI could wipe out half of mankind in 20-30 years – up from 10% last year – with 80% now supporting regulation, up from 20%. PTJ: “We need to do it tomorrow. We’re already late.” Regulation is coming, but it will shape how the cycle matures, not stop it.

The Second Cycle

The second structural cycle running alongside the AI thesis is less widely discussed but equally durable. I believe one outcome from the ME conflict is that a spotlight has been squarely placed on global supply line disruption, which will underpin the importance for nations to carry strategic stockpiles of essential materials and resources. The ‘just in time’ inventory model of the past several decades now carries a big question mark.

Copper is the central case. Comex copper looks to be in the early stage of breaking out above recent highs, and once confirmed, there are good prospects for copper to retest the record high at $6.50 in the coming months. This bodes well for the copper miners. We added copper mining exposure to our portfolios this week.

Other base metals are also stirring. Nickel also looks to be on the cusp of an important upside reversal, as is true for many of the other base metals.

Iron ore, holding above $110 against consensus expectations of weakness, is approaching the $111/112 level where a sustained break would confirm the resumption of upward momentum.

Gold is consolidating its new higher range. China’s central bank bought for the eighteenth straight month in April. China’s gold reserves added over 300,000oz to 74.64 million ounces by the end of April. The nation’s gold reserves now stand at $344.17 billion, and April saw a return to gold buying after a pause in March. Gold continues to consolidate and establish a new, higher range, and I see the upward trend resuming later this year, with spot prices likely to hurdle well above US$5000/oz.

The DB Invesco Agriculture fund (DBA) is on the cusp of breaking out to new record highs. Our commodities supercycle thesis is firmly intact.

The Middle East situation has followed an arc that we have called with conviction. The domestic US political imperative is clear – gasoline above $4.50 per gallon for the first time since July 2022, midterms six months out, an upcoming DJT-Xi summit – and the economic imperative on both sides to reopen the Strait only grows with time. JPMorgan said: “On a 3/6/12-month timeframe, one should continue using dips to add into.”

The Fat Prophets Global Contrarian Fund (ASX: FPC) added Capstone Copper this week as “one of the best stocks to get exposure to our secular bull market thesis on copper metal prices, which could continue for many years,” along with GDS Holdings (Chinese AI data centre infrastructure) and Futu Holdings (Chinese fintech). BT Group and Grab were also added to; Meta was sold; Microsoft is retained as undervalued. The portfolio is positioned directly behind both structural cycles running simultaneously.Another avenue is through our international and Asia managed account portfolios, which also have little in the way of direct exposure to Australia (reach out to patrick.ganley@fatprophets.com.au today for more information).

The ASX Read

The March trade balance swung to a $1.84 billion deficit – Australia’s first since December 2017 – on capital goods spending up 36.8% on a wave of data centre investment. The implication for portfolio construction is direct: the most powerful investment cycle running in global markets is being captured by Australian investors as buyers, not as producers. We made the case early in the week: “There is no question that the Australian economy is going to do it tougher this year, given potential future rate hikes and taxation reform, which arguably will come at the worst possible time.” Against the accumulated headwinds of an RBA now explicitly “restrictive” and a Federal Budget arriving Tuesday with CGT and negative gearing reform, diversification from Australian-only positioning has moved from prudent to necessary.

Within the ASX, the right framework remains the barbell of banks and resources, with the weight placed firmly away from discretionary retailers. Banks are increasingly a cost-out story – AI-driven labour reduction at the large institutions is accelerating, confirmed by all three half-year results this week. Resources carry global linkages that insulate them from the domestic rate cycle, deepened further by the strategic stockpiling thesis. For other domestic holdings, QBE and Suncorp carry entrenched pricing power through the rate environment; Telstra’s earnings are resilient against consumer pressure; and WiseTech and Xero have, in all probability, bottomed after their extended selloff.

We remain of the view that with resources and commodities in a super cycle (with a similar setup to 2000 and 2008), copper prices are set to make new record highs, and iron ore/energy remaining resilient, the ASX200 will retest the all-time highs later this year. A domestic recession (if it unfolds) would not necessarily change this narrative. Australia’s resources and mining sector has global linkages, and the banks are increasingly a cost-out story. Major Australian technology stocks could also provide support for the ASX200, given that these businesses have defensive moats with global customers, plenty of pricing power and are now screening very cheap on valuation.

Governor Bullock’s warning this week – “it doesn’t take much additional spending to make the job of returning inflation to target more challenging” – sets the frame for Tuesday’s Federal Budget – we will be watching. The full portfolio argument reads clearly against that backdrop. The barbell for the Australian-facing half, international diversification for the themes running offshore.

Capstone Copper (ASX: CSC & Toronto: CS) – BUY

Capstone delivered 1Q26 adjusted EBITDA of US$329 million, up 83% year-on-year, on ~48,000 tonnes of production — achieved despite a 35-day strike at Mantoverde cutting roughly 5,000 tonnes of output. Strip out the disruption, and the underlying performance is even more impressive. EBITDA margins expanded to ~50%, up from ~38% in late 2024, driven by record copper prices of US$5.92/lb and strong by-product credits from gold and silver. Critically, full-year production guidance is unchanged. The growth pipeline is advancing in parallel. Copper fundamentals remain tight: grid investment, data centres, EVs and constrained new supply all point in the same direction.

Following our last technical update, Capstone Copper has fallen to a low near $9.60, which we believe will prove enduring. The stock has since rebounded, tracing out a higher low near $11. We believe upward momentum is now returning for the copper miner following the sharp correction from record highs above $18. We believe CSC has become oversold, and a technical buying opportunity has now opened. We maintain a bullish medium to longer-term outlook for copper prices, which will underpin CSC shares.

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join on our Products page.

Have a great weekend.

Carpe Diem

Angus