Geopolitics and economic data faded into the background on Thursday as investors focused on fundamentals as the earnings season gets underway. Wall Street bounced back following a two-day slide after an outstanding profit result from Taiwan Semiconductor Manufacturing (TSM) reignited a rally in the chip sector. Solid results from Morgan Stanley and Goldman Sachs also boosted sentiment as the US reporting season gets underway.

The big event of the week, with potentially massive implications, was the Federal Reserve and Chair Jerome Powell being served grand jury subpoenas from the Justice Department, threatening a criminal indictment. In a forceful written and video statement released Sunday, Mr Powell said the action was related to his June congressional testimony on ongoing renovations of the Fed’s headquarters, but warned that independence was being compromised.

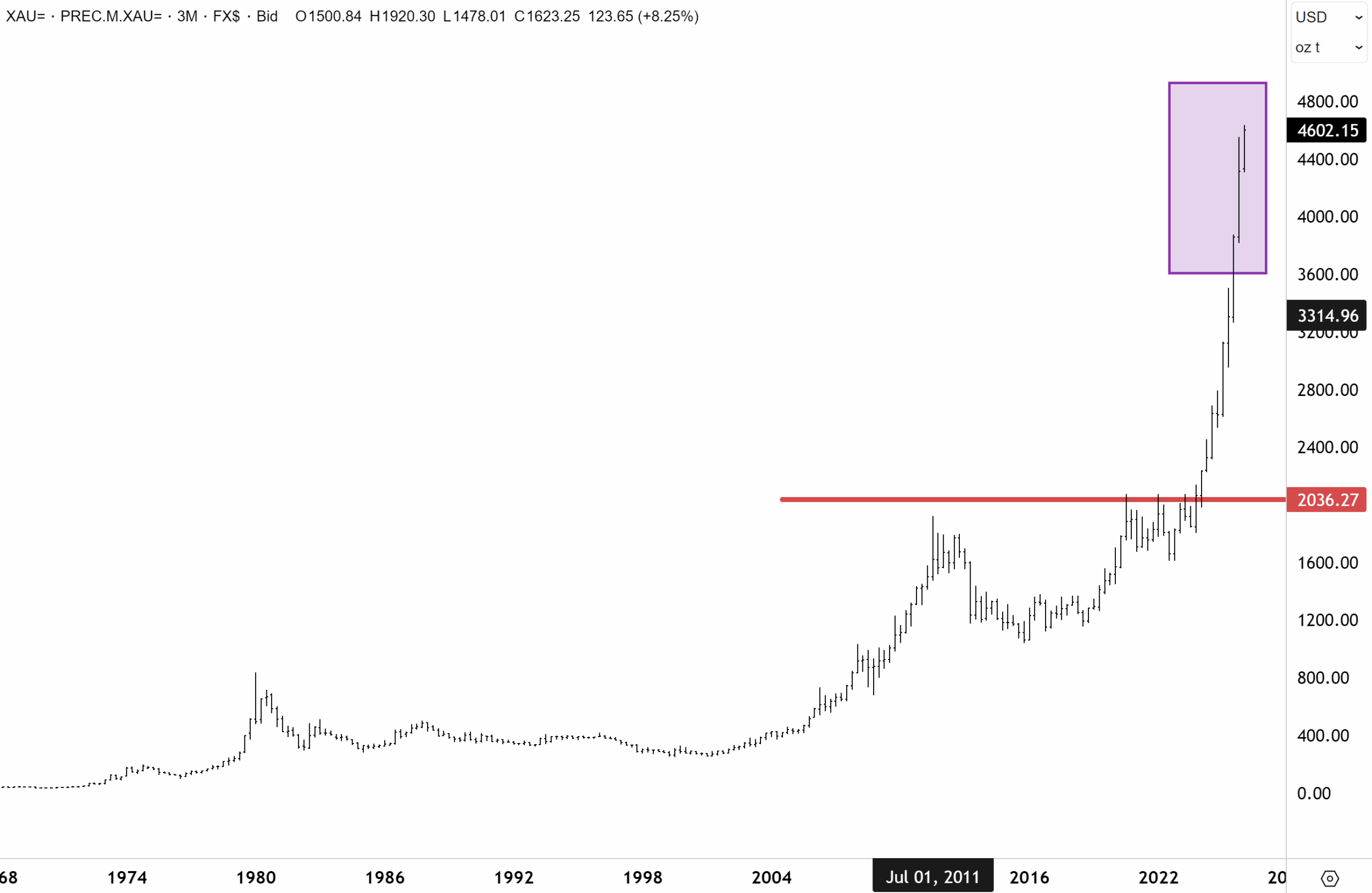

It was no surprise that precious metals surged to new record highs on Monday after the news hit the tape. If the White House succeeds in prosecuting Mr Powell and stacking the board after his tenure is up in April, then there will be ramifications. The market will not want to see the Federal Reserve politically controlled by the Trump Administration – or any government, for that matter. Sustained political intrusion into monetary policy will come at a cost, even if markets are willing to look through these events in the short term.

If the “Rubicon” of Fed independence is crossed, I foresee a much weaker US dollar, a steepening US yield curve, and higher long-term yields. Inflation could also accelerate higher. It is hard to envision precious metals and gold not remaining on the current trajectory and moving sharply higher in this environment.

Gold made a new record high above $4,600oz and is rapidly closing in on our 2026 end of year target at $5,000oz. It’s not even mid-January.

Source: LSEG

Commodities supercycle

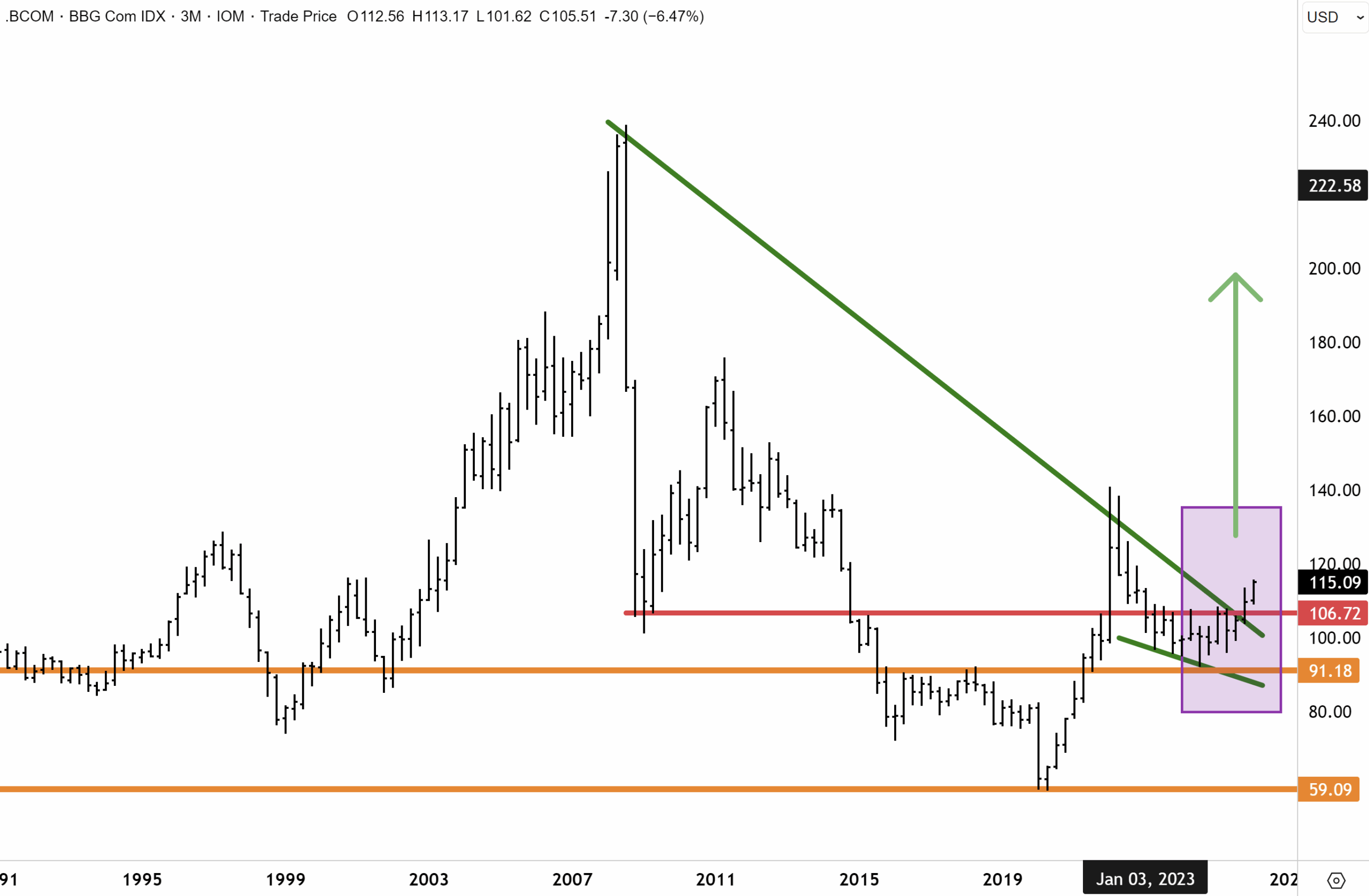

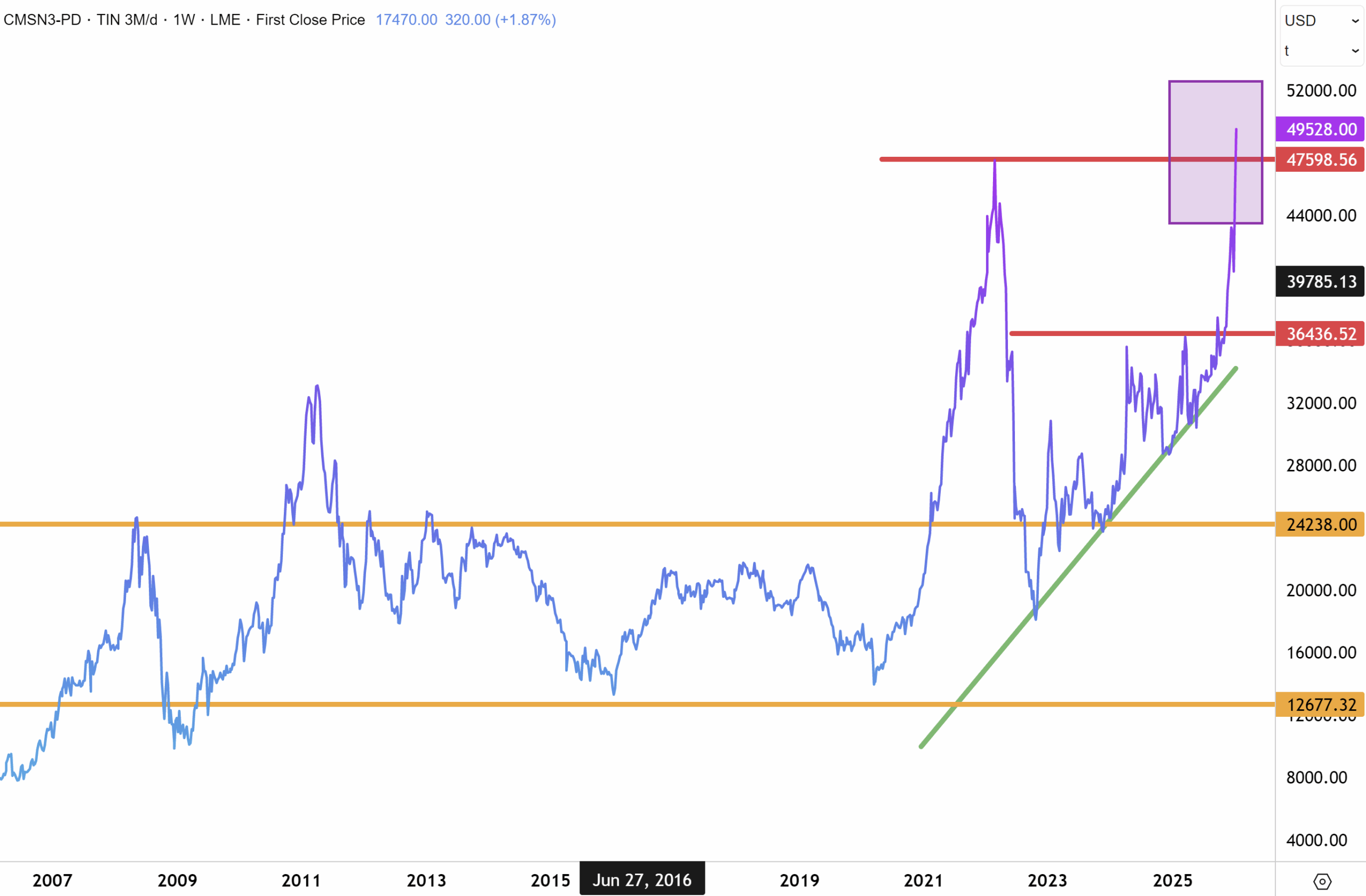

Meanwhile, the bull market in broader commodities seems to be gathering pace. The Bloomberg Commodity Index lifted to near 115 this week, boosted by big gains in base metals and oil. Tin has broken to fresh record highs on the LME this month, trading above $52,000/$53,000 per tonne, driven by a severe supply squeeze layered on top of structurally strong demand from electronics and the energy transition, and amplified by speculative flows in a very small market. Other base metals and commodities are emulating this as well.

The breakout late last year of the Bloomberg Commodity Index from the defining primary bear downtrend defines the “opening sounding shot” of another commodity super cycle that I believe will really get going this year.

Source: LSEG

Tin prices have surged to record highs on the LME, breaking through resistance at the previous historic peak established four years ago, back in 2021. I expect a number of other base metals to soon follow.

Source: LSEG

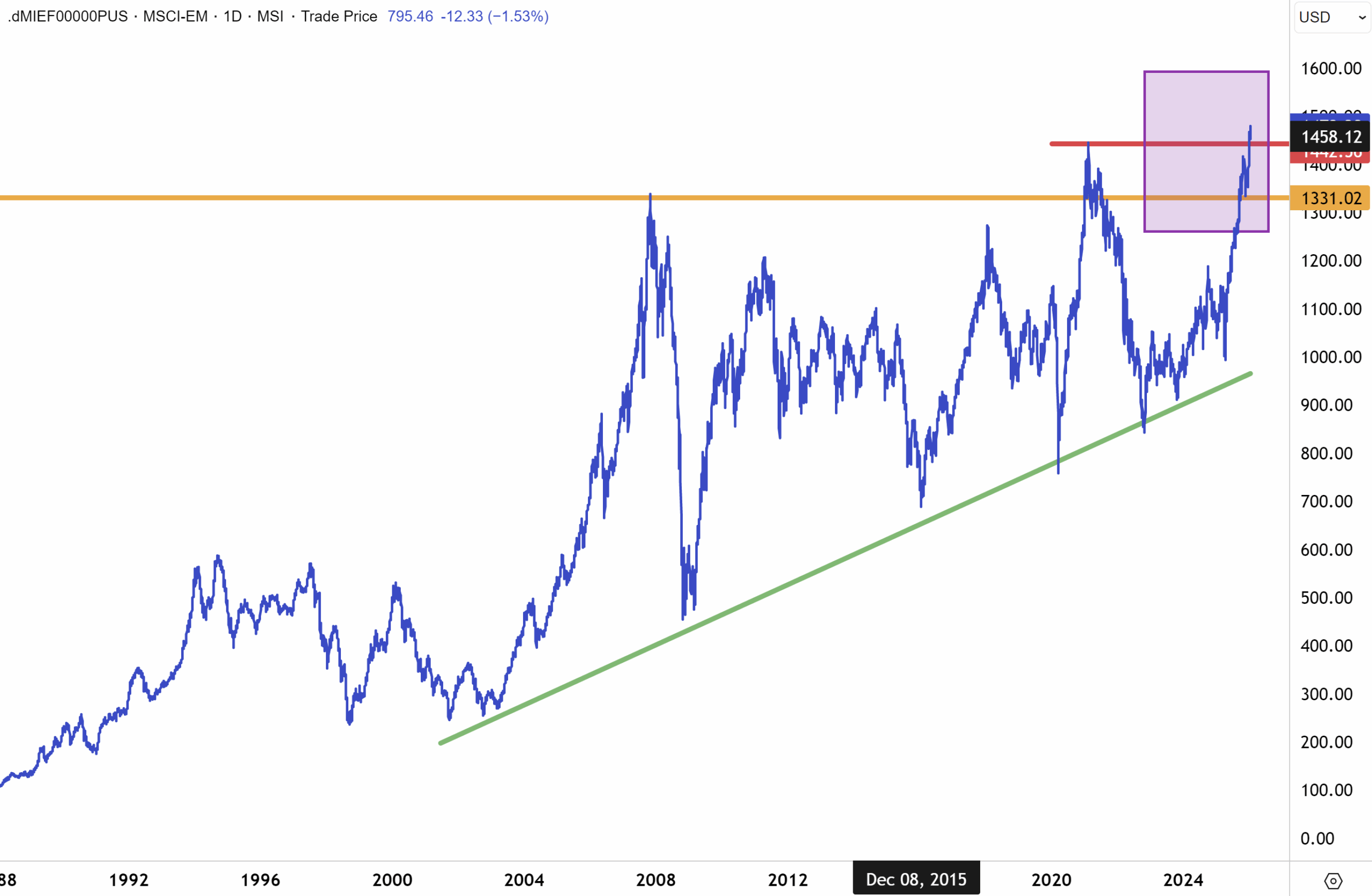

Did emerging markets just stage a short-term rebound phase after posting stellar returns in 2025 last year?

We have conviction that opportunity is emerging in “emerging markets”. We believe that EMs will have another solid performance this year and outperform the US and developed markets after more than a decade of not doing that well. Emerging markets have been underdogs for a long time, but the pendulum is shifting now. Since 2010, the benchmark MSCI Emerging Markets Index has not outperformed US benchmarks for two consecutive years. However, 2026 might prove different.

The MSCI Emerging markets index, which has since topping out in 2007, essentially traded sideways for nearly two decades, albeit establishing a series of higher reaction lows. Resistance above 1300/1400 has effectively capped any advance. The recent breakout above 1400 is encouraging, and if sustained over the coming months (our base case), then the MSCI EM Index could be in for a powerful advance this year – led by China/Hong Kong, but other countries including Brazil and Southeast Asia.

Source: LSEG

Source: LSEG

We have good reasons to believe that emerging markets have entered a multi-year “super cycle”. The foundations underpinned last year’s outperformance are still in place. These factors include a weaker US dollar, resilient global economic growth and a growing awareness amongst global investors that international diversification now makes sense.

Continued investor diversification away from US equities could power international and emerging market equities sharply higher this year. According to Citigroup strategists, outperformance could be prominent, and they cite “a key reason for this is a growing convergence between earnings in America and the rest of the world. Improvements in earnings per share remain possible in key markets outside the US, through government spending in Europe, reflation in Japan and widespread artificial intelligence adoption. Investors are now showing greater confidence in international equities, with current positioning significantly more bullish rest of the world versus the US, and risk appetite generally broader than a year ago”.

These are fair points that I concur with, and one of our calls for this year is that international and emerging markets will do much better and outperform the US on a risk-adjusted basis, with valuations much lower, and growth reasserting. Citigroup remains constructive on global equities and recommends greater diversification into international markets, with a particular preference for Europe and emerging markets over the near to medium term.

The Fat Prophets Global Contrarian Fund has got off to a solid start this year with a month-to-date gain of +7.5% in estimated pre-tax NTA to $2.09. The Fund’s core themes of precious metals, Japanese banks and major Chinese technology stocks all positively contributed to performance…the ASX release highlighted that “In terms of the outlook for markets, we believe a “risk on” environment in financial markets is set to prevail well into the new year. The US reporting season has gotten off to a solid start underpinning our bullish outlook over the first half of the year.”

Meanwhile, FPC shares continue to trade at a significant discount to NTA, allowing investors to buy into a high-quality portfolio of global shares at around $1.50 (yesterday’s closing price was c$1.48). I might be talking my own book, but the large discount seems illogical to me, given performance has been good over the past eighteen months, the Fund has remained true to a deep contrarian value disposition, and a fully franked special dividend of 5c was paid out last year.

One highlight in the ASX release was a relatively new position in GDS Holdings, which the Fund has increased this year. GDS Holdings is a data‑centre developer and operator focused on high-performance facilities for large cloud and internet customers, mainly in China. The company develops, owns and operates large, carrier-neutral data centres in major Chinese economic hubs, providing space, power, cooling and security so customers can house their IT infrastructure.

The ASX release concluded with “we remain bullish this year in our outlook for the China technology sector and see significant scope for outperformance following a severe bear market, when many financial institutions viewed the market as ‘un-investible’.”

Fortune sometimes does favour the brave.

In Australia, the ASX 200 climbed +0.47% to 8,861 and extended a winning streak to a fourth consecutive session on Thursday, despite a negative lead from Wall Street. SPI futures are pointing to a flat start today. Major diversified resource stocks continue to lead in Australia, as financial institutions rotate into the resource sector. BHP, Rio, FMG and S32 have led the ASX200 on the upside this year. This week’s gains have been masked by poor breadth, as decliners outnumbered gainers modestly across the ASX 300.

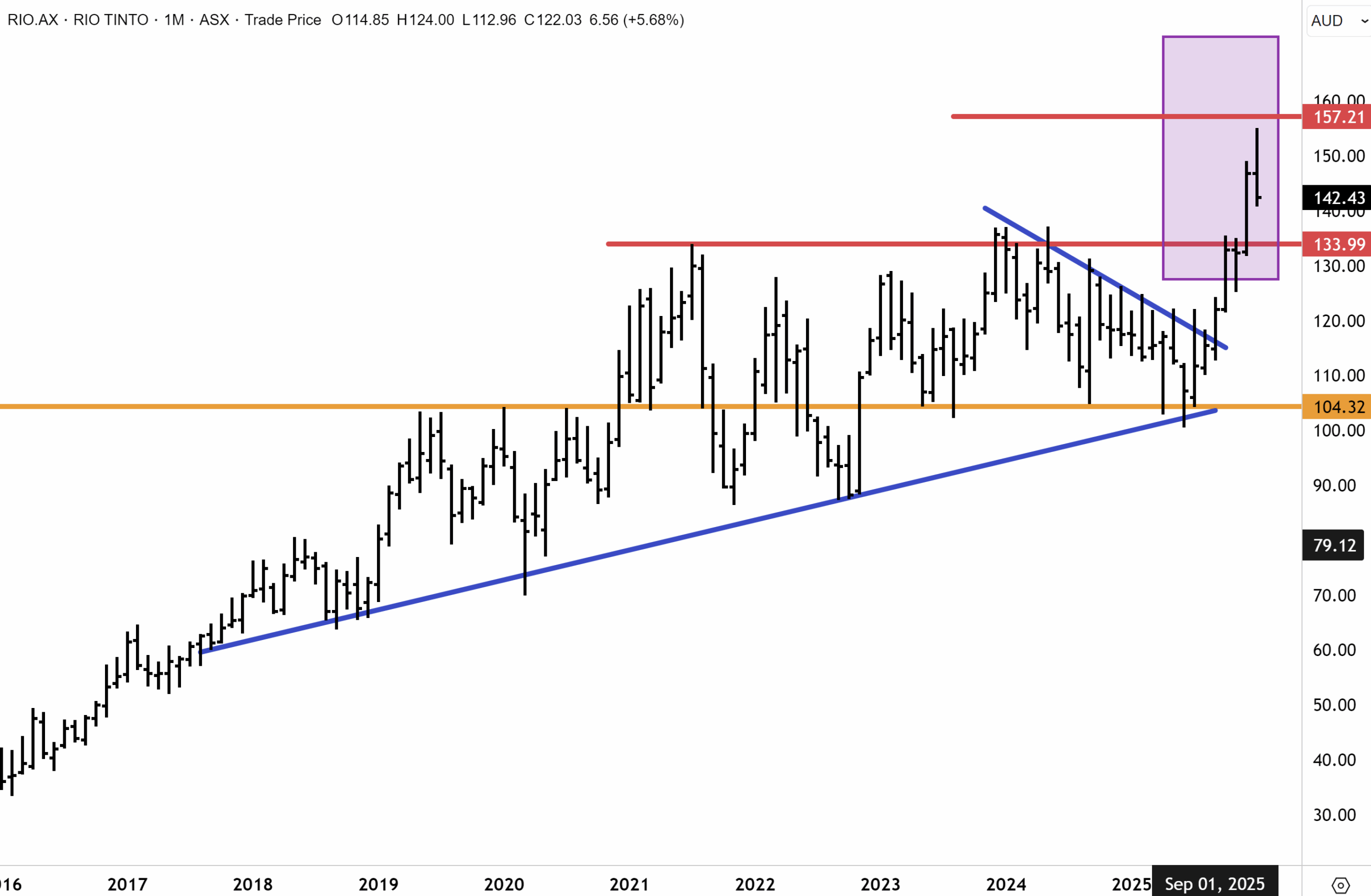

Rio Tinto -0.4% has confirmed early-stage talks with Glencore on a potential merger, prompting an immediate market reaction split between caution and optimism. Rio’s shares sold off on concerns around scale, complexity and execution risk, while Glencore rallied as the prospective target. Rio management stressed there is no certainty a deal will proceed, with a February deadline setting a near-term decision point. Strategically, the discussions highlight a possible path toward greater copper exposure and diversification, but valuation, coal exposure and regulatory hurdles remain central to investor scepticism.

Our bullish technical view on Rio Tinto has played out so far since our last technical update in early December. After breaking through key resistance around $134/$135, Rio surged to new record highs above $157. The stock has since corrected – but we note there is now very strong support at the breakout level at $134, which effectively capped Rio for close to five years. We expect this support level to hold. Our base case for Rio is that once the incumbent consolidation phase completes, upward momentum will resume and that the record highs above $157 will be retested. We continue to have conviction that Rio will extend higher into new territory this year, which is consistent with our bullish outlook for commodities, copper, and iron ore prices to hold well above $100/ton. Disclosure: Rio Tinto is held in our Australian separately managed account portfolios.

Source: LSEG

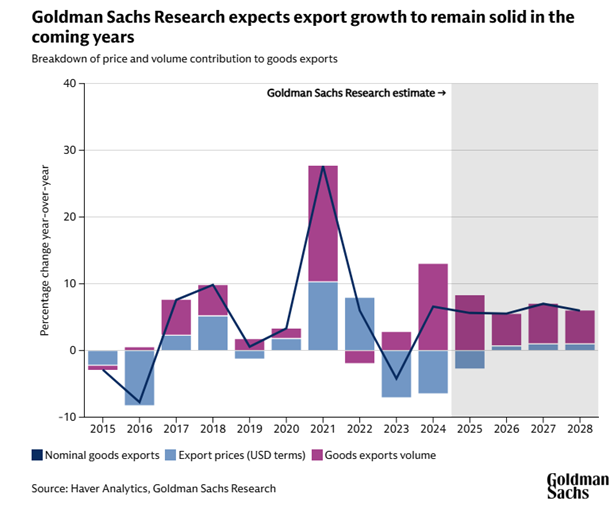

Turning to Asia, Goldman Sachs is issuing a bullish, out-of-consensus projection for China’s 2026 economic growth and export resilience. On this front, Goldman Sachs forecasts that China’s real GDP will grow by 4.8% in 2026. This is well above consensus estimates of 4.5%. Goldman’s projection is based on resilient export volumes (which they see growing) and less economic drag from a stabilising property market. Goldman noted earlier this week that “Chinese exporters have successfully diversified into non-US markets.” I would add that many of China’s new customers are coming from emerging markets. If emerging markets do better from a commodity supercycle, they will spend more on imports, and China will be a principal beneficiary.

Source: Goldman Sachs

Source: Goldman Sachs

I expect China’s property market to stabilise this year following a severe downturn that commenced back in 2021. Goldmans have a similar view. “China’s property sector is in its fifth year of decline. We expect that the property sector’s drag on annual real GDP growth — around 2 percentage points per year in 2024 and 2025 — will narrow by 0.5 percentage points per year over the next few years.”

I would add that domestic demand in China has remained tepid at best since the property downturn began. If green shoots begin to emerge in residential housing, then it stands to reason that domestic demand in China could make a big resurgence and potentially surprise most economists (many of whom remain focused on the rear-view mirror).

We expect China’s property to finally stabilise this year after a severe five-year downturn that began in 2021. A recovery in residential housing could unlock pent-up domestic demand and potentially surprise cautious global economists.

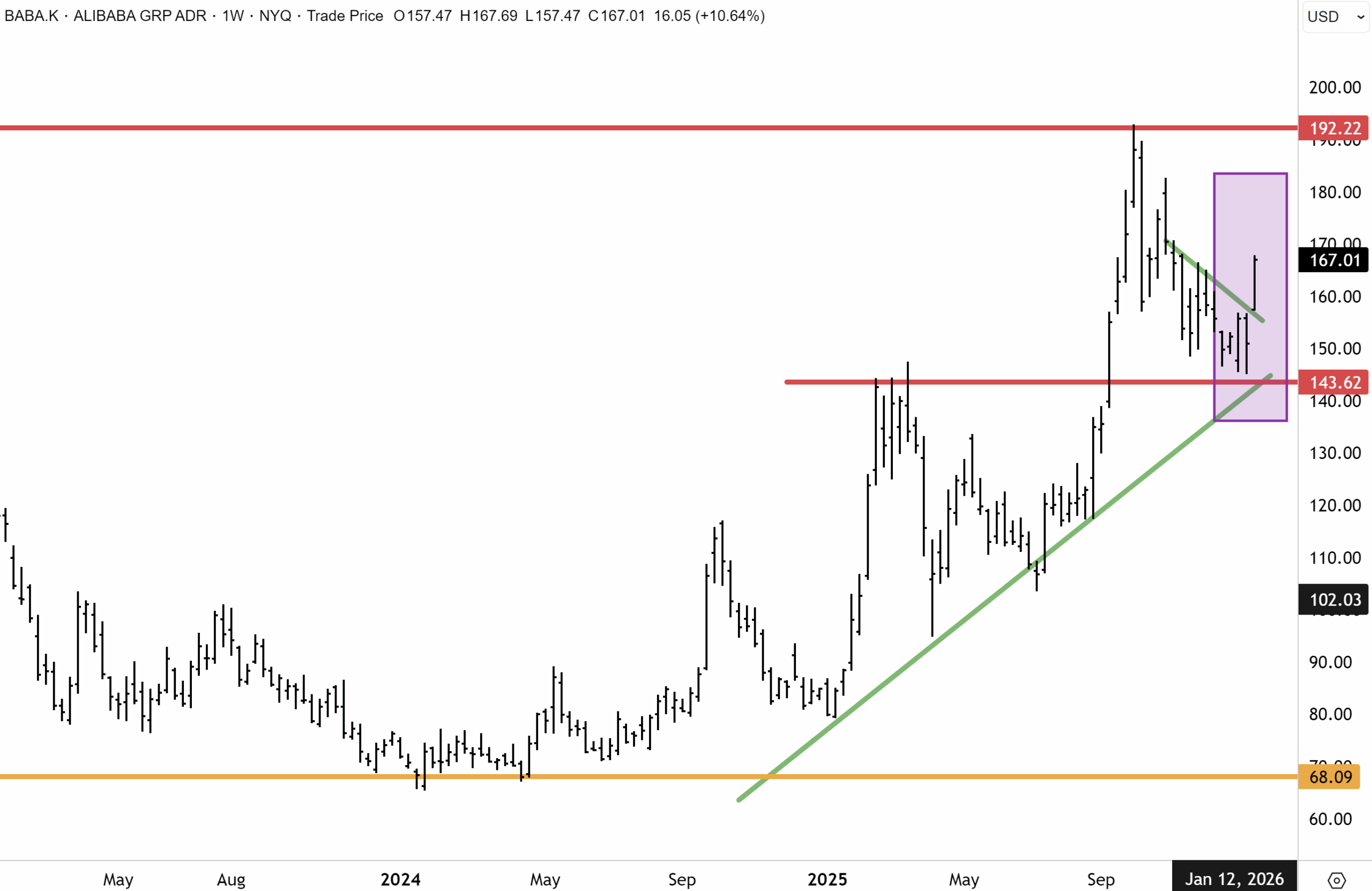

On the tech side, Alibaba’s ADRs outperformed earlier in the week. Beijing’s latest move to curb price wars in the food delivery market will ease “over competition” in the mainland China market. Fresh data has also highlighted the accelerating adoption of Alibaba Group’s Qwen AI models. Alibaba Cloud reported downloads of the Qwen model family surpassed 700 million as of January, underscoring rising interest from developers worldwide. Alibaba has driven uptake by open-sourcing Qwen across a broad range of model sizes, giving developers flexibility to balance performance, cost and deployment needs. The Chinese tech juggernaut is also extending Qwen beyond enterprise use into consumer-facing applications, including the Qwen AI assistant, the Quark search app and Ant Group’s health service.

Following the multi-month correction from the September highs above $190, Alibaba has found support at $140 and resumed upward momentum. The topside breakout this week above downtrend resistance at $155 raises scope for upside extension in our view, and for a potential retest of the three year highs in the months ahead. Disclosure: We hold Alibaba as a core top ten position in both the Asia and Global separately managed account portfolios. (Reach out to patrick.ganley@fatprophets.com.au today for more information).

Source: LSEG

Source: LSEG

The Takaichi Trade

The explosive move in Japanese stocks earlier this week reflected growing speculation that Prime Minister Sanae Takaichi could soon dissolve the government as early as January 23rd, setting up a general election for February 8th. Local media reports suggested Ms Takaichi, known as a fiscal dove, had communicated her intention to senior ruling party officials. Market participants widely believe that early elections could deliver a weaker yen, higher equities, and lower bond prices on expectations of proactive fiscal stimulus. This would be Ms Takaichi’s first electoral test since taking office in October, providing her an opportunity to capitalise on strong public approval ratings and potentially secure a larger majority for the Liberal Democratic Party.

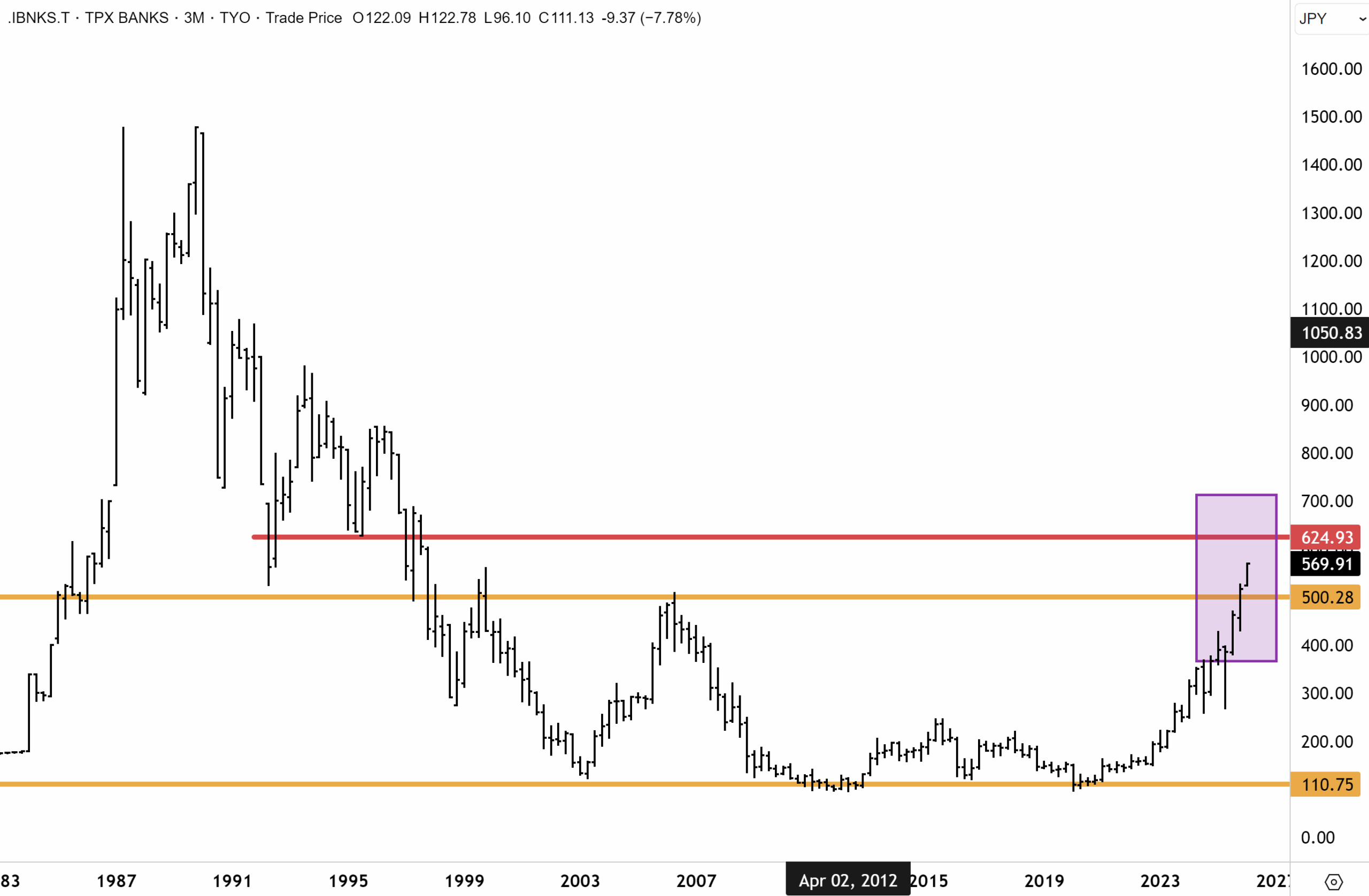

Japanese Banks are being rerated on rising local bond yields, which is driving earnings growth (along with other factors), and I have long been an advocate of the sector. We have maintained an overweight position in the Fat Prophets Global Contrarian Fund for several years now.

The TOPIX Bank index has risen sharply to 569 since hurdling major historical resistance at 500 last year. This resistance level effectively capped the TOPIX Bank index since 2007. With the TOPIX Bank index having now successfully exited an eighteen-year trading range, I believe scope is open for a further significant recovery this year as bank earnings are set to accelerate higher.

Source: LSEG

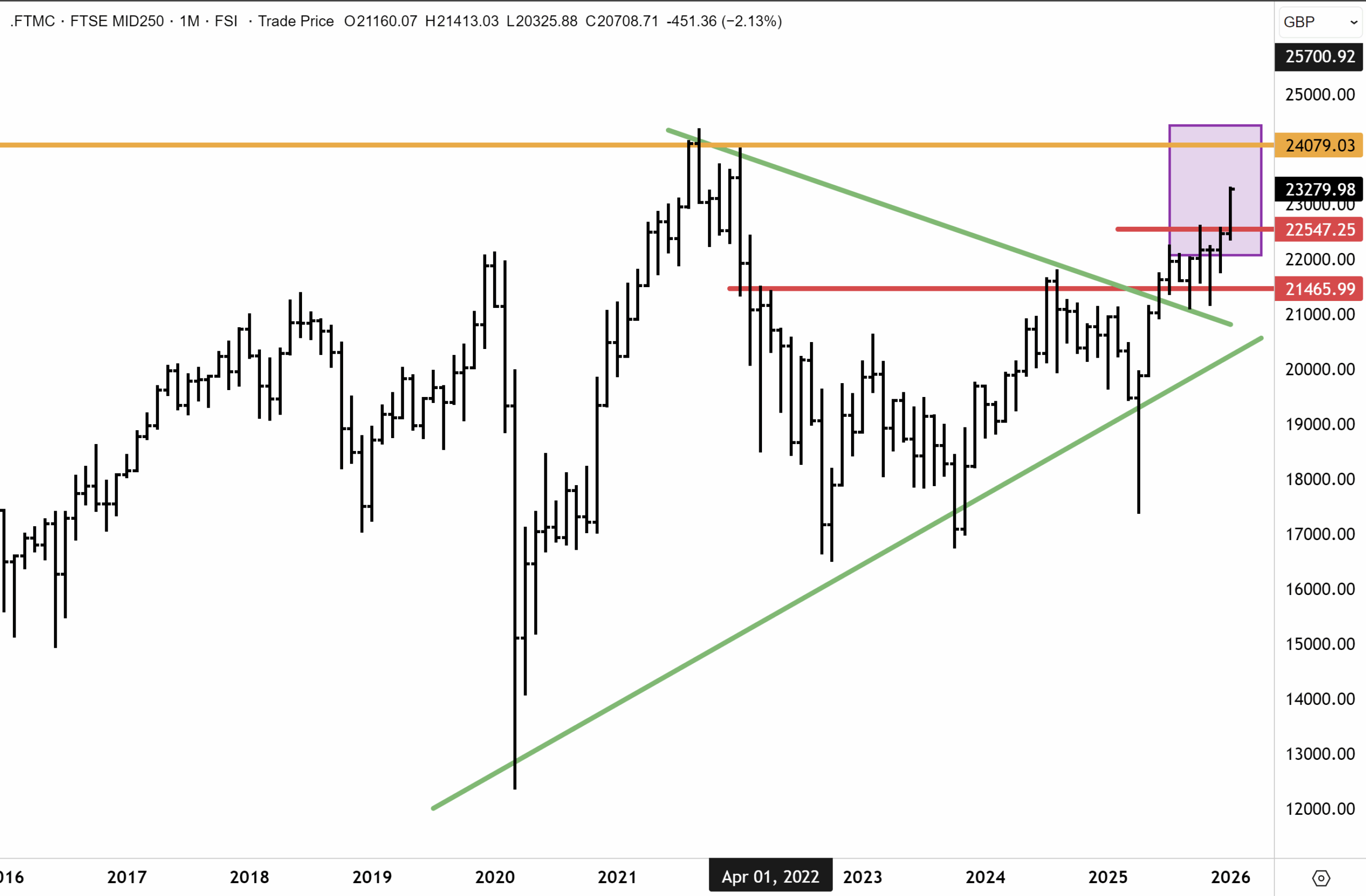

In London on Thursday, investors welcomed stronger-than-expected economic data. UK GDP expanded by 0.3% month-on-month in November, rebounding from a 0.1% contraction in October and exceeding forecasts for just 0.1% growth.

FTSE250 (which underperformed the FTSE100 over the past five years) now appears to be closing the gap. The recent breakout above key resistance points has seen the FTSE250 push higher up to 23,300 this week, with the 2021 record high above 24,000 now within sight. I expect a strong performance this year from UK small/midcap stocks. A breakout above 24,000 would herald the onset of a new bull cycle for the index.

Source: LSEG

Have a great weekend.

Carpe Diem!

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.