Markets Rebound After CPI Shock | Debate, Nvidia Rally, Gold Miners in Focus

Good morning,

Wednesday was a choppy session in the wake of the CPI print which was released prior to the market open. Core CPI (which excludes food & energy costs) came in at +0.3%, which was higher than consensus expectations for a +0.2% rise. This slightly hotter-than-expected print disappointed the market, effectively ruling out a 50 bp cut next week. Inflation is still proving sticky, but the trend is still to the downside, especially with oil prices back below $70. The jobs data is, however, going to dominate and be influential on the Fed in the coming months.

The benchmarks fell sharply on the open with the S&P500 down as much as 1.8% at the session lows before recovering throughout the day to close over 1% higher. It was a big intraday reversal, with the market changing course after the first debate between Harris and Trump and a boost from Nvidia.

The S&P 500 gained 1.07% to close at 5,554 after touching a low of 5,406 during the session. The Nasdaq Composite gained 2.17% while the Dow Jones added 0.31%. Bonds came for sale. Tech dominated, with Nvidia surging by over 8%. Sentiment also improved after the first debate between Harris and Trump, which some considered favoured the Democrats while others felt that the moderators were biased. November is shaping up to be a very close run race. After the presidential debate, pricing for a Trump victory was at 48 cents on the online betting site PredictIt and at 55 cents for a Harris win.

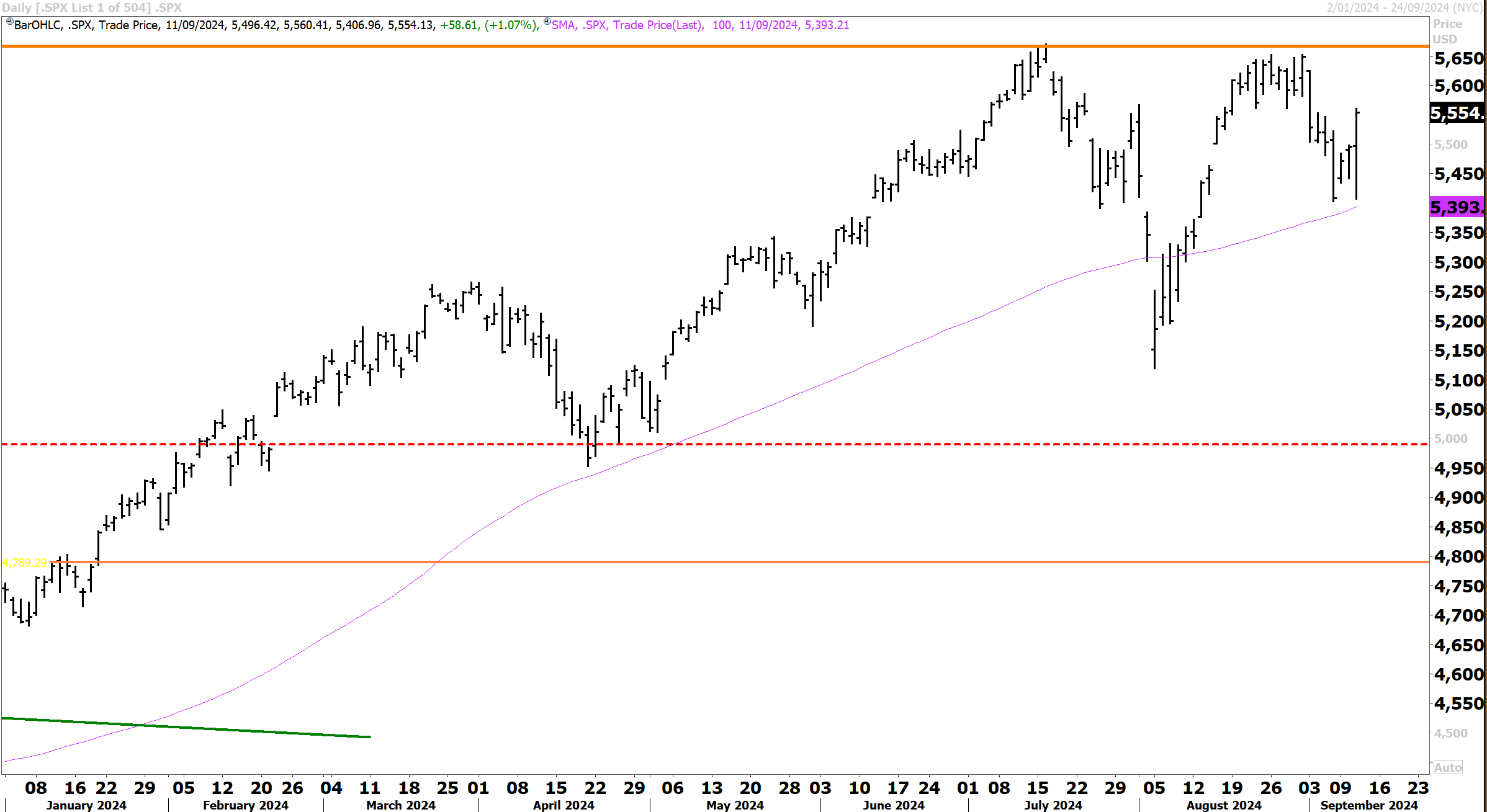

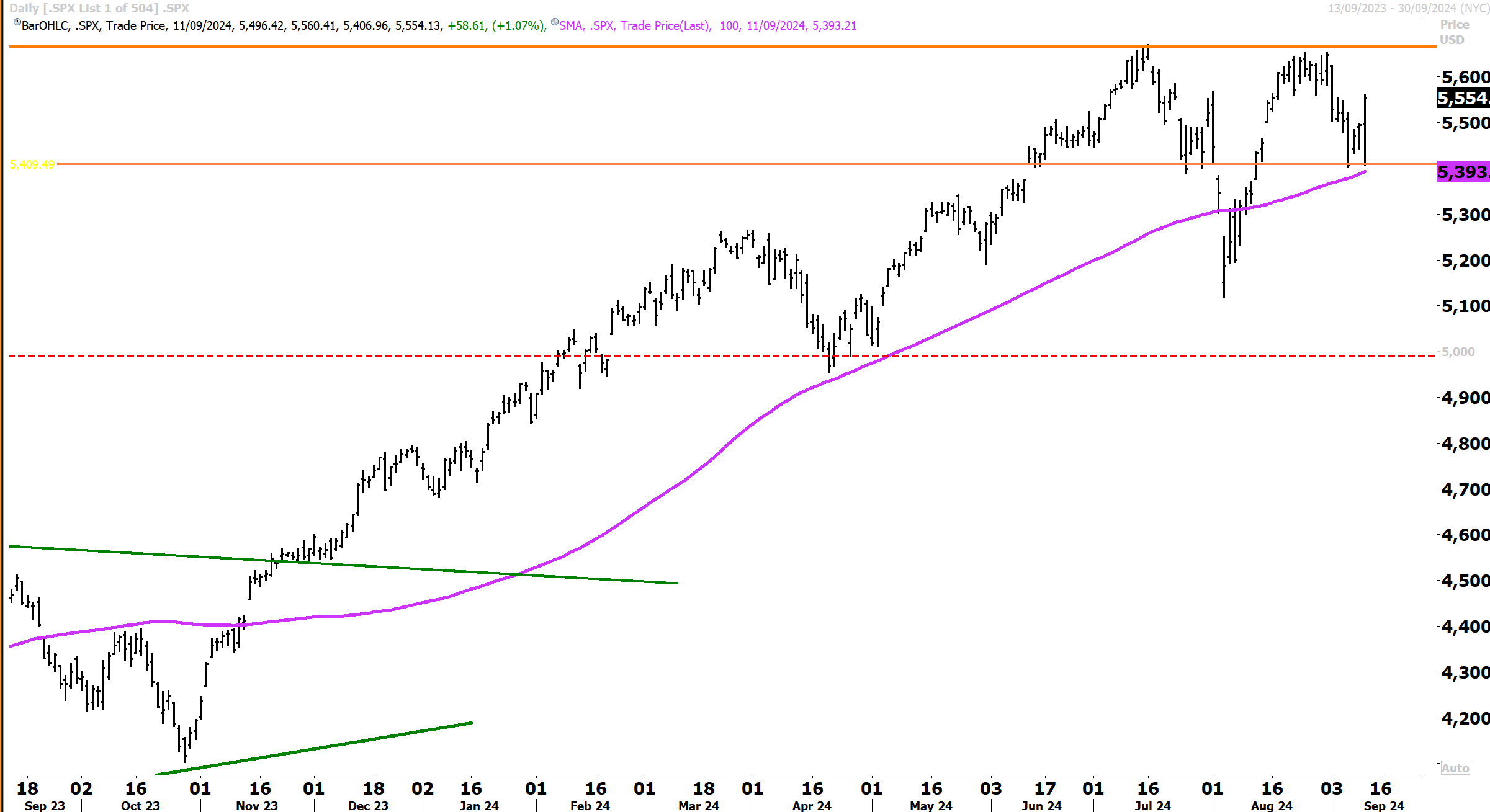

The SPX experienced a big intraday reversal on Wednesday, with the benchmark bouncing off the 100-day moving average.

Bonds sold off with the yields rising across the curve as the market dialled back expectations of 50 bp cut next week. The Fed will now err on the side of caution and go with 25 bps next week. However, risks continue to be weighted towards slowing growth and a deteriorating labour market, which is why traders are still pricing four more 25 bp cuts over the remainder of the year..

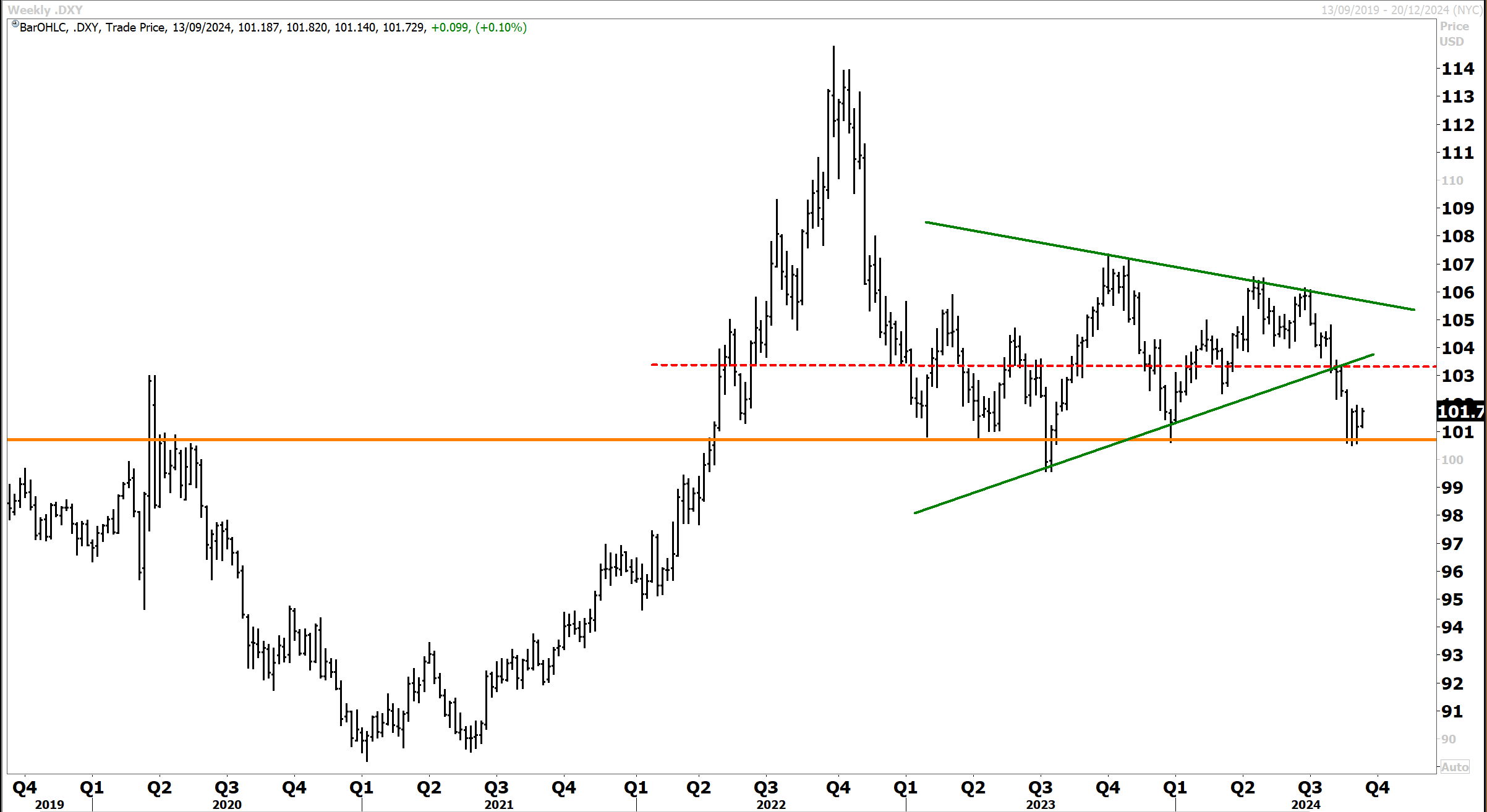

The US dollar was steady, and the DXY little changed at 101.7. Commodities were firmer, with oil rebounding. WTI crude added +2.3%. Precious metals were firmer, with silver adding +1% to $28.70, while platinum and palladium were higher. Gold held on near the record highs at $2,541. Copper firmed +1.7% while the soft ag complex and grains were all higher.

Yesterday’s upside reversal off the 100d moving average for the S&P500 was technically encouraging. However, we are not out of the woods yet. There will still be uncertainty over coming weeks, particularly on the election. The Democrats and Republicans have divergent policies. Trump is likely to raise tariffs, which could restoke inflation. Harris, on the other hand, could increase corporate taxes, which could pressure the economy. The market also has to navigate the upcoming earnings season. This week we saw some major banks come through with lower guidance, and more downgrades are likely to follow.

But having said that, today’s rebound and upside dynamic off the 100d moving average following the initial big swoon was technically encouraging and bullish. The SPX is now within 110pts of the record high. A breakout above the resistance level at the record high at 5666 would raise the scope for an upside extension. Our technical base case is for choppiness and volatility to continue over the coming weeks, but any selloffs or inherent market weakness can be used to deploy cash.

During an interview on Bloomberg yesterday, Morgan Stanley’s Chief US equity strategist, Mike Wilson, made an interesting point. Aside from taking “shelter in quality defensive stocks and avoiding AI related tech names”, Mike Wilson says investors are waiting for a new theme to emerge. “With the AI rally fading and that theme now gone, the market is looking for a new theme. On the growth side, there isn’t one, so what it does is it hunkers down into defensive, high-quality assets until we get the next thing. Whether that’s a bad outcome or a positive outcome, they’re going to hide out in these areas.”

The next big thing?

I think one new theme that could soon emerge is a growing awareness and recognition of the US dollar vulnerabilities and a coming widespread re-rating of the precious metal miners.

The US dollar appears technically to be on the edge of another decline. While many investment banks have a benign view on the greenback, this could change quickly. Both presidential policies will undermine the dollar. The near-term risks a technical rebound, but by the end of the year, the DXY could well have broken below the major support level at 101. The DXY now looks very vulnerable in terms of the technical setup.

What could drive a big move down in the US dollar? Narrowing rate differentials, for one, but a growing awareness of the structural problems that will ensue regardless of who wins in November. Neither Harris nor Trump will represent a panacea for the greenback. Meanwhile, the debt mountain keeps climbing with ever-increasing fiscal spending and is now much larger than the US economy. A tipping point is drawing closer.

Meanwhile, gold and silver miners have been left behind despite relative strength in the underlying spot metal prices. Gold is now outperforming the S&P500 in a relative sense, and the market is not appreciating this, given that the precious metal mining sector has lagged this year despite new record highs in spot prices.

One new theme that could soon emerge in financial markets is that gold, relative to the S&P500, could now outperform. On a big-picture basis, gold has underperformed massively since the 1970s.

But zeroing in on the last five years reveals a very different picture. Gold looks to be now outperforming the S&P500. A topside breakout above 1 on the relative performance chart below of the SPX vs spot gold price could potentially define an important inflection point.

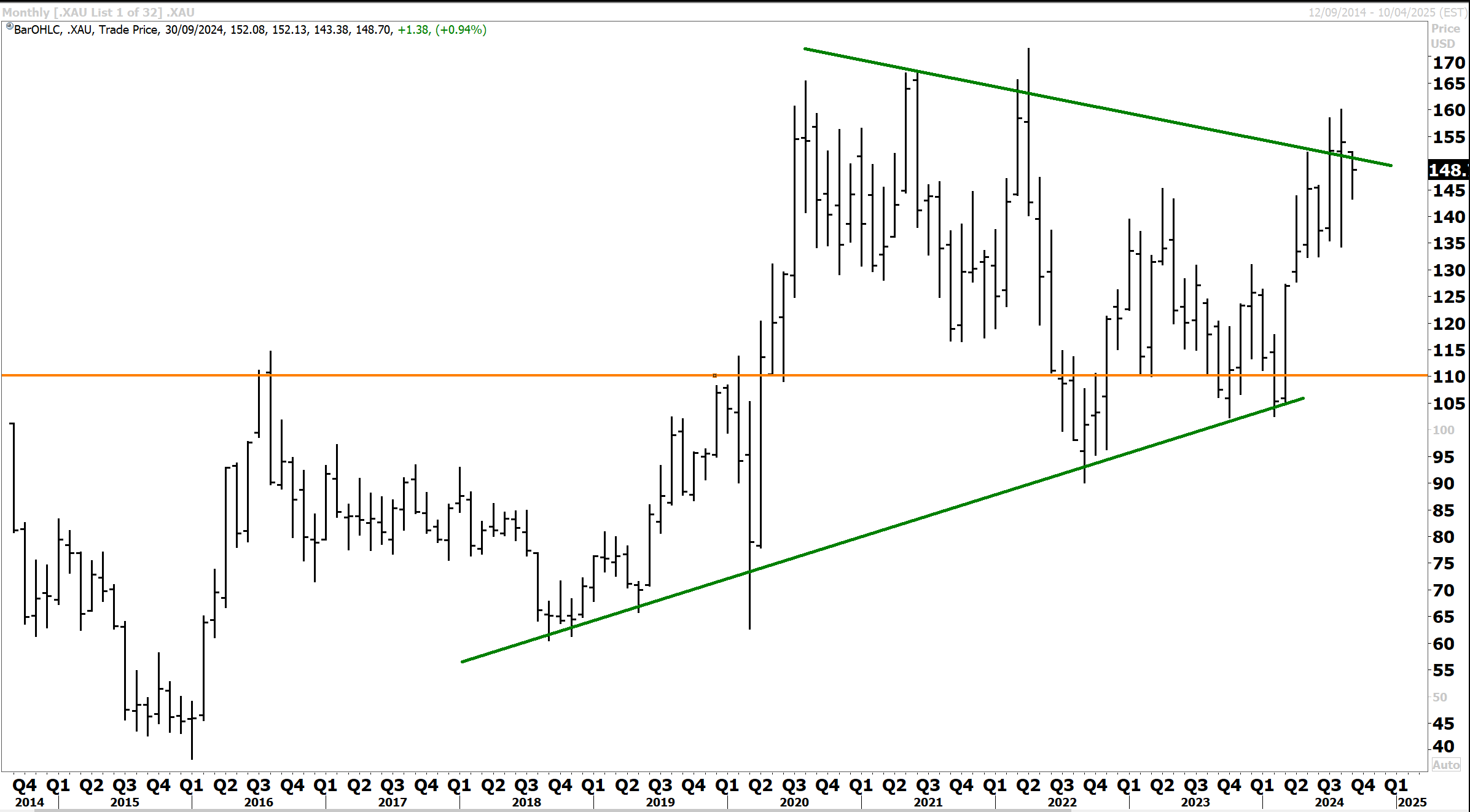

Meanwhile, the precious metal mining sector, as evidenced by the Philadelphia Gold & Silver Miners (XAU) Index, which has underperformed, is now looking much more bullish technically. The XAU index looks to be on the cusp of an important topside breakout on the 10-year chart below.

Carpe Diem!

Angus

Disclosure: Fat Prophets and its affiliates, officers, directors, and employees may hold an interest in the securities or other financial products relating to any company or issuer discussed in this report. Fat Prophet’s disclosure of interest related to Investment Recommendations can be provided upon request to members@fatprophets.com.au.

Chart Source: Thomson Reuters.