A catalyst around the corner?

China’s Ministry of Commerce (MOFCOM) has issued an interim draft proposing the removal of tariffs on Australian wine exports. Although not a final determination, we would be very surprised if the removal of tariffs didn’t go through after reaching this advanced stage. Speaking at The Australian Financial Review Business Summit, the Chinese ambassador indicated this would be the likely outcome.

The AFR quoted Xiao Qian as saying, “Currently, Chinese authorities are reviewing and investigating our tariffs on Australian wine and things are moving on the right track, in the right direction.”

After punitive tariffs were imposed in late 2020, devastating Australian wine exports to China, relations between the two countries have been distinctly cool for much of that time. We have seen signs of thawing over the past year and placed a significant probability that a review kicked off in late 2023 would result in a positive outcome for TWE, although we considered this a ‘bonus’ rather than a necessity for our buy recommendation on the stock. We noted a China ‘reopening’ would be a welcome growth opportunity, though the company has already executed well by filling that hole by increasing sales in Southeast Asia, materially strengthening the business.

We continue to see value at current levels, given the solid outlook for luxury wines, the addition of DAOU Vineyards products, and a possible nadir for the Treasury Americas business in 1H24. We are encouraged by the ongoing shift in sales strategy, focusing more on the high-end premium and luxury segments, with the Penfolds brand being a key differentiator and ‘crown jewel’ asset.

Additionally, we foresee more strategic divestments and refined internal investments, as previously indicated. This includes cutting costs in the Treasury Premium Brands segment and minimising the impact of soft demand for lower-tier wines, enhancing the business quality at the group level. As the company integrates DAOU, it is positioning to create a separate sales and marketing focus between luxury and premium product portfolios within the laggard Treasury Americas segment from the beginning of FY25. We rate Treasury Wine Estates a buy.

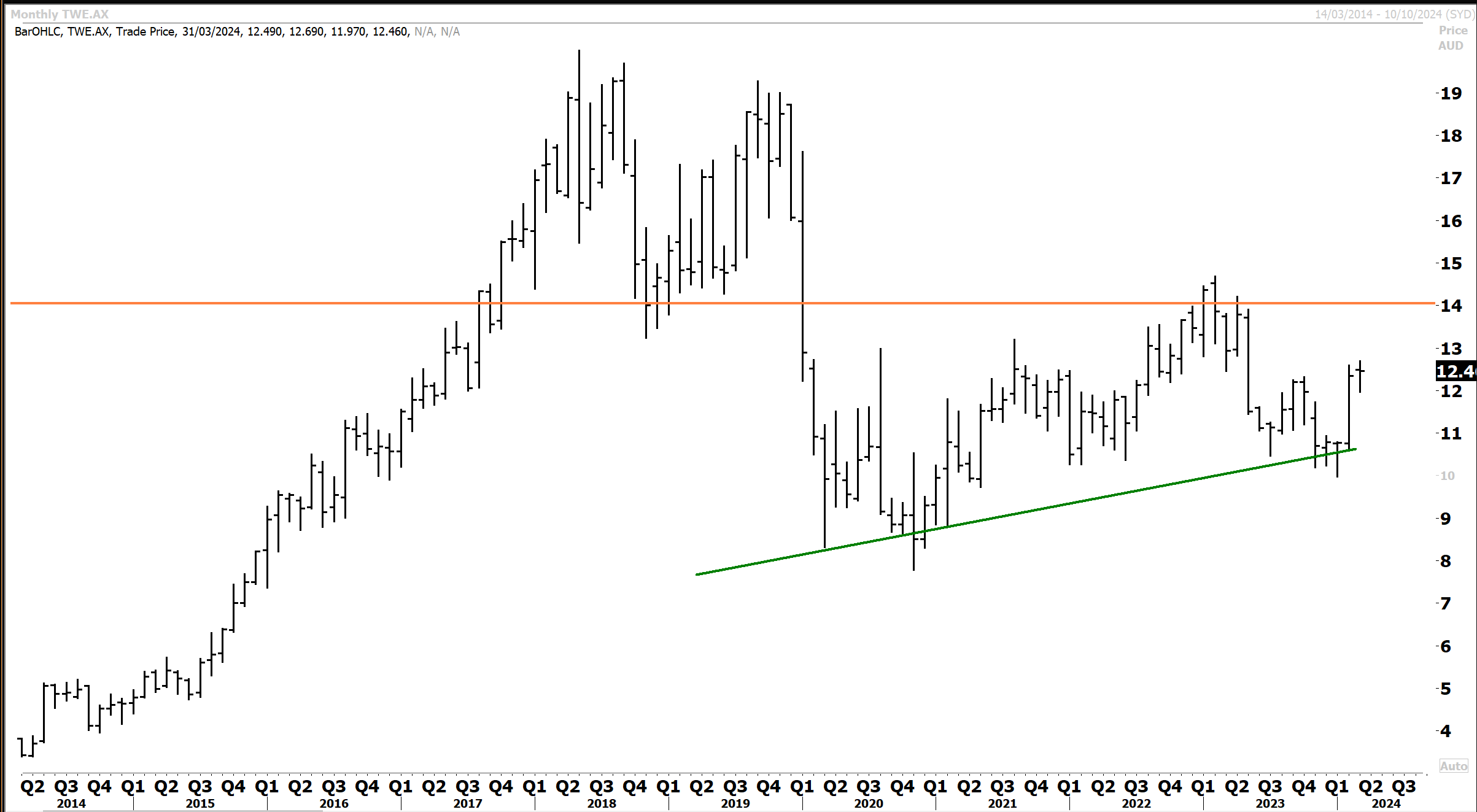

Treasury Wines has bounced off the primary uptrend and appears technically to be headed towards a retest of the major resistance level at $14. A breakout above $14 would significantly raise the scope for further upside and another run at the record highs. It is encouraging that TWE has held above the primary trendline since the pandemic lows and the introduction of Chinese tariffs.

An imminent outcome. The final determination from MOFCOM is now expected within the coming weeks, and we are firmly optimistic the outcome will be favourable.

Treasury Wine has kept its options open for this possible outcome. The company opted to keep some luxury premium Penfolds volume in reserve in 1H24, which was a headwind for the financials. The Chinese market accounted for roughly 30% of group earnings before the imposition of sky-high tariffs. TWE expects only a minimal incremental EBITS benefit from renewing Australian country of origin exports to China in FY24 should the tariffs soon be removed. We would expect this contribution to lift in FY25, although certainly aren’t expecting a return to the ‘old days’ anytime soon. Positively, TWE was able to successfully pivot to ASEAN sales, which has strengthened the business. Meanwhile, Penfolds’ buyers should brace for global price rises for the high-end Penfolds range if the Chinese tariffs are removed.

In the 1H24 results, group net sales revenue (NSR) of $1,284.3 million was flat on a reported basis and 2.3% lower in constant currency. Positively, luxury NSR increased by 4.3% as the premiumisation strategy continued. Penfolds was the only segment that posted an increase, with sales rising 9.2% to $448.1 million. The Penfolds segment remains the key earnings driver, with EBITS increasing 2.9% to $186.9 million. Group EBITS for the six months came in at $289.8 million, matching market expectations. This marked a 5.8% decrease, hampered by a 17.5% fall in Treasury Americas’ EBITS to $93.1 million. Treasury Premium Brands EBITS was down a more modest 3.2% at $45.8 million.

In summary, Treasury Wine Estates looks poised to benefit from the removal of China tariffs, which we expect to begin benefiting the financials from FY25. TWE delivered to market expectations overall in 1H24 despite a lacklustre performance from the Treasury Americas segment. A strategic shift away from the lower-tier market is ongoing. For investors with a mid-term perspective, Treasury Wine offers an attractive proposition in our view. The company is committed to a premiumisation strategy, eyeing sustainable growth and margin expansion, with a strategic game plan in place should Chinese tariffs ease. TWE has significant scope to expand the distribution of the DAOU luxury range. We retain a buy rating.