New Directions?

Shares in Alliance Aviation Services dipped lower despite 1H24 results revealing a three-fold jump in statutory profit before tax of $37.7 million. Alliance Aviation is the biggest independent aviation training centre in the United States and Latin America.

Turning to the technicals, listed on the ASX, Alliance Aviation has corrected sideways since 2020 in a primary downtrend. While the stock is holding above support at $2.70, only a breakout above $3.30 and price action follow through would confirm a topside inflection.

Company Overview

Alliance Aviation Services (ASX.AQZ), founded in 2002, is a leading provider of contract, charter, and allied aviation services in Australasia. With a focus on safety, reliability, and customer satisfaction, Alliance has established itself as a trusted partner for clients in the mining, energy, government, and aviation industries.

Alliance offers a diverse range of aviation services, including contract and charter flights tailored to the specific needs of its clientele. Its offerings also extend to wet lease services, providing support to other airlines. The key point here is that Alliance provides essential transportation (personnel, equipment, and cargo) and logistics for miners especially towards remote and challenging locations.

One of Alliance’s distinguishing features is its ownership of the entire fleet, comprising 37 Fokker 70/100 aircraft and 41 Embraer E190 aircraft. Additionally, the company has firm purchase commitments for an additional 26 E190 aircraft until mid-2026. This diverse fleet enables Alliance to cater to various operational requirements efficiently.

We find Alliance appealing largely due to its strategic role in providing contract and charter aviation services to essential industries like mining, energy, and government. With a diversified client base and ownership of its entire fleet, Alliance ensures operational flexibility and efficiency, making it a preferred partner for clients in safety-critical sectors.

Aligned with the positive outlook for the commodity and mining sector, Alliance stands to benefit from the increasing demand for reliable aviation services in remote and challenging locations. As mining activities expand globally, driven by population growth and infrastructure development, Alliance’s market position and growth potential are poised for further enhancement.

That aside, the company also recently appointed a new CEO. Mr. Stewart Tully, who currently serves as the Chief Operating Officer (COO) of the company, will be promoted to the position CEO effective March 1st, 2024. Mr. Tully has been with Alliance since 2015 when he joined as the General Manager – Operations in Brisbane. He brings with him extensive experience in the aviation industry, accumulating 34 years of direct or indirect involvement in the sector.

We like this development as [subscribe_to_unlock_form]Mr. Tully has demonstrated the necessary experience and leadership in running Alliance. With the company leaning heavily on operational excellence, a CEO with background in operations should keep the company in the right direction.

In addition to Mr. Tully’s promotion, Alliance has initiated a search process for two additional Directors as part of its Board renewal strategy. This process aims to ensure Board stability while bringing in fresh perspectives and expertise. The company plans to manage this renewal in an orderly manner.

1H24 Results Review

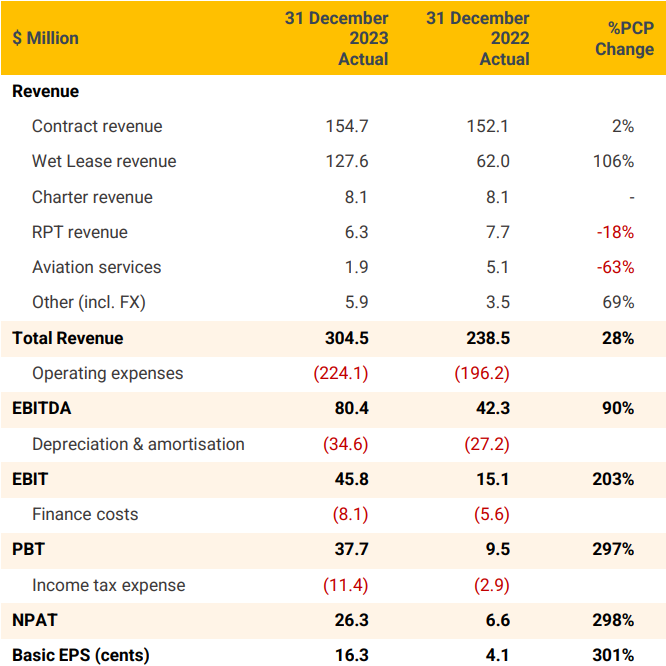

With that out of the way, a brief review of the 1H24 results. First off, Alliance Aviation reported total revenue from operations of $299.4 million for 1H24, showing an increase of $64.0 million from last year. Growth in revenue was driven by significant expansion in contracted wet lease operations.

While in terms of profitability, the Statutory Profit Before Tax (PBT) for 1H24 was $37.7 million, a significant increase from $9.5 million in the previous corresponding period (1H23). This represents a substantial growth of $28.2 million or 296% year-on-year.

Source: AQZ 1H24 Presentation

Source: AQZ 1H24 Presentation

The solid growth in Wet Lease operations has resulted in a substantial bump in record flight hours of 50,793 for 1H24, representing an increase from 32,365 flight hours in HY23.

Going forward, Alliance Aviation expects growth in earnings for the 2H24. Management plans to continue deploying capacity to meet increasing demand for wet lease and FIFO (fly-in-fly-out) operations. The delivery of seven E190 aircraft in the 2H24 should also add to the momentum. That aside, management expressed that their focus remains on cost control and maintaining profitability margins in a high inflation economy.

Despite its niche appeal, we do recognise the high-risk nature of this business with it subject not only to fuel prices – typical vulnerability of airline services – but also to commodity prices. Lower prices of minerals can impact demand for services though contractual nature may reduce impact.

That said, at this point, we believe it more prudent to issue a Traffic Light on Alliance Aviation Services (ASX.AQZ). We will track it as part of our watchlist and, when a better buying opportunity presents itself, we will revisit the company as a potential addition to the Fat Prophets portfolio.[/subscribe_to_unlock_form]