Waiting for a Bargain

Rebel and Supercheap auto owner, Super Retail Group (ASX.SUL) surged after a trading update revealed robust trading during the Christmas period with sales up 3% to $2.02 billion for the 1H23 – another record result and ahead of expectations. Management tried to temper expectations by issuing a warning on rising wages and rents that might dent profit margins.

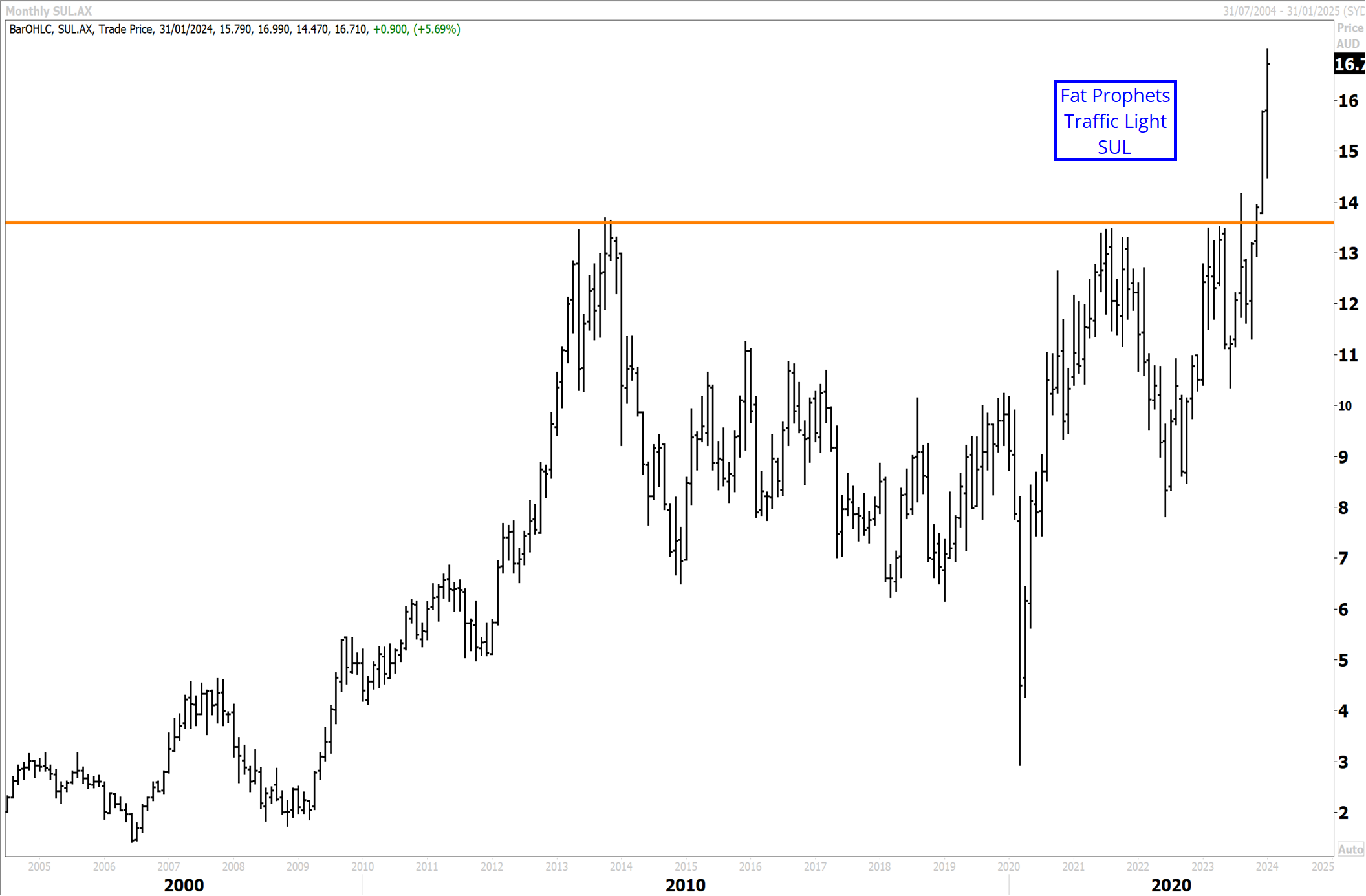

Before we look closer at the company, we quickly turn to the technicals. Super Retail Group has broken above historic resistance at $14 in dynamic fashion this month. The breakout marks the resumption of upward momentum to new record highs following a near ten-year consolidation.

Company Overview

For those unfamiliar, Super Retail Group is an Australian retail company (specifically ‘specialty’ retail) that operates several well-known brands, including Supercheap Auto, Rebel, BCF (Boating, Camping, Fishing), and Macpac. These brands specialize in automotive parts and accessories, sporting and fitness equipment, and outdoor recreational and camping gear.

That said, a quick rundown of the brands:

Supercheap Auto specializes in automotive parts, tools, accessories, and related products.

Rebel is a sporting goods and sportswear retailer offering a wide range of products for various sports and fitness activities.

BCF (Boating, Camping, Fishing), as based on its name, focuses on outdoor and leisure products, catering to camping, fishing, and boating enthusiasts.

Finally, Macpac specializes in outdoor equipment and apparel for activities such as hiking, camping, and travel.

We do like Super Retail because it operates a diverse retail portfolio which can be a solid hedge against downturns in any single segment. It also holds a leading position in the automotive, sporting and outdoor market segments which give it better economies of scale relative to the typical mom-and-pop retailers while enjoying stronger brand recall.

There is also the fact that there is a global trend towards health, fitness and outdoor activities which do match well with their various product ranges.

Additional positives for the group include its multi-channel strategy where both physical stores and an online retail platform allow customers to shop in their preferred manner. The strong online retail presence is also a key positive for the group making sales resilient even during the pandemic (a quick look at the charts prove the resilience during the outbreak).

Finally, we also recognise management’s willingness to engage in strategic acquisitions (think: Macpac) which has allowed to company to expand its product offerings and enter new markets.

Trading Update – 1H24

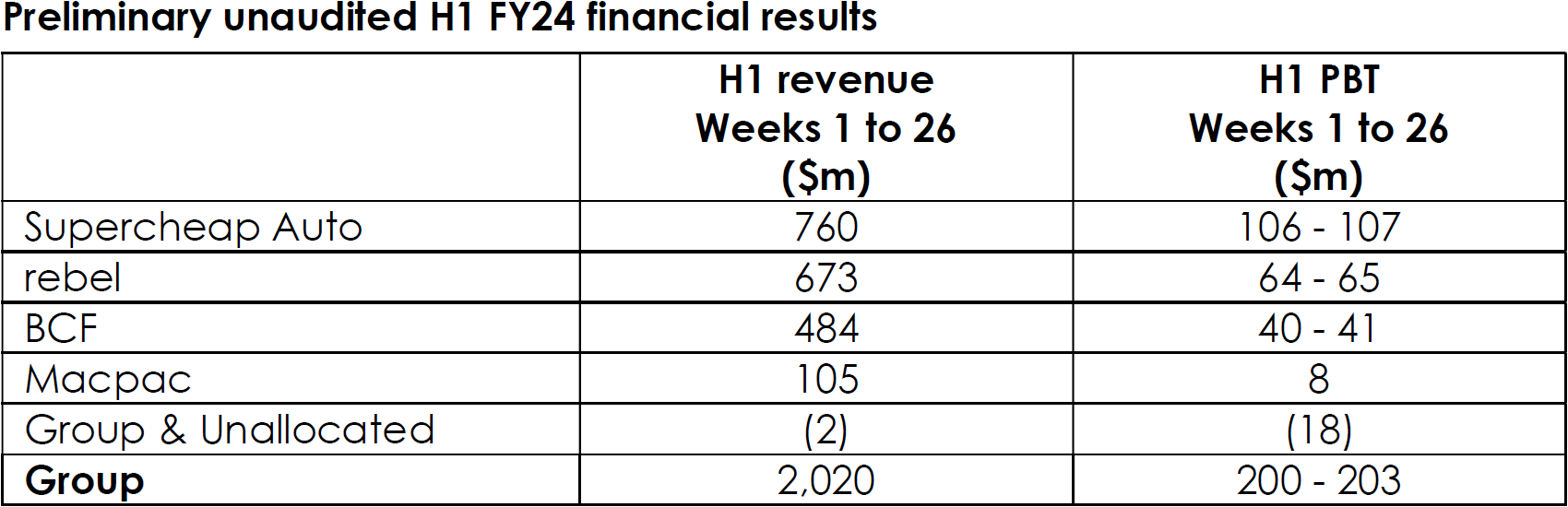

Moving on, the company also released an impressive trading update which covered the 1H24 period. Super Retail just exited a very successful holiday period with revneues hitting $2.02 billion – a record result. [subscribe_to_unlock_form]Super Retail Group’s CEO, Anthony Heraghty, commented that the holiday season was highly successful for the group, with positive like-for-like sales growth. However, cost of living pressures on consumers affected the retail trading environment in the 2Q24.

Source: SUL 1H24 Trading Update

Source: SUL 1H24 Trading Update

First, on a segment basis, Rebel Sports segment experienced a 1% decline in net sales, with comp sales decreasing by 3%. BCF segment showed positive results with an 8% increase in net sales and a 2% rise in comp sales. While Macpac segment reported a 4% increase in net sales, while comp sales remained flat.

On the margin front, Gross Margins are expected to be higher in 1H24 than in 1H23. However, the cost-of-doing-business (CODB) as a percentage of sales increased due to inflation impacting wages, rent, and electricity. This has particularly affected Rebel, considering its lease portfolio and higher team member-to-store ratio.

Going forward, management expects profits to fall slightly year-on-year due to CODB pressures. That said, management anticipates a profit before tax between $200 million and $203 million for the period. This is down from $218 million last year but exceeds consensus estimates – which was another major driver for the rally.

On the valuation front, Super Retail trades at reasonable levels with forward PE at 15.6x and a dividend yield expected to be around 4.6%. PB is also reasonable at around 2.62x.

At this point, we believe there is clear potential for Super Retail Group but the recent surge in prices mean that there will be considerable volatility while the market tries to figure out what the company is ultimately worth.

In the meantime, while we wait for a better opportunity to enter Super Retail Group (ASX.SUL), we will put it in our watchlist as a Traffic Light.[/subscribe_to_unlock_form]