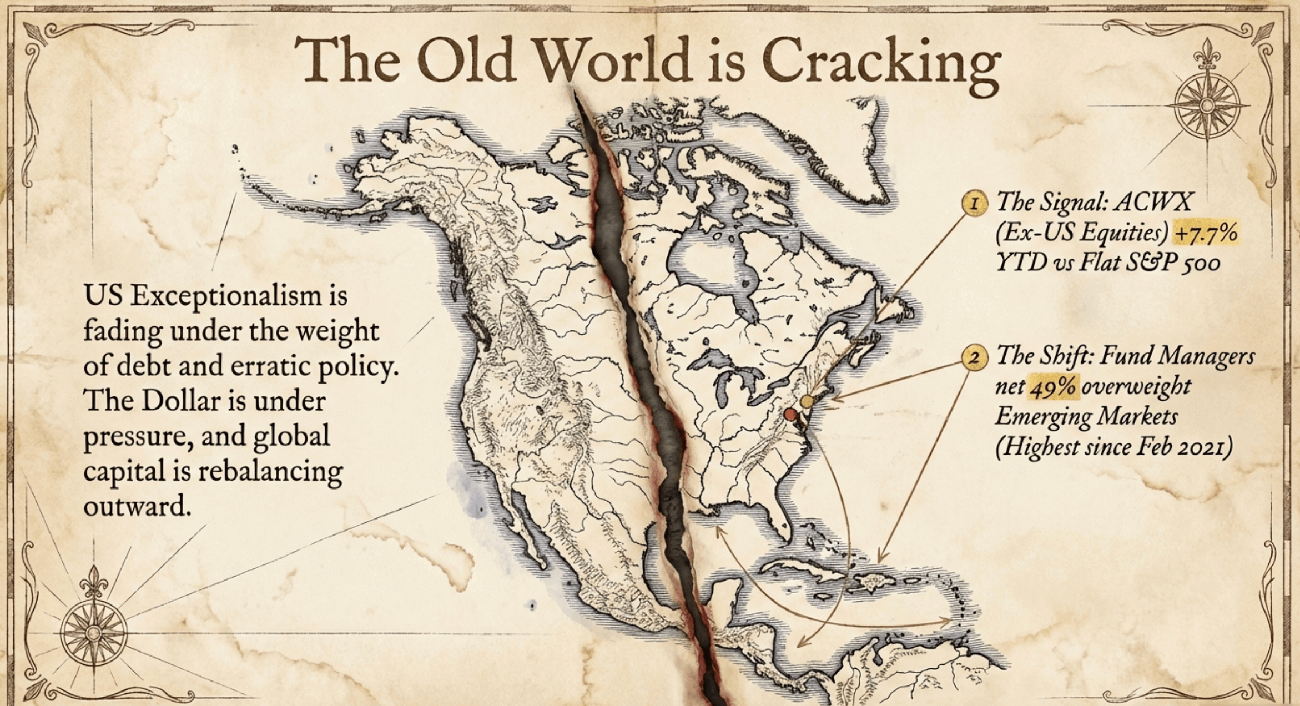

- The narrative of US exceptionalism is showing more cracks in early 2026, with policy uncertainty, AI valuation jitters and a softer dollar shifting capital flows globally.

- Global leadership is rotating: ACWI ex-US is up roughly +7.7% YTD, while the S&P 500 is flat and the Nasdaq is negative.

- Investor positioning confirms the shift, with fund managers now net 49% overweight emerging markets – a meaningful conviction change.

- US earnings remain fundamentally solid, but the market is becoming more selective, rewarding certainty and discounting execution risk more aggressively.

- The market is increasingly favouring AI infrastructure (chips, power, networking, commodities) over the software layer, where valuation risk is being repriced.

- Australia’s market strength remains heavily resources and bank-driven, consistent with the “Old School is New Again” theme.

- ASX reporting season dispersion is wide, with more than half of ASX 200 stocks moving >5% on results day, providing an opportunity set for investors – keep up to date with our daily and regular research reports.

- The domestic Australian macro remains finely balanced.

- The Year of the Fire Horse: China/HK equities retain a credible re-rating setup supported by reasonable valuations, improving shareholder returns and supportive liquidity conditions.

- Japan’s structural bull case is strengthening, underpinned by political clarity, targeted fiscal stimulus and accelerating corporate capital discipline.

Report spotlight

- BHP delivered a strong HY26, driven by copper strength, becoming the core earnings engine. The dividend was given a hefty bump. BUY.

Week Ahead

- China mainland markets reopen early next week following the Lunar New Year closure.

- US PCE inflation (Friday US time) is the key global macro catalyst; a print above 2.7% YoY risks pushing bond yields higher and pressuring risk assets.

- A softer PCE outcome would support the Fed easing narrative and provide relief to rate-sensitive equities.

- ASX reporting season enters its final heavy week, with continued potential for outsized single-stock moves.

- Markets will focus closely on earnings guidance quality rather than headline beats, given the high-dispersion environment.

- Watch AUD/USD sensitivity to US rates and inflation data.

- Monitor commodity price momentum

- Japanese equity flows remain important after renewed foreign buying interest.

- RBA expectations will continue to be shaped by incoming inflation data ahead of the April–May policy window.

2026 has opened awkwardly for investors who banked on US exceptionalism continuing uninterrupted. Erratic White House policy toward historical allies, a rapidly growing debt profile, a sharp sell-off in software, and jitters about mammoth AI-related capital spending have collectively weighed on Wall Street indices in the year’s opening weeks. The greenback continues to look pressured, and we see scope for emerging markets – particularly Asia, including the developed market Japan – to continue outperforming through 2026.

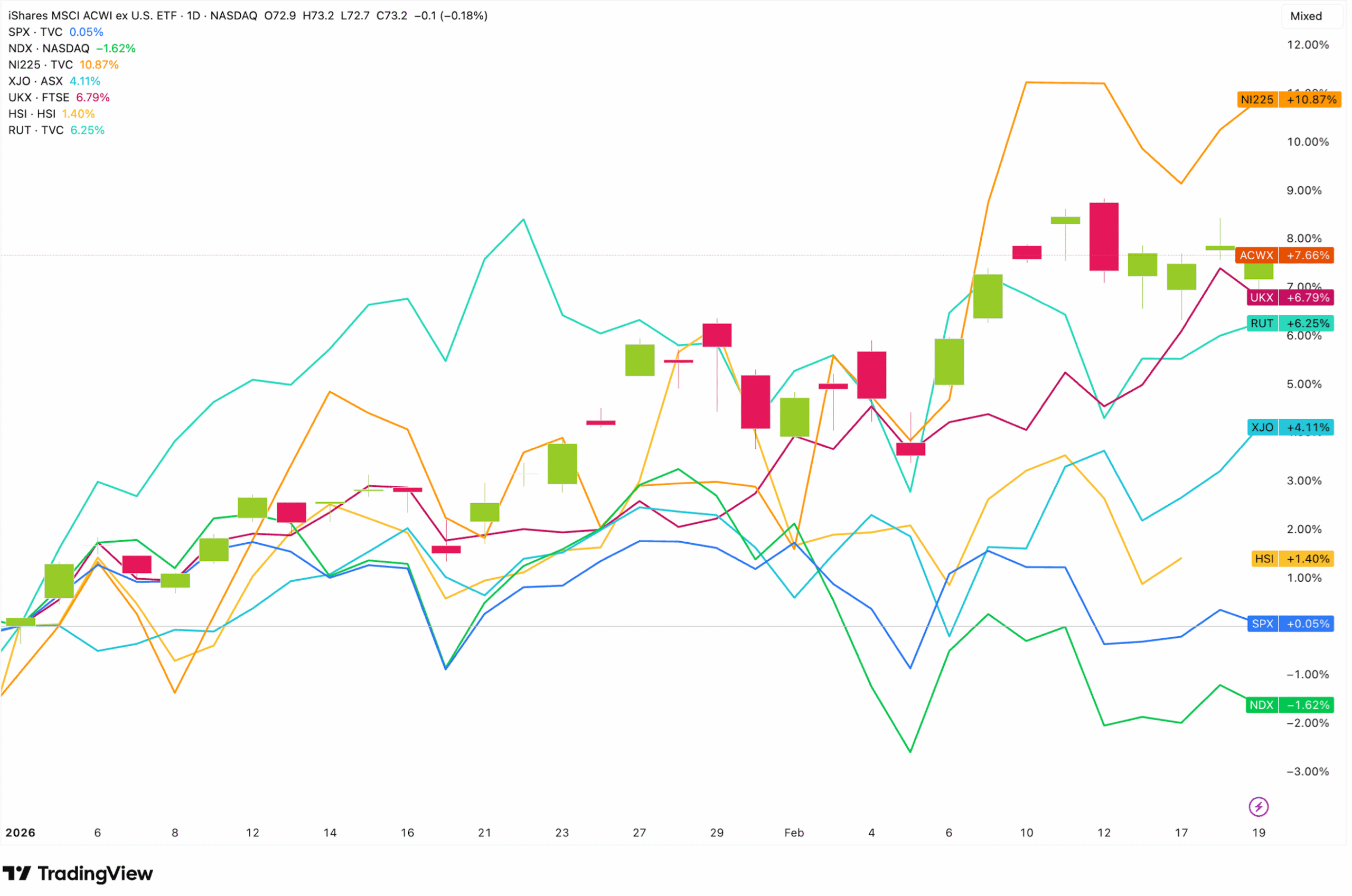

We have long talked about the structural cracks in the US dollar. The market capitalisation of the US as a percentage of global market cap far exceeds the relative share of the US economy in global GDP – a divergence that is increasingly difficult to justify and that has historically corrected when the dollar turns. The correction appears to be underway. At the close on 18 February, the iShares MSCI ACWI ex US ETF (ACWX) was up approximately 7.7% year-to-date, far outperforming an effectively flat S&P 500 and a Nasdaq Composite (NDX) currently below water.

ACWX is a broad proxy for developed and emerging markets, excluding the US, and the signal it is sending is unambiguous. We note that small-caps in the US are a pocket we find relatively more attractive (you can see the relative outperformance of the Russell 2000 – RUT – in the chart), along with more old school areas, like the broader commodities complex. Indeed, energy, basic materials, industrials and consumer staples have rallied hard YTD in the US. Meanwhile, Japan (NI225), the ASX200 (XJO) and the FTSE100 (UKX) are also faring well.

Bank of America strategist Michael Hartnett argues that 2025 and 2026 will be remembered as the inflection where US exceptionalism fades, and a broader global rebalancing begins. This is a topic we have long discussed and advocated that our members should consider for their portfolios.

He ties the rotation partly to Trump’s willingness to run the US economy hot – a mix that lifts inflation risk, pushes bond yields higher, and encourages investors to trim US-dollar asset exposure. He also connects it to AI: building out AI capability is commodity-intensive, and emerging markets are key suppliers of those inputs. That is a framing we find compelling and consistent with what we are seeing in copper, rare earths, and the broader resources complex.

Positioning data suggests the swing has gathered real pace. Bank of America’s latest fund manager survey shows managers are net 49% overweight emerging markets, up from 40% a month earlier, the strongest reading since February 2021, and reportedly sitting approximately 1.4 standard deviations above the long-run average. That is a conviction shift. Meanwhile, the Australian Financial Review reports that Goldman Sachs has lifted its forecast for Asian earnings growth to 31%, above the 29% consensus and up from its prior 24% view, while arguing emerging markets are markedly more resilient than they were five years ago. We certainly agree.

Another dominant market force this week was continued AI jitters – not because anyone changed their mind about AI’s potential, but because the market is struggling to sort out who actually captures the value. The early positioning is that the infrastructure layer is winning (semiconductors, data centre networking, power, commodities), and the software layer sitting above it is genuinely threatened.

This week’s moves (think continued pressure on software and platforms, to the Nikkei’s continued strength run, Australian banks rallying and BHP’s bumper dividend powered by transition-metals demand) certainly suggest that the seismic moves we have often talked about in our regular correspondence, remain in play. It is in the physical infrastructure of the new economy: copper wire, data centre networking, chip fabrication, and the commodity base that underpins all of it. Australian investors, with their structural exposure to real assets and a financial sector generating earnings certainty, are better positioned for this world than many of their global peers realise. BHP delivered a blockbuster half-year result with a hefty dividend increase, while NAB hit an all-time high. Elsewhere, energy stocks surged as Iran rejected US demands in Geneva and oil prices jumped. Meanwhile, foreign Japan added the final piece, with foreign investors buying Japanese equities in size. China’s market was closed this week for the Lunar New Year holiday. Hong Kong staged a modest +0.5% advance on Monday, before holidays from Tuesday to Thursday, reopening again today – this note is prepared on Friday mornings. Gold (US$4,997/oz at the time of writing) has hovered within a narrow range around the US$5,000/oz level over the course of the week, while silver is US$78/oz at the time of writing.

The US reporting season: Solid

FactSet data shows that with 74% of S&P 500 companies reported, the picture is robust. Think blended earnings growth of 13.2% (the fifth consecutive quarter of double-digit growth), revenue growth of 9.0% (the highest since Q3 2022), and net profit margins of 13.2% (the highest since FactSet began tracking them in 2009). On the other hand, the beat rate of 74% is below the five-year average of 78%, suggesting less aggressive guidance sandbagging or genuine management uncertainty about the outlook; revenue beats of 73% are above historical norms, pointing to top-line outperformance even as margin conversion is selective.

Information Technology leads all sectors at 30.7% earnings growth and 20.6% revenue growth, driven by NVIDIA and broad semiconductor strength. Communication Services follow at 13.6% on strong results from Alphabet and Meta. Industrials’ 26.0% headline growth is almost entirely a Boeing ‘bump’, strip out a $9.6 billion one-time gain on its Digital Aviation Solutions transaction and the sector would be showing a -1.1% decline. Energy was the only sector with a revenue decline (-0.3%), entirely driven by oil prices averaging $59.14/bbl in Q4 2025 versus $70.09/bbl a year earlier. Consumer Discretionary was the worst sector at -1.0%, consistent with the higher-rates-for-longer consumer stress visible in Australian data as well.

Forward guidance is positive. Some 55% of companies issuing Q1 2026 guidance guided positively, well above the five-year average of 42%. The forward P/E of 21.5x has compressed from 22.0x at year-end as EPS estimates rose 2.2% while the index barely moved. So earnings are growing into the valuation rather than multiple expansion doing the work – that is positive. Full-year 2026 earnings growth is projected at 14.4%.

An interesting takeaway here is the divergent performance we are seeing from the various sectors, relative to their reported performance and even guidance in many cases. This is a market now moving to pay a premium for more relative certainty (i.e. products that keep global trade going and households fed) versus discounting any hint of uncertainty (software).

ASX IN FOCUS

The ASX 200 has delivered a solid week, hitting a record 9,086 at the close on Thursday. The internal composition of the move was notably healthy, with energy, banks, industrials and communication services firm and a modest rebound in tech. Financials did a lot of the lifting are are up roughly +8% YTD, though outpaced by energy, up +12.5% and materials +11.5%.

Deliver or Drown — Earnings Season Sets a High Bar

The defining characteristic of this reporting season has been extreme dispersion. According to Global X strategist Marc Jocum, more than half the stocks on the ASX 200 moved more than 5% on their results day. Companies that beat and provided upbeat guidance enjoyed a ‘warm embrace’ from investors, but companies that merely met, or that beat the number but missed on some qualitative dimension, were sold without mercy – it is brutal out there these days, which is typically attributed to more quant players, hedge fund ‘pods’ and passive ETFs. Essentially, much trading around results days is automated, and stocks can easily overshoot in each direction. That is an opportunity for patient investors.

NAB, HUB24, Sonic Healthcare and Telstra were big winners this week. Zip Co, Medibank Private and Lifestyle Communities incurred punishment after their updates.

Australian Macro Note: The RBA Has a Problem

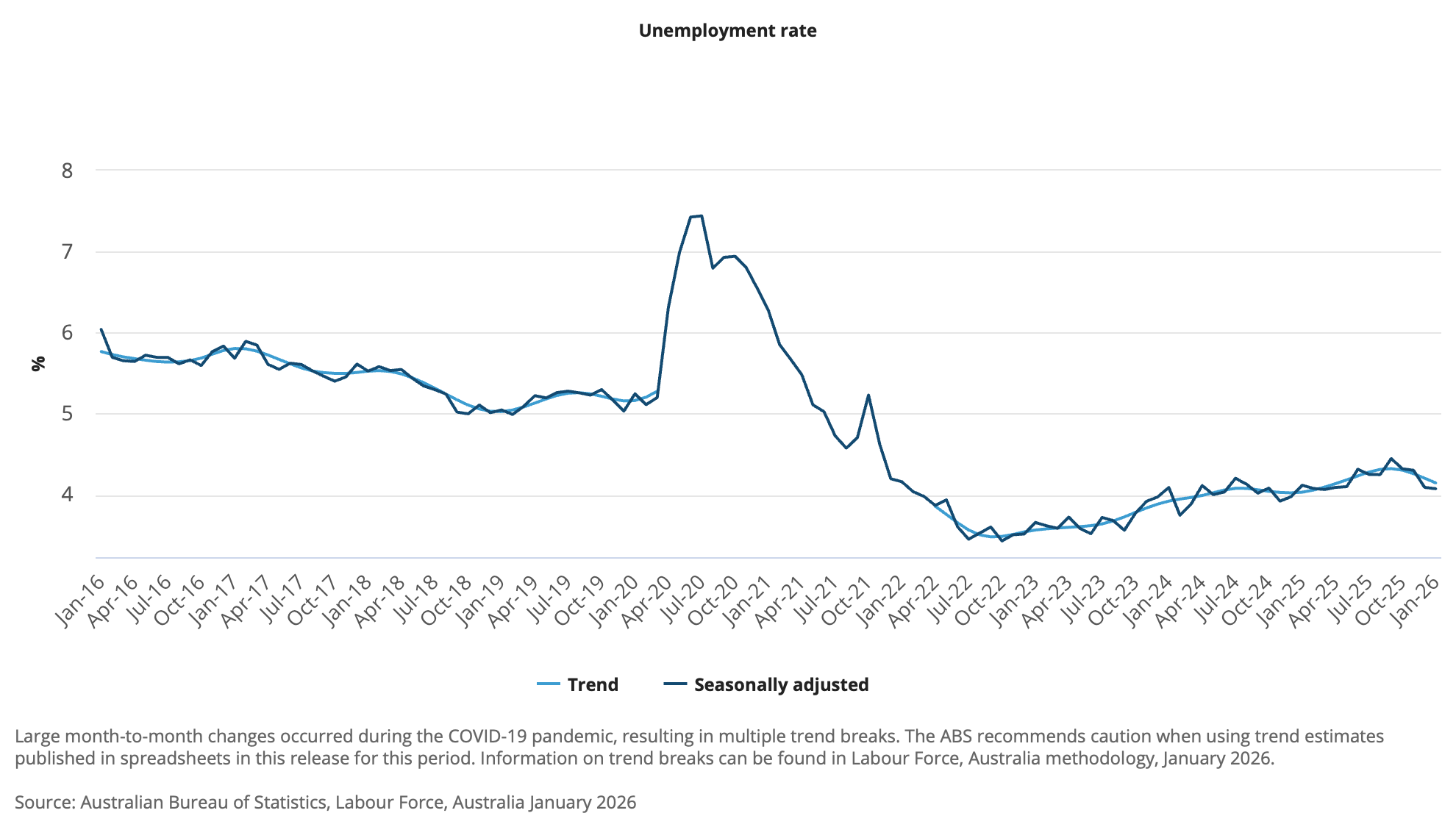

The week’s Australian macro data arrived in a consistent formation. The labour market is tight, wages are sticky, consumers are stressed, and the RBA has no credible pathway to cutting rates anytime soon; instead, bets on another rate hike in the coming months are rising.

January employment added 17,800 jobs, with unemployment holding at 4.1%, matching a nine-month low in trend terms. Full-time employment rose 50,000, partly offset by a 33,000 fall in part-time work.

The wage data published earlier in the week reinforced that reading. Australia’s Wage Price Index rose 0.8% in Q4 2025 and 3.4% year-on-year, in line with forecasts on the headline, but with a composition that keeps the RBA wary. Public-sector wages accelerated to 4.0% annually as new state enterprise agreements delivered multiple rounds of increases, with more still scheduled. Healthcare and social assistance wages rose 4.4%, and utilities 4.2%. Private sector wages at 3.4% are not reigniting a broad wage-price spiral, but pockets of 4%-plus growth in service-heavy industries will feed services inflation, which is the hardest component to bring back to target when productivity is weak.

The wage data published earlier in the week reinforced that reading. Australia’s Wage Price Index rose 0.8% in Q4 2025 and 3.4% year-on-year, in line with forecasts on the headline, but with a composition that keeps the RBA wary. Public-sector wages accelerated to 4.0% annually as new state enterprise agreements delivered multiple rounds of increases, with more still scheduled. Healthcare and social assistance wages rose 4.4%, and utilities 4.2%. Private sector wages at 3.4% are not reigniting a broad wage-price spiral, but pockets of 4%-plus growth in service-heavy industries will feed services inflation, which is the hardest component to bring back to target when productivity is weak.

Consumer confidence, meanwhile, is shaky. The ANZ-Roy Morgan index rose just 0.2 points to 77.1 in the week of 9–15 February, a number ANZ described as “very weak.” The four-week average fell to 79.6, its lowest since June 2024. Confidence is down 3.4 points since the February rate hike. Households feel marginally better about recent finances but are materially more nervous about the year ahead: expectations for personal finances over the next 12 months hit a decade low. Inflation expectations ticked up to 5.5%. With the cash rate at 3.85% and another move potentially two months away, the consumer sector will remain under pressure.

The RBA’s own February minutes confirmed the policy framework of “no preset path,” high uncertainty, and an explicit acknowledgement that the late-April quarterly CPI print is the key catalyst for the May meeting decision. If underlying inflation stays above target, and Thursday’s labour market data makes that more, not less, likely, the board has both the mandate and the macro cover to move again. The next RBA meeting is on 1 April; the inflation data drops on 23 April; and May’s decision will be made with full clarity on both.

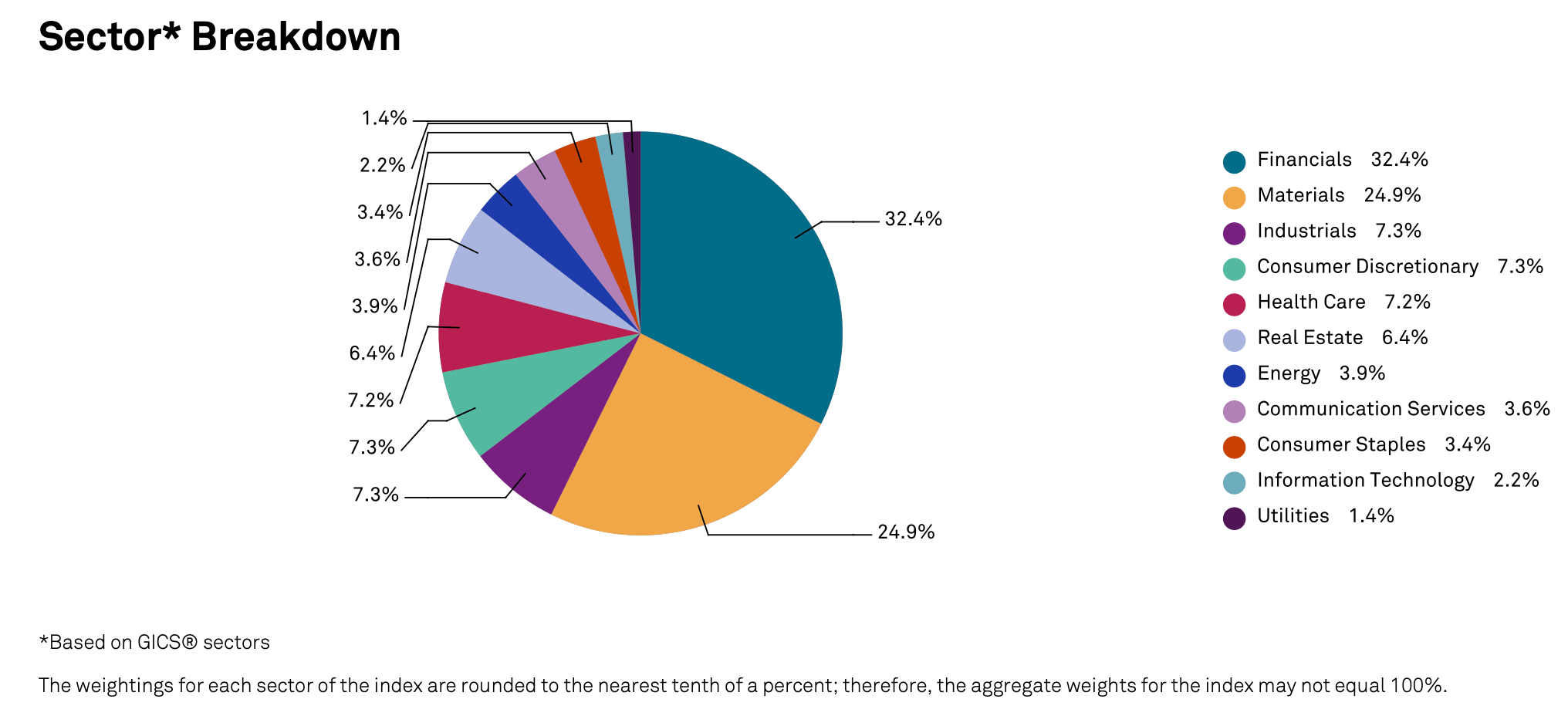

Remember, though, the stock market is not the economy, hence why the ASX200 has returned to its highs. In a special report this week, the research team outlined how the Old School is New Again theme is supporting the local market. The explanation is that miners and banks have been on a tear, extending gains enjoyed in 2025. Energy has also enjoyed firm bids, reversing course from a negative performance in 2025, though the sector does not have a huge influence on the benchmark due to a small 3.9% weighting at the end of January. That is far overshadowed by financials at 32.4% and materials at 24.9%, with the diversified industrials taking the bronze at 7.3%. Tech (just 2.2% weighting) also doesn’t have a big impact on the index, though that won’t make you feel any better if you are holding some of the major steep fallers within the group this year. Healthcare is moderately sized at ~7.2%.

Source: S&P Global

Source: S&P Global

Earnings breadth may be narrow, but earnings momentum is positive, and for the index, the direction and the weighting of those on the rise matter more than diffusion. Rising commodity prices feed directly into Australia’s national income, lifting nominal growth and underpinning fiscal receipts. That, in turn, stabilises confidence even as parts of the growth complex de-rate. Notably, this is an expectations cycle rather than a demand boom. China’s stabilisation, not resurgence, has been enough to trigger upgrades. That tells you positioning was defensive, and pessimism was too high. When revisions flip from negative to positive, liquidity follows. Global macro capital, particularly in a softer US dollar environment, looks for large, liquid exposures to global growth outside the US – Australia’s miners and banks fit the bill.

We continue recommending BHP, Rio Tinto, and selective gold miners, like Northern Star, some copper exposures and others across the metals complex. We also have buy ratings on the banks – see our research portfolio page for the latest updates.

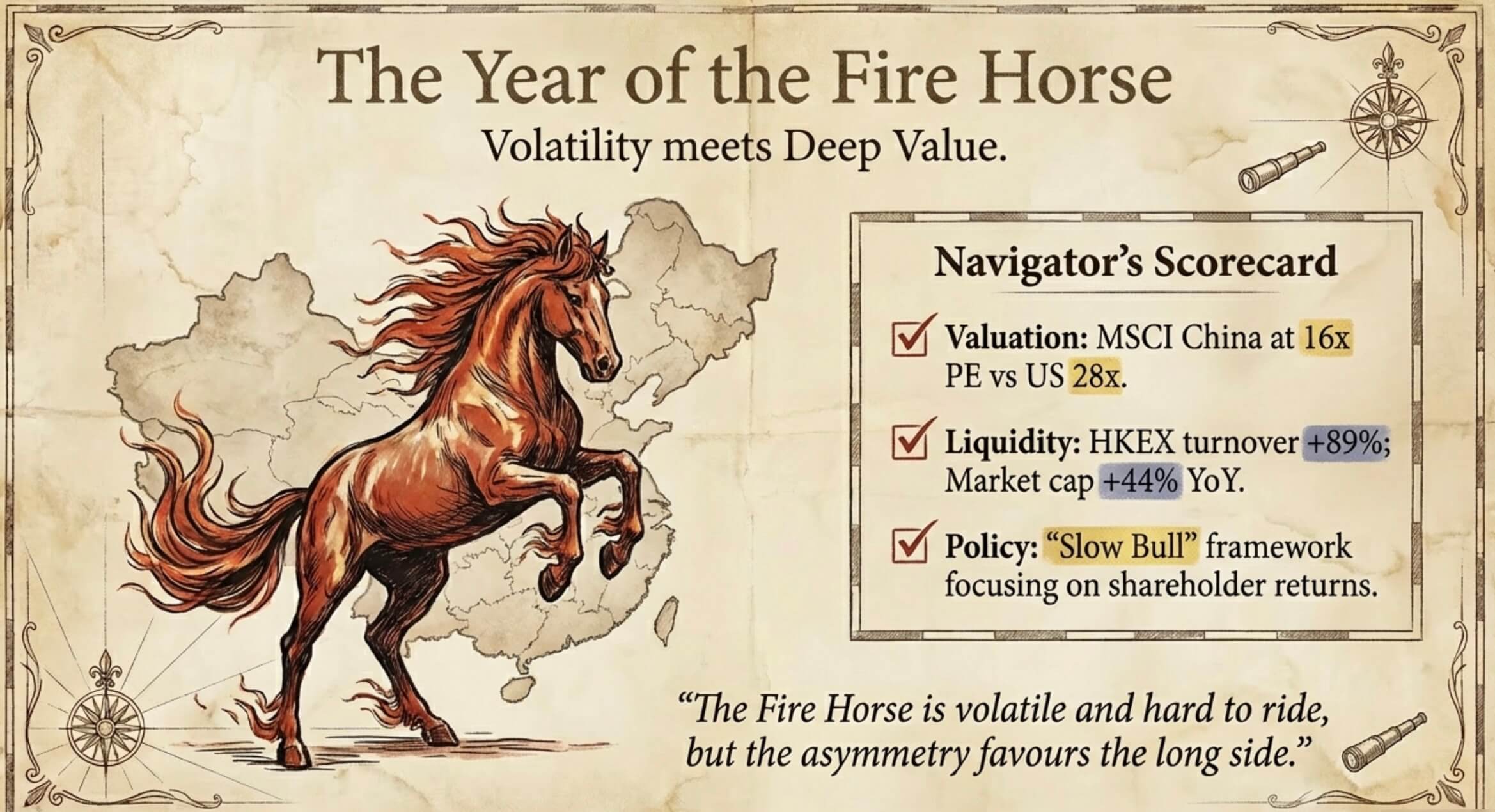

Year of the Fire Horse (2026)

Chinese and Hong Kong markets were quiet this week – by design. The mainland was shut for the Lunar New Year holiday, and Hong Kong saw only thin trade on Monday (+0.5%) before closing its own doors. We remain bullish on the setup for China and Hong Kong equities. The last Fire Horse year was 1966. Sixty years on, the metaphor fits better than most would have predicted twelve months ago.

The valuation case is plain. MSCI China trades at roughly 16x trailing earnings, while the Hang Seng screens at around 14x. Global active fund allocations to China equities sit at roughly 6.8% – this is a market that can re-rate meaningfully on even incremental institutional re-risking.

Earnings are starting to do the heavy lifting. Consensus expects MSCI China earnings growth of around 15% in 2026, with Hang Seng Index EPS growth of approximately 11.7% for the full year. More importantly, the structural drag of persistent share dilution is reversing. Buybacks and dividends are becoming mainstream. Baidu’s US$5 billion buyback authorisation through 2028 and its first-ever dividend in 2026 signal a shift in corporate culture that valuation models have not yet fully captured.

Liquidity is real and accelerating. HKEX market capitalisation hit approximately HK$50.8 trillion, while average daily turnover has also surged to HK$272.3 billion. Stock Connect southbound flows are providing a price anchor for offshore-listed Chinese companies.

Policy is pointed in the right direction. Beijing’s “slow bull” framework, cooling leverage while promoting shareholder returns, is a far more mature posture than the speculative environment that burned investors in 2015. January’s aggregate financing print of RMB 7.22 trillion was materially above expectations.

The dollar story amplifies all of the above. The DXY has broken decisively below multi-year support levels. A weaker dollar is historically inversely correlated with emerging market performance and provides the liquidity lubricant that EM re-ratings typically require. JPMorgan notes EM equities outperformed developed markets by 9% in 2025 and are already ahead again by 5% in USD terms year-to-date. China is its biggest expression.

There are challenges. January CPI came in at just +0.2% YoY with PPI still negative at -1.4%. Manufacturing PMI slipped to 49.3, with new orders below the expansion threshold.

Nevertheless, we see more positives than negatives for Chinese/HK equities in the Year of the Fire Horse. Our’ scorecard’ has four green lights (valuation, earnings, policy, liquidity), two amber (currency, geopolitics), and one red (deflation and private demand). The bull case does not require a macro miracle; it merely requires credit staying constructive. We recommend multiple China/HK exposures across our research offering, including in the tech space, where stocks trade at discounts to many international peers.

The Takaichi Trade

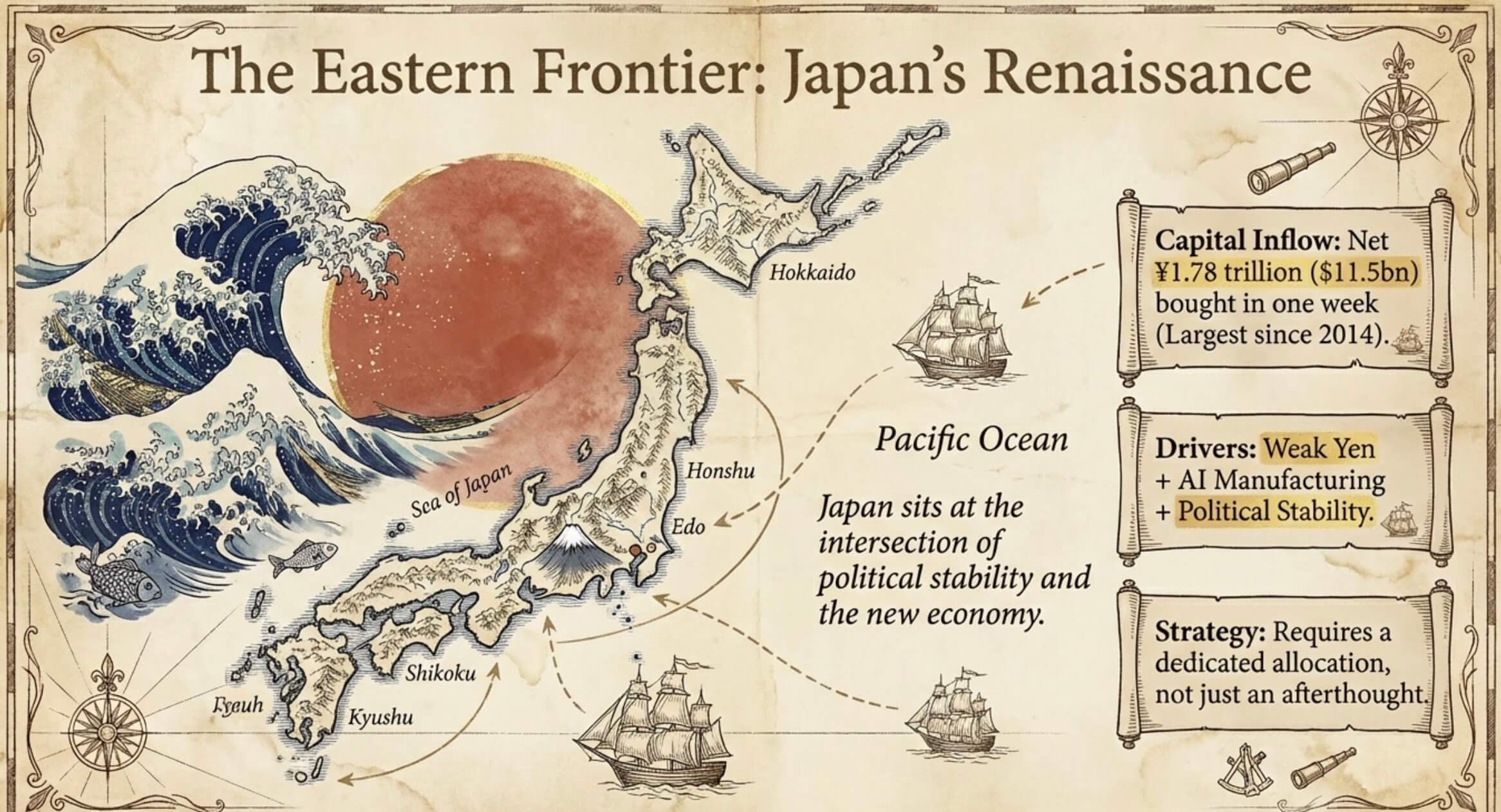

Sometimes even popular victors receive tepid stock-market welcomes. Japan in February 2026 is not one of those occasions. Sanae Takaichi’s Liberal Democratic Party has just delivered one of the most decisive electoral mandates in the country’s post-war history, claiming 316 seats and clearing the 310-seat threshold needed for a supermajority, the largest majority the LDP has won in its 70-year existence. The political uncertainty that has haunted Japanese equities for the better part of three years, a revolving door of prime ministers, a slush-fund scandal, and a coalition that buckled have been swept away. What remains is a clear runway for reflation, corporate reform and strategic investment. The so-called ‘Takaichi trade’ is the latest catalyst in what we believe is a multi-year secular bull market.

The ¥21.3 trillion stimulus package approved in late 2025 is not the sprawling, undifferentiated spending of prior administrations; it is targeted with surgical intent. Of that total, ¥11.7 trillion is directed at household support, underpinning consumption at a moment when real wages are finally turning positive for the first time in decades. The remaining ¥7.2 trillion targets strategic sectors – defence, semiconductors and the emerging category that Takaichi’s team has branded ‘Physical AI’, the intersection of artificial intelligence with robotics and advanced manufacturing. By effectively subsidising corporate capital expenditure in these areas, the administration is engineering a durable expansion in return on equity and return on invested capital across the economy’s most dynamic corners.

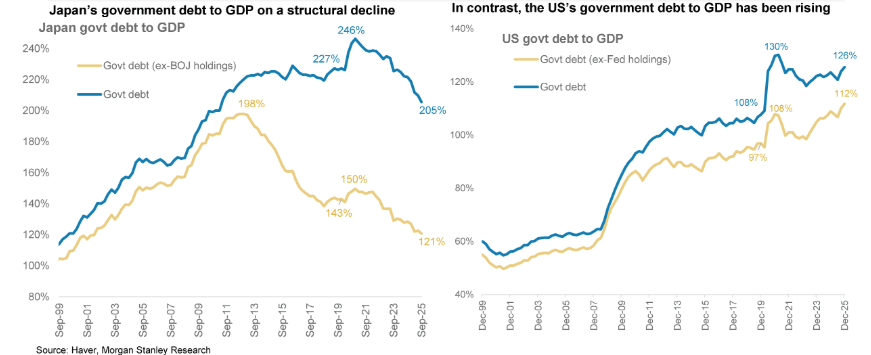

Crucially, this is a growth agenda married to fiscal discipline, not divorced from it. Japan’s fiscal deficit has narrowed to approximately -0.5% of GDP, the healthiest position in close to three decades. Contrast that with the United States, where the federal deficit is running at nearly 6% of GDP, and the conventional narrative that paints Japan as a sovereign debt basket case begins to look not just lazy but frankly backwards. Tax receipts have risen consistently for fifteen years, driven by growing corporate profitability and a return to inflation. The country’s primary budget position has improved meaningfully, placing Japan well ahead of many developed market peers on this metric — a reality that global allocators continue to underweight.

The Denominator Has Finally Arrived

The debt-to-GDP ratio is the perennial bear case on Japan, and it is worth addressing directly. Japan’s gross government debt sits well above 200% of GDP — the highest in the developed world. And yet the trajectory is what matters, not the level. That ratio peaked in 2020 and has been declining. The reason is structural and powerful: for the first time in decades, Japan’s nominal GDP is growing faster than its debt issuance. The ‘denominator effect’ — nominal GDP expanding thanks to inflation and underlying growth — is eroding the ratio from below. Meanwhile, inflation is doing further work: as real debt levels are steadily worn away by rising prices, the burden lightens without a single bond needing to be restructured. The bears have been anchored to a static snapshot of a dynamic system that is now moving firmly in the right direction.

Corporate Japan: From Compliance to Capital Efficiency

The Tokyo Stock Exchange’s governance reforms have now passed through their first phase — the compliance phase, where companies reluctantly acknowledged the need for change — and entered what we would call Capital Efficiency 2.0. The results are visible in the data. Japanese corporates sit on a record ¥115 trillion cash pile, and they are deploying it. Share buybacks hit a record ¥18 trillion in 2024 and were tracking materially higher through 2025; final figures, when released, are expected to confirm another record. Management buyouts, strategic divestments and cross-holding unwinds are accelerating, each one surfacing hidden value that has been trapped on balance sheets for a generation. Return on equity is rising. Earnings revisions are trending positively, a fundamental signal that the Japanese corporate machine is gaining traction relative to many international peers. Meanwhile, valuations are still very reasonable.

The Bank of Japan raised interest rates twice in 2025, the first meaningful policy tightening in roughly thirty years. Yield curve steepening and higher JGB yields have prompted some anxiety. We view this differently. A country purging three decades of deflation will, by definition, see its bond yields rise. The wage-price dynamic that policymakers have sought for a generation is now in place: real wages are positive, companies have the pricing power to expand margins even as the cost of capital normalises, and the BoJ has room to continue its gradual tightening path without derailing the expansion. Critically, Takaichi has struck the right tone with the central bank, resisting the temptation to lean on the BoJ publicly and instead asking only for clear communication and policy coordination. That restraint, given the size of her mandate, is itself a signal of a mature administration that understands the stakes.

The Takeaway

Japan is, in our view, in the early innings of a secular bull market. The structural tailwinds – an end to deflation, corporate governance reform, a government with both the mandate and the fiscal room to invest, and a central bank carefully normalising rather than slamming the brakes – are aligned in a way that has not been true for three decades. The Takaichi supermajority removes the last major source of near-term political uncertainty. What remains is a market trading at a meaningful discount to its global peers, with positive earnings revisions, record capital returns and a reform agenda that is structurally rewriting the return profile of corporate Japan. The Nikkei’s journey higher is a rational re-rating in progress. We are overweight and recommend a range of exposures in our research services.

THE WEEK AHEAD

China’s market will reopen early next week.

US PCE data is due on Friday morning US time and is the Fed’s preferred inflation measure. A print above 2.7% year-on-year would revive the FOMC’s “several officials considered rate hikes” language into a live discussion, pushing the 10-year higher and pressuring AUD/USD. A soft print confirms the easing path and would give ASX rate-sensitive sectors some relief.

ASX earnings continue into their final major week.

Report Spotlight

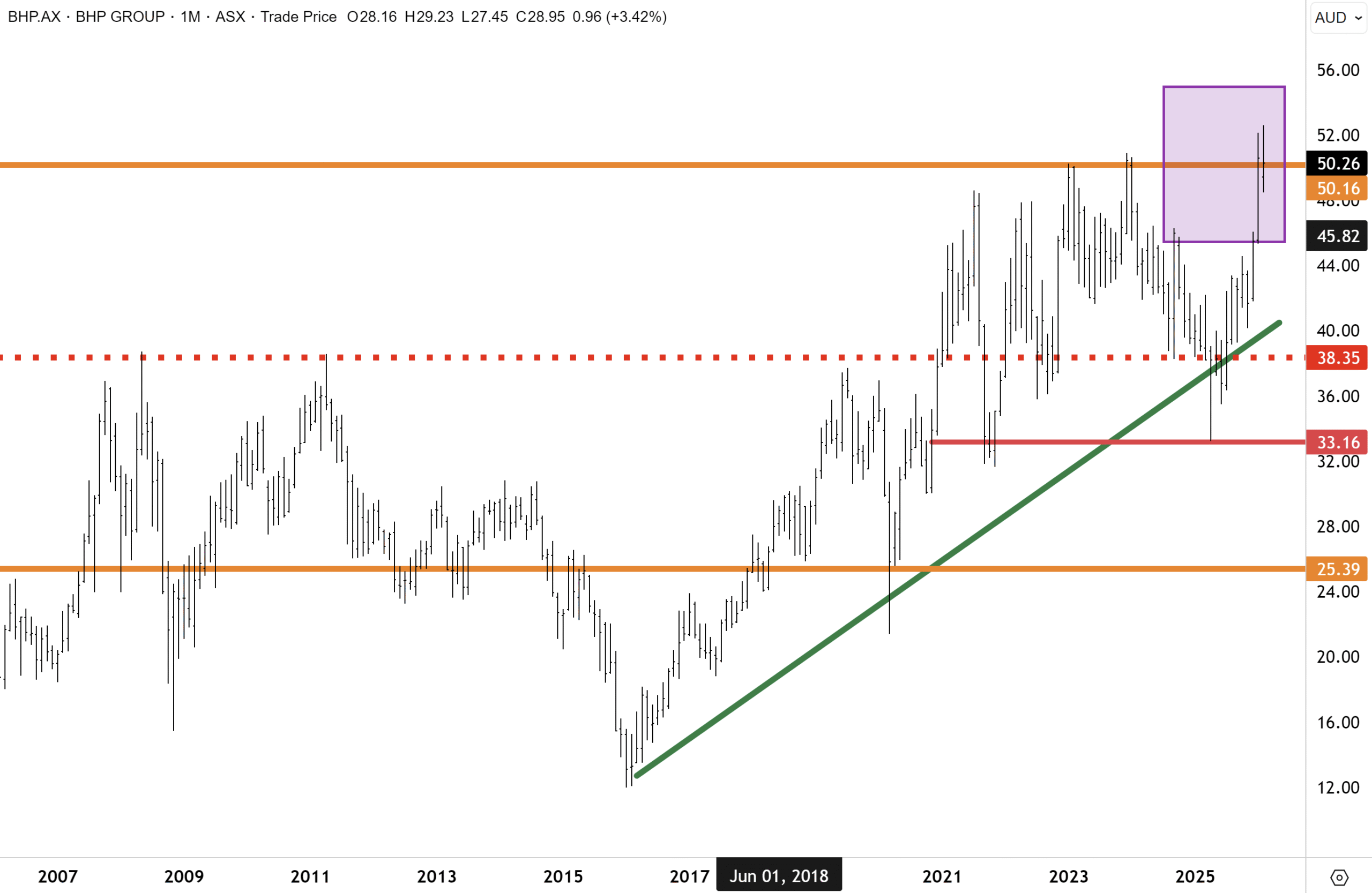

BHP’s HY26 result was a clean beat across the board, with revenue up 11% to US$27.9bn and Underlying EBITDA surging 25% to US$15.46bn. The headline story is the earnings mix shift. Copper now contributes 51% of group EBITDA for the first time, officially displacing iron ore as the primary earnings engine. Realised copper prices jumped 32% to US$5.28/lb, driving a 59% lift in copper EBITDA to US$8bn, while unit costs fell sharply at both Escondida and Copper South Australia. Iron ore remains a formidable cash generator – WAIO produced a 43% ROCE – funding growth across the portfolio.

BHP has sequentially respected the primary uptrend in place since the 2016 lows, with one breach occurring last April during the Liberation Day selloff. We highlighted last year that we viewed the selloff in BHP as climactic. We remain of the view that the path of least resistance for BHP lies firmly on the topside.

The 44% dividend hike to US$0.73/share (fully franked) smashed expectations, and the US$4.3bn Wheaton silver streaming deal adds near-term balance sheet firepower as part of a broader US$10bn capital recycling program. Copper production guidance was lifted for FY26, with a clear multi-year growth runway targeting 3-4% CuEq CAGR to FY35 via Escondida, Copper SA, Resolution and the Vicuna JV with Lundin. Coal remains immaterial to the thesis. We rate BHP a BUY.

This report and many others spanning Australasia, Mining and Global Equities are available online for your reading pleasure in the Members area, should you be interested in subscribing for investment snapshots and deep dives across a range of investment vectors, along with our regular Daily correspondence on the markets.

Have a great weekend

Carpe Diem

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.