KEY CONTENT

- Thursday delivered the paradox that often defines a market turning point: Elevated fear and signs of a credible off-ramp arrived in the same session.

- This correction represents a bull market reset, not Armageddon: The White House has strong political incentives to deliver a short war ahead of the November midterms.

- Hedge fund short exposure in S&P 500 futures and ETFs is at a five-year extreme, setting up a powerful short-covering rally when the off-ramp arrives.

- Gold’s -9.2% single-session collapse in the All Ords Gold index has the hallmarks of capitulation selling, not fundamental impairment.

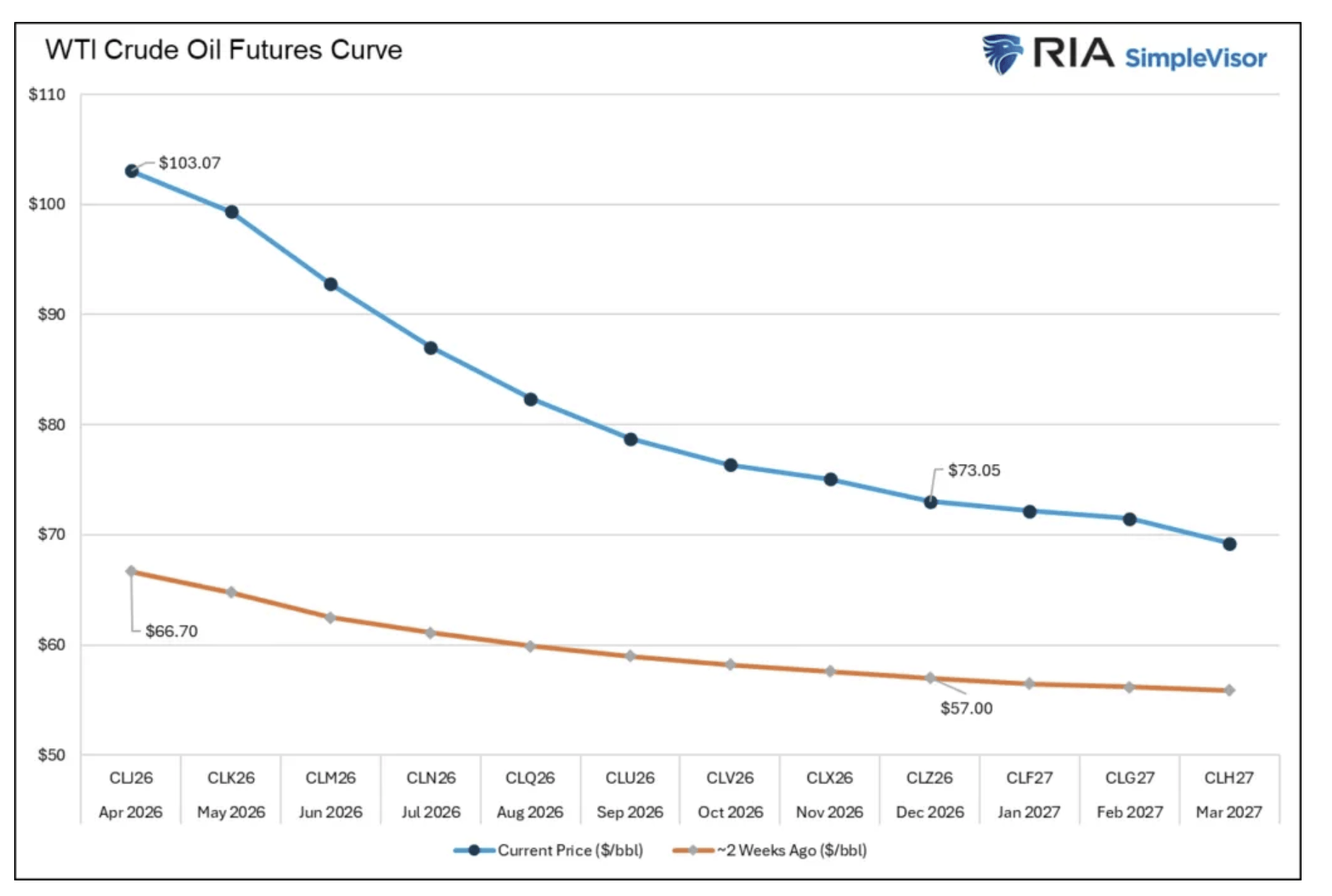

- Oil futures are in backwardation across the full NYMEX strip. The market’s own verdict is that today’s shock is temporary, and this is mirrored in the US bond market.

- The RBA’s 5-4 vote and Australia’s 4.3% unemployment surprise create a genuine policy dilemma. We discuss.

- Software stocks are approaching a floor: Deutsche Bank upgraded to overweight. We have topped up some positions.

REPORT SPOTLIGHT

- Woodside Energy (ASX: WDS) – Record 2025 output of 198.8 MMboe. Scarborough targeting first gas Q4 2026, Louisiana LNG reaffirmed under new CEO Liz Westcott. Primary beneficiary of the structural LNG repricing. HOLD

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join today.

Last Week in a Nutshell – Not Armageddon

Last week delivered the paradox that often defines a market turning point. Elevated fear and the first credible off-ramp arrived in the same session. Gold fell 5% to $4,660 on Thursday, while in Australia, the All Ords Gold index cratered -9.2%, Iranian attacks reportedly knocked out 17% of Qatar’s LNG export capacity and yet the S&P 500 closed down just 0.27%, the bond market held in well, and the US dollar cracked nearly 1%. This combination doesn’t typically occur in a world where the inflation shock is long-lived, and the bears are correct.

Goldman Sachs documented hedge fund short exposure at a five-year extreme. Morgan Stanley’s Mike Wilson told investors to prepare their shopping lists. The Economist ran its bearish cover. The Business Week “Death of Equities”. The relevance? The parallel is another was issued in August 1979, weeks before a decade-long bull market began. The RBA hiked to 4.10% in a 5-4 vote in a labour market that delivered a surprise 4.3% unemployment rate on the same day the gold miners were being liquidated. The correction that began in technology stocks in late 2025, extended through AI disruption fears, and reached a geopolitical crescendo with oil above $100 and the Strait of Hormuz closed, has induced a correction. Critically, in our view, this represents a correction in an ongoing bull market. Not Armageddon as the business press makes out. The candle is burning for the White House and shifts in tactical direction could be imminent.

Deeper Dive

Cash has been raised at the margin, and hedge funds have de-leveraged, with downside protection being bought on a record scale on fears around the ME and oil prices spiralling out of control. History has taught us that these conditions and reaction functions are often a precursor for a powerful counter-trend rally. In terms of the current market setup, sequentially, an upside surprise with a resolution to the war could drive a “short covering”.

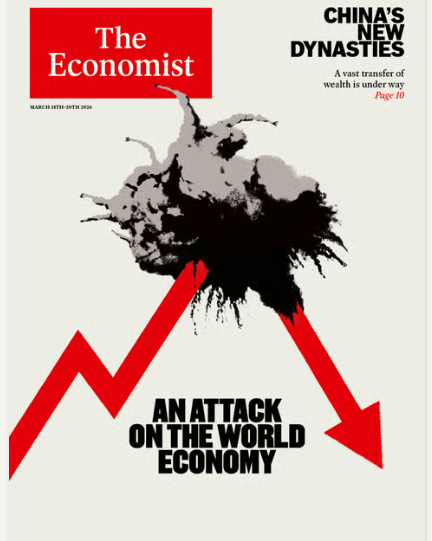

US strategist Ed Yardeni made an interesting point this week and highlighted the “The Economist” magazine cover as a good historical contrarian sign. The cover story featured “An Attack on the World Economy”. Ed noted that a bearish cover story is a very bullish signal for markets, and he has a good point.

Business Week magazine became infamous for publishing a cover in late 1979 claiming the “death of equities”. Not long after, global stock markets bottomed out, and then a powerful bull market ensued that ran for a decade. Popular business magazine covers often coincide with important market bottoms and tops.

I concur with Yardeni on this front, and we have been consistent in recent weeks in highlighting that market internals and the overall response mechanism in financial markets have been broadly constructive despite poor sentiment and significant cashing up by global investors. This price action could point to a “bullish resolution” possibly coming in financial markets despite all the bad headlines, widespread fear amongst professional investors and negative sentiment.

Last year, we saw the S&P500 plunge sharply after Liberation Day tariffs were announced on 2nd April 2025, hedge funds, financial institutions and professional investors put on a record amount of shorts. Downside protection was sought against the consensus bearish view at the time that tariffs could plunge the global economy into recession and ignite a trade war. What happened after Liberation Day was the opposite, as the market was “wrong-footed” and DJT dialled back the tariffs a week later. The market exploded higher on a short-covering rally and did not look back for the rest of the year. Financial markets today have a similar setup in my view.

When positioning becomes too skewed in a certain direction, the opposite can happen, especially if there is a ‘surprise’ event that catches the consensus off guard. According to Goldman Sachs, hedge funds have put on shorts at one of the fastest rates on record, lifting short exposure in Macro Products (SPX Index + ETF combined) to the highest level since Sep 2022. The investment bank trading desk believes that this is potentially priming the market for an “explosive short squeeze”.

Shorting of S&P500 futures along with ETFs is approaching the highest levels in five years.

The path of least resistance for the stock market lies on the topside in my view, with positioning extreme on the short side, cash now amassed on the sidelines, and many investors ready for the worst-case scenario of stagflation, recession, and possible systemic risk to the financial system from private credit. However, we are not seeing this in terms of market internals. The VIX has failed to rise above 35, and is well down in previous selloff highs, including the Yen carry trade unwind in 2024, Liberation Day tariffs last year, and the pandemic in 2020. This is surprising given that the global appetite has soared for downside protection as most investors have headed towards the sidelines.

Morgan Stanley’s CIO and Chief US strategist, Mike Wilson, was out with a note this week and highlighted a similar view that the incumbent correction in stocks “is closer to its ending stages in time and price” and that buyers should get ready with their ‘shopping lists.’ Mr Wilson didn’t go near politics or the ME but believes that most military conflicts tend to have only a short-term impact on markets. I agree.

Mr Wilson noted that “this correction is mature in time and price” and that with earnings acceleration continuing, the current set-up looks very different from prior late-cycle periods when an oil spike ended the business cycle. He concludes that investors should get their shopping lists ready and that the incumbent capitulation or drawdown will not be as bad as last year. “Market lows happen faster than tops, so be ready to add risk in anticipation of the bull market resuming”.

We are on the same page. I maintain our view that a pivot is coming, with high oil prices and financial markets instability (not to mention rising bond yields), all incongruent with winning elections at home. With positioning to the bearish side now extreme, a counter-trend rally in financial markets will no doubt surprise many once again, when it finally arrives.

Mid-term elections sit on the November horizon. The White House needs lower oil prices, lower rates, and a US housing market that is moving again. All three objectives are in direct conflict with oil above $100 and a Fed unable to cut in the near-term. I believe this weekend, if not today, will prove pivotal. However, the financial markets will need to know Tehran’s position and will be led by the oil price. The proof, as always, will be in the pudding, and this time around, the markets will not focus on a few politicians.

I believe the financial markets are approaching the very end of a corrective drawdown that began late last year and originated with the selloff in technology stocks. The selloff in precious metals on Thursday is likely the climactic final chapter. The weekend might be revealing in terms of a US/Israel pivot…

In Australia, the All Ords Gold index fell -9.2% in a single session. Northern Star lost -9.5%, Evolution Mining -9.6%, Westgold -12.8%, Ramelius -10.6%. Multiple others were in a similar boat. The move had the signature of forced and capitulation selling rather than fundamental reassessment, the kind of indiscriminate liquidation that occurs when a leveraged long meets a broken technical level. I see this as the final stages of a global correction in risk assets, which is close to conclusion.

Energy Markets

Iranian attacks reportedly struck the world’s largest LNG export plant on Wednesday, and by Thursday had knocked out an estimated 17% of Qatar’s LNG export capacity. Woodside Energy surged +7.2% on Thursday to its highest level in more than two years. Santos added +3.2%. Thermal coal names caught the same bid – Yancoal +6.8%, New Hope +5.3%, Whitehaven +2.3% – as the gas supply shock supported substitute fuel prices across the complex.

The distinction between this development and the broader oil shock matters. The Strait of Hormuz disruption is a transport route problem – it resolves when the Strait reopens. The Qatar infrastructure attack is a production problem. LNG export facilities take months to repair at full capacity, supply agreements cannot be rerouted overnight, and the political consequences are significant. Iran has pulled a big lever here.

On the other hand, the oil market is a different beast, and again, is telling a different story to the financial media – one that is significantly more positive for risk assets. WTI is in backwardation across essentially the whole visible NYMEX strip right now, with each successive month trading lower than the nearby spot market. The drop-off in future oil prices becomes more pronounced in late 2026 and beyond. One recent estimate has April 2026 WTI around the high‑80s to low‑90s per barrel, versus December 2026 being in the high‑60s, implying around USD 20/bbl of backwardation over eight months.

The RBA delivered a 25bps hike to 4.10% on Tuesday in a 5-4 vote, the narrowest split since the board began publicly disclosing tallies last July. Governor Bullock was clear: domestic inflation, running at 3.4% annually and forecast to reach 4.2% by mid-year, was the trigger. Not the Middle East, but this will be an overhang if the conflict extends. The four dissenters preferred to wait until May, when a full March-quarter inflation report would be available. The market read the near-split as slightly dovish, and the ASX closed higher on the day, with May hike probability retreating toward 50%.

Then Thursday delivered a number that changes the May calculus in both directions. Australia’s unemployment rate rose to 4.3%, a three-month high that surprised most economists given the pace of government hiring. A single data point, but a directional one. If unemployment pushes toward 4.5% over the coming months, the RBA faces a genuine policy dilemma – hiking into a deteriorating labour market with an oil shock compressing household discretionary spending simultaneously. The four dissenters were not wrong to wait. They may prove to have been early.

The domestic banks are the instrument through which this story is most directly expressed. Westpac CEO Anthony Miller’s assessment – that two hikes would recreate roughly the conditions households navigated without systemic distress a year ago – is the bull case. The banks held ground on Thursday when most stocks were being sold: financials fell just -0.5%. That relative resilience, into a week containing a rate hike and a gold capitulation, is the data point that matters. One variable the market is still under-pricing in our view. Kevin Warsh replaces Jerome Powell in approximately eight weeks. Warsh is expected to lean dovish, and Morgan Stanley maintains a call for two cuts this year, a timeline that could be rapidly repriced back into the consensus should the energy shock fade, as we expect, and a new chair takes the podium. We have buys on NAB, WBC and ANZ.

The Software Floor?

I believe that technology stocks are approaching an important bottom after the big selloff this year, amidst AI disruption and displacement fears. The decision by Meta Platforms to use AI technology and reduce its labour force by 20% is perhaps revealing in that other companies will follow suit. Longer term, this could be detrimental and induce rising white collar unemployment, but for now, investors will focus on rising margins, revenues and earnings.

Deutsche Bank concurs with this outlook and noted this week that “reality doesn’t align with investors’ fears that AI will eat software.” DB issued a bullish call on software stocks last Wednesday after weeks of worry that AI will drive a shakeout in the corner of the tech sector. The bank believes that investors are undervaluing top software stocks, which I also agree with.

DB noted that “software companies are trading at historically low premiums versus the market. Despite valuations signalling that the sector will underperform the broader market, the reality is different. Facts are telling a different story, and fears around AI have peaked.” The bank boosted its outlook for the sector and is now “overweight” software stocks and neutral on tech, an upgrade from the “underweight” rating they previously had for the sector.

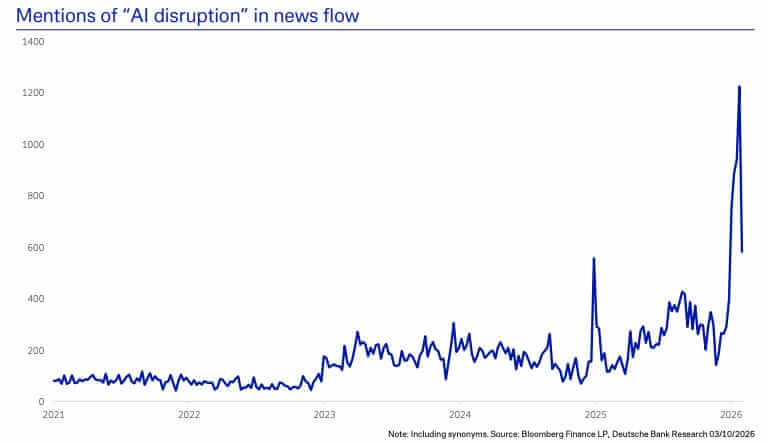

Deutsche Bank highlighted that AI disruption mentions have plunged from the dramatic spike seen earlier in the year. This points to a potential bottom now being reached for software companies.

I agree with DB’s outlook for software stocks and technology companies that have been hammered this year on AI disruption fears. The selloff looks not only overdone, but now complete with valuations sharply lower – and earnings for most incumbents still growing strongly. I would also argue that opportunities are equally promising for major tech companies outside the US. As mentioned above, and as disclosed to the ASX, we have added exposure to core IT and tech companies in China and Asia in recent weeks.

Alibaba’s quarterly result arrived during Thursday’s risk-off session and was sold on the headline, with net profit down -67%, below estimates. However, as we have written about previously, Alibaba is evolving into a full-stack AI player. Cloud Intelligence Group revenue grew +36% and AI-related products delivered triple-digit growth for the tenth consecutive quarter. CEO Eddie Wu put a five-year target on the table. A combined external cloud and AI revenue exceeding $100 billion. Alibaba’s T-Head semiconductor business, producing chips at scale and narrowing the gap with overseas alternatives, adds a strategic dimension that the profit miss entirely obscures. The valuation discount to American peers remains wide.

Record 2025 output of 198.8 MMboe and a solid growth pipeline – Scarborough targeting first gas by 4Q26, Trion drilling underway, Louisiana LNG reaffirmed – make Woodside a compelling LNG proxy. The Iran conflict has been a tailwind, lifting the stock to two-year highs near $32. New permanent CEO Liz Westcott signals continuity over disruption, with her operations-heavy background reducing execution risk on key projects. The market took the appointment calmly. On a near-term basis, Woodside looks overbought with overhead resistance likely to emerge above $32. A correction in WDS could ensue if oil prices correct from current levels, and there is some form of resolution to the conflict in the ME (our base case). In the event of a correction playing out, we believe Woodside would attract support below $30 and would wait for a better technical buying opportunity to play out over the coming months. We hold Woodside Energy across our Australian-managed account portfolios. We move Woodside to a HOLD at current levels.

This report and many others spanning Australasia, Mining and Global Equities are available online for your reading pleasure in the Members area, should you be interested in subscribing for investment snapshots and deep dives across a range of investment vectors, along with our regular Daily correspondence on the markets.

Have a great weekend.

Carpe Diem

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.