This Weekly Wrap Lite is our end-of-week synthesis of what actually mattered in markets. We connect the biggest macro, policy and geopolitical catalysts to what moved across rates, currencies, commodities and equities. We also pressure-test our conclusions against a small set of high-signal thinkers, not to outsource judgment, but to sharpen it. We finish with a focused set of actionable ideas across stocks, ETFs and commodities; members receive the expanded shelf and deeper setups.

Week-to-date snapshot

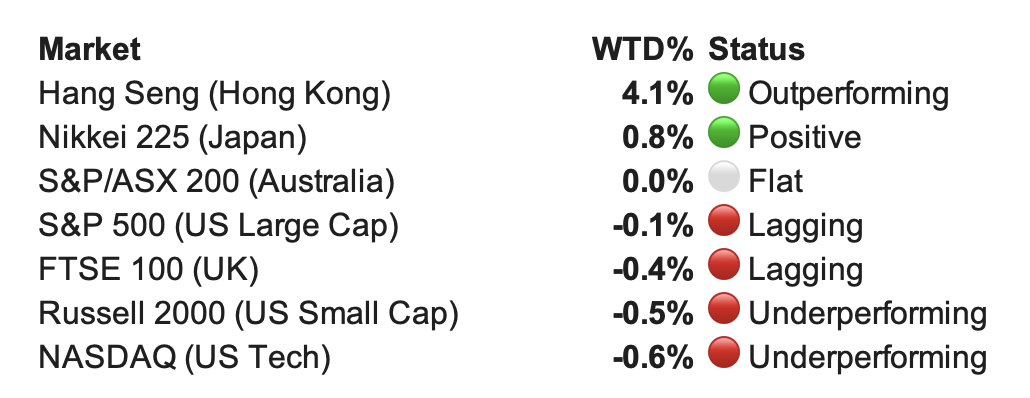

At the time of writing (Friday morning), a sharp East-West divergence had unfolded over the week-to-date. Hong Kong’s Hang Seng dominated the leaderboard with a +4.06% surge, while US Tech (NASDAQ -0.6%) served as the primary drag on global sentiment, finishing at the bottom of the pile, and the ASX200 was flattish after some modest ups and downs.

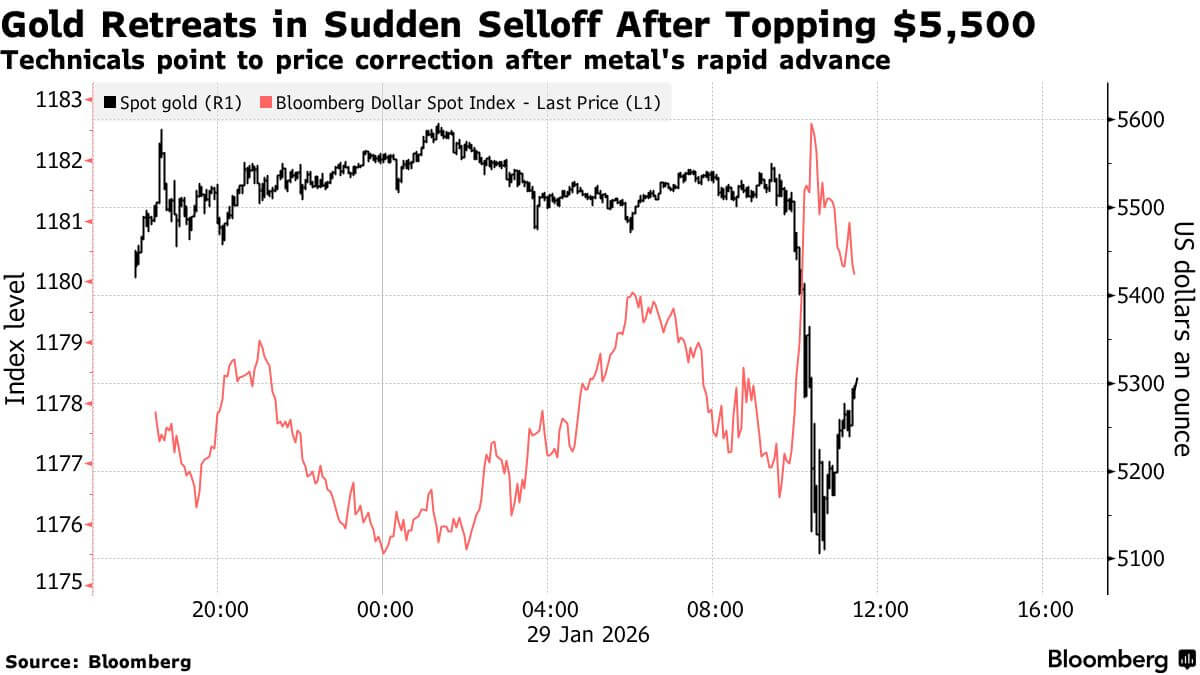

Cracks in the USD widened this week, gold blasted higher, with futures briefly hitting a stunning US$5,600/oz on Thursday during US trading, and the Treasury curve steepened to its widest since 2021. President Trump helped trigger the USD selloff himself, publicly cheering dollar weakness (“I think it’s great”) while his Treasury Secretary scrambled to reaffirm “strong dollar policy” to little effect. Markets weren’t buying it.

The Treasury curve steepening is a credibility tax. Bond vigilantes are demanding higher compensation to hold long-duration US debt. Central banks already have the memo and continue to accumulate gold. That trend broadened to a wide swathe of investors in 2025 and is reaching a crescendo in early 2026, with our gold price target for the year already taken out! Goldman Sachs lifted their price target, and we can expect plenty more investment banks to follow suit. While we remain bullish on the precious metals, after they have gone near vertical recently, we now urge caution and not to chase exposures here.

Policy divergence is sharpening. The Fed held at 3.50-3.75% with two dissenters favouring cuts, while markets price only 30% odds of easing before June. The Bank of Japan last Friday held at 0.75% but signalled hikes if yen weakness persists. Australia shocked with 3.6% inflation, pushing markets to price 60-70% odds of an early February hike to 3.85%. The A$ has surged above 70c against the greenback. Meanwhile, EUR/USD broke above 1.20 for the first time since June 2021.

A Great Repricing appears to be picking up pace. We foresee a structural realignment of global capital necessitated by the fracturing of the US Dollar. After decades of greenback dominance, a “debasement narrative” has finally taken hold, fuelled by aggressive Treasury selling from global central banks and a White House that is increasingly comfortable with a weaker currency and wants the Fed to push interest rates lower.

Deconstructing the Great Repricing/Rotation

Now, we dig into the details of the fundamental shifts that gathered pace this week and the profound investment implications they carry for the year ahead. As the greenback’s dominance recedes, it is acting as a “release valve,” reweighting the global financial architecture toward hard assets and deeply undervalued international risk. From the parabolic “moonshots” in gold and silver to the mounting “AI impatience” on Wall Street, the following analysis breaks down the mechanics of this transition, along with some risks and opportunities.

The dollar’s slump this month in the face of relatively steady performances in US stock and bond markets points to global investors raising hedges against a weaker greenback – rather than dumping US assets. Global funds have around 50% of portfolios allocated to the US, which in turn dominates global equity market capitalisation, which is also nudging 70%. I have maintained for some time that US equities are relatively expensive compared to the rest of the world, given that US GDP is about 28% of global GDP. International and emerging equity markets are cheap, given the RoW share of global GDP outside the US is around 72%. Equities ex US account for c30% of the global market cap.

I believe the downward move in the US dollar could prove influential and change global portfolio settings. Emerging and developed equity markets, which have much lower valuations, could benefit if global capital flows divert away from the US and international shares. A lower US dollar is typically inversely correlated with both EMs and DMs and provides liquidity. We saw this cycle playout dynamically between 2000 and 2013 when the DXY lost around 40%, and I have conviction this cycle will repeat over the coming years. We have positioned accordingly for this cycle in our Asia and Global managed account portfolios – and the Fat Prophets Global Contrarian fund (reach out to patrick.ganley@fatprophets.com.au for more information).

The greenback is sequentially on track for its worst month since June last year and has had one of the worst starts to the year in decades. I maintain a bearish outlook for the greenback this year and believe that the overallocation of international investors will exacerbate further hedging as portfolio managers have to confront the fact that a falling dollar will erode returns and US asset values, which, on average, account for 70% of respective portfolios.

The greenback is sequentially on track for its worst month since June last year and has had one of the worst starts to the year in decades. I maintain a bearish outlook for the greenback this year and believe that the overallocation of international investors will exacerbate further hedging as portfolio managers have to confront the fact that a falling dollar will erode returns and US asset values, which, on average, account for 70% of respective portfolios.

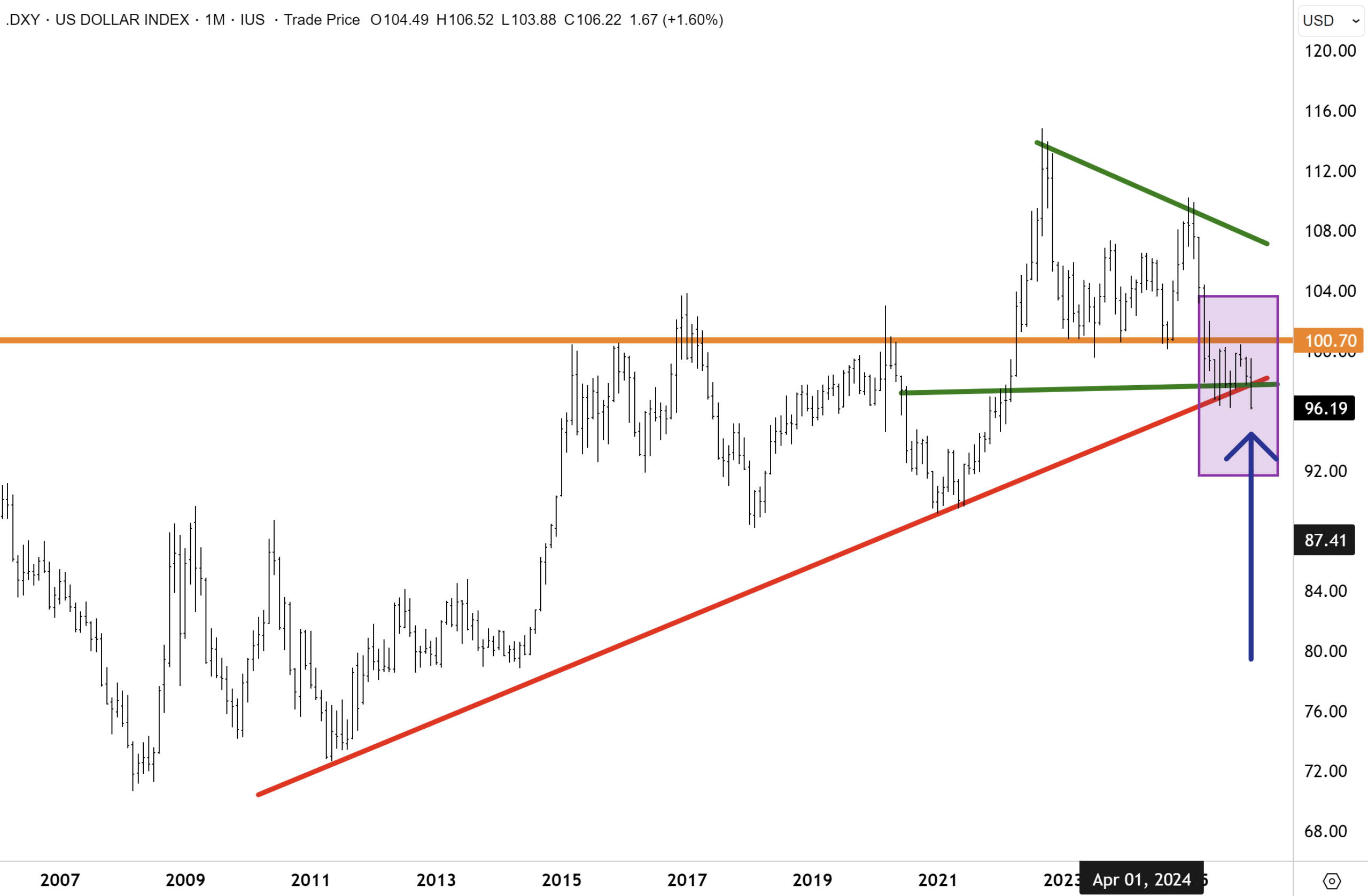

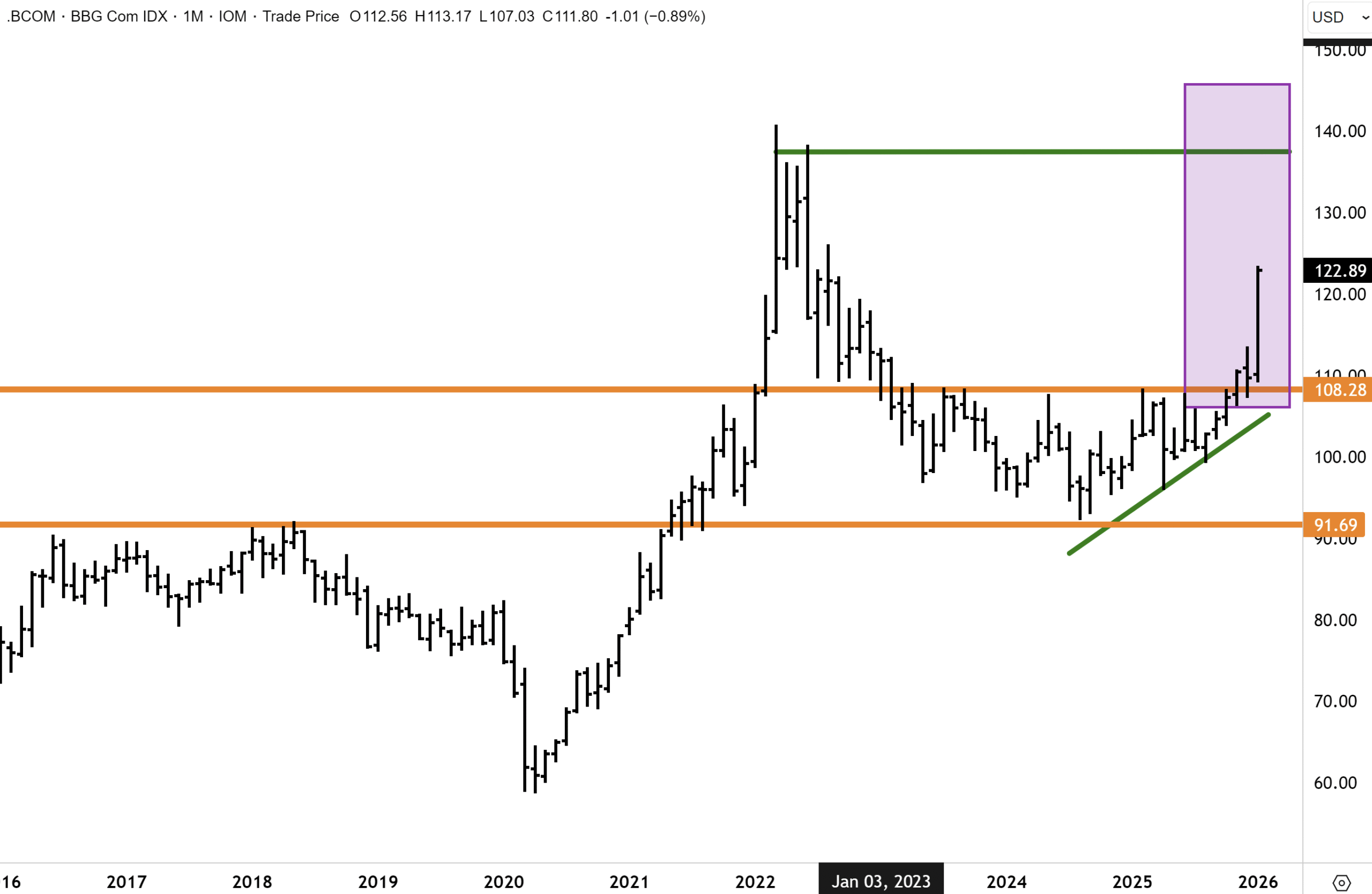

On the 20-year monthly chart below from earlier in the week, the DXY broke below the primary uptrend that has been in place since the last dollar bear market ended in 2009. After churning sideways within a range, the DXY has finally conceded with a breakdown below the bottom end of the six-month range, traced out between July ’25 and January this year. A sustained downside move below the primary uptrend would confirm a “break” in the dollar and point to rising technical risks of further downside this year (our base case).

![]()

For now, most fund managers and global investors are choosing to hold US financial assets and hedge out FX risks. This is to be expected given that the S&P500 has strongly outperformed international and emerging markets since around 2011, which marked the bottom of the last US dollar cycle. However, at some point, selling pressure by global investors could intensify, especially if emerging markets put in another strong year of outperformance similar to 2025. On this front, I expect global portfolio rebalancing into other markets to be another trend that will emerge this year.

Morgan Stanley’s Mike Wilson made some comments on the dollar’s recent weakness, noting that the “US Dollar Index is down more than 10% on a year-over-year basis, nearing a 5-year low in rate of change terms. As was the case last year, this is ultimately a positive tailwind for US earnings revisions — our work shows rate of change on the DXY leads US earnings revisions by 3 months.”

This is a good point, and US multinationals stand to benefit significantly from a falling dollar, which provides a powerful tailwind for earnings and revenues on accounting translation. I would also add that mega-cap tech stocks such as Apple, Amazon, Microsoft, Alphabet and Meta will also benefit significantly. Wall Street was blindsided by the dollar’s decline last year, which caught most of the investment banks off guard.

With most investment banks more optimistic on the outlook for the dollar in 2026, Mike Wilson makes a very pertinent point that a weaker greenback could drive another round of earnings revision upgrades. Investment banks and broker are could lower their outlook for the dollar over the coming quarters, and lift forecasts for S&P500 companies. I don’t think this is “in the price”. The bottom line, is we took a bullish stance on US, international and emerging market equities this year. A weaker US dollar is going to be inevitably bullish for financial markets.

Speaking on CNBC this week, hedge fund manager and billionaire Jeff Gundlach also outlined that his central investment theme was that the US dollar is going to be secularly weak in the coming years and will inevitably lead to fears around the US debt profile and the ability of the government to service its debt. More about some of Mr Gundlach’s other views later.

The outlook for global investment in the US was a hot topic last year after Trump’s announcement of sweeping tariffs in April sparked a rout in American assets and the sharpest first-half selloff for the dollar since the 1970s. This trend could continue this year, which has been our base case for some time now.

However, an outlier scenario could playout where the dollar’s decline accelerates, raising deeper questions about the longer-term value of the world’s primary reserve currency. I believe these forces are now already at work and influencing deeper capital flows. At some point, the dollar’s role as reserve currency is going to be questioned – and many of the US government’s foreign policies are contributing to and driving global scepticism.

On this front, Britain and China this week hailed a “reset in ties” with PM Starmer seeking a ‘sophisticated’ relationship. This political development would have been unthinkable a few years ago. Mr Starmer is the first British PM to visit China since 2018, and after meeting with President Xi, both countries have pledged greater cooperation on trade, investment and technology to the mutual benefit of both countries.

This outcome is to be expected. Western and European leaders have been left reeling from the total unpredictability of DJT’s policies and leadership style. This is not a criticism – but an observation – which is now playing out in financial markets, capital flows, and global politics. UK PM Starmer became just the latest leader to head to China, where the RoW has been frenetically working together to improve market access, lower tariffs, and boost investment deals now that DJT has effectively put every country on notice.

Meanwhile, President Xi said China was ready to develop a long-term partnership with Britain following “twists and turns” in the relationship that did not serve the interests of either country. “We can deliver a result that can withstand the test of history.” More countries are being pushed towards China for economic reasons. These trade deals with China could establish a new “trade bloc”, which will almost certainly see a significant shift away from the US dollar.

The bottom line is that should the dollar head lower this year, emerging markets will be a significant beneficiary. On this front, JP Morgan strategists noted this week that “emerging market equities had a good run last year, up 31%, beating developed markets by 9%, and are so far in 2026 ahead again, by 5% in USD terms.” This outperformance will continue this year in my view.

The Geographic Rotation

JPM is optimistic about emerging markets for a number of reasons. Firstly, the bank noted that “while many central banks are nearing the end of easing, we do not expect widespread tightening anytime soon, and 14 out of 23 emerging market central banks are still expected to make additional cuts from here.” JPM also said that their bearish USD outlook remains important for the emerging markets call, and with China’s domestic economy remaining subdued for a long while, “any improvement on this front, or a more forceful stimulus rollout, would be a positive surprise”. I believe the Chinese authorities will surprise on the stimulus front this year and move decisively to address the stagnant property market, amongst other initiatives.

And on valuation, emerging markets and China have a big advantage. JPM cited that EM equity valuations continue to screen very attractive vs developed markets, at 14x forward P/E vs 20x. Investor positioning in emerging market equities remains rather low, and inflows (into EM equities) have seen a strong start to the year. After years of having a cautious stance on emerging markets, we turned bullish (on EM vs DM) last year and believe that 2026 will be another year of EM outperformance.”

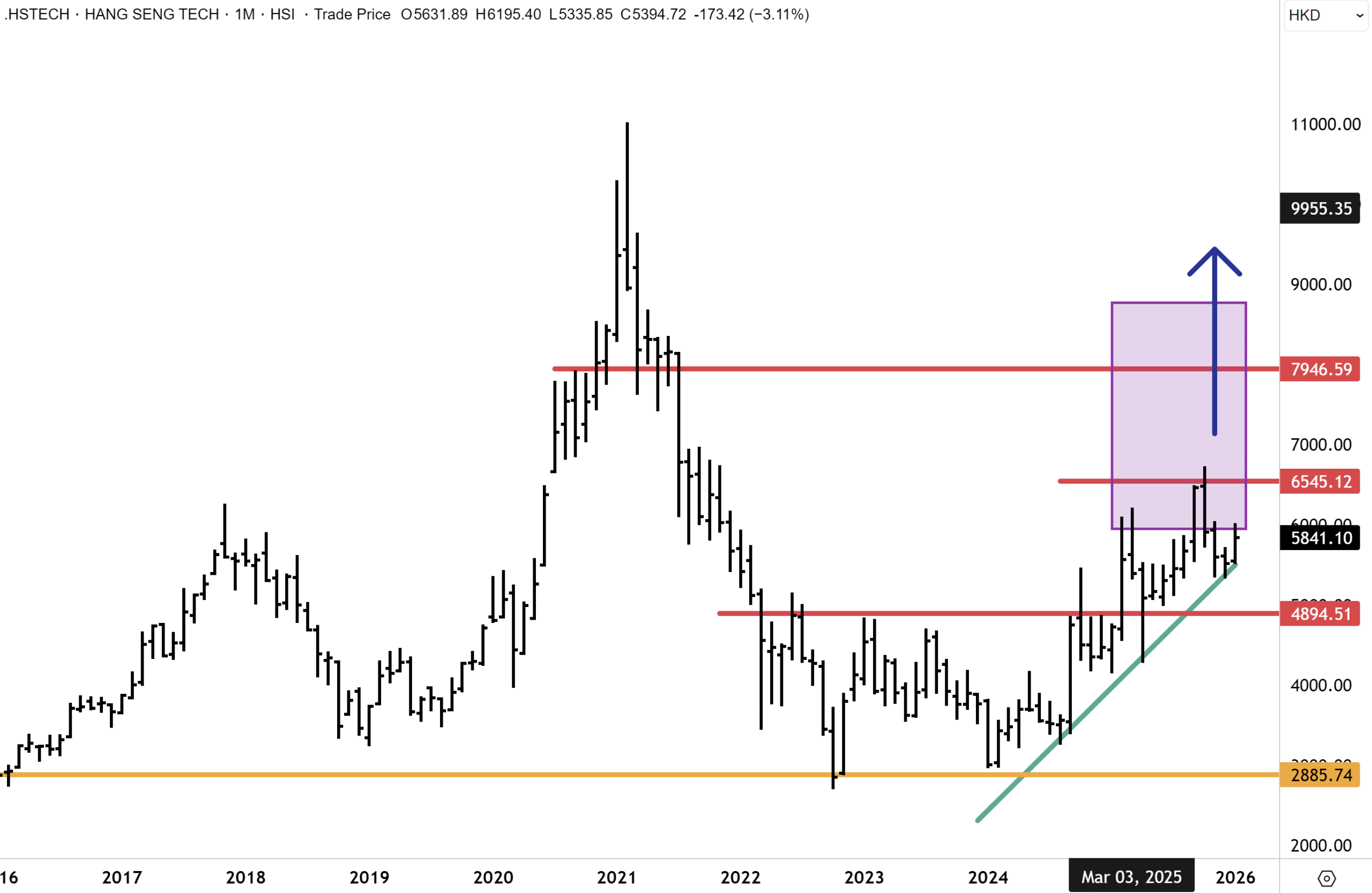

I concur, and the Chinese-laden Hang Seng Tech index has had a strong start to the year. The Hang Seng Tech index has corrected back to the primary uptrend in place since the defining double bottom was traced out in 2024. I have conviction the HS Tech index will resume upwards momentum and take out last year’s highs above 6,500 this year, with a retest of the 8,000 likely in my view. Major Chinese tech stocks are benefitting from the rapid rollout of AI, which is accelerating cloud revenues. China tech commands a much lower valuation than US peers.

![]()

Turning to Japan, whilst investors are concerned about the recent strength in the yen (which is spurring fears of another yen carry trade unwind, which led to extreme volatility in the market in 2024, when the Nikkei dropped 25% in three days – but then quickly recovered). Rising JGB bond yields have also put the spotlight on Japan’s indebtedness, with debt to GDP well over 200%, which is high. However, I believe these fears are overplayed, and there is an opportunity in Japan, if taking a medium to longer term view.

JP Morgan published an update on Japan this week and asked the question, “To what extent can Japanese equities withstand rising rates and JPY depreciation?” JPM cited that “With a snap general election on Feb 8 approaching, pledges by the ruling and opposition parties to cut consumption taxes on food, among other measures, have heightened concerns about further fiscal expansion and the possibility that higher long-term rates could trigger selling in Japanese equities. Since Takaichi’s victory in the LDP presidential election, the yen and bonds have sold off. While JPY weakness and the rise in long-term rates have persisted, Japanese equities have continued to rise. Global markets are watching closely for the interest-rate and USD/JPY levels at which Japanese equities would start to correct and whether a scenario like the “Truss shock” could happen in Japan.”

JP Morgan is more relaxed about Japan, and their base scenario assumes that the administration has the capability to calm market concerns. JPM noted that “even if the equity market corrects, we see the level as lower bound based on earnings, valuation and other investment themes. If the market falls further for no other reasons, we think the correction would represent a good buying opportunity for Japanese equities, as was the case in the summer of 2024.”

I totally agree with JP Morgan, and when the Japanese stock market lost 25% in three days, we didn’t reduce exposure in our portfolio’s (out of panic) like many other investors, and added selectively to positions when the market began to recover. If Japan were to undergo a decent correction in the coming weeks, I would advocate doing the same.

Morgan Stanley’s Mike Wilson had this to say about Japan. “Having just returned from seeing investors in Japan, it’s clear that the country is on a much different path than it has been for the past several decades. Deflation is a distant memory. In fact, most are now feeling the impact of inflation and rising import costs. With a snap election upcoming, purchasing power for households clearly in focus, and the yen dropping close to 160, market participants are increasingly expecting FX intervention to stabilize the currency. In the past, abrupt strengthening in the yen following JGB yield increases has led to volatility in risk assets tied to the carry trade at times. While the yen is worth watching closely in this context, we’d point out that these episodes have been temporary…”

Morgan Stanley upgraded their outlook for Japanese banks this week, where we hold significant exposure in the Fat Prophets Global Contrarian Fund and Asia and Global managed account portfolios. “Our macro team has revised its outlook for the BoJ’s policy interest rate and now expects additional rate hikes in June 2026 and April 2027. We view Japan’s rate normalization as still at an early stage, and upgrade our Japan Banks industry view to Attractive”. MS justifies an overweight stance on the banks because “amid the backdrop of a rate hike cycle and potential steeper yield curve from short to long zone, we see this as a period of earnings acceleration for banks. We believe bank stock price performance is unlikely to meaningfully peak till the market begins to focus on the terminal rate, a phase we see as some way off.” I have been making the same point on the Japanese banks for some time now, and a steeper yield curve and higher yield curve will provide a powerful tailwind to bank earnings this year, in my view.

I would also add that the Japanese yen is very undervalued. As a skier, a daily lift ticket at the major resorts is around A$70, which is full of Australians and other visitors, all there to take advantage of some of the best snow in the world! Eating out is cheap, and dinner per head, including a few beers or wine, is about $50pp. Given that negative real interest rates persist in Japan, and equity valuations are very cheap amidst rising return on equity for the broader market, I can’t get bearish on Japan and see the bull market continuing for some time, and possibly for some years.

In Gold we Trust

Moving on, gold spiked to a fresh record high above $5,600oz briefly on Thursday and then sharply reversed, which points to a coming period of consolidation after the strong run this year. We may well have seen a near-term peak in euphoria, with conditions now flashing “overbought”, which could see some of the heat now come out of the sector. This would be a healthy outcome.

But I remain resolutely bullish on gold and the PGMs over the medium to longer term, given our global macro framework and general outlook for financial markets – and of course the US dollar.

Hedge fund manager Jeff Gundlach, dubbed the “King of Bonds” by Barron’s noted that his overweights in gold and commodities were driving performance and that the Bloomberg Commodity index, which is well above the 200d moving average, had broken out. I referenced this last year, and Jeff Gundlach (along with ourselves) was one of the few to make a bullish call on the BCom index breaking out in 2025, with commodities doing well.

The Bloomberg Commodity Index has rallied +c14% since breaking out in late 2025 to make a fresh four-year high. The scope is open for upside extension towards 140 this year, in my view.

![]()

The billionaire said that “one of the things I have learnt over about 40 years in business – is when you have a very good thesis it’s hard to change – we have been on the right track – and I have not made any changes to key portfolio settings. In terms of my personal portfolio and changes made – I bought more gold miners in June along with ‘land’. I like the idea of holding real assets”. He also mentioned emerging markets and international equities as a diversifier for US dollar based investors.

On the record gold price, Jeff Gundlach said that he agreed with his old friend Jim Grant (a veteran US commentator in the treasury bond market), that “the price of gold is the absolute reciprocal of investor confidence in the central banking system”. I concur, and a breakdown in trust over some central banks and the respective management of their underlying currencies is one factor behind rising global appetite for gold and precious metals.

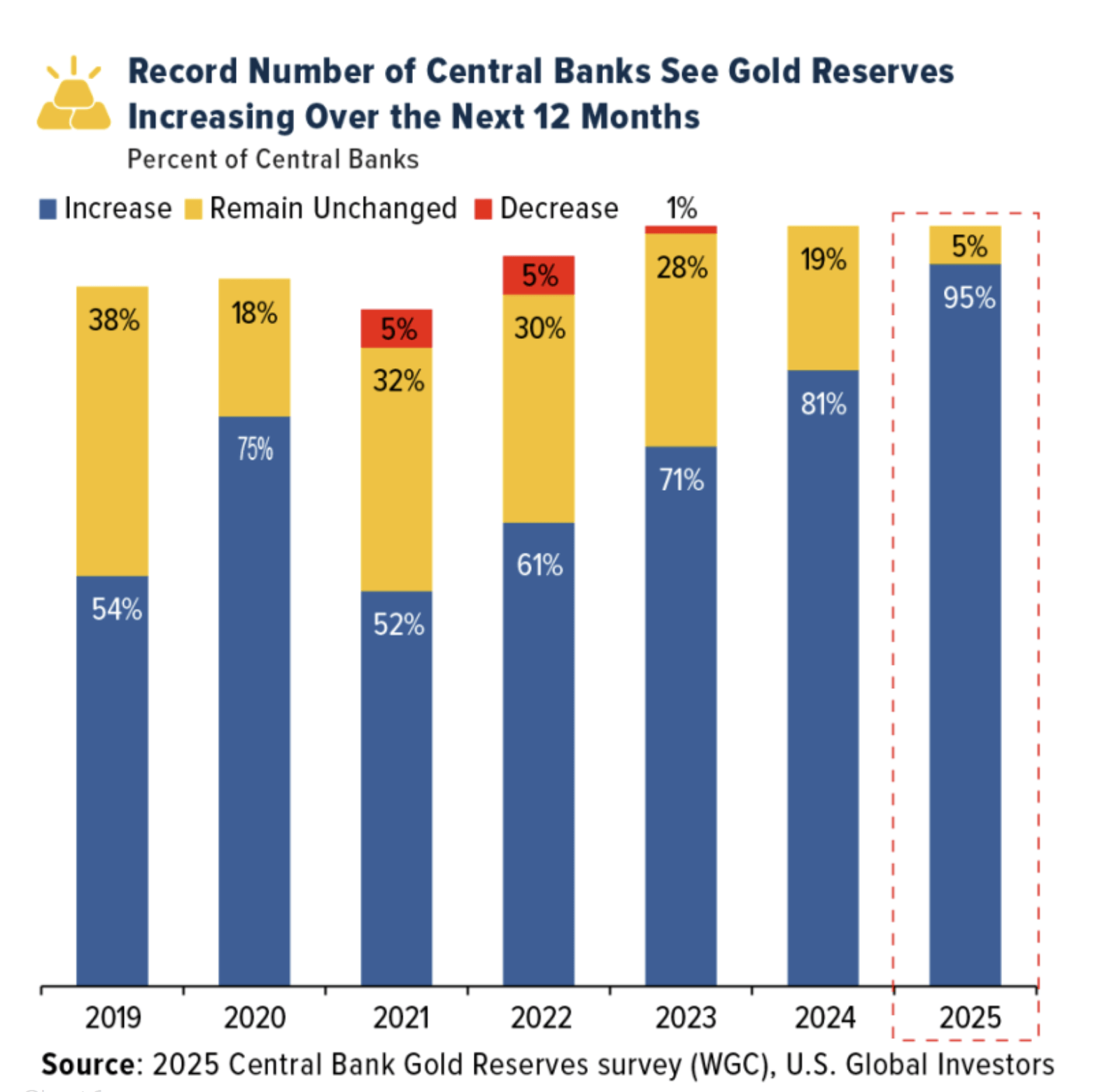

Central bank buying is accelerating

Some brokers are dialling back recommendations on gold and PGM miners, given the big run since late last year. Many investment banks run with very low long-term gold price forecasts in their valuation models, which are well below spot levels. JP Morgan is a notable exception.

This week, JP Morgan noted that “gold miners are in a brave new world”, and raised their long-term gold price forecast to $3,850oz. Pertinently, JP Morgan remains bullish on gold miners after formulating a new framework for forecasting long-term gold prices. The investment bank has justified raising its long-term gold price given “historical parallels from past reserve currency paradigm shifts”. This is one factor I have discussed repeatedly – and I believe the US dollar reserve currency status is now being tested.

JP Morgan cited other factors that justified a lift in their gold price assumption, which included further investor diversification into gold. The bank also conceded that the implied price [of gold was rising] as a “store of value amid unprecedented US debt. Although geopolitical headlines have dominated investor conversations regarding gold & gold miners, several more fundamental developments increase our confidence…which point to higher longer-term prices and support.” JPM forecasts gold will rise well above $5,000/oz this year.

In terms of buying support, JPM pointed to a number of new developments. These developments included “1) Nordic pension funds selling US debt, 2) Polish central bank buying more gold, & 3) Zambia permitting greater tax payments in RMB and less in USD. Overall, these reinforce our above consensus long-term gold price forecast, point to additional upside, & support our bullish call on Gold Miners.” In Europe/UK, AngloGold and Fresnillo remain their top picks “given strong mark-to-market upgrades, near-term cash returns upside, & re-rating potential vs peers”.

JPM highlighted that Nordic pension funds had been divesting US Treasuries and that one Swedish pension fund had sold most of its US Treasuries since the beginning of 2025. “Gold, as a diversification asset, could see incremental inflows. Our Commodities Research team estimates that diversification of around 0.5% of foreign US assets into gold, which equates to ~ $17bn quarterly rotation, could drive the gold price to ~$6,000/oz”. On that front, I note that the Polish central bank has steadily increased gold holdings by around 150 tonnes to 700 tonnes with plans to keep buying. Other central banks can be expected to follow suit.

The Bond Vigilante Tracker

We continue to watch global bond markets carefully. JGBs have been calmer this week after the surge in early to mid-January. Meanwhile, in the US, fiscal stability concerns are mounting alongside projected debt increases from aggressive military spending plans. Proposed surges in military spending to $1.5 trillion by 2027 could potentially add nearly $6 trillion to the national debt over the next decade – a trajectory that has already begun to coincide with rising Treasury yields.

Veteran US strategist Ed Yardeni said in a note this week that “broader geopolitical concerns during DJT’s second term are boosting both the precious and base metals complex.” Mr Yardeni cited that Defense companies are ramping up production, boosting demand for metals, while an intensifying AI arms race is fuelling capital spending across technology and infrastructure. I have flagged these points as well – and it’s no coincidence that the Bloomberg Commodity Index made a 4yr high this week above 121.

Mr Yardeni pointed to the US fiscal outlook after DJT proposed boosting military spending to $1.5 trillion by 2027, up sharply from current levels. (I made this very point a week or so ago). Mr Yardeni noted that “the Committee for a Responsible Federal Budget has warned that the plan could add nearly $6 trillion to the national debt over the next decade — a concern that has coincided with rising Treasury yields. We are on alert for an attack on the US by the bond vigilantes”. I concur with Ed and believe it is only a matter of time before pressure is exerted in the US bond market. Ed concluded that “despite gold’s dramatic run, we believe the rally isn’t over.” Yardeni is targeting gold at $6,000 by the end of this year — and $10,000 by the end of 2029.

While the bond market has remained resilient following the recent FOMC decision to hold rates at 3.50%–3.75% this week, the calm masks a looming structural test of the Federal Reserve’s independence.

Online betting markets are now attaching a 50% chance to BlackRock’s Rick Rieder as being the next Fed Chair. Mr Rieder is an advocate of lower rates and holds similar views to DJT. Whilst Jerome Powell can choose to stay at the Fed as a voting member of the FOMC until 2028, his departure would allow the White House to make another appointment, which would stack the board. The FX markets would not be comfortable with this outcome.

For now, the US bond market still appears well contained. I don’t think the Fed will cut rates now, whilst Powell is still Chair, with his tenure up in May. When Powell was asked about why he attended the Lisa Cook criminal investigation and hearing, he replied, “This is the most important test case for the Fed as an institution”. His reply obviously framed up his concerns over Fed independence being compromised.

Fed Chair Jerome Powell refused to comment on the US dollar when asked a question during the presser that followed the FOMC meeting. He also abstained from a question relating to surging gold prices and refused to be drawn in on a question about the dollar losing its status.

If the Fed cuts rates later this year and undermines independence through making a political appointment as the next Chair, then the dollar could come under more pressure – and this will likely only stoke the bull market in precious metals and push gold prices higher in my view. The White House is not far away from exerting fuller control over the Fed – and this is one risk for the dollar that is now squarely on the horizon with Jerome Powell’s tenure up in just a few months.

Inflation heats up Down Under

In Australia, higher-than-expected CPI data shifted market pricing about the likelihood of a looming RBA rate hike next week. Headline consumer prices accelerated to 3.8% year-on-year in the December quarter, up from 3.4%, overshooting market forecasts of 3.6%.

The closely watched trimmed mean measure of core inflation rose 0.9% quarter-on-quarter, exceeding the 0.8% consensus and lifting the annual rate to 3.4%, above market expectations and the RBA’s 2.5% midpoint target. The result marked a back-to-back rise in underlying inflation from the September quarter and represented the first sustained pick-up in the measure since 2022.

The breadth of price pressures will be concerning for policymakers, even if a few elements may still prove fleeting. More than two-thirds of all items measured in the consumer price index posted annual increases exceeding 3%, the top of the RBA’s target band. Money markets responded swiftly to the data, lifting the probability of a 25bp increase at the February 4 policy meeting to around 75%, up from 60% before the release. Westpac and ANZ backtracked on earlier calls for an extended hold, now anticipating one hike, while some economists warn that two may be on the cards. If the RBA does hike, it will be the first major central bank to reverse course this cycle.

Trimmed mean inflation came in too hot for comfort.

Australian Property’s Second Wind

Finally, Australia’s housing market roared back in 2025, with prices rising at the fastest pace since 2021 as tight supply, resilient demand and the expanded 5% Deposit Scheme fuelled a second-half surge. A report from KPMG expects momentum to carry into 2026, with solid but slower growth led by more affordable markets, while high-end prices are capped by borrowing constraints. Affordability remains stretched, and supply is still running well short of demand, meaning price pressures are likely to persist unless construction lifts materially.

KPMG’s January 2026 Residential Property Market Outlook argues that Australia’s housing market has moved decisively out of its post-2022 slowdown and into a new upswing. National house prices surged 8.6% and unit prices 7.3% over the year to December, the strongest calendar-year gains since the pandemic-era surge of 2021. The rebound was broad-based across capital cities, with Perth, Brisbane and Darwin leading the upswing as tight supply and strong population growth collided with renewed buyer confidence. Even Sydney and Melbourne, long constrained by affordability, continued to edge higher.

Looking ahead, KPMG expects housing momentum to remain solid through 2026. National house prices are forecast to rise 7.7% and unit prices 7.1%, supported by stabilising financial conditions and a chronic shortage of dwellings. The outlook points to a two-speed market, with affordable segments continuing to outperform while limited borrowing capacity caps gains at the upper end. City-level forecasts suggest further strength in Perth, Brisbane and Darwin, steadier growth in Sydney and Melbourne, and more moderate outcomes in markets where affordability pressures are already biting.

Beyond prices, the report highlights deepening structural challenges. Housing affordability has fallen back to levels last seen in mid-2023, with the median home now close to nine times average income. While rental inflation has moderated, vacancy rates remain near historic lows, and tenants are devoting a record share of income to rent. Crucially, KPMG estimates that net housing supply over the next two years will fall about 30% short of what is required to meet demand, putting the government’s 1.2-million-homes target at risk. Getting to a more affordable housing environment is going to take a huge uplift in housing supply!

Moving on from the report, rising dwelling prices underpin household balance sheets and wealth effects, supporting consumption even as borrowing costs remain elevated. At the same time, stretched affordability and tight rental markets keep underlying inflation sticky, particularly in housing-related services, complicating the path back to target for policymakers.

The chronic supply shortfall is the deeper issue. With construction failing to keep pace with population growth, housing is shifting from a cyclical to a structural inflation story. That raises the risk that interest rates need to stay higher for longer to restrain demand, even as parts of the economy slow.

The bias here is to overweight residential developers and building materials with exposure to affordable markets in Western Australia and Queensland. The sweet spot is companies leveraged to master-planned communities, land subdivisions and medium-density housing. Stockland and Mirvac fit the bill here. The Members area on the website contains notes on these REITs, along with multiple other recommendations in different sectors and geographies.

Report spotlight

Global X Silver Miners ETF – recommendation change

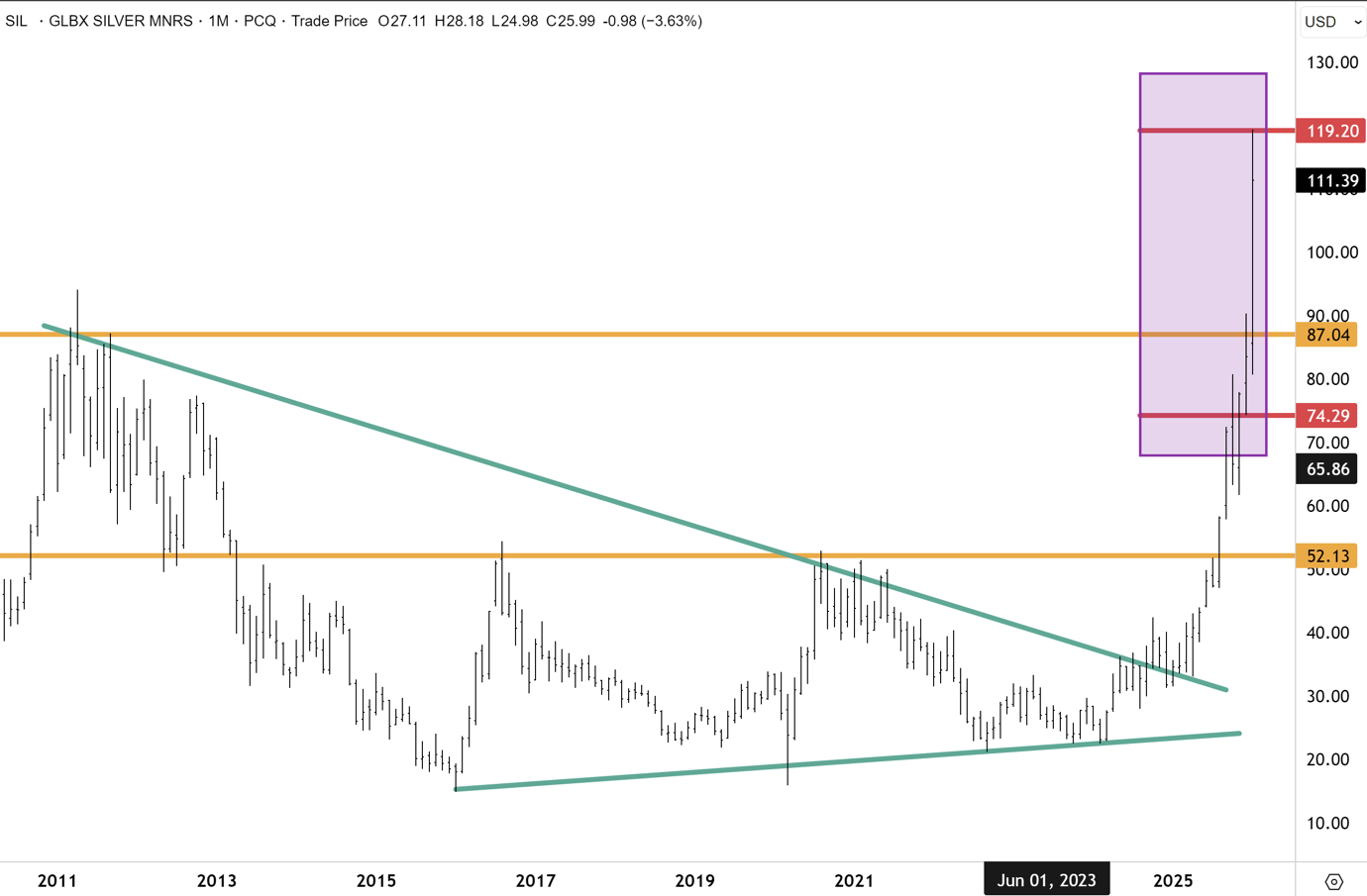

Silver has shattered $110 per ounce while gold broke through $5,500, capping an extraordinary run that saw the Global X Silver Miners ETF (SIL) surge 250% over the past year. But after advocating the bullish case throughout 2025, we’re shifting our rating to HOLD as overbought conditions and FOMO-driven speculation signal a consolidation period ahead.

The fundamentals remain ironclad. Silver is entering its sixth consecutive year of structural deficit, where supply simply cannot keep pace with the modern world’s insatiable appetite. About 70-75% of silver is mined as a byproduct, making supply difficult to scale quickly. Meanwhile, demand drivers have multiplied beyond traditional monetary, industrial and jewellery uses into the “Compute Age” and energy transition.

Data centres have become the engine of the 2020s, and silver’s unmatched electrical and thermal conductivity makes it pivotal in high-density computing. Global IT power capacity has exploded by an estimated 53x since 2000, with data centre construction forecasted to keep growing rapidly over the next decade. Solar capacity is projected to grow at a 16-17% compound annual rate through 2030, amplified by next-generation cells like TOPCon and HJT that require substantially more silver than previous industry standards. A single battery electric vehicle consumes 67-79% more silver than a traditional combustion engine, primarily for battery management systems and charging infrastructure.

Tactical Pause: While our bearish dollar view is playing out and the precious metals bull market isn’t over, the easy gains have been captured. SIL has hurdled historic resistance to make new record highs above $120, but we expect consolidation before upward momentum resumes later this year. For those whose positions have outgrown their risk tolerance, trimming secures gains. We’re staying in the trade but advocating against chasing at these levels.

The Global X Silver Miners ETF (US: SIL) has successfully hurdled historic overhead resistance and confirmed an important inflection to make new record highs above $120. We believe that SIL will now enter a period of consolidation as overbought conditions are worked off, before upward momentum resumes later this year. Our bearish view on the US dollar is playing out.

We expect silver spot prices to undergo a corrective consolidation before reasserting upward momentum later this year. Our base case for precious metals is that the bull market is not over yet, given further downside risk in the US dollar.

![]()

This report and many others spanning Australasia, Mining and Global Equities are available online for your reading pleasure in the Members area, should you be interested in subscribing for investment snapshots and deep dives across a range of investment vectors, along with our regular Daily correspondence on the markets and key investment themes.

Turning to the Fat Prophets Global Contrarian Fund, released an update to the ASX this morning with the estimated pre-tax NTA climbing above $2.20 for the first time. The Fund had a strong start to the year with January NTA climbing +13%, which was one of the best months. FPC shares also traded at a record high yesterday at $1.64, with the discount still wide. I have noticed in recent months that the share register is beginning to tighten up, with increasingly fewer sellers.

The listed investment company has just 28.1 million shares on issue, with around 30% now locked up amongst the top 20 shareholders. This is encouraging, and I am optimistic that the share register will become even more tightly held this year. Depending on future performance, of course, and it is not guaranteed, but ‘plausible’ that one day the discount disappears entirely, and FPC shares even trade at a premium.

Excerpt from the FPC ASX this morning:

Have a great weekend!

Carpe Diem!

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.