- AI investment fatigue has intensified as markets question the timing of returns on the massive infrastructure spend. The “Mag 7” faces increased scrutiny over combined capital expenditure plans exceeding $650 billion, forcing a valuation reassessment in the highest-multiple tech names. Meanwhile, AI displacement worries have swept through multiple market pockets.

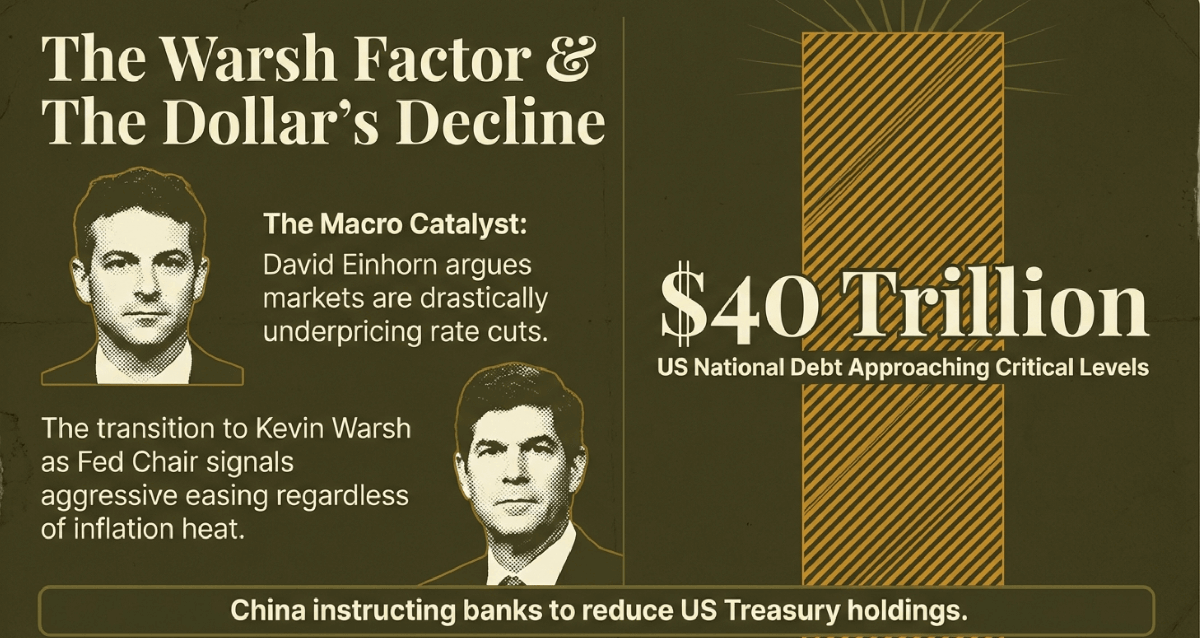

- Fed cut expectations have emerged as a primary fault line. David Einhorn argues markets are “wrong” to view strong jobs data as a reason not to cut, betting on substantially more than two cuts this year as incoming Chair Kevin Warsh potentially uses “productivity” as an argument to ease policy.

- Sovereign debt risks are triggering a strategic rotation. Beijing’s signal to mainland banks to pare down US Treasury holdings reflects a global wariness of US fiscal discipline as national debt breaches $38 trillion. The technical setup for the 30-year yield remains decisively bearish.

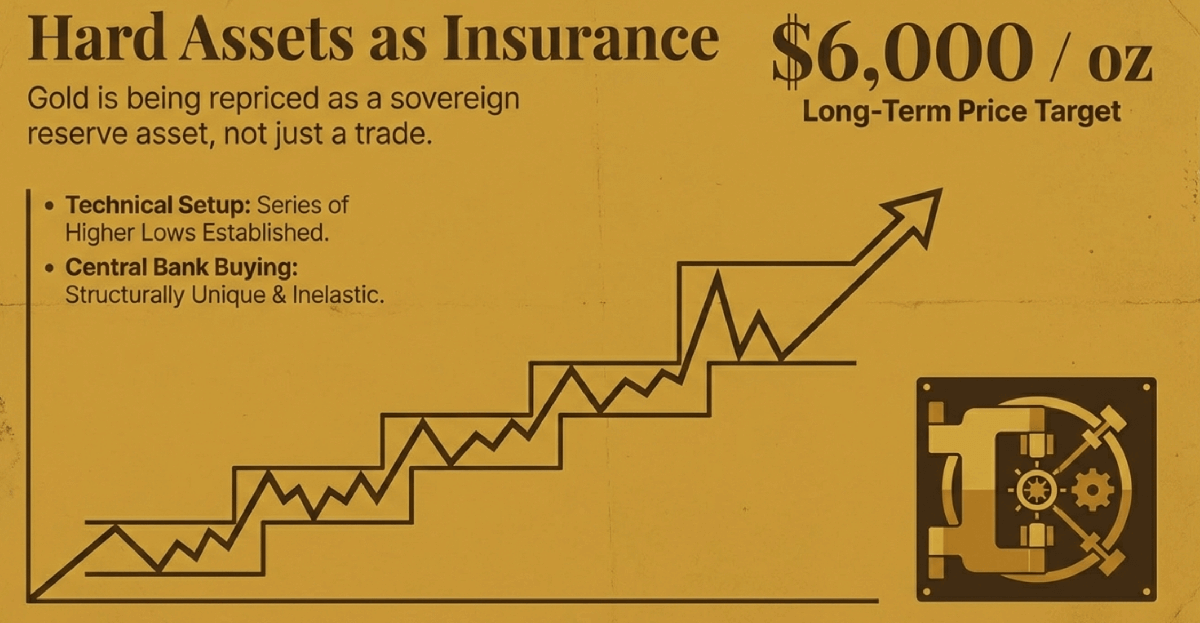

- Gold is transitioning from an inflation hedge to a core reserve asset. Central bank buying remains the dominant force as nations seek to settle trade in something other than US dollars. Despite a recent washout, the series of higher lows points to constructive consolidation before a potential run materially higher.

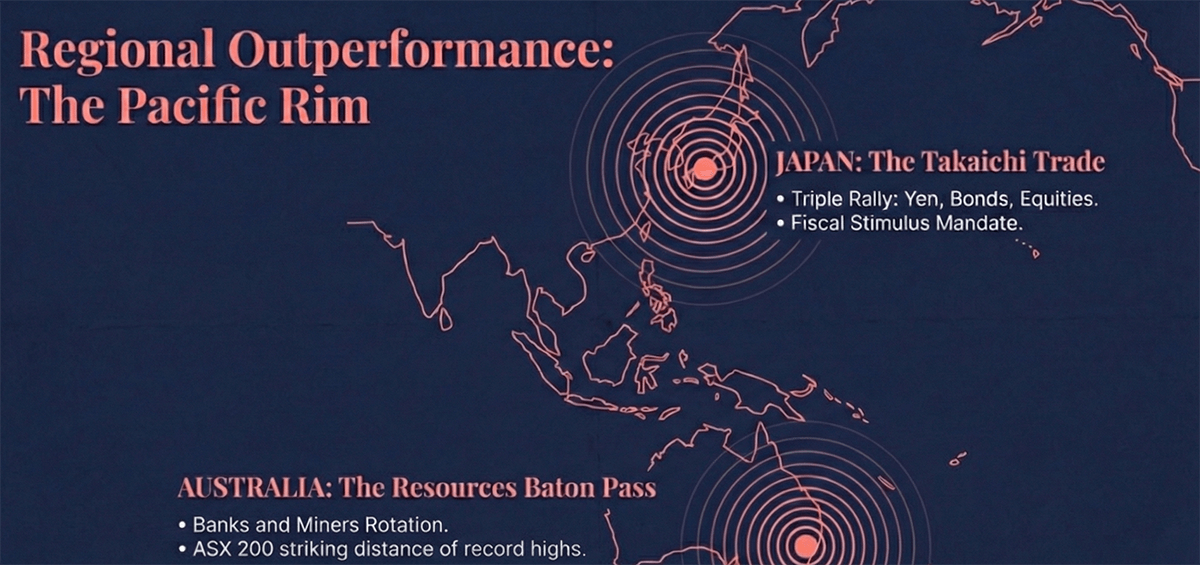

- Japan’s “Takaichi Trade” has unleashed a rare triple rally. A landslide election victory has provided a mandate for aggressive fiscal stimulus, causing the yen, bonds, and equities to rally simultaneously as political uncertainty evaporates

- The RBA has delivered its weakest medium-term growth outlook on record. Governor Michele Bullock has warned that government spending and interest rates are inextricably linked, signalling a hawkish pivot that prepares Australians for higher-for-longer rates amid a chronic productivity slump. However, the economy is not the market. We see continued upside for the ASX200.

Report Spotlight

- James Hardie (ASX: JHX, US: JHX): Resilience in US pricing and AZEK synergies support a recovery thesis – BUY

What to watch next week

- US: Fed meeting minutes, more housing and jobs data. CPI numbers tonight could move money markets.

- Australia: RBA minutes, jobs data. If jobs hold up, the case for another hike later this year increases.

- Software “Circuit Breakers”: Whether earnings from software names can provide a fundamental bottom to the “SaaSpocalypse”.

- Bond Market Stability

It has been another busy week. By connecting the dots between sovereign debt signals in Beijing, hawkish pivots in Canberra, and the “SaaSpocalypse” on Wall Street, we provide a concrete game plan for navigating a landscape that increasingly echoes the hard-money cycles of the 1970s. Let’s dive in.

Global Markets

The Dow Hit 50,000

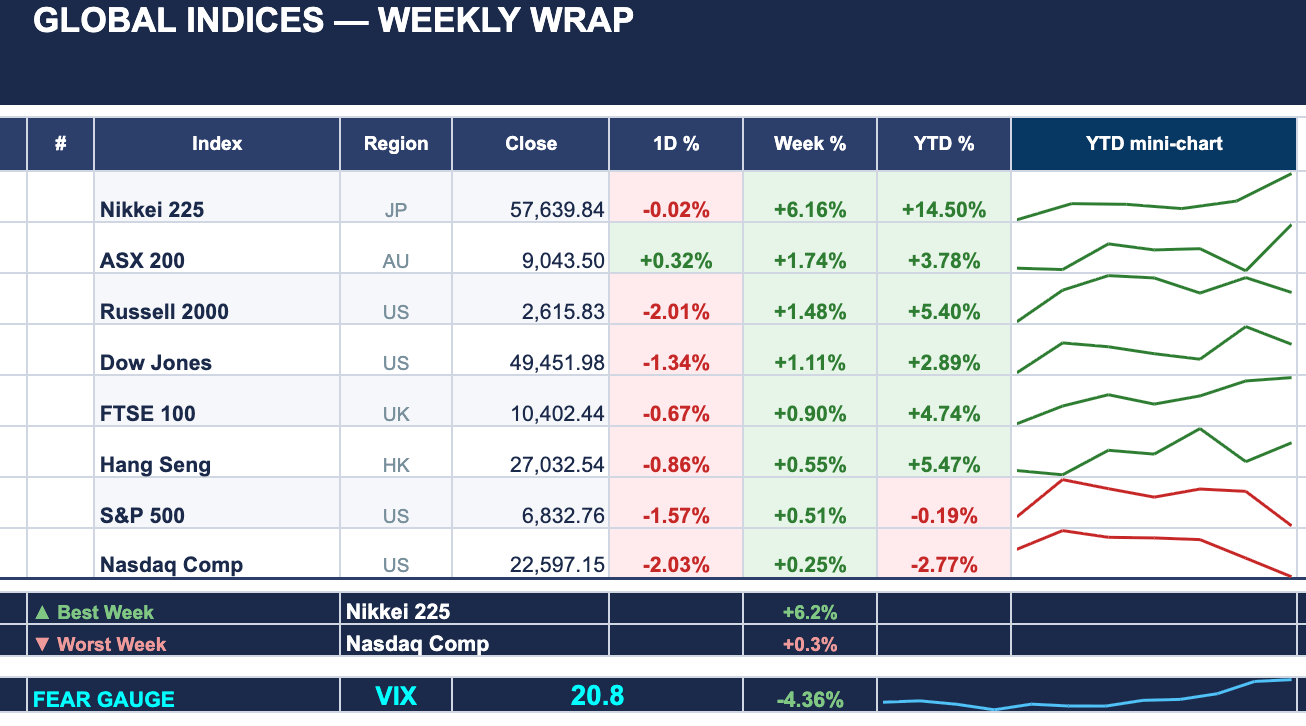

The week began with champagne and ended with a cold shower. Last Friday, the Dow Jones Industrial Average breached the 50,000 mark for the first time in its 129-year history and continued the party early in the week, retaining the historic level amid solid demand for ‘old school’ names. It wasn’t the only index doing so. Indeed, the MSCI gauge of global equities hit a record high mid-week.

By Thursday, the mood had shifted in the US, though the Dow Jones Index was still up +1.1% over the past week. Two key factors over the past week in the US were job market data and the continued shifting perspectives on the AI trade. We are seeing a Great Rotation playing out in markets.

From “AI growth at any cost”, many investors are tilting toward tangible assets, financials, and defensive value. The “SaaSpocalypse” that has decimated many software and high-multiple tech stocks has continued, rotating through different areas like wealth management and platforms, insurance brokers, data providers, alternative asset managers and transportation and logistics. Meanwhile, on the other side of the trade, investors are increasingly questioning the prospects of sufficient return on $650 billion in AI capital expenditures outlined by just a handful of tech titans. Concurrently, Beijing signalled diversification away from US Treasuries, adding complexity to the bond market.

The week was characterised by distinct divergence. Digital assets faced liquidation, while gold, copper, industrials and defensives caught an “insurance” bid against geopolitical friction.

Macroeconomically, early-week labour strength in the US pushed yields higher and dampened rate-cut hopes. This reversed sharply on unexpectedly flat December retail sales and sliding home sales, reigniting the “bad news is good news” trade. Yields across the bond curve fell on Thursday. Over the past week, the Dow and Russell 2000 showed modest outperformance, highlighting rotation into cyclicals and small caps.

Note: 1D% performance represents Thursday’s trading (12 February)

Note: 1D% performance represents Thursday’s trading (12 February)

Japan was the star performer, surging to record highs (+6.2% over the past week and +14% YTD). PM Sanae Takaichi’s landslide victory provides a mandate for aggressive fiscal stimulus. Japanese equities rallied alongside the Yen, which strengthened to ¥152 against the dollar. The “Takaichi trade” lifted banks and reignited domestic demand sectors.

China offered mixed signals. State liquidity and AI focus (ByteDance’s new video model) lifted mainland tech, though Hong Kong counterparts struggled. Nevertheless, we are bullish on Chinese tech names and view them as relatively defensive given the substantial valuation discounts.

European markets drifted in the US volatility’s slipstream but are hovering around record highs. The FTSE 100 dipped on Thursday, but crested record levels earlier in the week. The “old economy” composition of the blue chip FTSE 100 index provided a buffer. Miners tracked higher commodity prices.

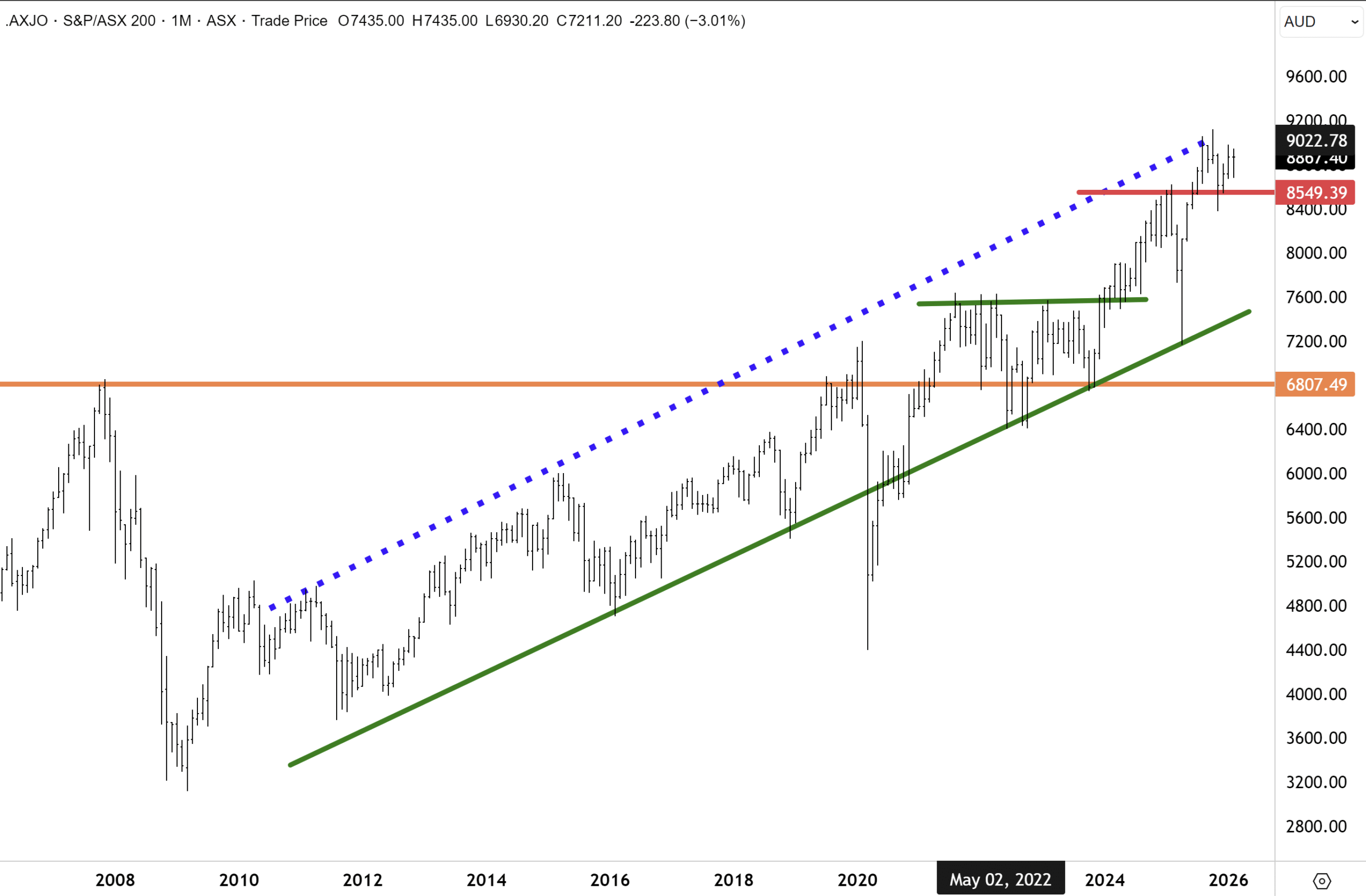

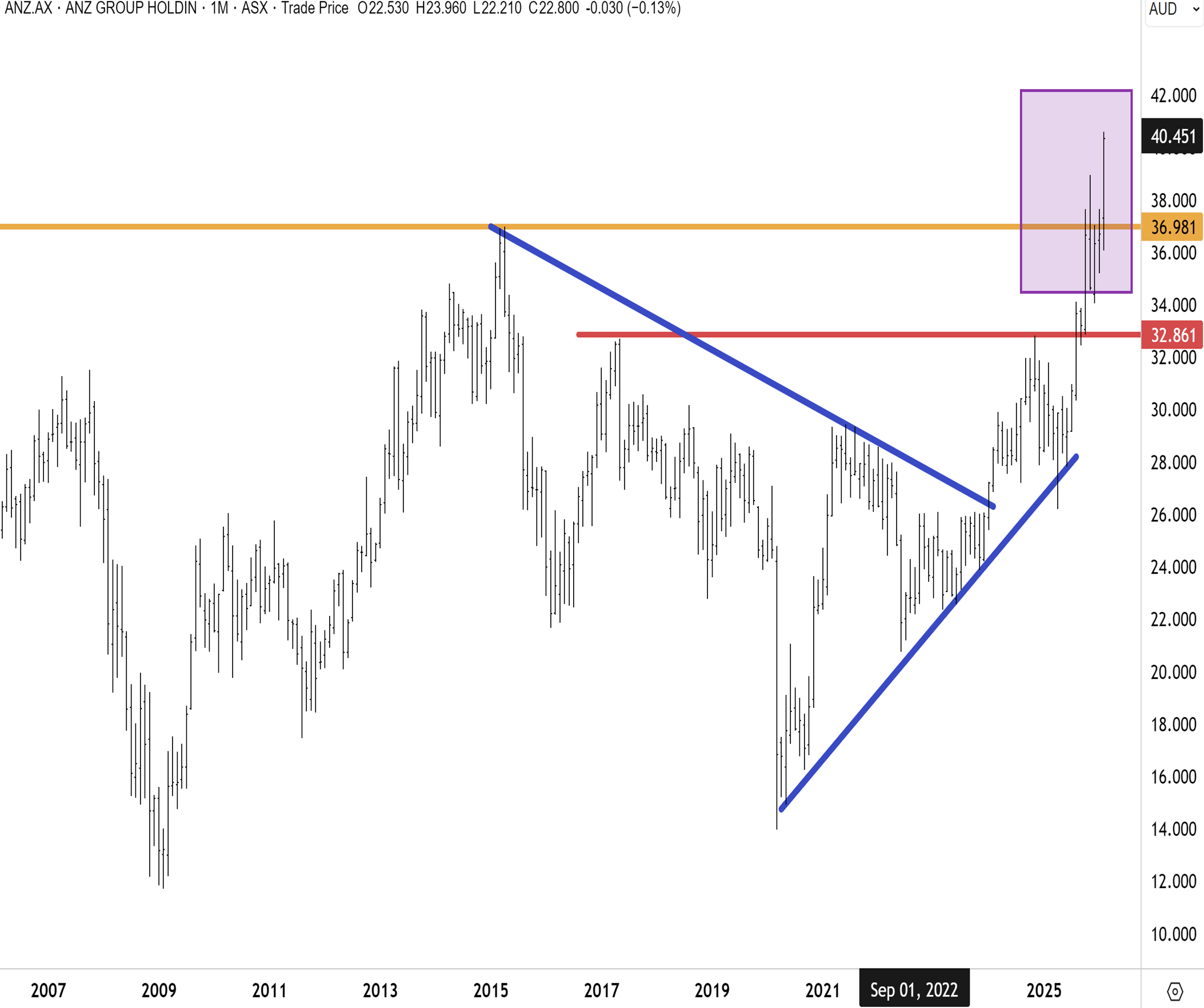

Australia’s ASX 200 ground pushed through 9,000 despite global tech carnage. Former high-flyers like WiseTech, Xero, and Pro Medicus suffered double-digit corrections, offset by Big Four banks (ANZ hit record highs) and broad materials strength. The RBA forecast weak growth over the medium term, but the economy is not the market, and the ASX200 is back within striking distance of the record highs visited last October – we believe a commodities super-cycle will be an assistive factor.

Hawkish Hints Down Under

The Reserve Bank of Australia delivered a poor economic forecast and said that Australia is staring at its weakest medium-term growth outlook on record. Should this pan out, it will threaten living standards and deepen pressure on an already deteriorating federal budget. This isn’t set in stone, of course, as central banks and economists often get it wrong. But still, the outlook was gloomy and pessimistic.

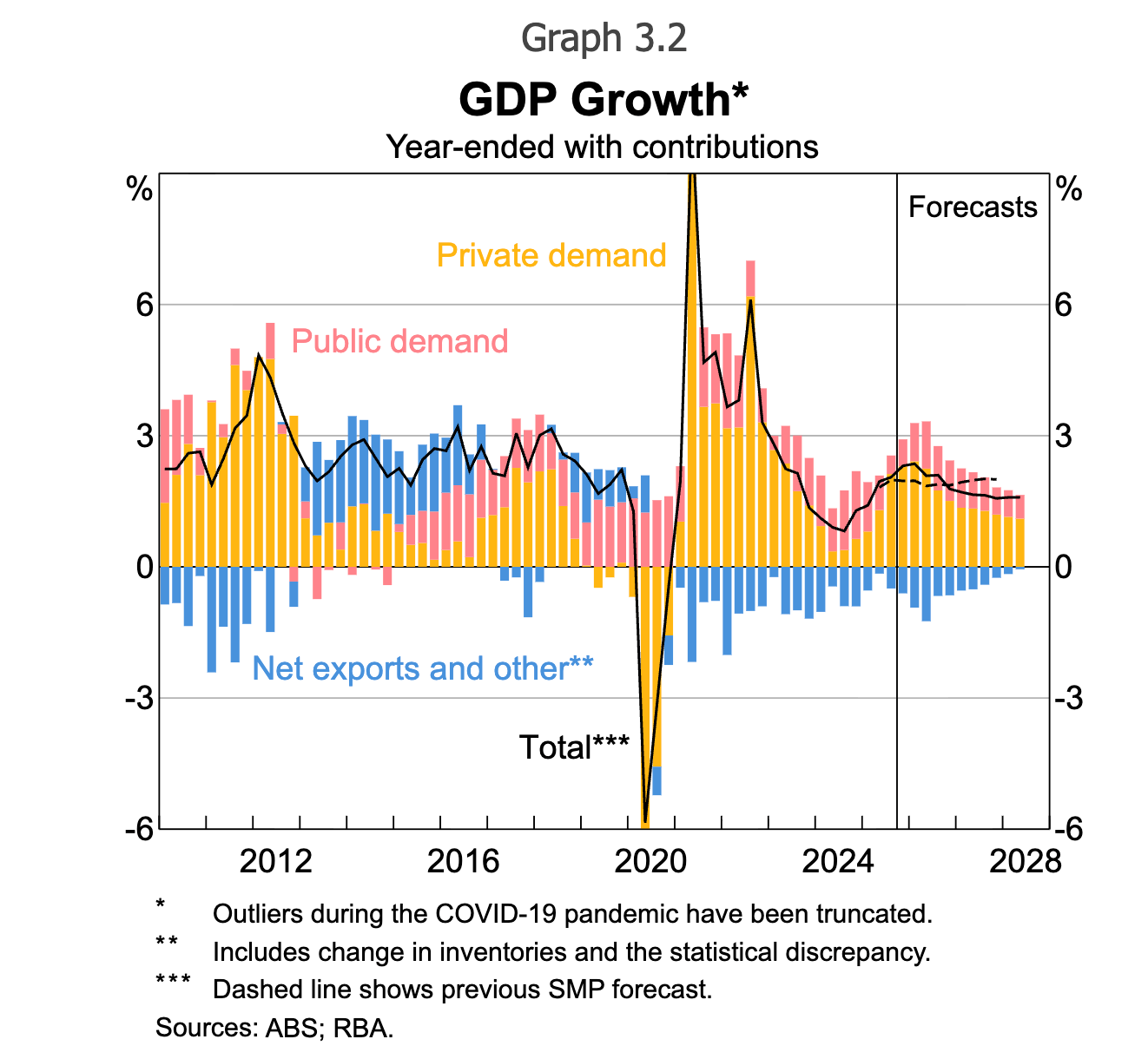

The RBA now expects the economy to expand by just 1.6% over the year to June 2028, the slowest outcome in its published forecasting history, underscoring how persistently low productivity and constrained capacity are shaping the outlook.

The forecasts landed as RBA governor Ms Michele Bullock told parliament’s economics committee that government spending, inflation and interest rates are linked, a message that quickly, reportedly, spilled into heated political exchanges. Prime Minister Anthony Albanese and Treasurer Jim Chalmers rejected claims that rising public outlays contributed to the RBA’s recent rate increase, arguing instead that inflation has been trending lower, unemployment remains low and real wages have begun to recover, even as inflation has ticked up again.

The near-term story is less bleak. According to the RBA’s February forecast, assuming the cash rate tracks market pricing, Australian economic growth is expected to strengthen in the near term before easing back. On current projections, the RBA says that, ‘year-ended’ GDP growth through most of 2026 should run above assessed potential and exceed the central bank’s previous forecast, reflecting a period of stronger momentum. The lift is being driven by private demand, which has outperformed recent expectations as a mix of domestic and global forces has gathered strength. The RBA says that none of these factors is a major surprise in isolation, but together they have produced a materially stronger upswing in spending as they converged in the second half of last year.

Source: RBA February 2026 Statement

Source: RBA February 2026 Statement

Where the RBA forecasts the economy to begin to go pear-shaped is from late 2026, when economic growth is expected to slow more sharply than previously anticipated and to run below estimates of potential, as a higher interest-rate track increasingly restrains private demand.

Compared with the November outlook, the key change is the assumed path for monetary policy. The projections are now conditioned on market pricing that implies the cash rate rising by about 0.6%, whereas the earlier forecasts had assumed a further 0.3% easing. That is a big swing in central bank land!

That shift has prompted a broad downgrade to interest-sensitive parts of the economy. Growth in dwelling investment has been revised lower, reflecting both the direct drag from higher borrowing costs and a softer outlook for housing prices across the forecast horizon. Household consumption and non-mining business investment are also expected to be weaker in 2027 than previously forecast, as tighter financial conditions take hold. A stronger exchange rate is an additional headwind. It is expected to support faster growth in imports while dampening some categories of exports, reducing the net trade’s contribution to GDP. Export growth is also forecast to slow as resource shipments ease back toward underlying productive capacity, after being temporarily lifted by inventory drawdowns. Together, these forces underpin the RBA’s view that growth will undershoot potential in the latter part of the forecast period.

If realised, the medium-term slowdown would weigh on living standards and intensify pressure on a federal budget that is already fraying. That concern is already playing out in budget scrutiny. Earlier in the week, on Monday, officials from the Parliamentary Budget Office were questioned about a post-election deterioration in the budget outlook first reported by the Australian Financial Review. While unable to verify a $57 billion figure cited by the opposition, the PBO said revisions were driven up about 60% by higher spending and 40% by weaker tax receipts in the latter half of the decade.

Low productivity is central to the risk profile. The AFR reported that former Treasury official Gene Tunny warned that if productive capacity expands too slowly while demand continues to rise, inflation could prove harder to contain over time, eroding long-run living standards. He argued that part of the productivity drag reflects rapid growth in labour-intensive government services, particularly the National Disability Insurance Scheme, which has absorbed workers from the private sector and offers limited scope for efficiency gains despite its social benefits.

While population growth and labour force participation have offset some of the slowdown, economists say those levers are now losing traction. Attention is therefore turning to the May budget, where the government has flagged a productivity package aimed at lifting the economy’s capacity.

What does this mean for the stock market? Well, as the old saying goes, the economy is not the stock market, and the stock market is not the economy. We remain bullish in our outlook for Australian equities and see the ASX200 well above 9,000 by year’s end. This view is predicated on twin propulsion arriving from the resources sector and our view that commodities are entering a ‘super cycle’. The banks led the market higher in 2024/25, but the resources sector is now squarely in the lead.

In terms of the technical setup for the ASX200, the index on the 20yr chart below, remains within a well-defined upward trend channel that has been in place since the 2008/9 lows. This upward trend channel is likely to remain in place for some time. One notable characteristic is that the ASX200 has always corrected lower after hitting the top of the channel. The most recent time this occurred was late last year.

In terms of the near-term setup, the ASX200 is nicely working off overbought conditions that manifested late last year. Pertinently, the Australian share market has withstood a rate hike by the RBA and a pivot to a hawkish bias. This has driven the currency higher. However, the resources sector is behind the resurgence in the Australian stock market as commodity prices have lifted across the spectrum. I have conviction that the index will soon be retesting the 9,000 level.

Later in the week, deputy governor Andrew Hauser signalled the central bank is prepared to tighten further to bring inflation back under control, saying price pressures remain “too high” and the bank will “continue to do whatever is necessary” to return inflation to the 2–3% target band. He delivered the message at a business luncheon. The warning follows last week’s 25bp increase in the cash rate to 3.85%, a policy U-turn that unwound an easing move made in August after inflation ran above the bank’s expectations. Recent data have left both headline and underlying inflation above target, and the RBA’s projections suggest inflation may not return to the band anytime soon, which is why officials are keeping the door open to additional action.

Mr Hauser argued the shift from easing to tightening reflects “three key facts” that have changed, including a stronger-than-expected global economy and a rebound in domestic private demand that has kept capacity pressures uncomfortably firm. He also pushed back on the idea that policy is designed to suit particular groups (i.e. politics), framing the bank’s focus on restoring price stability as the most direct way to reduce the ongoing burden that high inflation places on households. The bottom line is that Australians need to prepare for higher interest rates.

Commodities

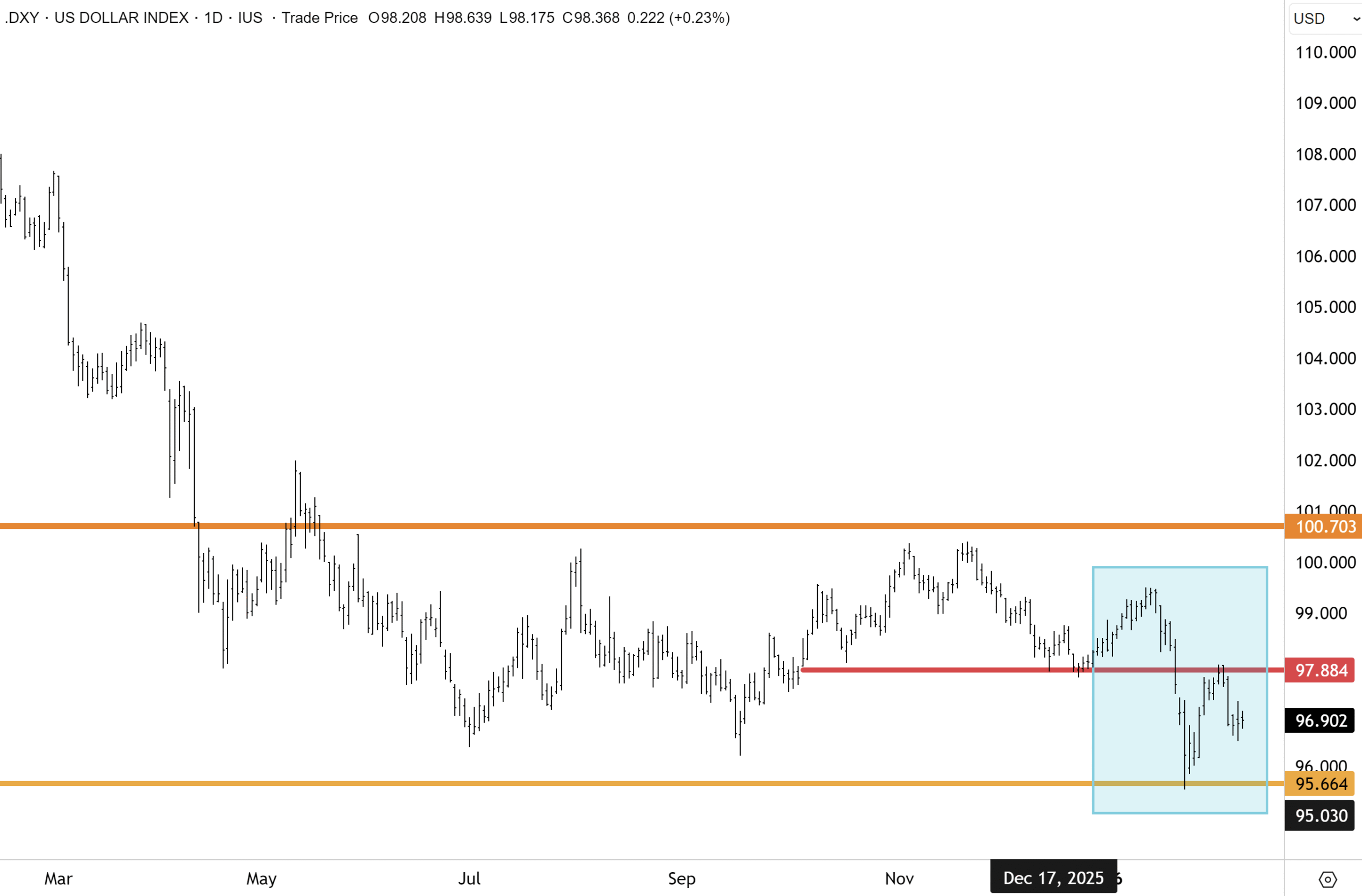

Gold consolidated around $5,000/oz, increasingly viewed as geopolitical “insurance” rather than just an inflation hedge. We discuss this in detail below. Industrial metals caught a bid on supply-side constraints. Copper pushed higher as investors stockpiled physical metal, while Nickel spiked on Indonesian production cuts. The US Dollar Index softened below 97 as yields retraced. The bond market is pricing a complex scenario – softening US growth, colliding with foreign Treasury divestment. China’s Treasury signal is a critical factor to consider, and we dive into this below.

This week marked a psychological shift from technology FOMO to rotation. The market is demanding proof of AI monetisation before bidding prices higher. Indeed, Amazon is down around 10% over the past week, the weakest performance among the Mag 7. Amazon just happened to outline the biggest AI capex plans at a mammoth $200bn! On the other side, there have been brutal software unwinds.

Simultaneously, the “commodity super-cycle” is gaining traction with a new nuance: fragmentation. Markets are pricing in regionalised supply chains and commodities as strategic assets. Strength in copper and gold alongside bank rotation suggests positioning for a reflationary environment where “stuff” outperforms “code” for a while. Now, let’s do a deeper dive into the insights from the desk of our CIO, Angus Geddes, over the past week.

Market Insights

The Sovereign Debt Trigger

First up, Chinese regulators have advised financial institutions to rein in their holdings of US treasuries, according to a report out Monday on Bloomberg. Apparently, Chinese officials have urged mainland domestic banks to limit purchases of US government bonds and “instructed those with high exposure to pare down their positions”. The directive doesn’t apply to China’s state holdings of US Treasuries.

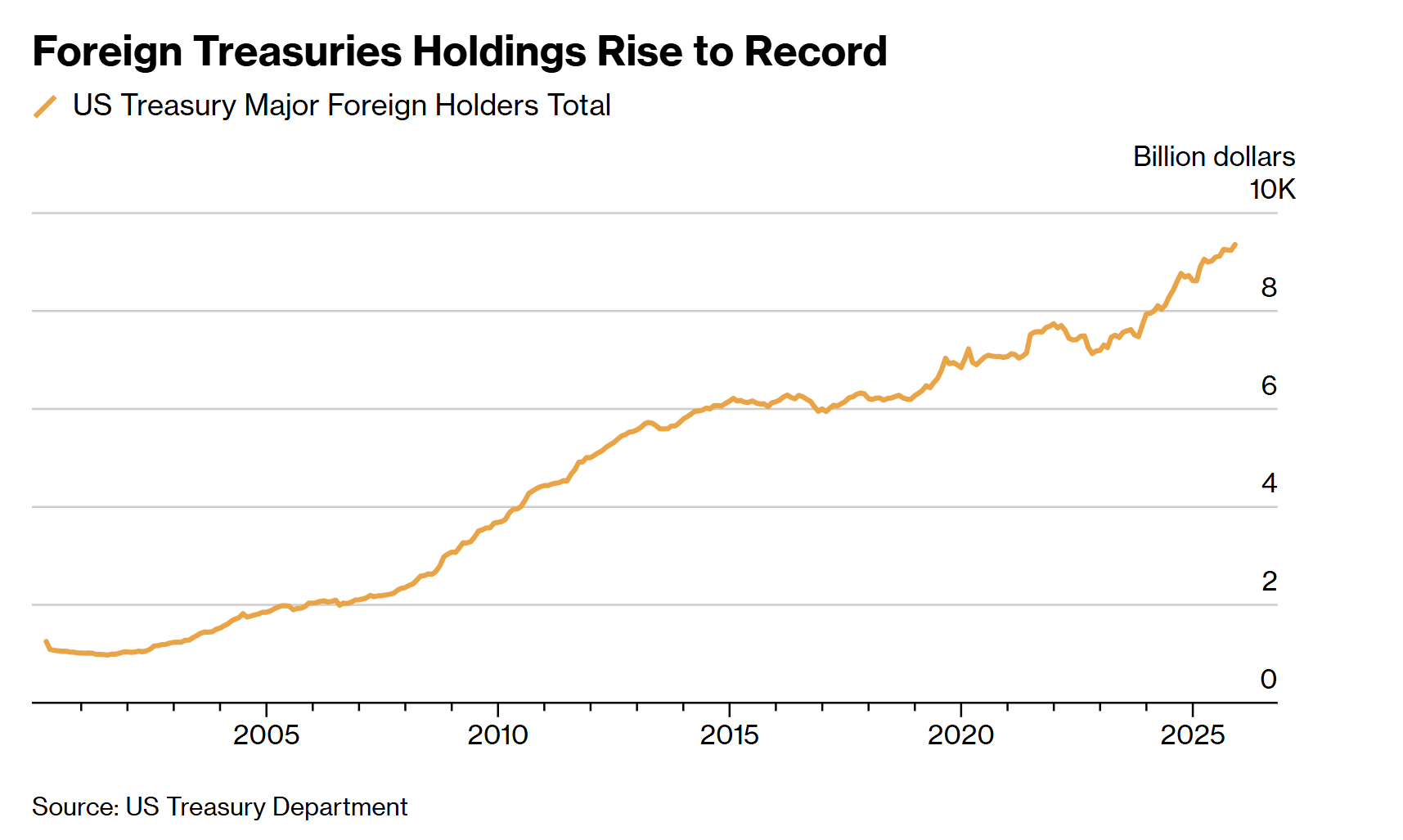

However, this directive is interesting and points to growing wariness among Chinese officials that large holdings of US government debt could pose a problem for the banking sector. I have made this point about foreign holders of US assets diversifying for some time now. We anticipate many central banks, governments and corporates to reduce exposure to US treasuries and diversify into other assets and bonds. With US debt to GDP running at well over 120%, the government could have a problem on its hands if bond yields were to rise over the medium to longer term (which is our base case).

While the Chinese regulators said the move was framed around diversifying market risk rather than geopolitical manoeuvring or a fundamental loss of confidence in US creditworthiness, there is a more obvious rationale. With the introduction of the tariffs, the Trump administration has pushed the world away from trade. The seizure of Russian assets (by the powerful US banking system, which dominates global financial markets) at the onset of the Ukraine war is another contributing factor. Many countries will likely follow China’s move, if they are not already doing so.

While Chinese officials did not provide any specific target on size or timing, it would not surprise me if US treasury holdings within China’s banking sector fell close to zero over the coming years. Treasuries slipped on the news, with yields edging higher across maturities in US trading – but the dollar weakened sharply against major peers. DJT held a phone call with Xi Jinping last week, and plans to meet the Chinese leader at a presidential summit in Beijing as soon as April. I believe this latest development will be on the list of issues discussed.

Chinese banks held around $300 billion of US dollar-denominated bonds as of September. I would not be surprised if this holding has declined significantly since then. We have had concerns around the US government’s fiscal discipline, and with the tax cuts and higher spending on military and defence, etc., the deficit could widen further. The national debt recently went above $38 trillion and will likely top $40 trillion by next year. These factors could also soon begin to weigh on the US dollar, which looks to be approaching another downward leg.

Last month, Deutsche Bank’s top currency strategist, George Saravelos (whom I have much time for), warned that money managers in Europe could soon choose to trim their holdings in response to Trump’s threats on tariffs and the proposed acquisition of Greenland. Meanwhile, DJT indicated in late January that he’s comfortable with the dollar’s recent decline. He was later contradicted by Scott Bessent, the US Treasury secretary.

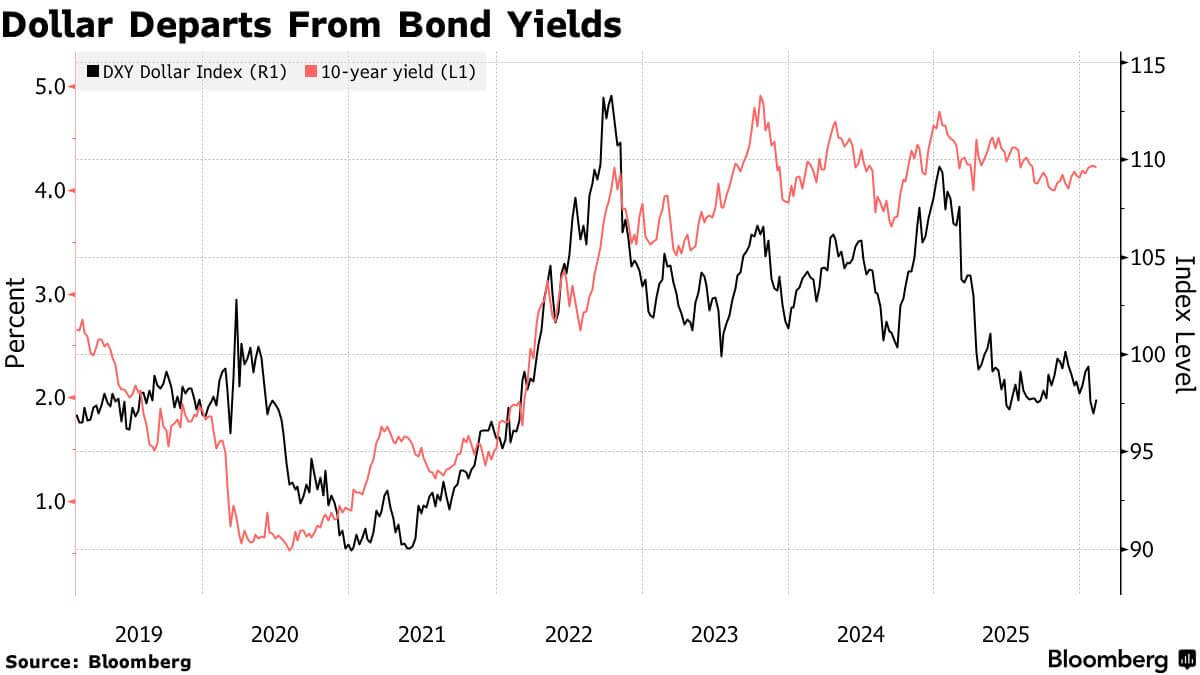

The US dollar is no longer tracking the 10yr bond yield, with the historic correlation breaking down…

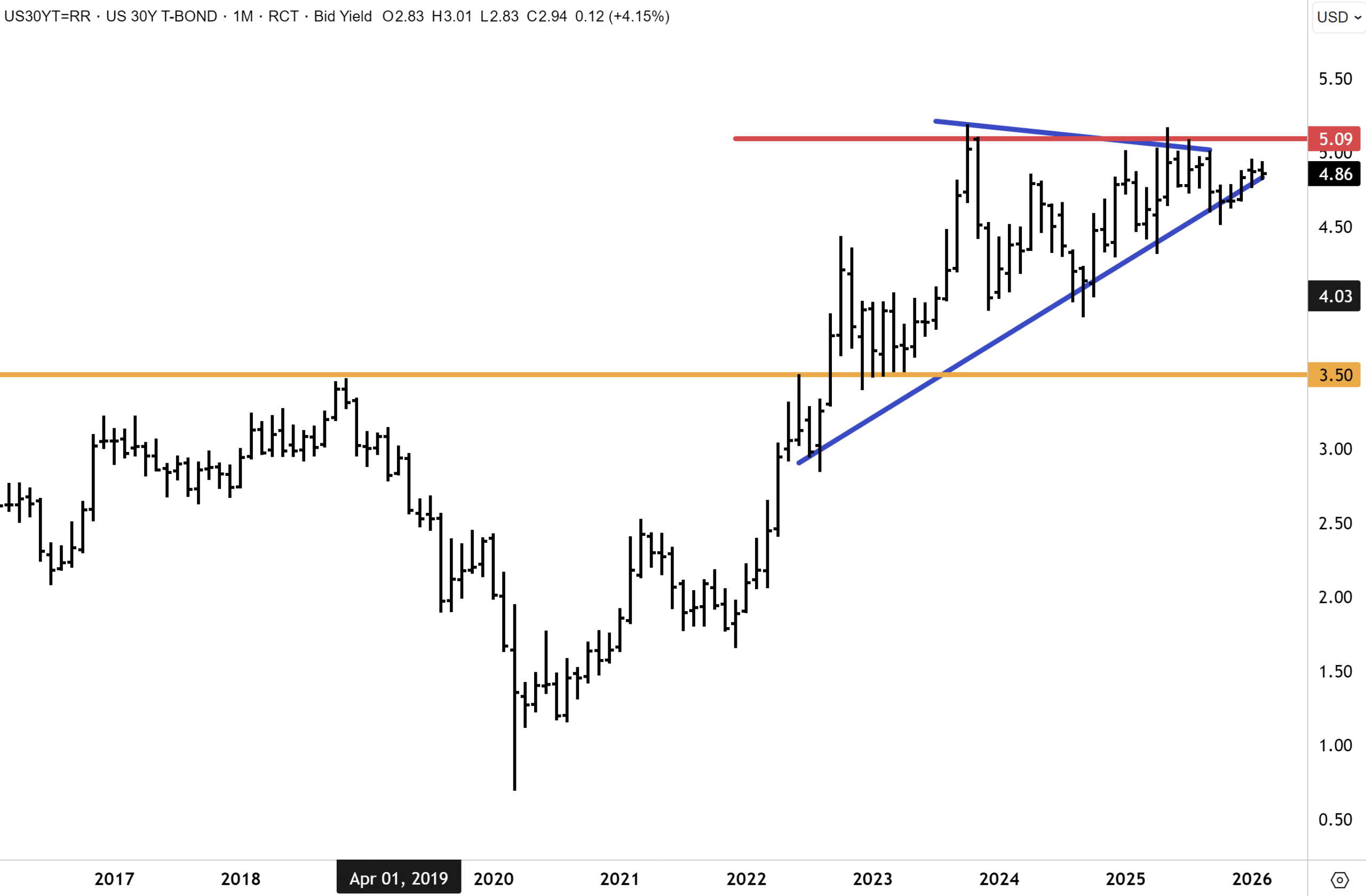

For now, the US bond market is stable, and yields have fluctuated in a narrow range. But I continue to watch the US30yr and expect the highs just above 5% to be breached sometime this year. Foreign holdings collectively accounted for a record $9.4 trillion in November, more than $500 billion higher than a year earlier, but I expect this to decline this year after the latest political wrangling over Greenland and more tariff threats. The bottom line is that the world is overweight US assets, which in itself is an outsized asset class of total market capitalisation when considering America has around 18% of global GDP. Placing eggs in different baskets makes a lot of sense. Diversification is therefore long overdue!

The technical setup for the US Treasury bond is decisively bearish in my view. The yield on the 30-year could rise well above 5% this year, if the 2023 high is breached on the topside.

Source: US Treasury Department

Source: US Treasury Department

Is the market under-pricing rate cuts?

I watched an interesting interview yesterday on CNBC with billionaire hedge fund founder and Greenlight Capital CIO David Einhorn. Mr Einhorn has successfully run a multi-billion hedge fund for several decades, and he has a contrarian disposition and often does the opposite of what Wall Street does. The hedge fund manager anticipates the Fed will deliver more rate cuts this year than what’s being anticipated, and that’s giving him greater confidence in gold, where his fund is heavily positioned. Rate cut expectations diminished this week following the much better-than-expected Jobs report data and lower unemployment rate, with market consensus pricing in a more than 88% chance the Fed will make two 25 bps cuts by December.

Mr David Einhorn on CNBC discussing the US dollar and gold, amongst other themes.

But Mr Einhorn believes that the market viewing the latest jobs figures as a reason not to cut is “wrong.” His view is that the number of rate cuts could be higher than that, due to Kevin Warsh – DJT’s top pick to succeed Jerome Powell as Chair, being able to persuade the FOMC committee to do so. He might well be right, given the imperative of the mid-term elections at the end of the year, and how much the Republicans have riding on retaining control of both the upper and lower houses in Congress.

Mr Einhorn said that “If we have 4% or 5% inflation, sure then he won’t be able to persuade people, but otherwise Warsh is going to argue productivity. Warsh is going to take the position of cutting even if the economy is running hot. I think by the time we get to the end of the year, it’s going to be substantially more than two cuts.” This is a non-consensus view, and if David Einhorn is right, then the dollar could descend faster and come under a lot more pressure into yearend. The hedge fund manager has owned a lot of gold exposure since 2024 and retains a bullish view.

The US dollar index has managed to rebound off five-year lows in the mid 95s and recover above 97. However, the technical setup still looks bearish. Whilst the Fed likely won’t cut again under Jerome Powell, when Kevin Warsh assumes the helm, it might be a different story. Two rate cuts this year would, in my opinion, weigh heavily on the US dollar. If David Einhorn is correct and the Fed cuts multiple times, the fallout on the dollar could be severe.

Mr Einhorn gained notoriety on Wall Street during 2008, when he bet heavily against Lehman Brothers just months before the investment bank declared bankruptcy. When asked about gold, he said, “Gold has actually gone up over the past couple of years as a result of ‘becoming the reserve asset’ to own among central banks around the world. US trade policy is very unstable, and it’s causing other countries to say we want to settle our trade in something other than US dollars.” Good points and ones I have been making for some time.

He went on to say, “In the long term, one reason to own gold is due to the fact that the current relationship between US fiscal and monetary policies doesn’t make any sense. Other major developed currencies around the world are ‘as bad or worse’ than the US. There are some issues that sometime over the next number of years could play out with some of the major currencies.” I could not agree more with David Einhorn, and it is not just the US, but many other countries are spending beyond their means, and they will keep spending and borrowing heavily.

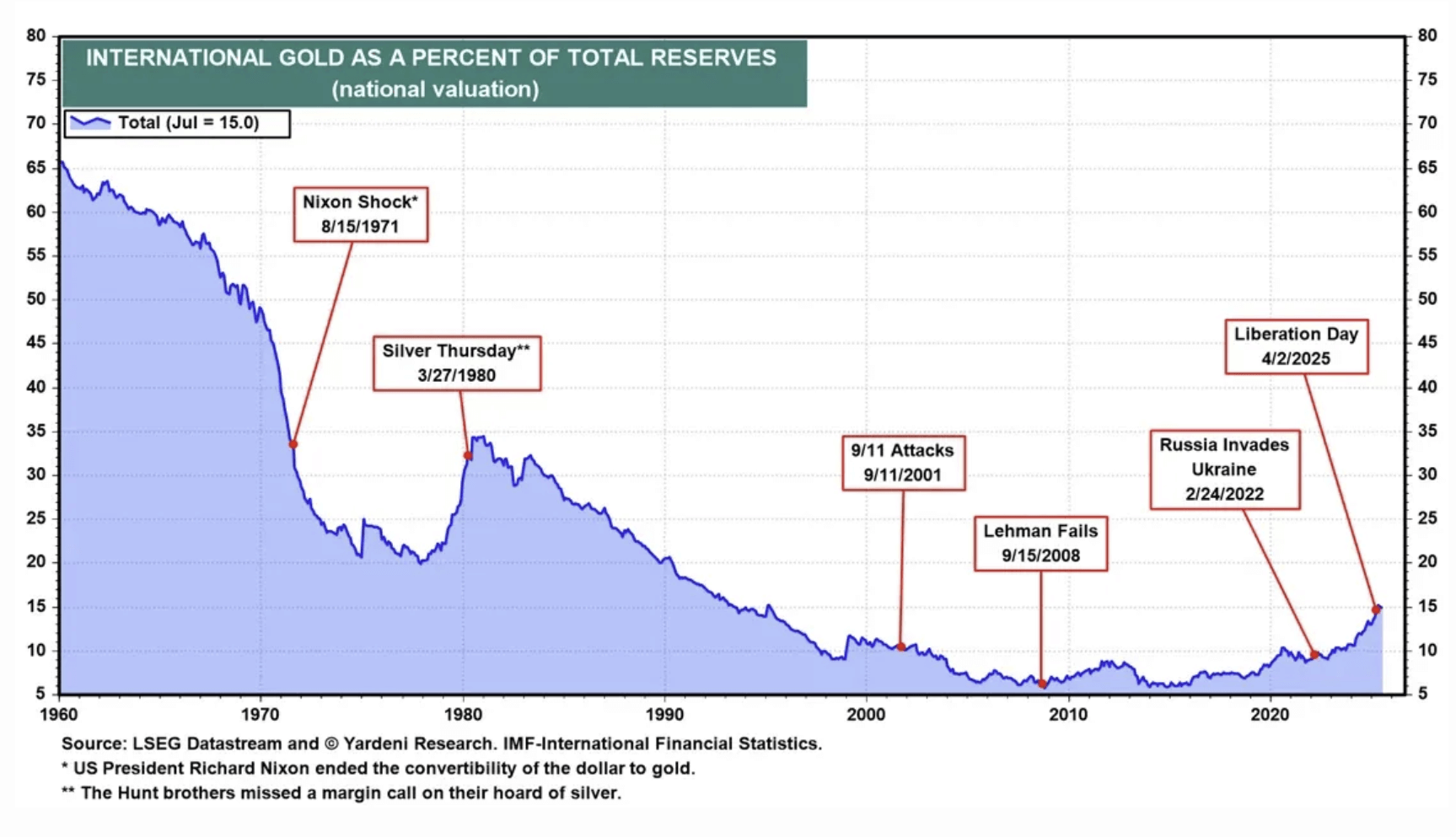

Trouble is coming for the global bond market in my view, and likely towards the end of this year or certainly in 2027. Gold will increasingly be seen as a hedge against not just fiat currencies, but also bonds, which could lose a lot more in value over the coming years. Many central banks can see this now and are actively recalibrating financial reserves and diversifying into gold, and this trend could continue for some time, given that gold as a % of total international reserves is still quite low, and well down on levels seen between the 1960s and 1980s.

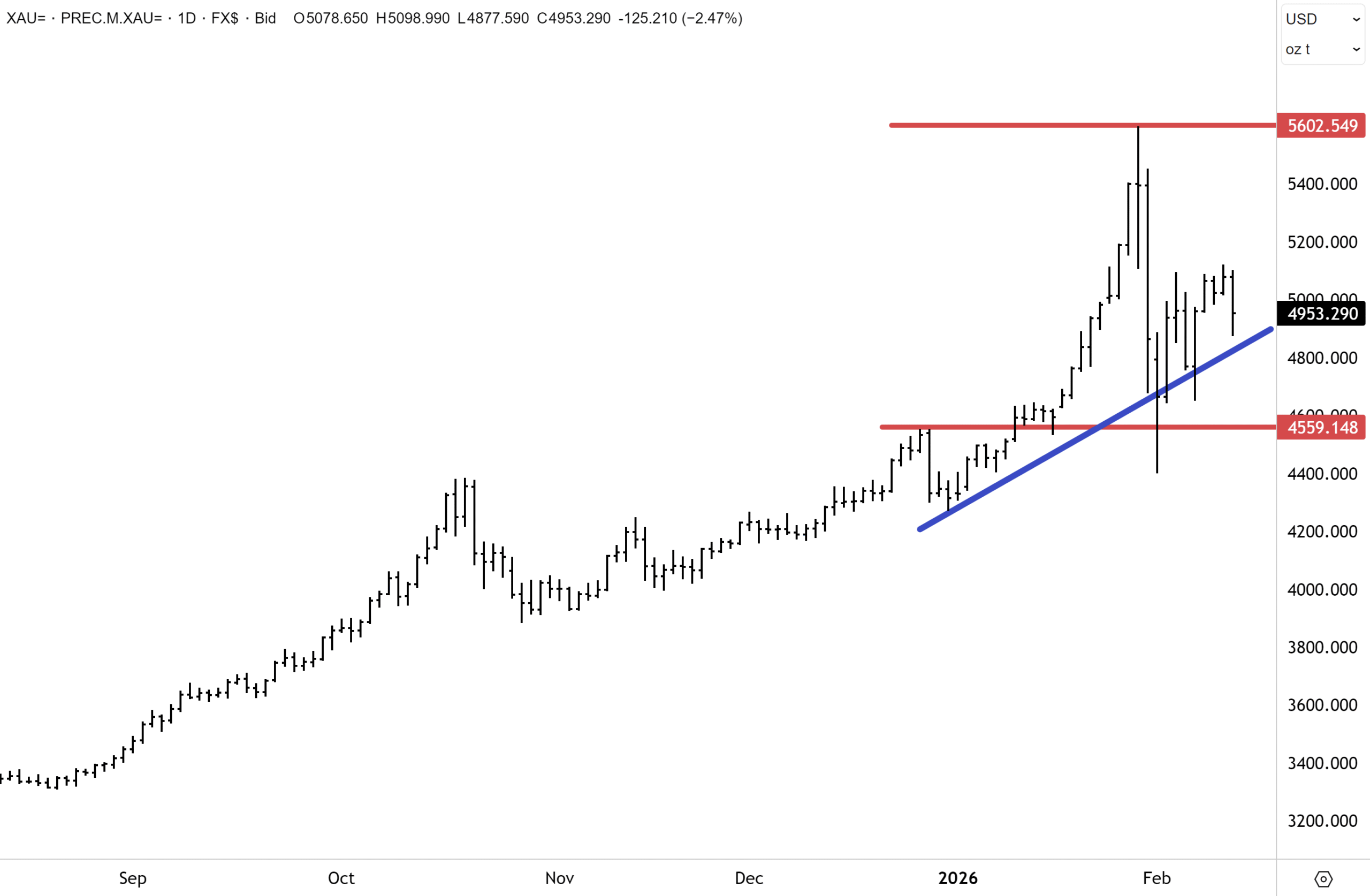

Gold has managed to consolidate quickly and constructively since the steep selloff at the end of January. I would not rule out more volatility, but the acute phase that occurred a few weeks ago has likely passed. Further consolidation is likely to be on the cards over the coming months, which is healthy for the bull market and will allow overbought conditions to be fully worked off.

In terms of the six-month spot chart, gold has established in recent weeks a series of higher lows, which is constructive. The bottom line, I expect gold to settle down into a new range and consolidate further before upward momentum resumes later this year.

An outside call!

Mr Einhorn concluded that betting on more rate cuts is one of the best trades out there right now. Mr Einhorn said he was also long futures on SOFR (Secured Overnight Financing Rate), which essentially is a bet that short-term rates will continue to go lower. Should the Fed cut aggressively this year, then the dollar could fall sharply, inflation could accelerate, and long-end bond yields could potentially soar. Gold under this scenario could, in my view, top $6,000. We are well-positioned across our portfolios for a weaker dollar, strong gold price, and higher inflationary environment. But the magnitude of Fed cuts this year remains to be seen.

The ‘Insurance’ Bid

Moving on, global markets have experienced sharp moves this year, with gold surging then seeing its biggest decline in four decades, Japan’s government bond market suffering a $41 billion meltdown, and the dollar and yen fluctuating wildly. I am of the view that gold is in a long-term bull market, but over the past month, had become quite overbought and in need of a healthy consolidation. I think this consolidation is playing out now and don’t envision gold taking out the record high above $5,600/oz anytime soon, but quite possibly later this year or in 2027.

Treasury Secretary Scott Bessent waded into the debate on gold and said that Chinese traders were a key reason behind last week’s wild swings in the gold market. In an interview on Fox News, Mr Bessent said that “The gold move thing — things have gotten a little unruly in China. They’re having to tighten margin requirements. So gold looks to me kind of like a classical, speculative blowoff.”

Mr Bessent was responding to a question about the record-breaking rally in precious metals — fuelled by widespread central bank buying, geopolitical turmoil and concern about the Fed’s independence — which Mr Bessent shrugged off. Mr Bessent has to tow the official government line, which is why he refused to concede that the US has a weaker dollar policy. His comments were to be expected – but taken with a grain of salt. I also disagree that gold has had a final blow off top, but do anticipate a much-needed period of consolidation where the price needs to establish a new (albeit higher) trading range.

Goldman Sachs came out with an update on gold this week and stated that the historic rally isn’t just about precious metals. “It’s part of a broader shift in how governments and investors are treating commodities. Central bank buying has helped drive gold’s surge in recent years as governments seek to hedge geopolitical and financial risks. Now, similar “insurance”-style strategies are emerging across other commodity markets.”

This was an interesting comment, and we have been highlighting for some time that commodities will enter a super-cycle phase that could playout over the next five years. Part of our bullish view is also linked to a weaker outlook for the US dollar. Goldman, however, has gone one step further and said nations are stockpiling commodities and diversifying away from financial reserves.

Goldman noted that “As some of these risk-management policies have taken hold, some commodity markets appear to be transitioning — at least temporarily — from a single, global balance toward more regionally segmented systems, raising the risk of higher volatility. That shift stems from recent supply shocks. After 2020’s supply-chain disruptions and 2022’s food and energy shocks, policymakers focused on securing access to critical materials. That has included tariffs, export controls, support for domestic production, and the buildup of government stockpiles. Together, those measures are reshaping commodity markets in ways that can make prices more sensitive to shocks.”

Goldman highlighted copper as an early example. Despite expectations of a global oversupply in 2025, prices surged as US stockpiling pulled material out of international markets. That left markets outside the US, where global benchmark prices are largely set, with much tighter inventories. Silver has been another example, with inventories at the Shanghai and London Metals exchanges plunging to historic lows.

Goldman also made the point that the dynamic isn’t limited to just governments. “Recent client feedback suggests that insurance-type demand for several commodities — not only gold but also industrial metals such as copper — has broadened beyond the public sector, as private sector investors turn to hard assets for diversification in an uncertain global policy environment. Those investor flows are supporting metals prices and amplifying volatility.” I agree with Goldman and would also add that the weakening US dollar is also boosting demand for commodities in many emerging markets.

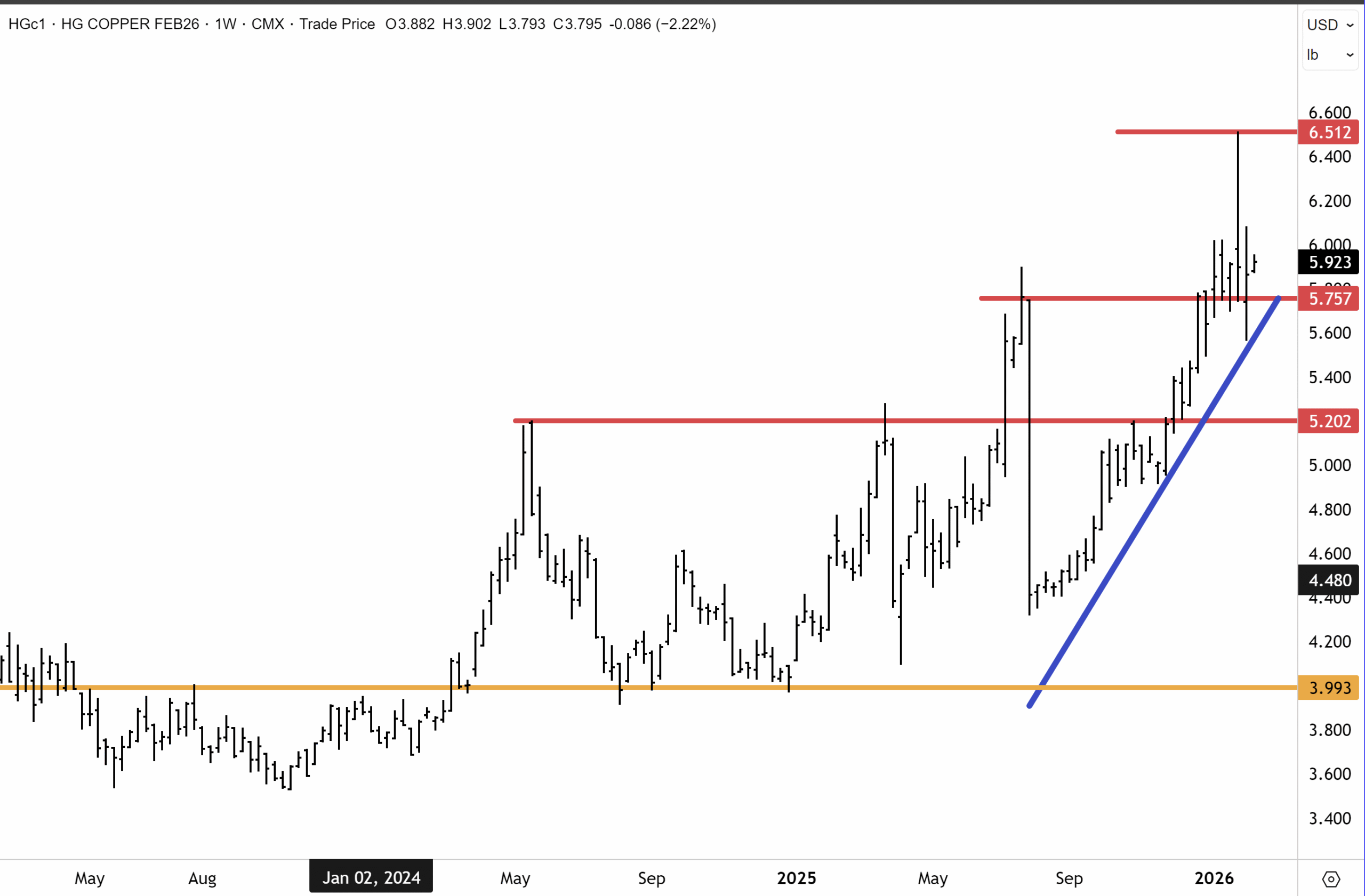

Copper has consolidated constructively since breaking out to new record highs this year. Whilst a correction ensued at $6.50, copper is finding solid support at $5.90 and below. This setup favours copper reclaiming a ‘6’ handle in the coming weeks, in my view.

The investment bank said that gold was different. “For most commodities, supply can adjust when prices rise. Producers often ramp up output, helping cool price spikes driven by “insurance” demand. But policies aimed at making supply more secure can also encourage overproduction. That can push prices lower, drive out smaller producers, and leave supply more concentrated, increasing the risk of future disruptions and sharp price swings. Gold, however, remains structurally different.”

I highlighted the same point a few weeks ago. Nearly all the gold ever mined still exists above ground, and the annual supply is relatively stable and slow to respond to price moves. That means demand driven by risk concerns can keep pushing gold prices higher for longer. JP Morgan recently upgraded their 2026 price target upwards to $6,300oz.

I would also add that central banking demand could have a long way to go. Gold held as a % total reserves has been rising in recent years, but remains well below the levels seen between 1960 and 1980. I have conviction that while history doesn’t always repeat, in financial markets it often rhymes. We could see a similar cycle to the 1970s (and also between 2000 and 2011) playout when gold entered a bull market and increased by multiples as the US dollar weakened.

Source: Yardeni Research

Source: Yardeni Research

Small Caps Have Their Day

Morgan Stanley Chief Strategist Mike Wilson highlighted this week in a note to clients that the “Equal Weighted S&P 500 and S&P Small Cap indices broke out to new highs last week, led by cyclicals”. This is a clear sign that the US bull market is broadening out, which is healthy and also a sign that a major drawdown this year (barring a left-of-field event) is unlikely this year. Corrections will, of course, occur, and we might see one or two this year between 5% and 10%, but the US indexes technically look to be setting up for another advance higher this year. The same can be said of the international equity markets, many of which are beating the US this year by “a sound margin”. I remain bullish on emerging markets in 2026, and notably China/Hong Kong.

The very strong earnings season is one reason the US benchmarks are stable and likely to track higher. The December quarter reporting season has not only driven another strong round of beats, but this is coming from nearly all corners of the US stock market. Mike Wilson cited that “earnings growth for the median stock in the Russell 3000 is +11% Y/Y, which is the strongest growth in 4 years…The S&P Small Cap Index is seeing its best revisions breadth since August (+7%) and its strongest EPS growth since 2022 (+10%). Further, it just made a new relative high versus large caps last week. These developments are supportive of our small-cap relative preference amid a return of positive operating leverage.”

Small caps generally only do well in a risk-on environment. What has been interesting about the last few months is that market leadership has been wrestled away from Mag 7 and technology stocks, with the Russell 2000 breaking out to new record highs and leading the US market. Earnings strength is behind the move, and for this reason, I remain bullish on the S&P493 (ex mag), and Russell 2000 playing catch-up this year as the “great rotation” continues.

The Great Tech Rotation

Some pockets of tech have performed very badly, and this has been a rout not just occurring in the US, but a global phenomenon. Investors have become concerned about the disruption AI will cause and potentially displace many technology companies. At the centre are the “Software as a service” or SAAS companies. Some of these companies are down 50% to 70%, such as well-known names including PayPal.

Morgan Stanley believes this is now overdone for SAAS companies. Mike Wilson noted this week that “despite last week’s volatility in Tech, we remain constructive on the sector”. MS believes that “forward revenue growth expectations for mega cap Tech have accelerated to multi-decade highs (+18%)m and that earnings revisions breadth across Semis, Software, Tech Hardware, and the Mag 7 has started to rebound over the past 2 weeks.” The CIO also noted that the US dollar is down 9% year on year, and this will provide a tailwind for mega cap tech, which derive 50% of revenues outside the US. I have made this point on a number of occasions, and the dollar could decline even further this year, which would be bullish for US multinationals.

In terms of the SAAS companies, an opportunity is potentially going to arrive soon. A catalyst and circuit breaker could be earnings. Companies that beat soundly are likely to be sharply rerated by the market, which perhaps has been too bearish. We hold tech companies in our portfolios that include Grab, Tencent Music, WiseTech, Xero, and Money Forward that could also soon stage dramatic rebounds, given there has been no significant change to underlying company fundamentals.

US strategist Ed Yardeni also waded into the debate and highlighted this week that the indiscriminate selling looks overdone. Ed has been cautious towards technology and Mag 7 names since last year and advocates underweighting the sector. But he made a good point this week, saying that “we believe the selloff in software and financial company stocks has been overdone because they will use AI to lower costs and deliver better products and services to their customers.”

I also concur with this point, in that many established technology and SAAS companies have reasonably large moats and could prove hard to dislodge by AI disrupters. However, the pendulum has clearly swung in the market, and many investors have headed for the exits. Momentum is still clearly to the downside, but an opportunity could emerge in the coming months as valuations become cheaper and multiples compress. However, with momentum still to the downside, I would advocate waiting on the sidelines and letting the dust settle.

Yardeni Research recommends overweighting financials, and the “old economy” Industrials and Health Care sectors. Mr Yardeni is bullish on precious and base metals and is now overweighting the Materials sector, which is a view I certainly share. He also this week recommended overweighting foreign stock markets, particularly those of emerging markets, which is a view we have held for some time.

Report Spotlight

Better Foundations – James Hardie

James Hardie delivered the quarter it desperately needed, with shares surging 13.6% after Adjusted EBITDA of US$330m beat consensus by 6% and landed comfortably above the top end of guidance (US$298m–US$318m). For a stock battered by AZEK acquisition concerns and soft US housing, this upside surprise mattered.

The core Siding & Trim business showed genuine operational resilience. While organic volumes were down as US single-family construction remained weak (particularly in the South), pricing held firm, mix was favourable, and margin recovered sharply. Adjusted EBITDA margin of 34.1% was only modestly below last year, with management highlighting nearly five percentage points of sequential margin expansion versus September. Volumes are soft, but the business isn’t losing pricing power or cost discipline under the Hardie Operating System.

The AZEK segment (Deck, Rail & Accessories) is tracking better than feared. Sales grew modestly on price and mix, margins sat at a healthy 25%, and crucially, synergies are already ahead of plan, explaining why group EBITDA beat expectations.

We have conviction that James Hardie is close to confirming an important inflection after passing through last year, which we believe was a bearish extreme and a major bottom in the stock. JHX has this week broken out above the primary downtrend at $35.60, which points to upward momentum resuming, and if sustained, we would have confidence that an inflection will then be confirmed.

The next price target for JHX is the overhead resistance cluster above $45. We continue to have confidence in the recovery potential for JHX over the coming year if the US housing market rebounds (our base case). We believe a significant technical buying opportunity is still open for those investors prepared to take at least a one-to-two-year view.

This isn’t a housing boom yet, though our base case is that the Trump administration will continue to push policies supportive of the US housing market. Risks remain (leverage, organic volume softness), but the balance of probabilities shifted in favour of the bull case after this result. We continue to view JHX (ASX: JHX, US: JHX) as attractively priced on a risk-to-reward basis. BUY for those without exposure.

The Fat Prophets Global Contrarian Fund updated the ASX this morning and noted the following about the global selloff in tech stocks:

“Selling in global technology stocks deepened this week as investors fear that coming AI disruptors will dislodge many established companies. Whilst we believe the selling is somewhat overdone, downward momentum in the global tech sector might continue for some time…Our focus in the portfolio continues to be on China technology companies, which have lower valuations, and have generally held up much better. We have noted the high valuation discrepancy between US and Chinese technology companies for some time. Sequentially, we still see Chinese tech stocks as a relatively safer harbour.”

The Fund is performing well in February, which follows a solid performance in January and over the course of last year. It has been encouraging to see new shareholders on the register, which continues to tighten up, especially amongst the top 50.

This report and many others spanning Australasia, Mining and Global Equities are available online for your reading pleasure in the Members area, should you be interested in subscribing for investment snapshots and deep dives across a range of investment vectors, along with our regular Daily correspondence on the markets.

Have a great weekend.

Carpe Diem

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.