According to RBC Capital Markets, investors should take cover from a protracted selloff in the US dollar that could “mirror the boom-and-bust cycle of the Internet bubble once the drivers that are supporting the currency turn into headwinds”. At yesterday’s FPC AGM, I discussed our outlook for the US dollar and emphasised that, near term, the dollar might continue to rally from oversold conditions after one of the steepest annual declines on record.

The dollar has been hit hard this year by uncertainty associated with government policies, which are isolationist and have pushed key trading partners away. De-dollarisation trends, however, will likely persist for years to come. RBC Capital Markets believes that support from a soaring stock market and US asset allocations from global investors, chief among them mammoth, passive investment funds, could unwind in the coming years.

I also emphasised this point yesterday, given that US stocks now account for +70% of global stock market capitalisation versus GDP, which is tracking at around 28%. Foreign investors, meanwhile, are skewed heavily towards the US in terms of global portfolio weights. Is the rest of the world that unattractive?

RBC made the point that over the last two decades, these global players have favoured increasingly expensive US assets, particularly stocks, with flows in turn favouring the dollar. “This concentration worked well in the past 15 years but poses risks in the current environment. A measurable change in demand (and relative performance) can have profound implications in FX.”

Once capital diversifies away from the US – as the outlook for the rest of the world improves – I would expect downward pressure to reassert next year on the dollar. Many foreign investors will have no choice but to hedge and sell the dollar to protect returns on US assets. We saw this cycle play out during the internet bubble, which, after it began deflating in 2000, saw the dollar sink 40% peak-to-trough between 2001 and 2008.

RBC highlighted that the 2000s experience offers “valuable guidance” and cited that high valuations, changing trade paradigms and shifting safe havens are among the challenges for the dollar over the next few years. The “longer-term tail risk on the dollar should be top of mind as we move into 2026.” I concur, and investors with overexposure to US assets and Mag 7 names should consider hedging out FX risk.

The RBC analysis also highlighted how today’s environment differs from the 2000s, particularly given the rise of illiquid and private-asset investing that can exacerbate swings across financial markets during times of market stress. “The historical lessons from the post-2000 period provide valuable guidance, but today’s unique combination of technological change, geopolitical tension, and monetary policy experimentation requires some adaptation as allocation frameworks are no longer traditional.”

The US dollar index made three notable bull market peaks in the past 45 years, in 1981, 2000 and in 2021. Equally, there have been three notable bear market troughs – in the early 1970s, early 1990s, and in 2011. One key observation is that each peak has been sequentially lower, while the 2011 market reached a new historic low. It is worth considering that once the primary uptrend in place since the 2011 lows is definitively broken, the Dollar Index could retest or even make new historic lows that are proportional to what played out in the 2000s. Each cycle took a number of years to play out, and I don’t see the DXY falling 40% next year.

However, I have conviction that this scenario has a high probability of occurring over the next five years. This year’s sharp decline is a warning of what could come down the line. (I emphasised at yesterday’s AGM that we are not trying to trade the incumbent correction in gold, PGMs and other select commodities, given we are there for the longer term).

Whilst US technology stocks and Mag 7 names are expensive, and over-owned with crowded positioning, opportunity is knocking in China. Yesterday, Chinese Premier Li Qiang suggested his country’s economy will maintain the current growth pace. He said that China was an attractive market for global companies as Beijing seeks to mitigate concerns over trade imbalances. I agree with the Premier that global investors are not yet buying China and remain chronically underweight in the world’s second-largest economy. It was only a few years that Wall Street considered China “un-investible”. This contrasts starkly with the overweight global positioning at the top of the previous bull market, back in 2021. I see this dynamic as a powerful tailwind for Chinese equities, however.

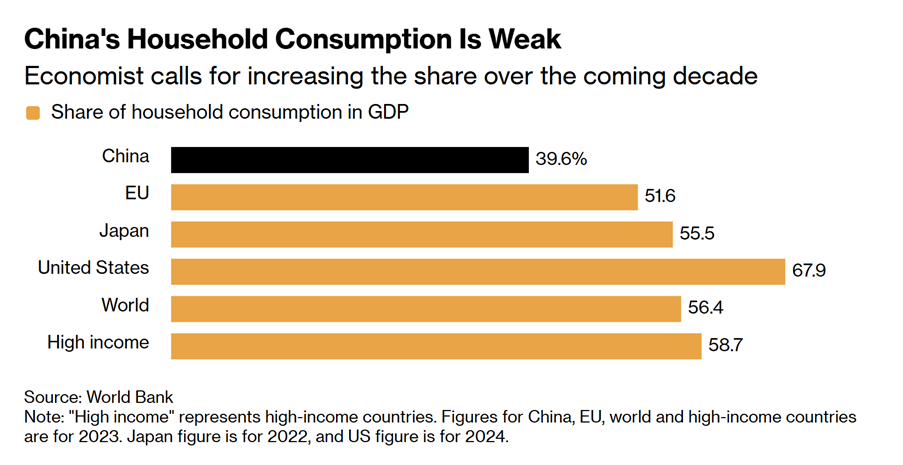

Mr Li said GDP is expected to surpass 170 trillion yuan (US$23.9 trillion) in five years, implying an average annual growth rate of about 4% through 2030 without adjusting for price changes. Mr Li said that the increase represents “new significant contributions to global growth” and stressed that “China would focus on expanding domestic demand, especially on boosting consumption” to unleash the potential of the market.

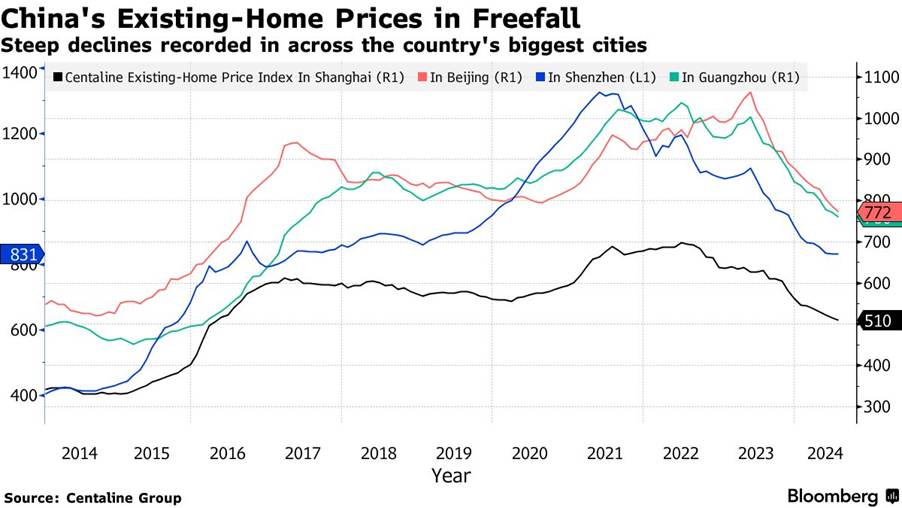

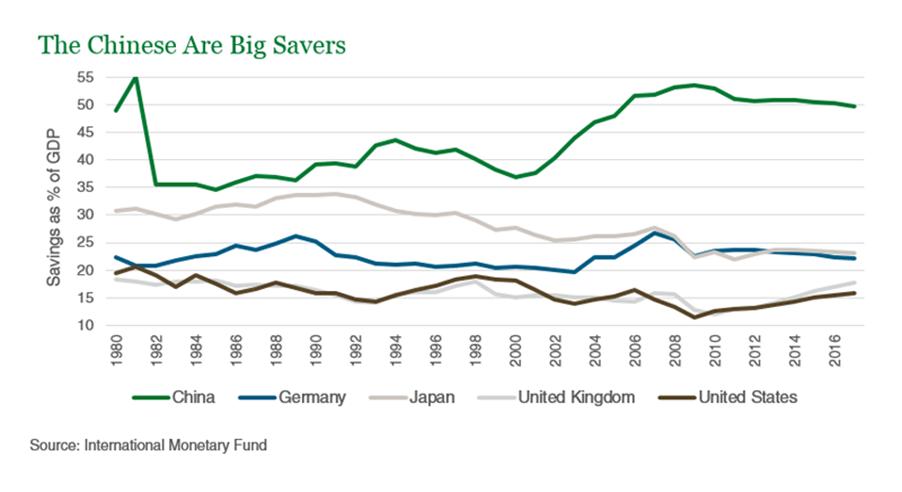

With around US$18 trillion in cash and short-term deposits, China’s population has the largest savings in the world – by a significant margin. This buildup has been due to the downturn in the housing market and the fact that China lags the developed world on social security and safety nets. Up until 2021, many Chinese relied on housing and residential property as a core foundation for retirement. The massive accumulation in savings has been a direct byproduct of the downturn in the housing market.

But this dynamic could all change in the years ahead. When Beijing eventually gets it right in terms of policy settings and finally unleashes consumer spending and pertinently, the impact US$18 trillion in savings on the domestic economy (and stock market) could be transformational.

Yesterday, Premier Li Qiang reaffirmed plans to boost the economy and lure investors during a speech at a trade event in Shanghai. While he didn’t give a precise target, I have confidence that the government sees this as a top priority. China is on track to achieve its real GDP growth goal of about 5% this year, but nominal expansion has been slower due to falling prices.

Persistent deflation has come from falling house prices – but also tepid consumer spending. In China, consumers have delayed purchases to reduce debts, but the fallout has been on profit margins, which have been squeezed. This in turn has led to excessive competition in the market, weaker spending and lower investment – in a deflationary spiral. The government needs to break this cycle.

“Breaking this cycle” appears to have now become the top policy priority. Beijing has launched the “anti-involution” policy targeted at excessive industry price cutting and over production in an attempt to stamp out the price wars. At some point, the government will succeed, but it needs to stabilise the property market as well and make this also a priority.

The government plans to “significantly” boost consumption’s contribution to the economy and increase spending on public services, and work on promoting employment according to basic principles for the next five-year plan starting in 2026. The new language signals a growing resolve on the part of China’s policymakers to promote consumption among its 1.4 billion people, as some countries push back on cheaper goods flooding global markets.

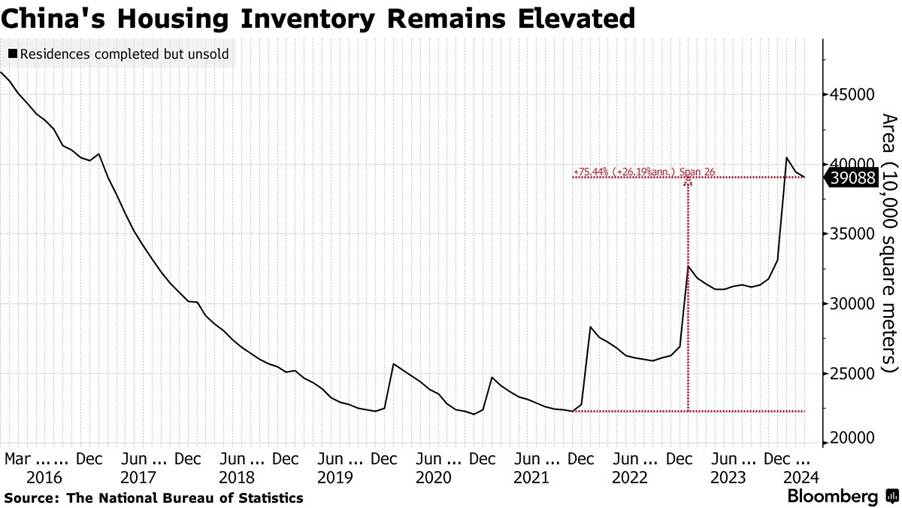

A good start towards achieving this goal is clearing the residential housing inventory overhang, with oversupply presently running at around 3 to 4 years and around 20 months in major cities.

On this front, top-rated analyst at UBS Jon Lam, who heads China and Hong Kong property research at UBS Asia, holds a more optimistic outlook for later in 2026. I hold a lot of regard for Mr Lam, who correctly called the top of China’s housing market in 2020/21 and advised investors to exit. He now expects home prices in top-tier cities to “turn stable” by mid-to late 2026.

Mr Lam has cited that he expects the major cities to rebound first and then filter down to regional cities and the rest of the country, and the growing importance of real estate investment trusts (REITs) as a structural shift. I think owning Chinese property developers and REITs is still too early, and we have a strong preference for technology companies, primarily the bellwethers that will benefit from AI.

But the bottom line is that when the property market does inflect, and likely next year, then we can expect consumer demand to have a resurgence with significant pent-up demand. For every $1 that gets spent of the $18 trillion tucked away in savings accounts, there is a multiplier effect. The inflection in consumer demand that is coming could be transformational for the Chinese economy and stock market when it finally arrives.

An outside call

Legendary hedge fund investor and billionaire Ray Dalio was back on the soapbox advocating his views that the stock market is headed for “one last hurrah” before the bubble bursts. I have a lot of time for Ray Dalio, even if his views can be somewhat extreme. He is a student of financial markets history and often finds patterns that may not always repeat but often rhyme.

Ray Dalio, 76, founded Bridgewater Associates in 1975 from a small New York apartment and grew the business into the world’s largest hedge fund, which at its peak managed over $160 billion. He is regarded for global macro investing and famously predicted major events such as the 2008 GFC. Mr Dalio stepped down as CEO, CIO, and chairman in 2022, but I still follow his comments about the financial market, which include a lot of philosophy, history and observations on human behaviour.

This week, he sounded the alarm again over what he sees as the dire state of the US economy. Mr Dalio’s main concern in recent months has been the impact of soaring US debt levels and high deficit spending, but now also warning on the path of monetary policy.

Mr Ray Dalio

The hedge fund manager is very concerned about the Fed and that “easing interest rates will stimulate a dangerous bubble in markets and the economy — and the market could see one final surge before it bursts.” I share a lot of his views, although I see events maybe taking longer. I also believe that some equities/stocks are not necessarily going to be a bad hedge against what is likely higher inflation down the line and coming turmoil in the US dollar and FX markets.

Ray’s analysis and framework for markets is focused on the incumbent and growing large-scale debt cycle in the US and other major economies. In his most recent observation, Mr Dalio argues that the Fed’s decision to move toward more dovish policy marks the final stage of the big debt cycle. “It would be reasonable to expect that, similar to late 1999 or 2010-2011, there would be a strong liquidity melt-up that will eventually become too risky and will have to be restrained. During that melt-up and just before the tightening that is enough to rein in inflation that will pop the bubble is classically the ideal time to sell.”

He might well be right about next year, and if the Fed does move to aggressively ease rates next year, combined with a lot of euphoria around AI, we could see the bull market shift into top gear, which eventually leads to a sharp selloff at some point. But markets are not at that crossroads yet. And equally, we could also see another sharp decline in the US dollar next year with favourable tailwinds for gold and a lot of commodities.

Ray Dalio believes that aggressive Fed easing next year would prolong the bull market and the upward trajectory of tech stocks in particular, driven by the ongoing AI boom. However, he also believes that it will be short-lived, and if history is any guide, the bubble is destined to burst. Dalio also offered tips on the stocks he thinks will benefit once economic conditions shift and prefers “tangible asset companies like miners, infrastructure, real assets would likely outperform over pure long-duration tech once inflation risk re-awakens.” I would agree with that comment, and for investors with little or no exposure to gold and precious metals, would take advantage of the incumbent correction/consolidation to selectively add exposure.

Finally, James Hardie crashed -12.7% yesterday but finished above intraday lows and right on key historical support at the 2023 lows. The stock went into a trading halt briefly and responded to an ASX price query, saying the sharp fall may have been due to the announcement that the locally-listed CDIs have been removed from MSCI’s Australia index. Certainly, passive flows linked to index inclusion are a notable factor, but the fall overnight in Owens Corning and Trex (both operate in the building materials industry) after poorly-received results and commentary also looks to have been a factor.

JHX has come under severe pressure this year, but the selling certainly looks overdone at these levels. I would also add that James Hardie has an entrenched position in the US with close to 45% share of the fibre cement cladding and engineered timber flooring market. Both businesses continue to grow strongly and capture market share from other industry competitors.

The US housing sector has been in a slump despite an acute and growing shortage of homes. The present US housing shortage in 2025 is estimated to be around 2.8 to 4.7 million homes, with the higher end cited by sources including the US Chamber of Commerce. This deficit is the result of years of underbuilding relative to population growth, and recent construction booms have not yet been sufficient to close the gap. Over 1.6 million homes were completed nationally last year, but this barely kept pace with new household formation.

The shortage is most pronounced in major metro cities such as New York, Los Angeles, Boston, San Francisco, and Washington DC, each with six-figure deficits. Closing the shortage is projected to take up to a decade, assuming steady annual construction growth. I can’t get too bearish about James Hardie, particularly given the growing underlying trend towards using fibre cement in cladding and engineered timber in decking and flooring.

With the US labour market now rolling over, significant easing from the Fed is likely coming. I hold conviction that US mortgage rates will come down rapidly next year, which could set off one of the biggest housing booms since the 2000s. Combined with the fact that there is an acute housing shortage and significant pent-up demand, the recovery in the US housing sector could deliver a significant upside surprise to the market.

In terms of the JHX share price, many institutional shareholders have exited or reduced positions. I sense an opportunity for those investors willing to hold JHX for a year or so, until the recovery in the US housing market takes hold. Many ‘insto’ investors were very upset that JHX management merged with Azek and paid a premium. These shareholders had a point, but this is now in the price, and JHX shares have fully discounted this.

I have used the chart below of James Hardie ADRs in the US and not Australia for a key reason. The US market is now the bigger market for James Hardie shares, both in terms of trading volume and strategic focus. Historically, James Hardie’s primary listing was on the Australian Securities Exchange (ASX), but as of 2025, the company has announced plans to shift its primary listing to the New York Stock Exchange following the Azek acquisition. The shareholder base is now dominant in the US, with daily trading volumes on the NYSE exceeding those on the ASX. In recent trading in JHX, over 15 million shares traded in the US compared to 2–3 million on the ASX.

This is an outside call…but I would not be surprised if Berkshire Hathaway shows up on the JHX share register in a few months. The company likely ticks a lot of boxes for the sage of Omaha, who has spent a lifetime building a career around buying “great businesses at attractive prices”. Let’s see.

James Hardie ADRs fell yesterday to US$17.48 to retest the 2023 lows when the housing market was in real trouble due to the Fed putting through the fastest pace of rate hikes. Today, the opposite framework is in place. There is a good probability, in my view, that the 2023 lows will hold. A downside break below this level could see JHX extend lower towards the next major support around $15, but this remains to be seen.

A very dire outlook on the merger and the US housing market has now been priced into JHX, which, in all likelihood, doesn’t actually reflect reality. I might be totally wrong on JHX, but the risk/reward skew at the current share price seems highly favourable to me. Disclosure: I bought some JHX for my personal account a few weeks ago at higher levels and will consider adding more to this position today.

Carpe Diem

Sign up to receive full reports for

the best stocks in 2025!

Where to Invest in 2025?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.