The next steps

Sonic Healthcare shares took a hit after the recently reported 1H24 results, interrupting a fledging recovery that began playing out in late 2023, as top-line growth was overshadowed by a sharp fall in earnings. The collapse in pandemic-related revenues made for a stiff headwind in what CEO Colin Goldschmidt calls a “transition” year. Still, some notable cost increases squeezed margins, and net interest expense picked up.

Sonic maintained the FY24 EBITDA guidance range of $1.7 to $1.8 billion provided in August 2023, though it is now expected to lean towards the lower end of this range. A Belgian fee cut and FX headwinds were drags. Even at the lower end, this implies management is anticipating a material improvement in 2H24, given the $737 million in 1H24 EBITDA only constitutes roughly 43% of the lower bound.

Whether this is achieved remains to be seen; we don’t think it will be easy. However, given the lower bar, we anticipate a material improvement in the second half and beyond. We certainly back the senior management at Sonic, who has grown the business explosively over three decades from humble beginnings. Sonic now command a dominant share in the Australian market, followed by a leading share in Germany, the UK and Switzerland, while achieving a commendable third place standing in the competitive US market.

Despite the waning of the Covid-related business, Sonic remains well-positioned to capitalise on the favourable growth prospects inherent in the healthcare sector. The diagnostic imaging segment typically showcases resilience across economic cycles. The company is advancing sophisticated digital and AI capabilities. These should dramatically improve efficiency in the years ahead, alleviating the recent cost pressure, as should the bedding down of the recent acquisitions. On that note, the windfall from the pandemic left Sonic with a robust balance sheet, providing a platform for a pipeline of bolt-on acquisitions.

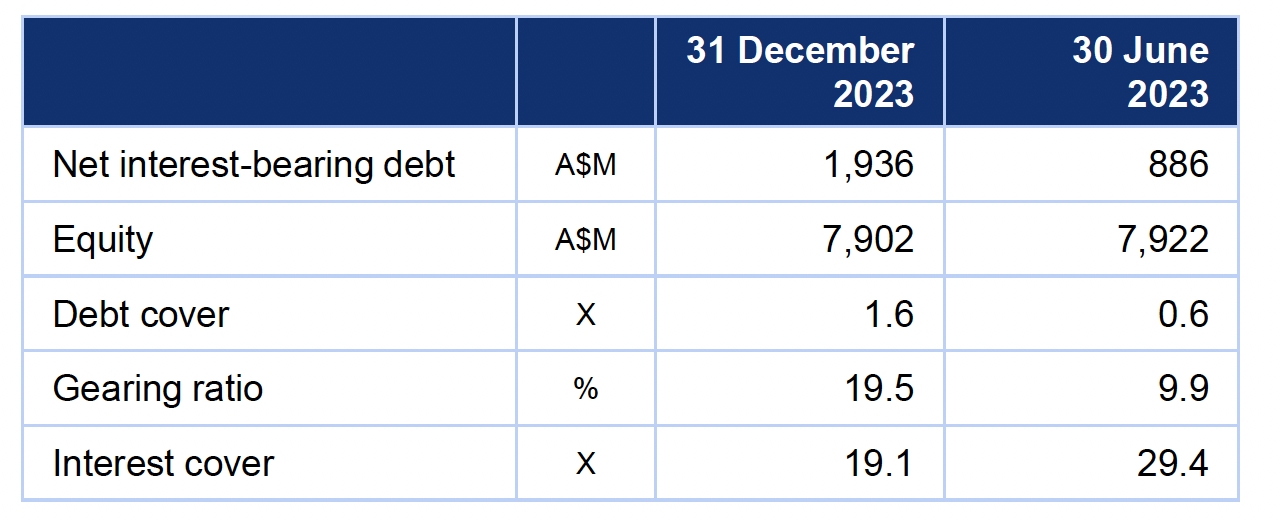

While Sonic’s debt levels rose over the past six months due to ~$0.9 billion in acquisition spending, the balance sheet remains healthy, with around $1.5 billion in available headroom.

Source: Sonic Healthcare

Source: Sonic Healthcare

Given Sonic’s current market valuation, we perceive these attributes to be overlooked, presenting a robust investment opportunity for those seeking a steady dividend grower. Stocks like Sonic and the broader healthcare sector should attract more interest as the market anticipates looming rate cuts from the RBA. As a defensive sector, healthcare has been vulnerable to elevated bond yields.

Meanwhile, the compression in the valuation and downward revisions from the brokerage community have significantly lowered the bar for future outperformance. Along with some other company-specific elements we view positively, we rate Sonic Healthcare a buy.

Despite the pullback, support from the primary uptrend looks solid for Sonic Healthcare, which should hold and drive a rebound over the coming year. [subscribe_to_unlock_form]Only a breakdown below the primary support level would raise the scope for further corrective downside. The shares have tested and held above the primary uptrend numerous times, as evidenced by the 20-year monthly chart below.

1H24 headline numbers

Total revenue increased 5.5% year-on-year to $4.3 billion in the six months ended December 2023. A headwind was the plunge in Covid-related revenue to just $37.4 million from $378.6 million a year earlier. This masked the robust 15.2% increase in base revenue to $4.09 billion. This Covid-related headwind is now primarily a spent force and won’t have a (material) drag from FY25. Base organic growth in the half year was 6.2% (with this pace continuing in January), while some $500 million in revenue stemmed from acquisitions and new contract wins. Management noted that they are running the ruler over more acquisition opportunities. Organic revenue growth was strong in the core Australian business (+9%), the UK (+13%), Germany (+8%) and the Radiology division (+11%).

EBITDA fell 20% to $737 million, notably below consensus expectations. The typical weighting towards more robust 2H performance is expected to be enhanced in FY24. Statutory NPAT almost halved (-47%) to $202 million as there were hefty increases in labour (and related costs), consumables, transportation, utilities, borrowing costs expenses and others. Earnings per share fell 47% to 42.6 cents. Still, the interim dividend was given a 2.4% bump to 43 cents per share, reflecting management confidence.

Management has set out cost-reduction programs across the company to tackle elevated costs resulting from the rapid growth seen during the pandemic and recent acquisitions. In addition, there are synergies to flow through from those acquisitions. Combined with digitisation efficiencies to come, we see the scope to fatten up margins materially from the levels seen in 1H24.

In summary, aside from the top-line momentum for base revenue, there wasn’t much to like in Sonic’s 1H24 numbers on the surface. However, there were more favourable underlying elements when digging below the surface, with the EBITDA performance being more heavily weighted to 2H24. Meanwhile, there is significant scope to lift margins from these levels, which, combined with top-line growth, could see a step-up in FY25 earnings growth. The company is well-placed to continue with accretive M&A due to the robust balance sheet, while favourable structural trends support the core business. The valuation is moderate, with catalysts on the horizon that could drive a re-rating. We rate Sonic Healthcare a buy.[/subscribe_to_unlock_form]