US benchmarks led by tech rose on Wednesday after a benign CPI print and release of the Fed minutes cemented expectations for a rate cut next week. The reaction in the bond market was very different, however, with yields rising across the curve. Financial markets seem divided over the future direction of inflation. The US dollar rose while precious metals and commodities were higher. Bitcoin climbed back above $100k while Comex gold futures rose to $2755.

The Dow Jones dipped 0.22%, the S&P 500 gained 0.82% to 6084, while the Nasdaq Composite jumped 1.77%. The Russell 2000 added close to 0.5%. Mag 7 stocks led the rally with growing optimism on Wall Street the Fed will deliver another rate cut next week despite the consumer price index rising 0.3% in November for the fourth-straight month, while core CPI, which excludes volatile food and energy costs, rose by the same amount. The core gauge was up 3.3% from a year before, in line with estimates but well above the Fed’s target level. Investors shrugged this off, with the Xmas rally on track to deliver a strong December with the new year just over two weeks away.

The Bank of Canada lowered its rate by half a percentage Wednesday, its second straight outsized cut. Other central banks are also expected to lower rates, and in some cases cut faster and deeper than the Fed. The ECB and Swiss National Bank are likely to follow suit on Thursday. Meanwhile, China’s two-day Central Economic Work Conference is expected to map out policies for next year, following strong fiscal and monetary stimulus signals from top leaders this week.

The reaction in the US bond market was swift to the elevated inflation print, with the long end of the curve rising sharply. The 10yr and 30yr rose 5 bps to 4.27% and 4.48%. The bond market is still pricing in a rate cut next week, albeit at a much slower pace of easing next year. Inflation is proving sticky, and the jury is still out in terms of what impact the Trump administration will have next year after assuming office. Wall Street doesn’t appear too worried however with the volatility index or VIX dropping below 14.

The dollar rallied after a report that Chinese leaders are considering allowing their currency to weaken as they brace for higher tariffs under a second Donald Trump presidency. Competitive currency devaluation seems to be the way most countries will position against the tariffs. Commodities were higher with WTI and Brent crude jumping 2.7% to $70.48 and $73.68. The Biden administration is considering new sanctions on Russia’s oil trade, a move that could tighten the market. The White House also warned that Russia may fire another intermediate-range ballistic missile at Ukraine, after what Moscow said were strikes on its territory with US-supplied weapons. Comex gold added +1.3% to $2753 while silver futures lifted to $32.80.

Sometimes, good news is bad news in the stock market especially when it comes to indicators like investor sentiment. Contrarian investing is exactly what it sounds like — it’s an investing strategy that deliberately trades in opposition to the prevailing investor outlook. At Fat Prophets, we have, on many occasions over the decades, taken the opposite side to the prevailing view. Contrarian investors typically sell in a bull market and buy during a bear market when assets are very depressed. Warren Buffett aptly summarised the contrarian strategy with his famous quote “attempting to be fearful while others are greedy and to be greedy when others are fearful.

We did this several years ago in Japan when the Nikkei was only just exiting a multidecade bear market. Valuations were pulverised following thirty years of deflation and periodic recessions. For example, we were able to buy the Japanese banks at price-to-book ratios of below 0.4X. This year, we have been focused on China, where equities sell for valuations also at multidecade lows. Well-known economist Ed Yardeni also has a similar philosophy.

While the S&P 500 has continually hit new record highs, driven by expectations around the incoming Trump Administration – I have called out the nosebleed valuations where a lot of the good news on the economy next year has been priced into the market already and brought forward. At some point, there has to be a correction in US stocks. I continue to see relative safety in stock markets outside the US, given much lower valuations. [stu alias=”daily_121224″]While US stocks are likely to be vulnerable to a correction early next year, I don’t see the roaring 2020s bull market ending anytime soon, but the case for a pullback is now elevated in my view.

Ed Yardeni also thinks there’s reason for a pause in the US bull market (which I think will occur around the time of Trump assuming office in late January). As Ed Yardeni said in an update this week “There may be too many charged-up bulls. Contrarian indicators are turning bearish, suggesting the new year might start with a stock market pullback.”

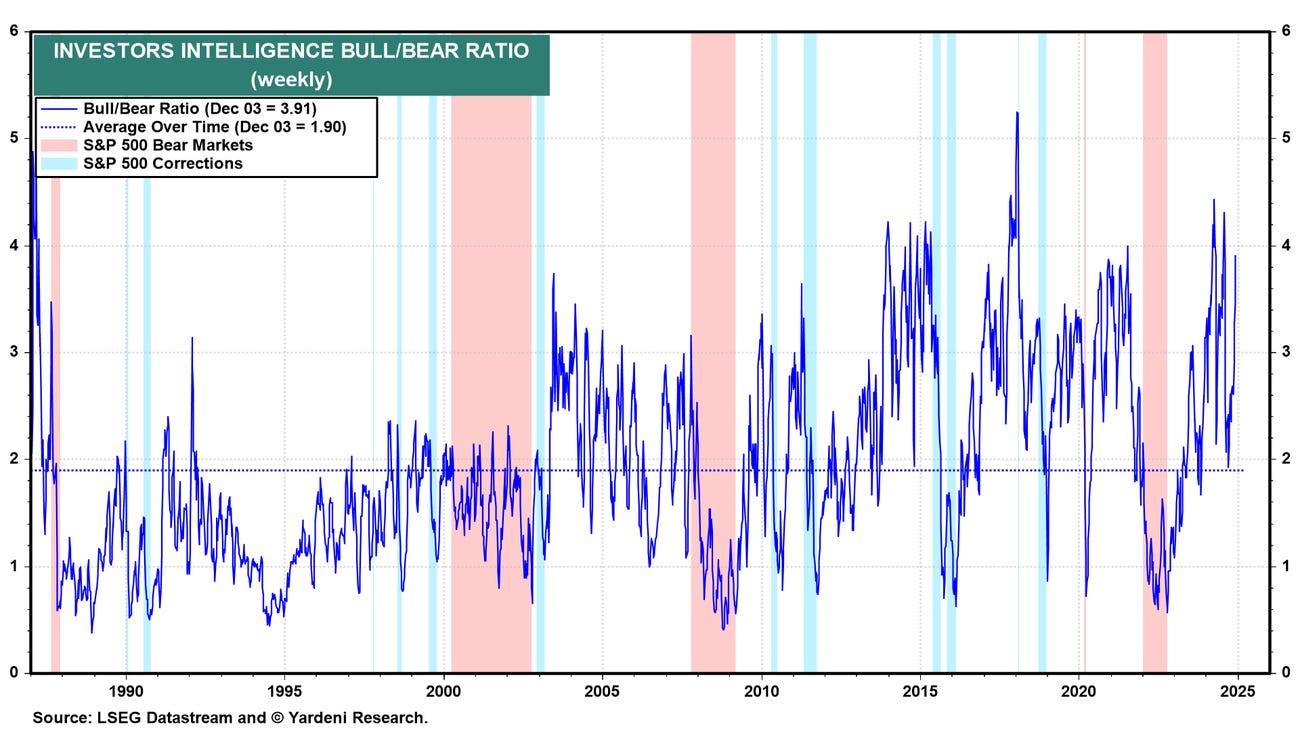

Ed Yardeni cited 4 bullish indicators signalling runaway optimism in the market has potentially gone too far. First, the Investors Intelligence Bull/Bear ratio, an economic indicator measuring the proportion of financial advisors taking a bull or bear stance, is currently standing at 3.9, with 62.9% of advisors in the bull camp. That’s up from 2.3 in mid-October. Elevated Bull/Bear Ratio levels are potentially bearish, indicating an excess of bullish sentiment – but also buyer exhaustion. We have sent a relentless wave of buying in the US post election, but there is a limit to how much longer this continues before counter-correction.

Source: Yardeni Research

Additionally, the S&P 500 is trading well above the 200-day moving average in terms of price action. As of early December, it was trading 11.2% above its average closing price in the last 200 days, which often precedes a corrective pullback. A stock or an index advancing well beyond a moving average can be a sign that a rally is approaching exhaustion. I see this as being the case with the US indexes.

The S&P500 is becoming increasingly vulnerable to a correction early in the new year. However, support is well defined at 5,700 and 5,400. Any selloff is likely to be well contained with investors buying the dip and deploying considerable liquidity amassed on the sidelines.

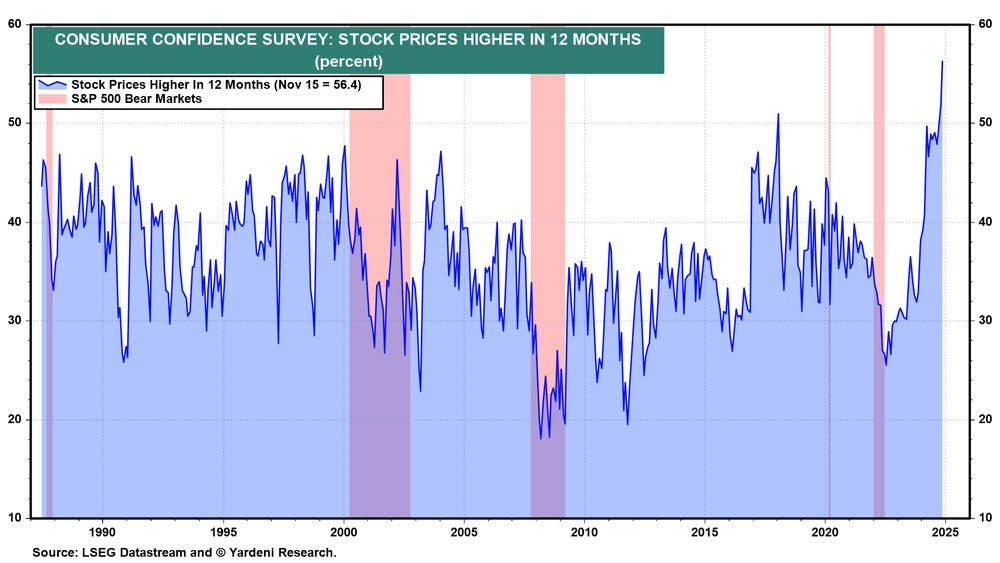

Another sign is consumer confidence. According to the Conference Board’s Consumer Confidence Index (CCI), a record-breaking 56.4% of consumers expect stock prices to increase in 2025. This is another clear sign that US stocks are now overbought. I prefer international equities on balance at this point given that valuations are not overextended as much. Ed Yardeni said that this week, the CCI reading “is even more bullish than ahead of the tech wreck in 2000.”

When measures of bullishness or complacency get too stretched, they can be precursors to market selloffs. I think one is coming soon for the US market, and likely to get underway in the new year. However, I don’t believe this will be the end of the bull market, but really a setback to correct what is now overexuberance.

While international stock markets have been left behind in the wake of the US rally this quarter, on the other hand, foreign buying of US stocks remains very elevated. International investors are turning their backs literally on their own backyard and buying America. In September, the 3-month moving average of foreign private purchases of US stocks hit a record high. As Mr Yardeni noted this week, “historically, foreigners have been poor timers of the US stock market, tending to chase rallies into blow-off tops.”

I am not concerned about a potential January pullback. US stocks are in one of the most richly priced markets of all time right now. A pullback would be a great opportunity to add stocks to portfolios at cheaper prices but also set market sentiment back to a more sustainable level.

With Donald Trump taking office next January, investors are expecting more favourable tax legislation, less regulation and a pro-business environment. The US economy is also fundamentally strong, but the market has got ahead of itself. I don’t expect a corrective selloff to last very long, but expectations will be healthily reset and allow the still significant liquidity in money markets accounts to be drawn in from the sidelines.

I don’t see the same probability of a drawdown being significant in other markets we favour including Australia (rate cuts are coming soon), Japan, the UK and notably China where the early-stage bull market is climbing a wall of worry. I also like commodities.

A contrarian’s dream?

China’s stock market offers bargain basement prices at current levels for patient contrarian investors. The Hang Seng index resumed upward momentum this week, which will likely gather impetus once investors become more confident about fiscal stimulus measures aimed at domestic consumers being confirmed. Both the CSI300 and Hang Seng Index are priced on historically depressed multiples below 10X. China/Hong Kong stocks are, therefore well insulated against any corrective selloff in the US market.

Citibank notably said this week that crude prices will gradually decline by up to 20% to $US60 a barrel by the middle of 2025 as the physical market tips into a surplus of 1.5m barrels a day by the second quarter. Supply from non-OPEC+ countries and notably the US, is expected to surge. OPEC is also expected to cut output. But it’s not all bad news for commodities. I see a continued surge next year in the soft ag complex including the grains but also in precious metals with China now re-entering the market on the buy side. Other central banks are likely to also follow.

Citibank expects gold’s stellar run this year to continue in ’25 with prices to hit $US3000 an ounce and for silver to surge by a similar amount to $36oz. The bank argues that the combination of a further deterioration in the US labour market, elevated interest rates weighing on growth and higher demand from exchange-traded funds is expected to lift gold to record levels. Citi also believes central banks and governments will keep buying gold even if tensions in the Middle East and Russia subside.

Silver has followed gold and resumed upward momentum this week. The twelve-year highs near $36 an ounce are within sight and likely to be retested next year.

I think this outlook will prove prescient but would also add that gold and silver miners are likely to accelerate in a bull market – particularly as corporate M&A activity picks up in the sector. Valuations are still very cheap and it’s outright easier for many of the miners to buy one another, rather than develop new greenfield operations from scratch. I am expecting a wave of takeover activity in the sector to drive prices up to historical norms. Gold and silver producers (along with many other miners) have been left behind this year despite surging spot prices, but this arbitrage could be corrected next year.

Silver is particularly notable given the large global supply deficit versus rising demand. On this front, Citibank sees silver performing in line with gold, noting that prices around $US29 are a good opportunity to build positions in the metal. The silver market is expected to be in a deficit at around 190/210 million ounces as global supply lags robust industrial demand and a pick-up in silver ETF purchases.

Gold and silver miners are cheap relative to historic valuations with M&A likely to pick up sharply within the sector next year. UK-listed silver producer Fresnillo is one stock with significant recovery potential next year. After exiting a multi-year bear market this year, Fresnillo has resumed upward momentum with the September highs near 800p likely to be retested in the coming months.

The ASX 200 slipped -0.47% to 8353 on Wednesday following broad-based, but not deep declines in most cases, with real estate and gold miners offering some respite. This followed a soft lead from Wall Street and a cautious mood ahead of that US consumer inflation data. There were no major local economic releases, although the unemployment print is on today’s agenda. SPI futures are pointing to a 0.3% gain on the open. A$ spot gold prices are within a whisker of new record highs at A$4262 which should underpin domestic gold miners today. As outlined above, I am expecting M&A activity within the sector to accelerate over the coming year and restore valuations closer to historical norms.

A$ spot gold has resumed upward momentum in recent weeks, marching to new record highs.

The Australian dollar remained subdued, holding below US64¢ after sliding almost -1% on Tuesday. The decline followed heightened expectations of a potential rate cut from the Reserve Bank, driven by its dovish tilt on Tuesday. A shift lower for local yields supported the real estate sector, which was the only broad ASX sector to post a solid gain on Wednesday, up +0.81%, although this was largely driven by narrow advances, including Stockland +2.2% and Goodman Group +1.7% with the latter benefitting from positive Citi coverage, upgrading the REIT to buy.

Consumer discretionary inched +0.09% higher despite weak breadth, where decliners outnumbered advancers. Wesfarmers +1% was the only top 10 stock in the sector to post an advance. Further down the market cap table, Eagers Automotive jumped +5.3% after Barrenjoey upgraded the stock to overweight.

The other nine broad ASX sectors declined, led lower by tech -1.35%, which extended losses after its -4% slide on Tuesday. Industrials -1.01% and energy -1% were the next-worst performers on Wednesday.

Energy’s day in the sun (with solid gains on Tuesday) this week was short-lived, and the sector was back in the red on Wednesday. Stocks were broadly weaker, with Santos falling -1.4% and Woodside down -0.8%. Coal miners were mixed, as Whitehaven Coal rose +0.5%, but New Hope Corporation dropped -1%. Uranium stocks were also soft, with Deep Yellow up +0.8%, but Paladin Energy and Boss Energy fell -1.05% and -1.2%, respectively.

The heavyweight financial sector declined -0.61% as the big four banks experienced modest losses ranging from -1.1% for CBA and NAB to -1.3% for ANZ. Insurers saw more aggressive selling as yields came down, hurting QBE -2.7%, Suncorp -2.9% and IAG -1.7%.

The materials sector slipped -0.41% as base metal commodity prices gave back some of Tuesday’s advances. A +0.4% advance from BHP was offset by Rio Tinto falling -1.2% and Fortescue dropping -1.7%. South32 was a notable drag, tumbling -4.4% after warning that civil unrest in Mozambique had disrupted transport operations, threatening its production guidance. Copper exposures tilted lower, with Sandfire Resources down -1.2%, the Global X Copper Miners ETF declining -0.4%, while 29Metals was unchanged.

The gold sub-index +0.2% rose modestly, reflecting strength in the gold price. Northern Star gained +0.2%, while Evolution Mining slipped -1.5%, and Newmont edged down -0.3%. St Barbara +1.5%, Genesis Minerals +1.1% and Ramelius Resources +1.3% advanced. The Global X Physical Gold ETF advanced +0.6% and has a steady track record of tracking its benchmark closely, with solid gains YTD.

[/stu]Carpe Diem!

Angus

Disclosure: Fat Prophets and its affiliates, officers, directors, and employees may hold an interest in the securities or other financial products relating to any company or issuer discussed in this report. Fat Prophet’s disclosure of interest related to Investment Recommendations can be provided upon request to members@fatprophets.com.au.

Chart Source: Thomson Reuters