KEY CONTENT

- Markets got ahead of themselves: Equities rallied in anticipation of a ceasefire, but Trump’s Wednesday night address – neither “mission accomplished” nor full escalation – reset the timeline. Oil rose, futures slipped, ASX tech and resources sold off.

- The structural bull case remains intact, just delayed. BofA fund flows ($29B equity outflows, record $10.5B from materials), Goldman’s CTA data (net short $50B globally, buyers in most scenarios over the next month), a less-hawkish Fed, China PMI back in expansion, and resilient US retail/ISM data all point in the same direction.

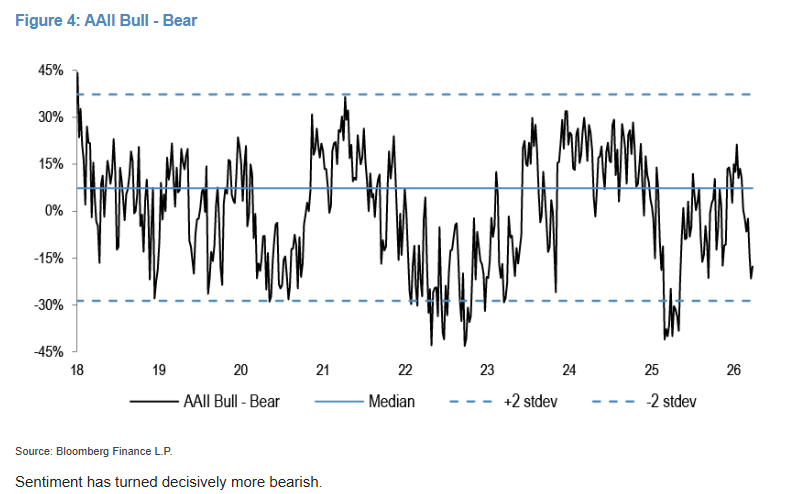

- Sentiment is deeply bearish, which is historically bullish. Hedge fund short exposure at 11% (10-year high), six straight weeks of net selling, and Hartnett’s Bull/Bear Ratio at 1.12. Goldman sees capitulation signals emerging.

- Historical parallel: 1942. Markets bottomed well before WWII ended – Midway and Stalingrad were the turning points. The argument here is that markets are already pricing an offramp from the ME conflict, with the oil futures curve already in backwardation.

- Valuations have re-rated sharply. Nasdaq 100 at ~21x forward earnings, S&P forward P/E compressed ~17% — Morgan Stanley’s Mike Wilson sees risk/reward improving materially on a 6–12 month view.

- Gold conviction unchanged. Yardeni targets $5,000/oz by December; JPMorgan’s commodities desk holds $6,000/oz. A weaker USD post-war is the macro catalyst.

REPORT SPOTLIGHT

- Rio Tinto (ASX: RIO) – BUY

Full reports across Australasia, Global Equities and Global Mining are available to members, along with our complete model portfolio positioning. If you’re not yet a member, you can join today.

ON THE HORIZON

- Middle East Escalation & Energy: Trump’s speech on Thursday afternoon prolongs the uncertainty

- Nonfarm Payrolls (Friday, April 3): This is the marquee economic event of the week. A weak report will amplify recessionary and stagflation fears, while a strong report could alleviate growth concerns but keep the Federal Reserve’s rate path tighter for longer.

- Holiday liquidity: Expect thinned volumes around Easter

- Australia: Household spending data

Good afternoon,

Wayne Gretzky’s rule was simple: skate to where the puck will be, not where it is. Last week, markets did that – pricing the ceasefire, the rate pivot, and the short-covering unwind before any of them fully arrived. The only problem is that the puck took a different trajectory. Trump’s prime-time address on Wednesday night complicated the timing.

Trump addressed the nation at 9pm Eastern on Wednesday, his first prime-time speech since launching Operation Epic Fury more than a month ago. The message was neither the mission accomplished markets had been pricing nor an open-ended commitment to escalation – it sat between the two. Objectives were “nearing completion,” he said, but the US would hit Iran “extremely hard” for another two to three weeks, with the electricity grid and oil infrastructure explicitly on the table if Tehran failed to engage. The Strait would reopen “naturally” once those objectives were met. Trump claimed Iran had requested a ceasefire; Iran’s foreign ministry called the claim “baseless.” Just another typical messaging session from the White House, in other words. Trump’s speech ran just nineteen minutes. Traders responded quickly – oil prices headed higher again, and equity futures slipped into the red. On the Australian boards during the afternoon session, trading turned on a dime. Tech and resources were dumped.

Perhaps the market had skated to the right spot, but it just arrived a fortnight early. That caveat noted, many of the structural elements that drove this week’s recovery before Trump’s speech suggest our thesis remains intact, though it may be delayed. The BofA fund flow data – $29 billion in equity outflows, a record $10.5 billion from materials, $6.3 billion from gold – captured a market that had already gone maximum defensive. Goldman’s prime desk confirmed the mechanical reality: CTAs had sold approximately $190 billion across the prior month, were net short $50 billion globally, and would be buyers in most scenarios for the coming month. A Fed that was less hawkish than it could have been. China PMI back in expansion, and US retail sales and ISM data dismantling the recession narrative all point in the same direction.

The Q1 earnings season beginning in two weeks remains an upcoming catalyst, and the structural case for gold, uranium, and ASX rate-sensitives is intact. But Thursday’s US open will be messy, and at the time of writing, it seems likely that the market has much more volatility to absorb before the resolution it began to price in this week actually arrives.

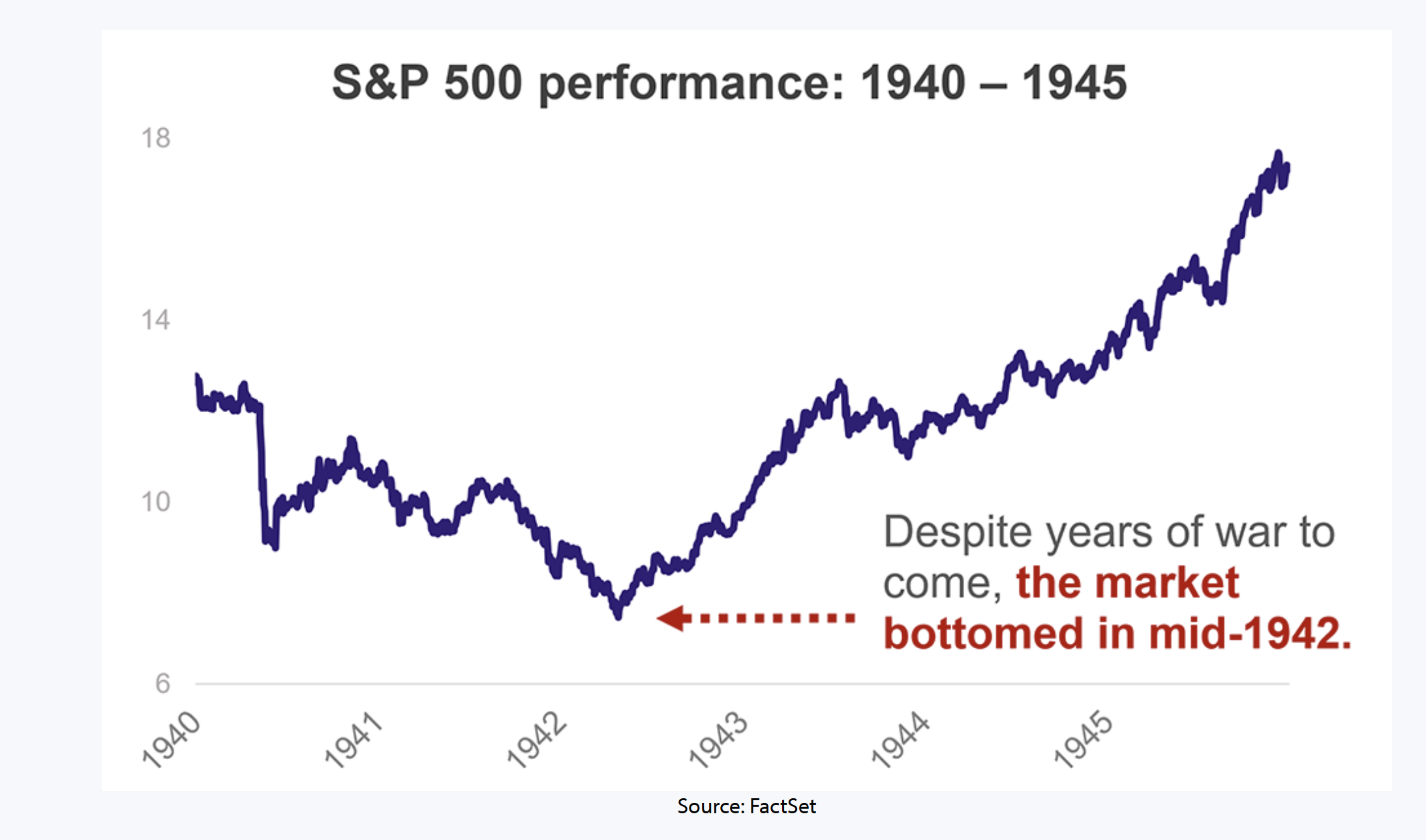

Wars and their overall impact on financial markets tend to pass quickly. In 1941–42, the S&P 500 initially declined as the Germans were winning at the beginning. But a turning point arrived much sooner than one would expect for the stock market, and years before World War 2 concluded. The Battle of Midway happened in June of 1942 and represented a key turning point for the war in the Pacific. Later in the year, another key turning point arrived during the Battle of Stalingrad, with the Soviet counteroffensive which began on November 19–23, 1942. This massive operation encircled the German 6th Army, shifting the initiative on the Eastern Front to the Red Army. Interestingly, the S&P 500 never looked back following those two key turning points in 1942, even though the war would run for another two years. The key point here is that financial markets are already looking ahead through the ME war, despite all the dire headlines, and seeing a resolution to the conflict.

Wars and their overall impact on financial markets tend to pass quickly. In 1941–42, the S&P 500 initially declined as the Germans were winning at the beginning. But a turning point arrived much sooner than one would expect for the stock market, and years before World War 2 concluded. The Battle of Midway happened in June of 1942 and represented a key turning point for the war in the Pacific. Later in the year, another key turning point arrived during the Battle of Stalingrad, with the Soviet counteroffensive which began on November 19–23, 1942. This massive operation encircled the German 6th Army, shifting the initiative on the Eastern Front to the Red Army. Interestingly, the S&P 500 never looked back following those two key turning points in 1942, even though the war would run for another two years. The key point here is that financial markets are already looking ahead through the ME war, despite all the dire headlines, and seeing a resolution to the conflict.

Visibility in the current ME conflict remains low, similar to 1942. But markets are already pricing in an off-ramp and a turning point – and importantly, coming alleviation in terms of the oil supply shock. The oil futures curve is in backwardation, with prices much lower in further out months.

Unlike the onset of war between Russia and Ukraine, the setup for the US and global economy is more constructive. Earnings have been revised up since January, which contrasts sharply with 2022, while interest rate settings are much higher. Four years ago, interest rates were still very low, with most central banks adopting the view that inflation was transitory. There is significantly more buffer today – the starting point for the US 10-year yield is about 350 basis points higher than four years ago. What is different to 2022 is that a lot of the supply chain constraints from Covid and rising wages are not present in the system. The sole pressure point at this stage is fuel costs, and the narrative around this could change quickly.

Fund flow data has shown investors turning much more defensive. Bank of America reported that bond funds were the only major asset class to see inflows, taking in $2.7 billion, while equities recorded $29 billion in outflows. US equities led the declines with $23.6 billion in outflows, the largest in 13 weeks. Materials funds posted a record $10.5 billion in redemptions, while gold funds lost $6.3 billion, the largest outflow since October. These withdrawals are often a precursor to an upside reversal as market positioning is reduced.

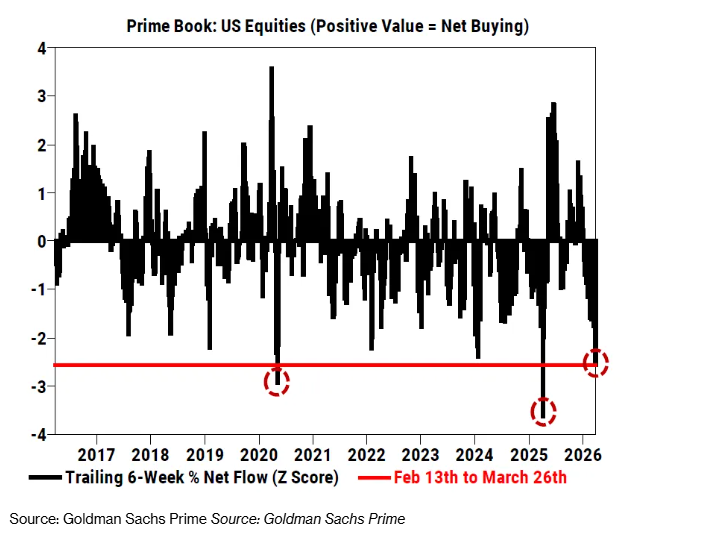

Signs of capitulation are starting to emerge among hedge funds, and the systematic community is running out of steam. The trading desk at Goldman Sachs noted that signs of capitulation are starting to emerge among hedge funds, and the systematic community is running out of steam. Goldman anticipates that the influential Commodity Traders Advisers or CTA’s “will be buyers in every scenario over the next month.”

CTAs are typically momentum traders and trend followers. Goldman noted that “the group of trend-following investors [CTAs] has sold about $190 billion over the past month and is now short by about $50 billion across global equities. The systematic community is running out of steam. Asymmetry lives to the upside — over the next month, we estimate CTAs are buyers in every scenario.”

Meanwhile, Goldman noted that “hedge funds have cut global equity holdings for a sixth straight week, driven by short sales. The latest selling was widespread, with net disposals across all major regions, including Europe and Japan. I expect big rebounds coming for those markets given that short exposure has reached 11%, a 10-year high, according to Goldman. The Goldman team noted that “some signs of capitulation are starting to emerge, with many funds being close to their maximum levels of pessimism about the market. On a trailing six-week basis, US net selling was the third-largest over the past decade. The selling approached levels seen during the Covid selloff, while still short of the April 2025 “Liberation Day” episode. This is all very constructive in trying to determine inflection points in market corrections.

Morgan Stanley’s CIO Mike Wilson has a constructive view, and noted this week that “we think the equity market is less complacent on growth risks than consensus believes—over 50% of the Russell 3000 is down more than 20%, and the S&P multiple is now down over 15%. We also see differences vs prior periods where an oil spike ended the business cycle. Rate move is a potential risk.” Mr Wilson believes there is growing evidence that the S&P 500 correction is getting closer to its ending stages, with the S&P forward P/E ratio now compressed by 17%, which is in the range of prior growth scare outcomes in the absence of a recession or the Fed hiking. He is correct in my view, given that a solid earnings season is likely to underscore what is now a much cheaper US market. The case for international equities is more compelling.

While the MS strategist conceded that a “recession is not priced obviously, but that makes sense given the key differences versus prior periods where an oil shock ended the business cycle.” He highlighted that earnings growth is accelerating and positive (whereas it was decelerating and negative in previous periods and the oil move today in year-over-year terms is about half of what it was in those historical periods.” The fact that the US economy is still very resilient and companies are likely to report better than expected earnings seems to be a big factor presently being ignored by investors. Wilson concluded that “on a 6-12 month basis, the risk-reward now looks more attractive than at the beginning of the year…this helps to reinforce our point that we’re likely toward the ending stages of this correction.”

Another good Chief strategist “worth his salt” is Michael Hartnett, of Bank of America. He outlined in a note over the weekend that “a dip in the S&P500 below 6,600 is kickstarting policy panic, though current signals still show no evidence of bull capitulation or broader macro panic”. I think we are seeing this now, as evidenced by significant bearish positioning by hedge funds and financial institutions. The recent leg down in technology stocks to PE valuations that have hit multi-year lows is another sign of the capitulation that is creeping into the market.

Mr Hartnett expects the policy backdrop to evolve into broader support for markets. “We assume policy panic to avoid recession.” I have maintained a similar line, and the WH needs to get back to focusing on the domestic economy ahead of the mid-term elections in November. Oil prices at current levels could spell the end to Republican control of both the upper & lower houses in Congress. Hartnett believes that consumer discretionary stocks are a key opportunity, noting the sector is trading “at relative lows similar to past crisis periods such as 2008 and 2020”, describing the trade as a “favourite contrarian long’ given a ‘post-war policy pivot is coming and will be aimed at addressing affordability pressures and a slump in approval ratings’.

Ed Yardeni wrote this week: “If Trump is declaring mission accomplished, then so are we regarding our stock market correction call. We will probably lower our recession odds from 35% back to 20% once we have a better handle on whether the conflict in the Persian Gulf is actually over. We reserve the right to change our minds as often as the President does. Nevertheless, we have maintained our 7,700 S&P 500 year-end target and our commitment to our Roaring 2020s base case.” He also sees gold at $5,000/oz by December, and the JPMorgan commodity strategist is at $6,000. The Bull/Bear ratio dropped to 1.12 this week from 1.57 the prior week: “Such bearish sentiment readings are bullish from a contrarian perspective. So much pessimism usually instigates a surprisingly bullish government policy response.”

We remain similarly bullish on gold to Yardeni and JPMorgan. Recently, we upgraded a major Australian gold miner to BUY, taking advantage of the sell-off in March, which sees one of the best operational executors in the industry undervalued.

March is now behind the market. I am optimistic that what was an acute and severe correction is now over, and the bull market in US and global equities will soon resume. As discussed above, and similar to last year, it might take several months, but I fully expect risk assets and global benchmarks to be retesting their record highs later this year. March wasn’t an easy month, especially with numerous news headlines and the business press calling up the risks of a global recession and a coming bear market in stocks and risk assets.

One learns that market panics and human behaviour when it comes to fear are predictable and repeat time and time again. This manifests in asset and stock prices and leads to extremes in the market. However, each event has, in itself, its own unique characteristics which can be unnerving. Not many had ever been through a pandemic before, people dying from an unknown virus, and a world going into collective lockdown. No one had really seen a synchronised global banking system teetering on the edge of oblivion before, and major companies such as General Motors entered Chapter 11. It might look easy dealing with extreme volatility, but in reality, it isn’t, and on every occasion, one has to dig deep and fight the emotion that comes from the crowd.

Morgan Stanley’s CIO Mike Wilson is one strategist who held the line during some of those March pressure cooker days. And it is ‘pressure’ to hold the line when the markets are tanking and everything coming from the press, brokers & strategists is dire and bleak. It’s hard to maintain a sense of sensibility and objectivity. Mike did well in March, and it’s no surprise that he is the top-rated strategist in the US.

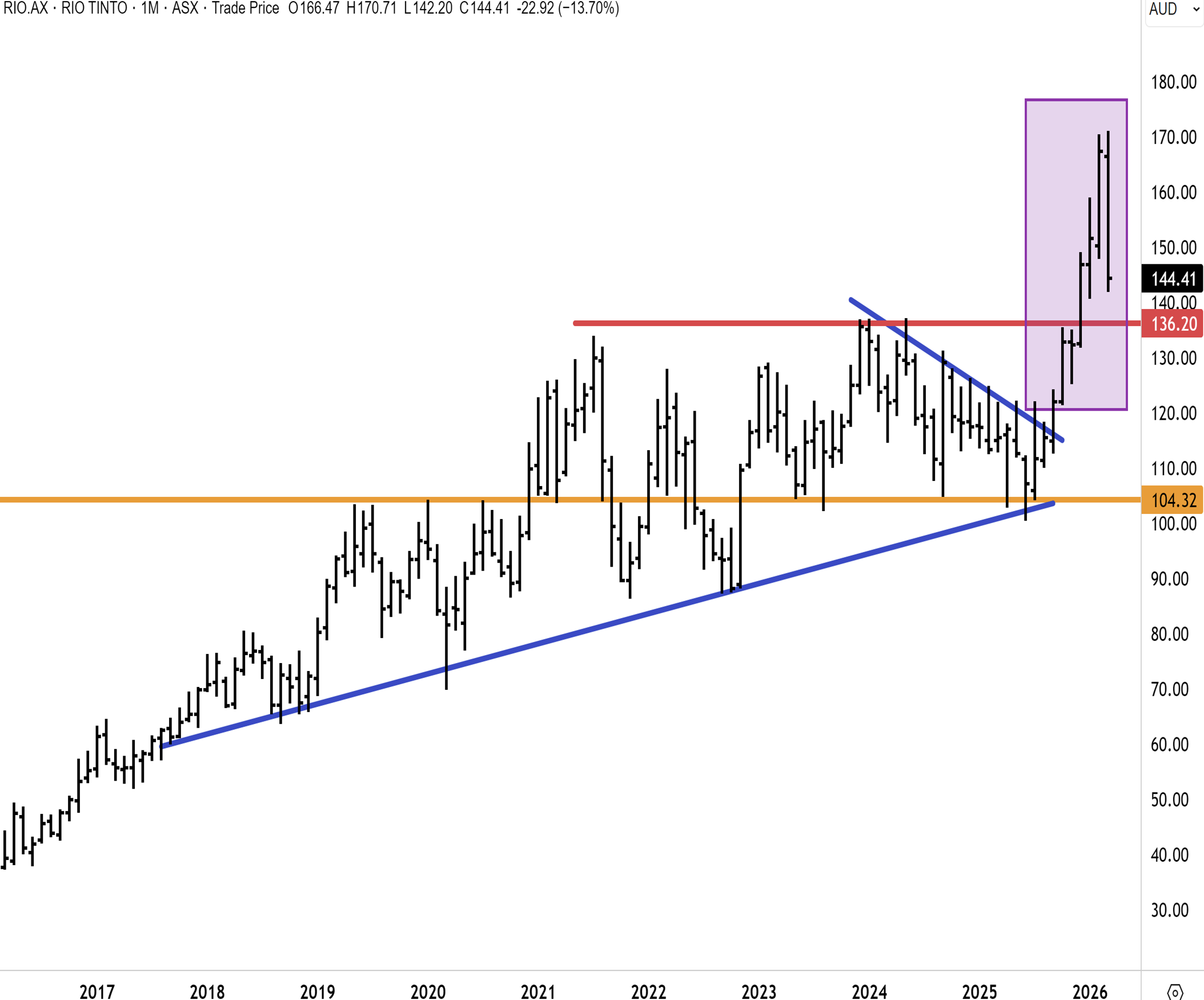

Rio Tinto (ASX: RIO)

The bull case on Rio Tinto has three engines running simultaneously. First, the damage to smelting capacity at EGA and Alba in late March in the Middle East will likely quickly shift the market into deficit, and Rio’s geopolitically secure Canadian and Australian smelters can now command strategic premiums. Second, Oyu Tolgoi’s underground ramp-up is delivering on schedule and helps underpin a credible 3% CAGR in copper-equivalent production through 2030. Third, the Pilbara iron ore remains the cash engine, and Simandou is ramping up. We believe a commodity upcycle has much further to go. RIO is well-positioned.

Rio Tinto surged to a new record high near $170. The stock has since corrected sharply, but encouragingly, is approaching a major support level near $137, which we believe will hold. This key support represents the breakout level from a multi-year trading range, which effectively capped Rio for close to five years. We expect this support level near $137 to hold.

Our base case for Rio is that once the incumbent consolidation phase completes, and the acute risk-off environment abates, upward momentum will resume with the record highs near $170 likely to be retested in the coming year. We continue to have conviction that Rio will extend higher, which is consistent with our bullish outlook for commodities, copper, and iron ore prices to hold above $100/ton.

Want the Full Picture?

This edition of The Narrow Path is a condensed version of our full weekly Wrap, which includes deeper positioning analysis and more targeted investment opportunities. A subscription also includes 4 daily market commentaries during the week and reports on stocks, ETFs and special reports spanning Australasia, Mining and Global Equities.

Have a great Easter weekend.

Carpe Diem

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.