- Global markets moved from early-week anxiety regarding tariffs and AI to a moderate “risk-on” revival as initial blanket US tariff threats were scaled back from 15% to 10%.

- Major indices in Australia, Japan, and the UK hit fresh record highs during the week.

- The Nasdaq is underwater in February, on track for its worst monthly performance since last March. Even a “blockbuster” earnings report from Nvidia resulted in a “sell the news” reaction, with shares falling more than 5% on Thursday.

- With tariff threats moderating and a softer dollar easing global liquidity, the fundamental backdrop favours a sustained allocation to broadening equity themes and structurally tight commodities.

- Hedge fund manager Stanley Druckenmiller warns that the US is nearing a “liquidity trap” for 2026, where fiscal dominance prevents the Fed from tightening enough to contain inflation without a serious recession.

- Current inflation patterns are “uncomfortably similar” to the 1970s.

- There is a good case for a structural shift toward physical assets, specifically being bullish on gold, copper, and energy.

- The Australian dollar reached $715 against the USD, the highest level since June 2022, driven by widening yield differentials

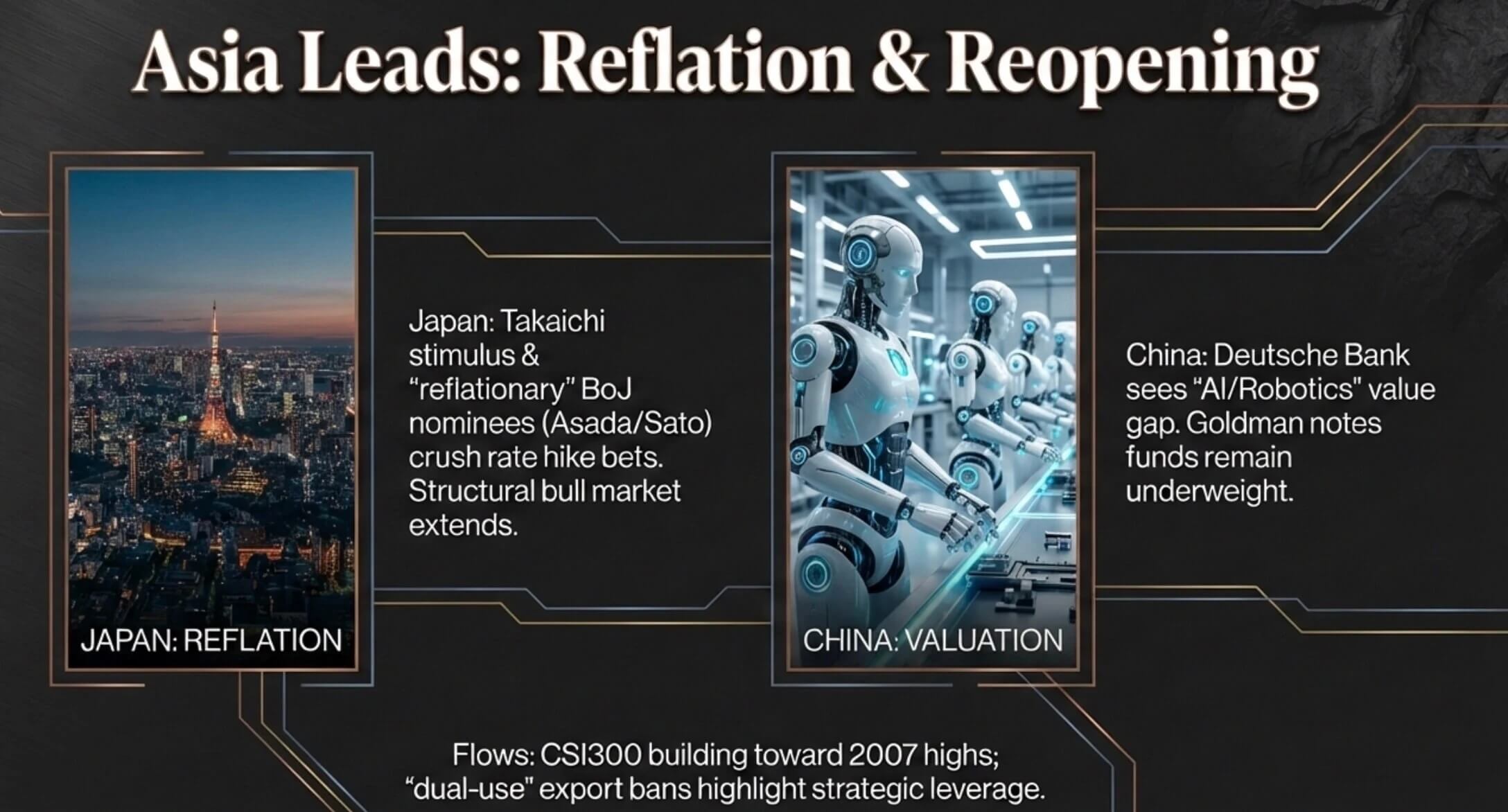

- Japanese equities continue a strong run following the removal of political uncertainty with the Takaichi government’s win.

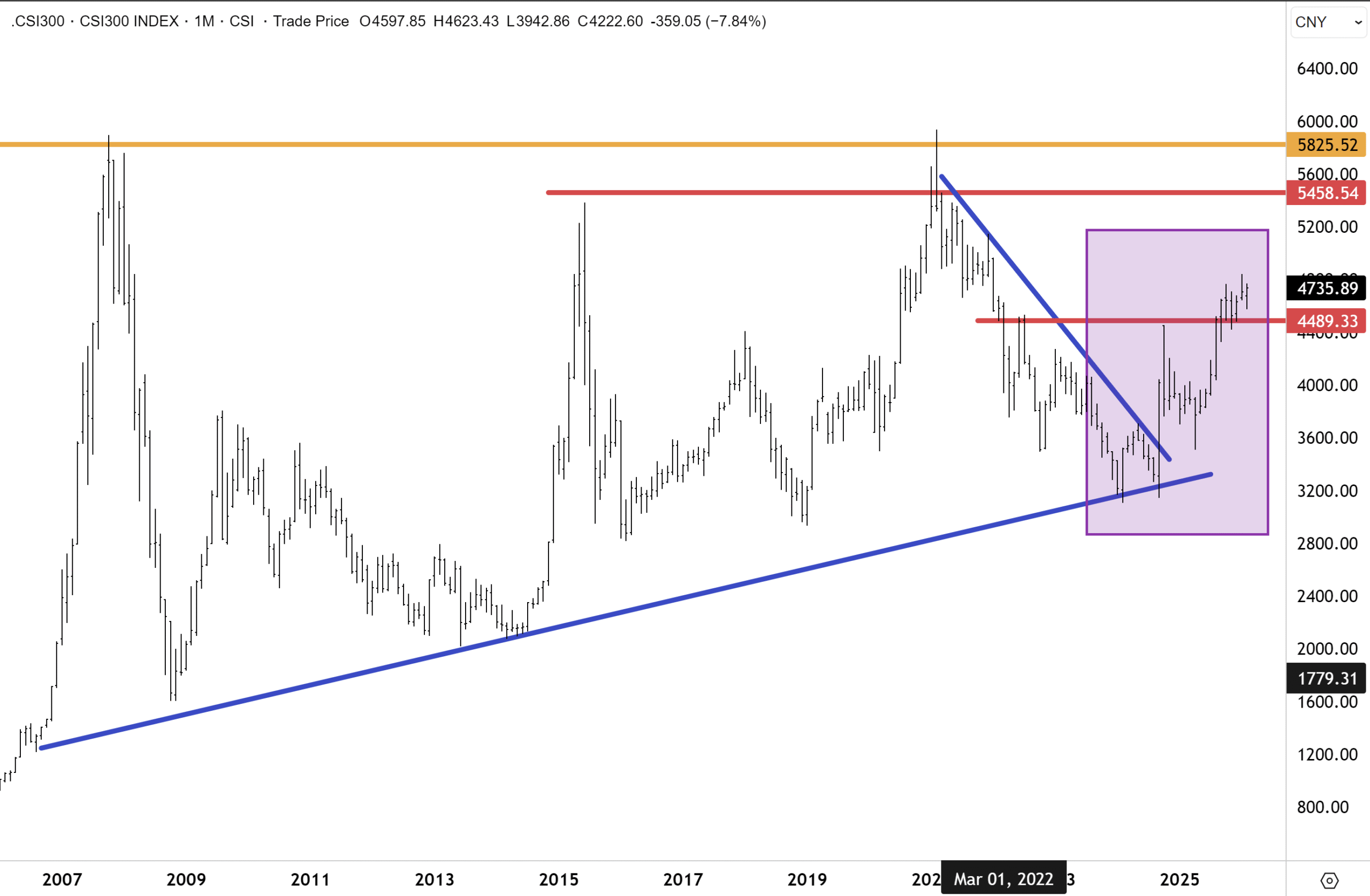

- China is increasingly attractive due to its “tech prowess” in AI and robotics, with the CSI300 making a potential run at its 2007 highs.

Report Spotlight

- Woodside Energy (WDS) – BUY: Despite profit softness, operating cash flow surged 23%, and the stock is nearing a confirmed technical inflection.

What to Watch

- Wholesale Inflation: Data is set to drop on Friday morning, New York time.

- Australian GDP: Figures are expected to be released on March 4th.

- National People’s Congress (China): Opening on March 5th, investors will be looking for clear fiscal stimulus signals from Beijing.

- Non-Farm Jobs Report (US): This closely-watched employment data is due on March 6th.

- UK Fiscal Statement: Chancellor Rachel Reeves will deliver this next Tuesday against a backdrop of softening domestic retail conditions.

Global markets navigated a volatile transition from early-week tariff and AI-related anxiety to a cautious risk-on revival. The dominant narrative shifted as a 15% threatened blanket US tariff threat was ultimately scaled back to 10%. A landmark data centre partnership between Meta and AMD and an update from Anthropic eased some AI fears, as did a few updates from software companies, though even a blowout report from Nvidia on Thursday wasn’t enough to keep those shares from falling more than -5% and sinking other semiconductor stocks. This was a classic “sell the news” reaction despite blockbuster results.

As of Friday morning, Sydney time, the major US indices had posted small advances of between +0.5% (Dow Jones) and +1.2% (Nasdaq), with a similar advance in Australia, while Japanese equities continued a strong run, up more than +3% and having posted new record highs mid-week. We make the case for why we remain bullish on Australia and Japan, among others, below. Risk appetite mostly improved as the week progressed. The VIX, which initially surged 10% to 21 on tariff fears, stood at 18.6% at the close of US trading on Thursday.

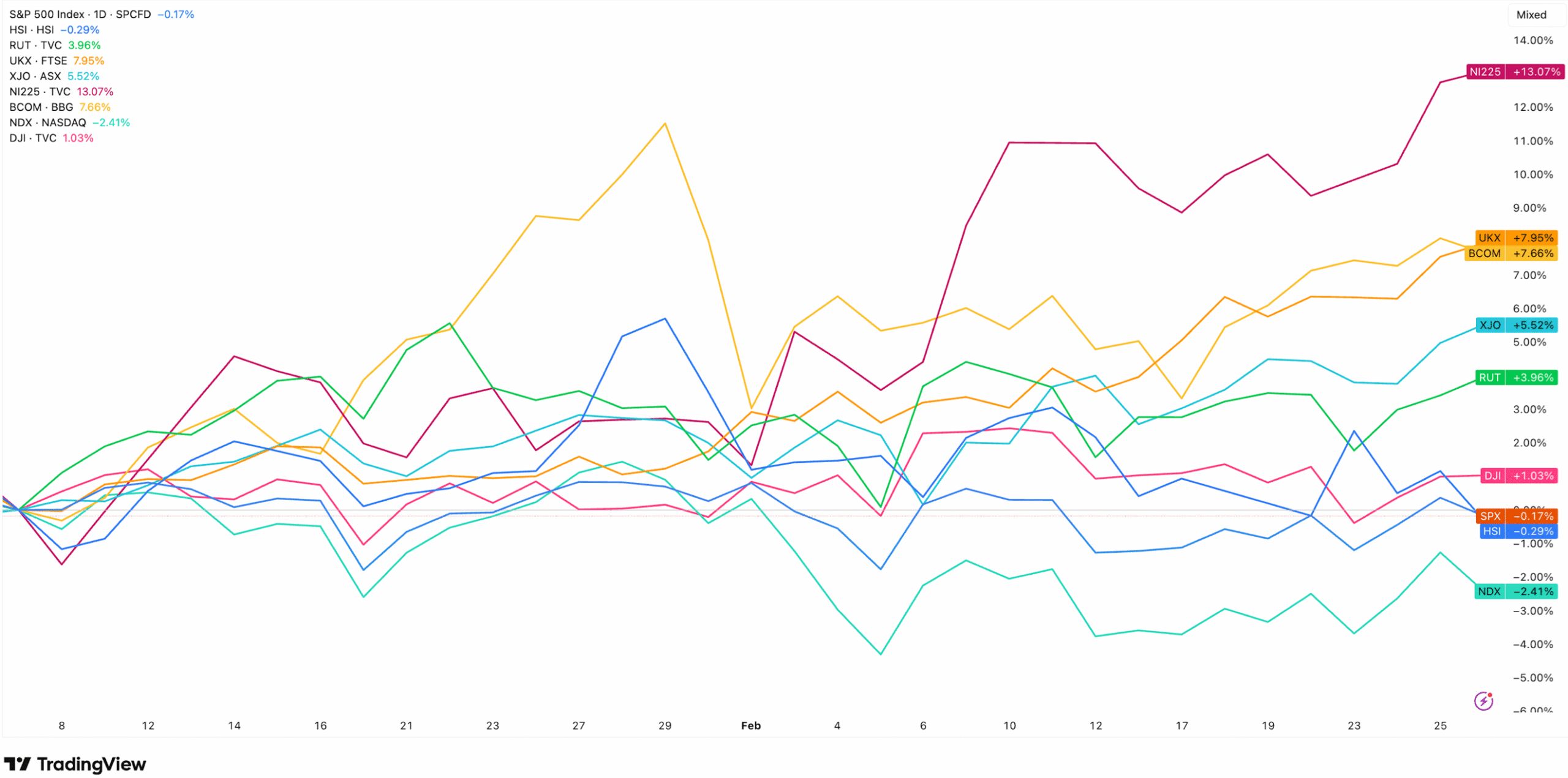

Many global market indices hit fresh record highs during the week, including the ASX200, Nikkei, FTSE100 and European indices. The following chart highlights the YTD performance of several key indices under our coverage.

YTD, the standout story of 2025 so far is Japan’s Nikkei, surging +13% to lead all major indices by a wide margin. The blue-chip FTSE 100 (UKX in the chart) has also impressed, up around +8%, while the ASX has delivered a solid +5.5%. The real laggards? US tech. The Nasdaq is down -2.4% YTD, dragging the S&P 500 into negative territory at -0.17%. The Hang Seng is flat, while the Russell 2000’s +4% gain suggests small-caps are holding up better than mega-cap growth. The rotation away from US tech dominance is the defining theme, even as Mag 7 names made a bit of a comeback over the past week. Stock futures show that the Nasdaq Composite is on pace for a -2.5% slide in February, marking its worst monthly performance since last March, while the S&P 500 is on track for a 0.4% loss.

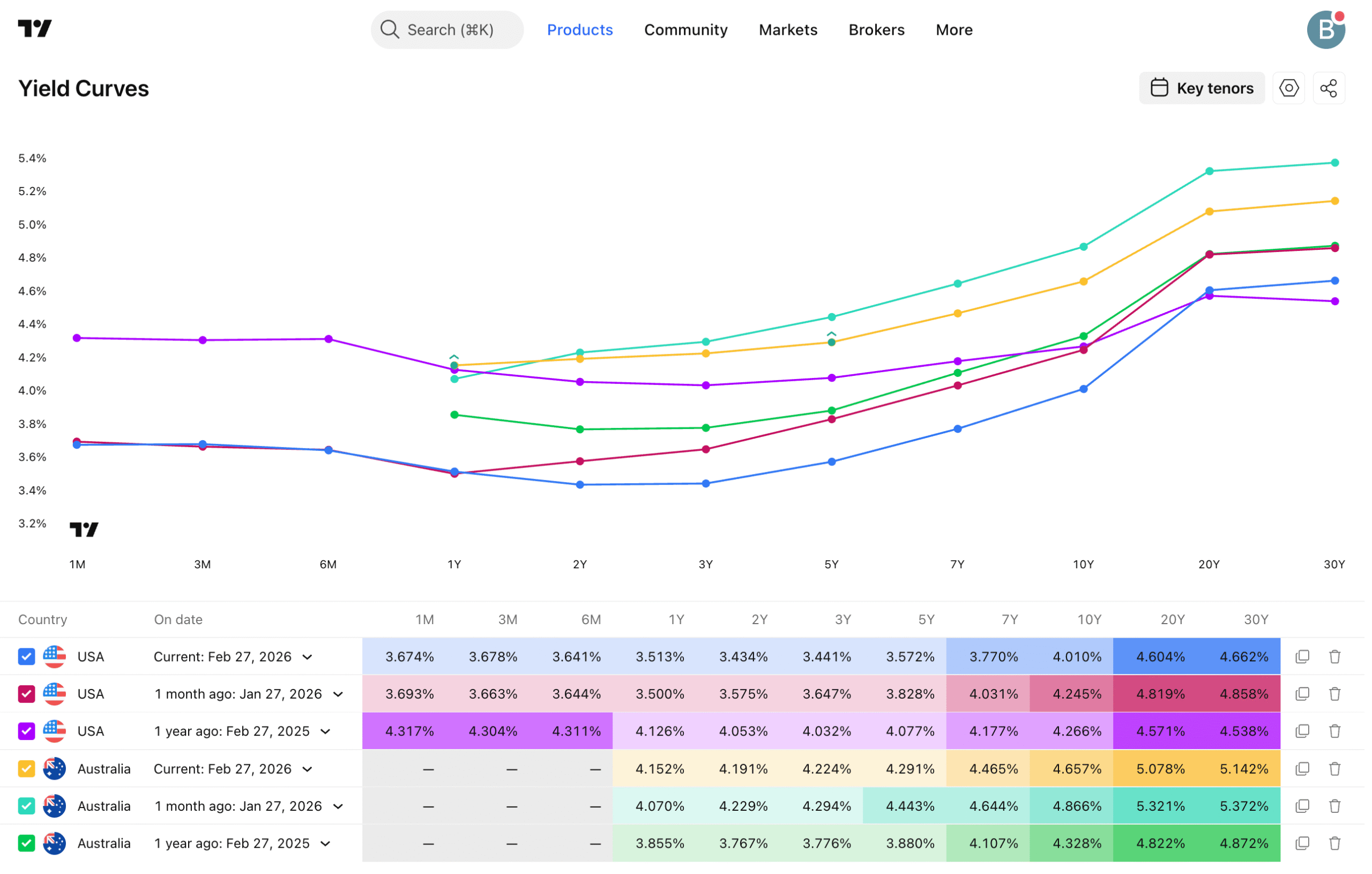

US Treasury yields edged marginally lower over the week, with the 10-year sitting around 4.002% at the close on Thursday. It was a different story in Australia, as we dive into later, which supported the Australian dollar.

The US dollar index (DXY) softened, dipping to 97.7. This weaker greenback is feeding directly into commodity strength and explicitly improving the liquidity backdrop for emerging markets and China.

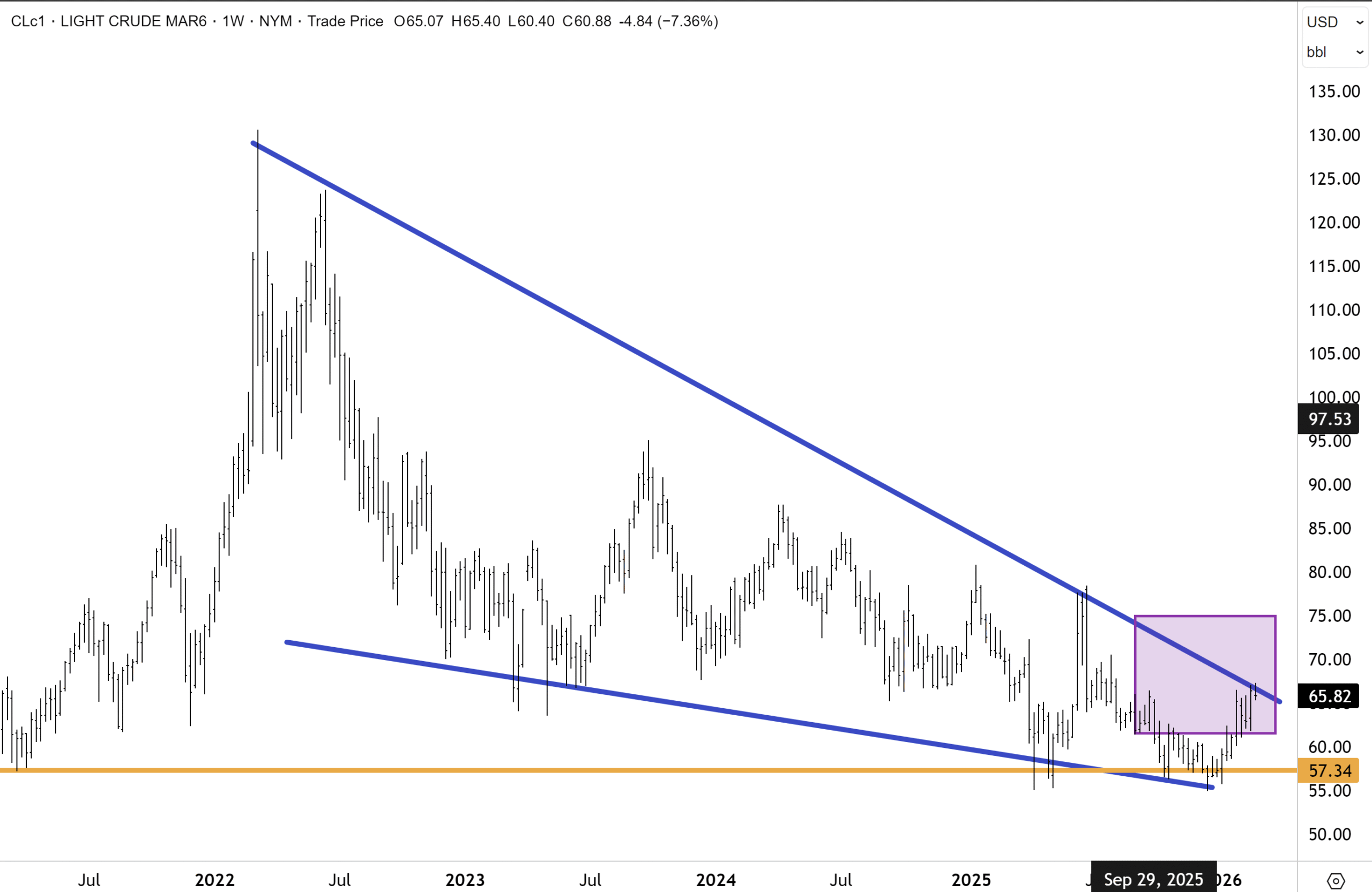

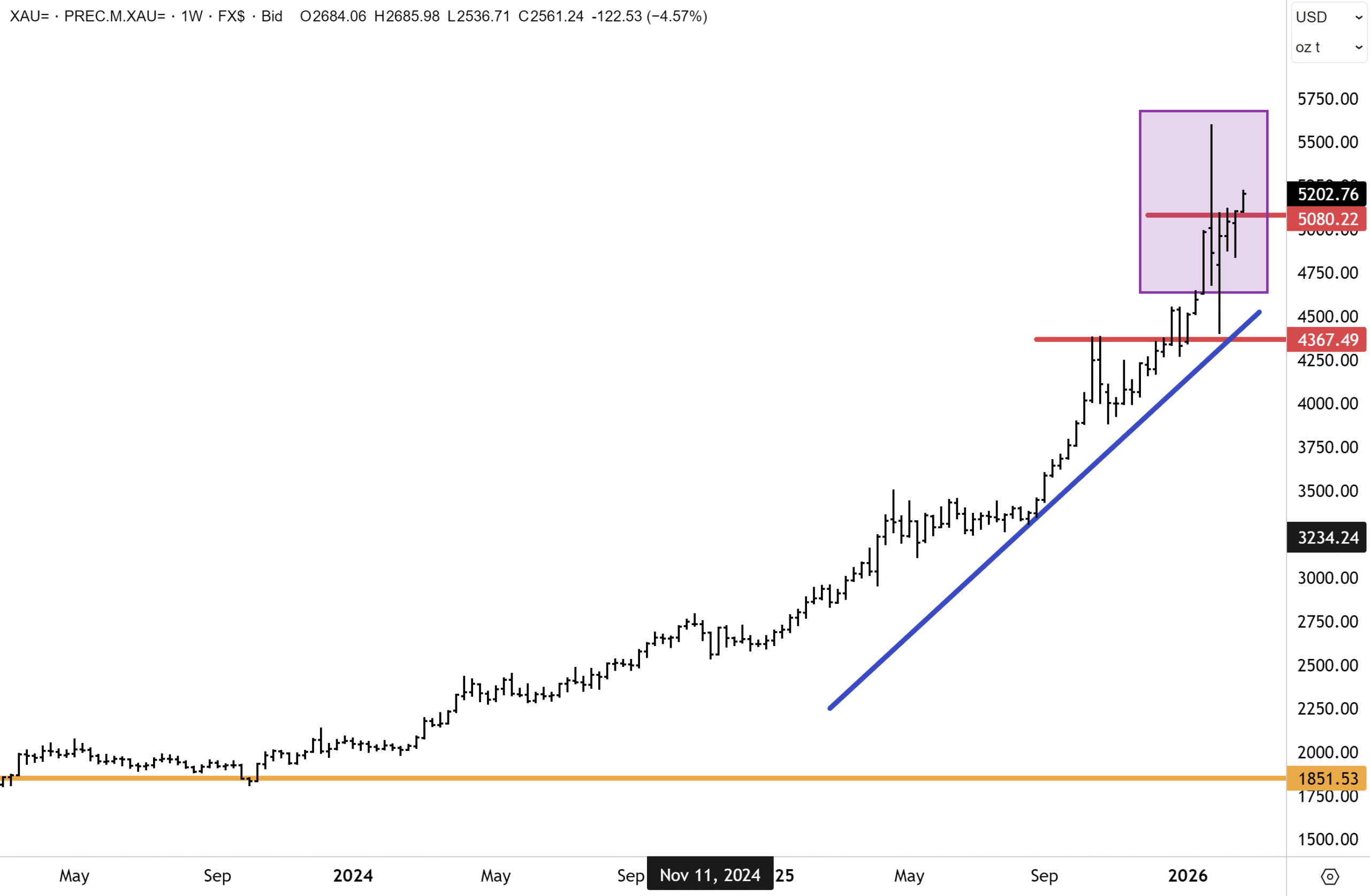

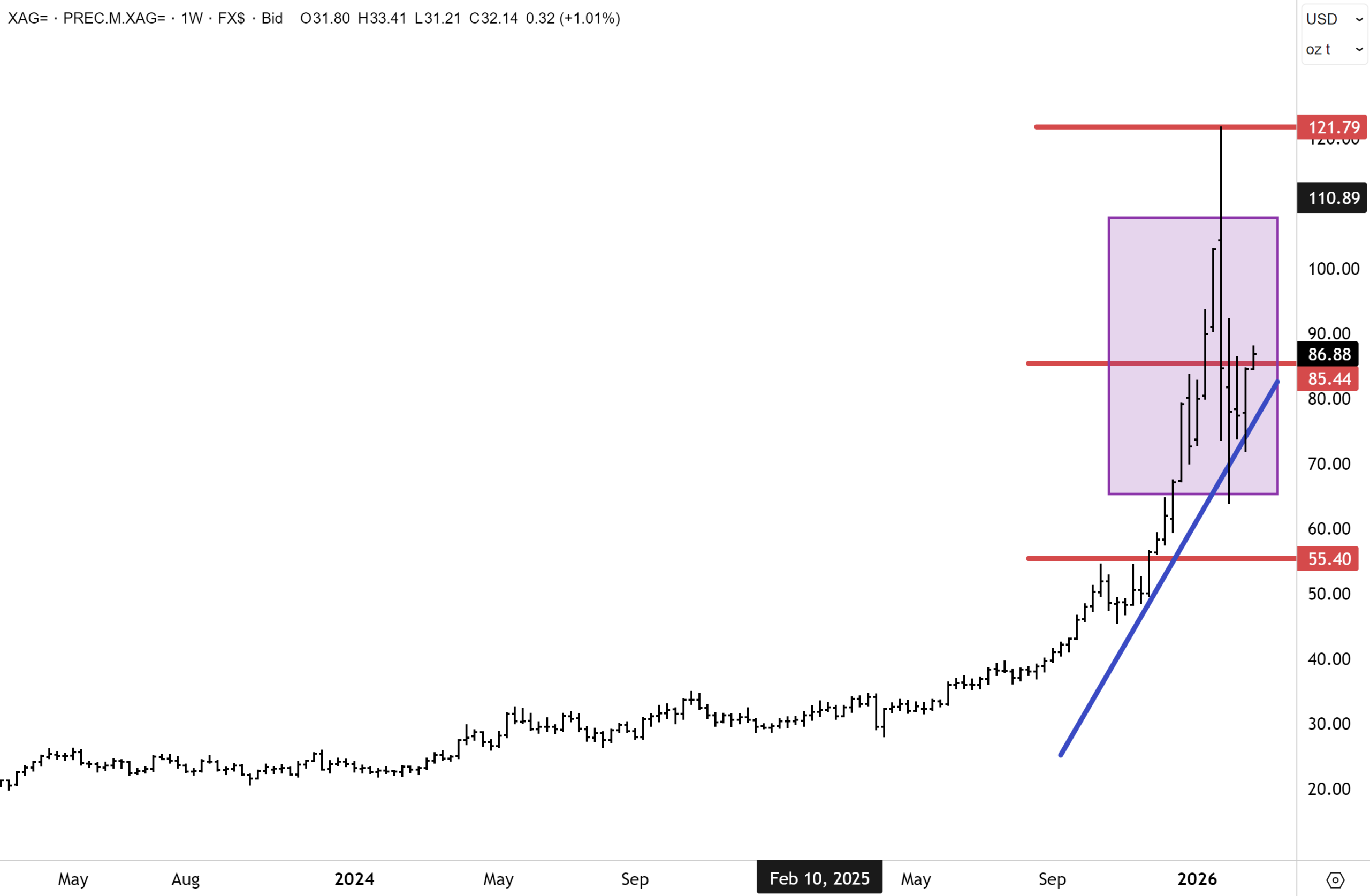

Gold momentum was positive, gaining more than +3% over the past week, trading near US$5,195/oz at the time of writing, while silver was up +13% to knock on the door of $89/oz. We provide a technical update on these below. Copper was up more than +4% for the week, trading around $6.01/lb, and this is providing powerful support for majors like BHP and Rio Tinto. Crude oil held steady with WTI trading around $65/bbl, anchored by an ongoing Middle East risk premium. As can be seen in the earlier chart, the Bloomberg Commodity Index (BCOM) is up a solid +8% YTD, which includes soft commodities. We are on record as calling for a substantial upcycle, particularly across the metals complex, in 2026.

Policy & Geopolitical Catalysts

Trade policy dominated the macroeconomic landscape. The US Supreme Court struck down prior emergency tariffs, prompting a brief 15% global tariff threat from the White House that ultimately settled at 10%. Trump amped up his rhetoric around Iran. Beijing imposed dual-use export bans on seven rare earth materials targeting Japanese defence entities. This strategic manoeuvre ignited critical minerals plays and highlighted China’s immense supply-chain leverage.

What to Watch

- Wholesale inflation drops on Friday morning, New York time.

- The closely-watched non-farm jobs report is due on March 6th

- Australian GDP data is due on March 4th

- The National People’s Congress opens on March 5th. Investors will look for clear fiscal stimulus signals from Beijing to keep the Chinese policy backdrop supportive.

- Chancellor Rachel Reeves will deliver the fiscal statement next Tuesday against a backdrop of softening domestic retail conditions.

The Takeaway: With tariff threats moderating and a softer dollar easing global liquidity, the fundamental backdrop favours a sustained allocation to broadening equity themes and structurally tight commodities.

Australia

The Australian market pushed deeper into record territory on Thursday as jitters around AI subsided and a run of stronger-than-expected earnings reinforced risk appetite. The benchmark ASX 200 gained +0.51% to 9,175, building on the prior session’s all-time closing high. An overall robust February reporting season, led by heavyweight miners and banks alongside consumer staples and energy names, has underpinned the ascent. Given the upward earnings revisions we are seeing across the commodities and banking complex and their heavy weight in the index composition, the benchmark appears poised for further gains in 2026, though don’t expect this to be linear; there will be ebbs and flows.

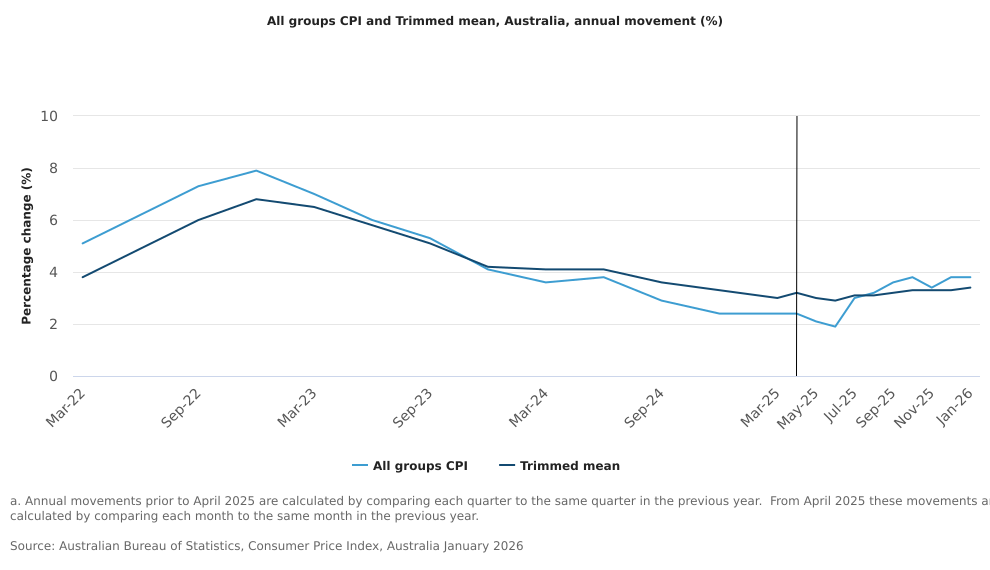

On Wednesday, investors shrugged aside the latest data, which showed that January CPI came in at 3.8% year-on-year, matching December but running above the 3.7% market forecast, while the trimmed mean underlying measure nudged to 3.4%, a tick above expectations and a step up after three consecutive months at the same pace. The latter is what the RBA focuses on, and the 3-year yield rose a few basis points to 4.27% after the data dropped. Meanwhile, markets are still only pricing in a modest 22% chance of another rate hike in March, though the odds for a hike in May rose to 82%.

Goods prices firmed as state electricity rebates expired, while services inflation eased to 3.9%. The figures leave inflation well above the RBA’s 2–3% target band and narrowed near-term rate cut expectations.

To recap, in early February, the RBA’s Monetary Policy Board unanimously raised the cash rate by 25bp to 3.85%, the first hike in more than two years. The hike reversed one of last year’s three cuts and came after inflation accelerated sharply in H2 2025, with elevated services costs and a tight labour market driving broad-based price pressures.

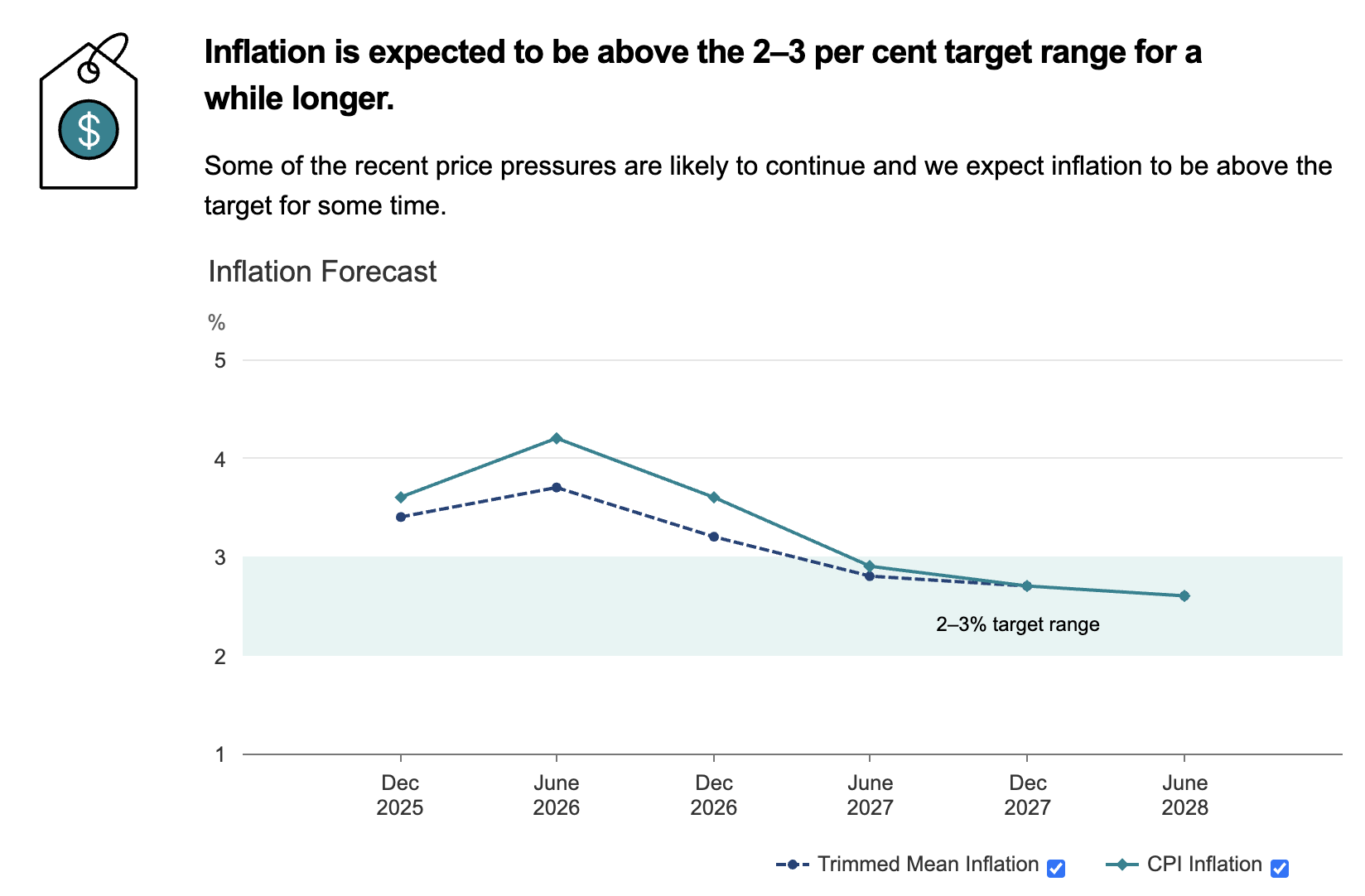

The RBA upgraded its inflation forecasts to be ‘materially higher,’ with the consumer price index now expected to rise above 4% by mid-year. It now expects trimmed mean inflation (the key figure to watch) to be 3.7% by June, up from a previous 3.2%, and 3.2% by December rather than 2.7%, with inflation not expected to return to the midpoint of the 2%–3% target band until mid-2028. If we don’t see some improvement in the coming months, this implies that at least one more rate rise is likely, and this week’s CPI data adds to that probability.

Source: RBA

The risk of another early rate hike in the first half of calendar 2026 has increased significantly, even as leading indicators point to a gradual cooling in broader consumer spending.

Over the past month, the Australian market has outperformed the US indices as local materials and banking stocks found renewed favour. Heavyweight miners like BHP and Rio Tinto benefited from firmer copper prices and a post-Lunar New Year pickup in Chinese demand. Even after a rebound over the past few days, tech was little changed for the week and down sharply over the past month as valuation multiples compressed on AI jitters. Many Australian tech stocks trade at higher multiples than American peers, despite inferior growth profiles, so there remain vulnerabilities here, alongside some pockets of opportunities emerging due to almost indiscriminate selling.

Reflecting the persistent inflation print and the hawkish RBA outlook, the Australian 10-year Government Bond yield climbed to 4.66% at the time of writing, its highest level in several months. This rise in yields has occurred even as US 10-year yields have fallen, creating a divergence that has fundamentally supported the Aussie dollar.

The AUD/USD cross soared to a high of 0.715 on Thursday, marking the highest level since June 2022, as the market priced in higher-for-longer interest rates in Australia compared to the easing expectations in other developed economies. The Australian Dollar has gained firmly over the past month, functioning as a primary vehicle for the “carry trade” as the yield differential widens. It may be time to book that overseas holiday.

Don’t forget your essentials!

Market Insights

Fiscal Dominance & The Liquidity Trap

Legendary hedge fund manager and multi-billionaire Stanley Druckenmiller was recently reported to have made some very interesting comments about the markets. I have great respect for Stan Druckenmiller’s views and, alongside George Soros, see him as one of the best market observers and investors of our time.

George Soros and Stan Druckenmiller, back in the day, during the 1990s, just after their hedge fund helped break the Bank of England. The pair heavily shorted the British pound to the point where the BOE ran out of reserves and could no longer defend it. The pound plummeted, and Soros reportedly made over $1 billion in a single day.

Key recent themes from Stan’s recent comments and positioning include a warning that the US is effectively in or near a “liquidity trap” for 2026, where fiscal dominance and structurally loose financial conditions mean the Fed cannot truly tighten enough to contain inflation without triggering a serious recession. Mr Druckenmiller continues to argue that the “post‑2020 inflation pattern looks uncomfortably similar to the 1970s”, and that the Fed risks having declared victory on inflation too early, with a renewed flare-up possible into 2027–28 if policy is eased too fast. I totally concur and have nothing to really add other than this is a core theme we have been running with for some time.

In terms of portfolio stance, he has highlighted energy (especially oil and large-cap US producers) as a core overweight, arguing that underinvestment in supply and ongoing demand will create a sizeable deficit later this decade, giving energy equities substantial upside. This is a non-consensus view with mainstream investment banks, and one that I share.

Stan is also bullish on commodities, and his positioning clusters around being structurally long energy, selected metals, including gold, and especially copper. In terms of energy (oil and gas) – he has repeatedly framed oil and gas as attractive because “years of under‑investment plus ongoing demand leave supply too tight, implying upside risk to prices; more recent “2026 strategy” content has him allocating a large sleeve of capital to energy producers, with an emphasis on “low‑cost, high‑quality names that still make money around 60 USD/bbl and generate significant free cash flow if crude trades in the 100–120 range.”

Oil prices may be down – but for how much longer? Despite near consensus amongst major investment banks and brokers, oil prices have not collapsed. The majority of brokers and banks expect oil to weaken significantly later this year, amidst a supply glut. The technical pattern and setup for WTI oil suggest quite the opposite in my view. A breakout above the primary trendline could mark an important inflection point for the oil market. Meanwhile, major diversified energy majors are doing much better this year, with some, including Exxon Mobil, notching up new record highs. This is bullish price action for the global sector – not bearish, and this is at odds with a bearish outlook on oil prices.

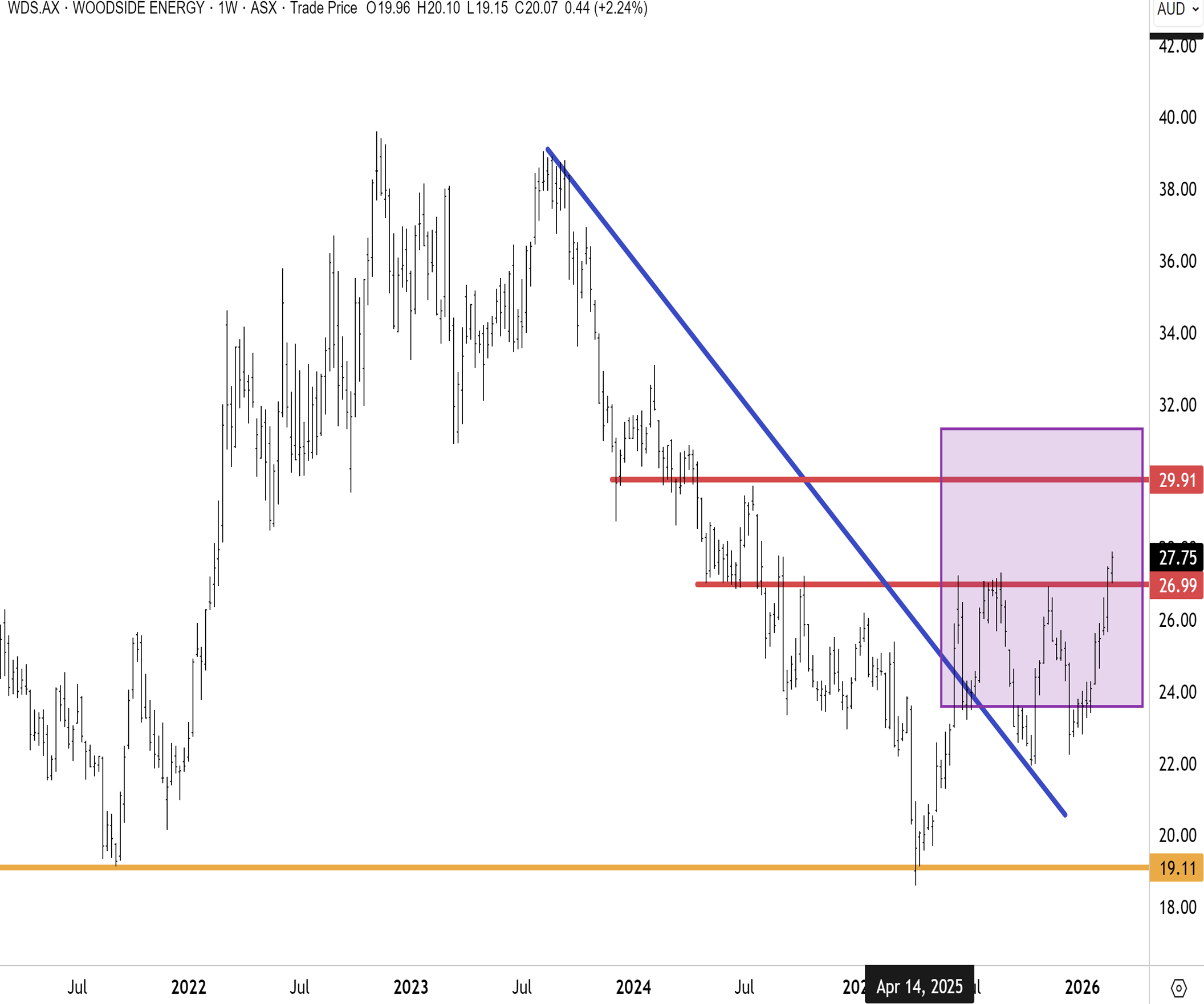

I believe Stan Druckenmiller will prove to be spot on here. We have maintained overweight positioning in Woodside and Santos in our Australian managed account portfolios for some time, and I expect both stocks to outperform this year, which will surprise most strategists and many fund managers. The sector has underperformed for the past few years, but I expect this to change in 2026.

In terms of copper and base metals – Mr Druckenmiller singled out copper as a “great bet” for the next five to six years, arguing that “EVs, grid upgrades, data centres and munitions will drive demand while 10‑plus‑year lead times for new mines keep supply constrained, so new record highs in copper are plausible over that horizon”; he has expressed that view via positions in names like Freeport‑McMoRan and, more recently, Alcoa for broader capex/commodity exposure. We hold a lot of BHP and other major copper producers in our portfolios.

In terms of gold, Stan believes that gold sits alongside T-bills and energy as a core asset, with an explicit thesis “that persistent fiscal issues and policy constraints could push gold materially higher into 2026, making it both an inflation hedge and defensive macro trade.” I can’t argue with Stan’s logic on this front. I have to read a lot of research reports daily, and I respect a lot of the work that many of the investment banks put out.

However, I place more weight on what some of the world’s leading hedge fund managers do, who are often positioning their portfolios at odds with what the consensus in the markets is doing. This year is shaping up to be an opportunistic one, and I believe large energy diversified majors are now looking ripe in terms of timing. In Australia, Woodside and Santos stand out in terms of valuations, being at a significant discount to global peers.

The commodity bull is reloaded

The Tariff Squall & USD Volatility

Constant shifts in US trade policy create a “constantly changing tariff landscape” that weakens confidence in dealing with the Trump administration. While the US Supreme Court’s annulment of emergency tariffs initially sparked optimism, the subsequent 15% blanket threat forced an initial defensive rotation. Paradoxically, this volatility is a tailwind for China. Morgan Stanley estimates Chinese levies could fall from 32% to 24%, the largest reduction of any country. As it turned out, the global blanket tariff was initially set at 10%, with the 15% figure getting no follow-up, which is a welcome outcome.

The renewed tariff drama pressured the USD and benefited gold and silver on Monday.

Gold has resumed upward momentum in recent trading sessions. The breakout on Monday above $5,200, if sustained, might point to the end of the correction that began for gold back in late January. This is a similar pattern to what occurred last October.

For silver, a similar pattern is also playing out. The recent breakout above $85 could also point to an end to the big correction that played out at the end of January. Silver needs to sustain the breakout and hold above this level, but technically, the price action this week has been encouraging. We can’t rule out the possibility of the next leg in the PGM bull market now being underway.

For silver, a similar pattern is also playing out. The recent breakout above $85 could also point to an end to the big correction that played out at the end of January. Silver needs to sustain the breakout and hold above this level, but technically, the price action this week has been encouraging. We can’t rule out the possibility of the next leg in the PGM bull market now being underway.

Eastbound

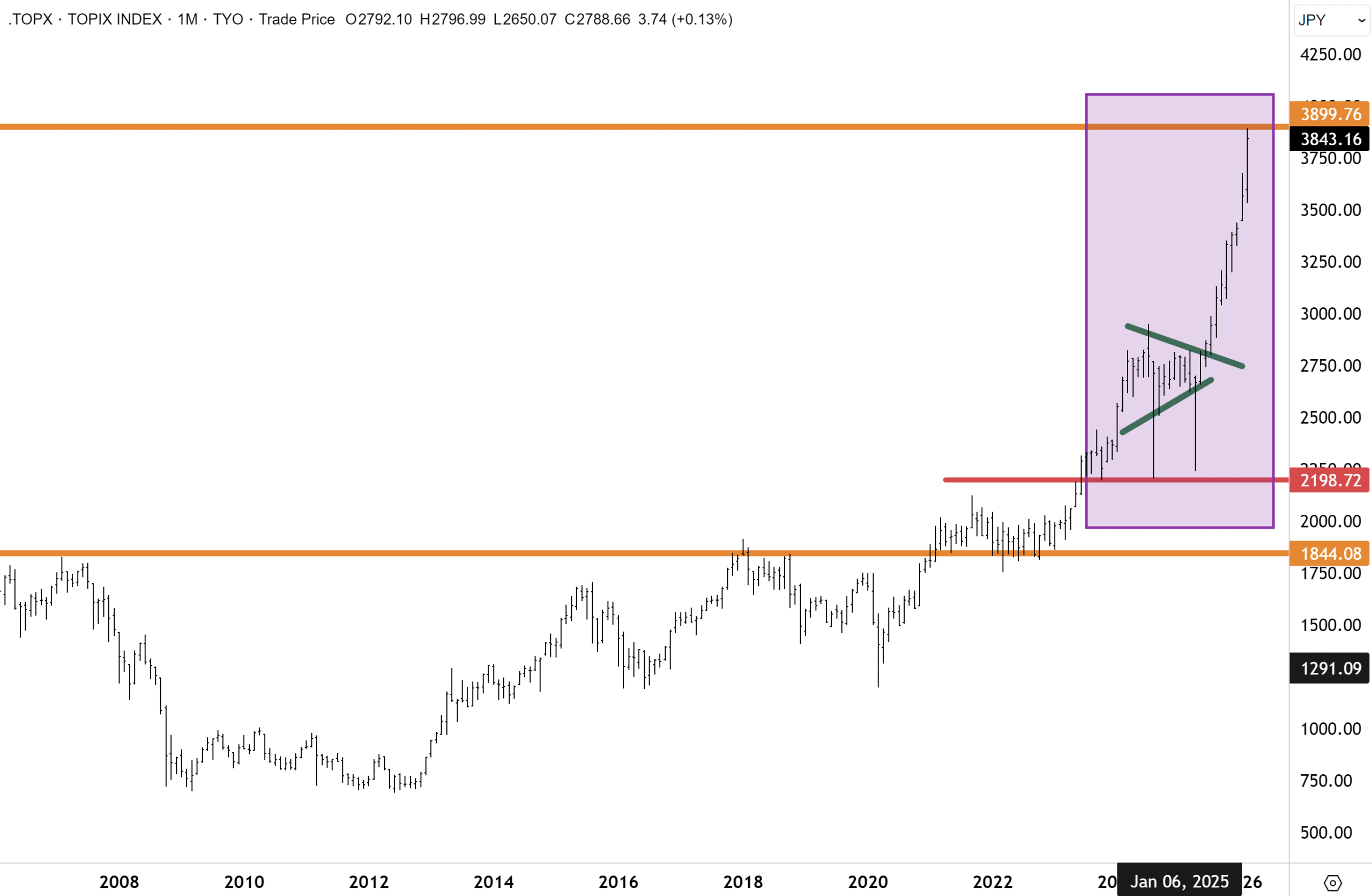

Whilst Japanese equities have been strong performers in recent years, Goldman Sachs wrote in a note this week that the bull market rally is not over and that further upside awaits following decades of lacklustre underperformance. The key Nikkei 225 has been regularly making new record highs since 2024, gaining 52% over the past 12 months alone, while the broader Topix index is up 12% this year and 41% over the past 12 months. I certainly concur with Goldman’s and hold the view that Japan’s stock market will continue to climb this year after nearly 30 years of crippling deflation.

Goldman also agrees and said this week that “we believe that we’re still very much in the upward phase of the current market cycle, and we think that market cycle started in the autumn of 2022.” One key driver this year has been the removal of political uncertainty with the landslide win by the Takaichi government. PM Ms Sanae Takaichi is pro-economic growth and will likely soon embark on fiscal stimulus.

Whilst putting near term risks of a correction aside, Goldman did highlight that the next phase of the bull market could be more challenging and hinges on whether Japan moves into a “delivery phase” — where policymakers and the corporate sector prove they can follow through on the expectations investors have built up.

“If that top-down pressure can align with what investors, both foreign and domestic, are trying to do from a bottom-up perspective in terms of engaging with management, then we think we could see a really interesting dynamic moving forward.” Corporate reforms have been very positively received by both domestic and international investors alike. Companies are unlocking lethargic and inefficient balance sheets and returning cash to shareholders, which is positively exerting higher returns on both investment and equity. I see this trend continuing for some time.

The TOPIX has surged this year to a new all-time record high of around 4,000. Correction risks are elevated near term, but the primary uptrend remains intact, and I expect the record highs to be retested (and likely taken out) over the course of this year. A correction, if one ensues, would be healthy and serve to remove froth from the market and reset overbought conditions.

A recovery in foreign investment into Japan is another reason Goldman sees room for the rally to continue.

After a sharp 24% peak-to-trough correction in the Topix following the massive sell-off in August 2024 that spooked many investors, a wave of foreign money is coming in again. According to Goldman, recent data shows 1.8 trillion Japanese yen in net buying in the week before the election — the second-highest weekly total on record.

And Japanese equities are under-owned amongst most international investors. Goldman noted that foreign positioning is not yet stretched. “Mutual funds remain underweight Japan, and foreign allocations are only back to levels seen at the start of 2012, when former Prime Minister Shinzo Abe’s policy agenda of aggressive monetary easing, fiscal stimulus, and structural reforms first sparked meaningful gains in Japanese equities.” For the rally to be sustained, investors need proof of improving corporate profitability and rising return on equity, which Goldman cited as a trend set to continue.

Another market I am bullish on this year is China. Deutsche Bank’s global CIO said this week in an interview that “China’s tech prowess is making the country an increasingly attractive investment destination.” And similar to Japan, most global investors are significantly underweight China.

DB highlighted that “Inflows into China equities are likely to rise this year, driven by investors in Southeast Asia and Europe. The weak dollar is also contributing to the shift as asset managers seek alternatives to US assets. We are optimistic about China as an investment location. It is no longer the extended workbench where companies go for cheap production. It’s the second-largest global AI hub after the US and has a leading role in industries like robotics and EVs.”

I think this year will see a rising tide of bullish optimism amongst global fund managers, many of whom just a few years ago considered China as “un-investible”.

In the past 20 years, the CSI300 has made several attempts at breaching the bubble highs above 5800 set nearly twenty years ago in 2007. I believe the CSI300 will make another run at those highs this year for multiple reasons, including an improving domestic economy, which is recovering after the housing market burst four years ago. Chinese companies sell for a fraction of the multiples that US stocks sell for. A weaker US dollar this year could further improve the liquidity backdrop for emerging markets, with China likely a major beneficiary.

Report Spotlight

A small selection from recent research updates. Log on to the website for more updates.

Woodside delivered record production of 198.8 million barrels of oil equivalent in FY25, yet the headline profit figure disappointed, with net profit falling 24% to US$2.72 billion as realised prices dropped 5% to around US$60/boe and higher taxes and one-off items weighed on the bottom line. Dig beneath the surface, however, and the operating picture is considerably more encouraging. EBITDA held flat at US$9.3 billion, operating cash flow surged 23% to US$7.2 billion, free cash flow swung from negative to US$1.9 billion, and unit production costs fell 4% to US$7.8/boe, reinforcing Woodside’s position on the lower half of the global LNG cost curve. The board maintained its generous payout, declaring a fully franked final dividend of US59 cents, taking the full-year distribution to US112 cents — 80% of underlying profit — while gearing remained conservative at 18-19% with liquidity of US$9.3 billion.

In 2025 and in our recent update on the 29th January, we maintained the conviction that for Woodside Energy, the capitulation lows were made last April at $19. Since our last update, Woodside has broken through important resistance around $27 and made a two-year high. We maintain our view that Woodside Energy has significant recovery potential ahead, now that an inflection is close to being confirmed. Despite near-consensual bearishness on oil prices, major global diversified energy stocks have outperformed this year. We are confident this trend will continue this year despite the still current pervasive gloom surrounding the energy sector. If Woodside can sustain the recent breakout, we have conviction that a minimum price target of $30 could be achieved this year. We hold Woodside Energy across our Australian-managed account portfolios.

The growth pipeline and low valuation underpin the investment thesis. Scarborough, the flagship Australian LNG expansion, was 94% complete at year-end with first cargo targeted for Q4 2026. Louisiana LNG is 22% complete with partners Stonepeak and Williams on board, cutting Woodside’s capital exposure to US$9.9 billion of the US$17.5 billion total. Trion, the Mexican deepwater oil project, is 50% complete and on track for first oil in 2028. Together, these three projects underpin a material step-change in production and cash generation capacity from late 2026 onward. For investors willing to look through near-term earnings softness and commodity price volatility, Woodside offers a compelling combination of high, well-covered dividends today and visible volume-driven cash flow growth ahead. BUY.

This report and many others spanning Australasia, Mining and Global Equities are available online for your reading pleasure in the Members area, should you be interested in subscribing for investment snapshots and deep dives across a range of investment vectors, along with our regular Daily correspondence on the markets.

Have a great weekend

Carpe Diem

Angus

Sign up to receive full reports for

the best stocks in 2026!

Where to Invest in 2026?

The market is full of opportunities—but which stocks will deliver real wealth-building potential?

At Fat Prophets, our expert analysts uncover the best Australian and global stocks to help you stay ahead of the curve. Whether you’re looking for growth, income, or diversification, our carefully curated portfolio gives you access to high-conviction stock recommendations backed by deep research and proven insights.

Subscribe now to get full reports of these stocks and get ready for the next big opportunities!

Over 25,000 customers worldwide

Need a try? You’re first-time customer?

Enjoy our Welcome Gift with $500 OFF your Membership

Use code: FPWELCOME

FAQ’s

How much does a Membership cost?

We have a number of Membership options for the DIY investor. Our research services cover individual stock opportunities in Australia, as well as the UK, global markets, and a sector-specific report focussing on the mining space. Annual Membership prices start at $1395.

Do you offer execution services?

No we do not, and our research is independent in the sense that we are not conflicted by operating broking services alongside them. We also do not offer ‘sponsored research’ and are not financially incentivised by any of the companies that we recommend to Members.

Can I access any special offers?

Our introductory joining offers relate only to new Members. We do however offer ‘early bird’ discounts to existing Members who renew in advance of their Membership expiring.

Can I get tailored financial advice?

Our research products are ‘general advice’ in nature only, however we do categorise all our recommendations by the level of risk appetite which we believe is involved. Members looking for more direct advice can also make an inquiry to our wealth management team which offers a separately managed accounts service.

Do you offer a Money-Back guarantee?

Yes we do. Fat Prophets offers a 100% money back guarantee on annual subscriptions within 30 days of taking out a Membership.